Earlier this month, the SEC sued Rio Tinto (RIO), Tom Albanese (Rio’s ex-CEO) and Guy Elliott (Rio’s ex-CFO) on alleged fraud related to the acquisition of Riversdale Resources in 2011 and keeping the subsequent impairments hidden from Rio’s board of Directors and investors in the company.

In 2011, Rio Tinto acquired Riversdale Resources, an ASX-listed company focusing on developing its 13 billion tonnes coal project in Mozambique. As Rio wanted to increase its exposure to the coal sector, it spent $3.8B to acquire Riversdale only to find out less than a year later the assets were virtually worthless and would have a negative NPV if they would be developed.

Not only was the due diligence flawed, looking at the SEC claim, it also appears the warning signs provided by ‘the people on the ground’ were ignored by the CEO and CFO when they presented the case to the board of directors. It was only when a member of the Rio Tinto Technology & Innovation Group bypassed the CEO and CFO and directly reported his findings to the Chairman of the board, the true size of the mess was revealed.

You can read the entire 60 page document by clicking on the link here below. It’s a relatively long document, but it reads like a thriller and we have highlighted some parts below the link-button.

If there’s anything you need to take away from this, it’s that ‘healthy scepticism’ is a good thing in this sector. Whether it’s a small junior exploration company or a large mammoth company, it’s always a good idea to double-check statements and expectations.

Click here to read the entire SEC document

- After the acquisition, the business, now called Rio Tinto Coal Mozambique (“RTCM”), began to suffer one setback after another. By November 2011, Rio Tinto had determined that its barging assumptions were unrealistic. In December 2011, the Government of Mozambique rejected Rio Tinto’s proposal to barge coal down the Zambezi River. Rio Tinto also learned that existing railway capacity was severely limited. As a result, by the end of 2011, Rio Tinto knew that it could transport and sell only about five percent of the amount of coal it had originally assumed. Rio Tinto also learned that there was significantly less and lower quality coal than it had assumed at acquisition.

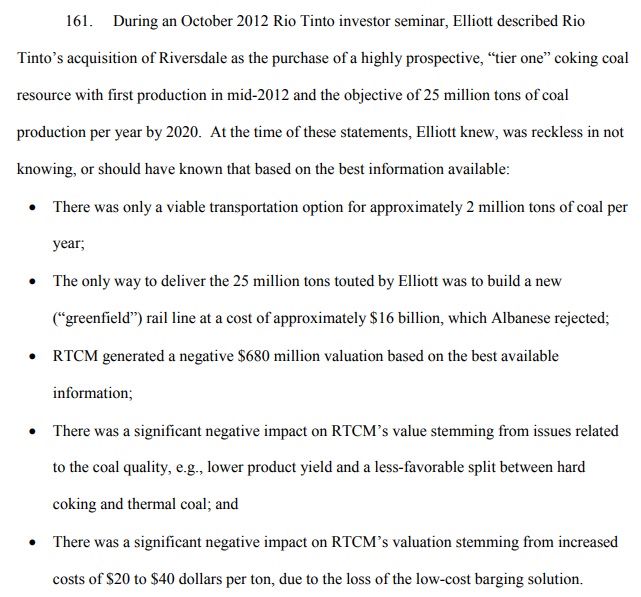

- In contrast to the risks described by Rio Tinto’s in-house experts and known to Albanese and Elliott, Defendants consistently described Riversdale as a significant opportunity—a “tier one” asset—with numerous transportation options that it could develop quickly into a project producing 45 million tons of coal per year. In Rio Tinto parlance, “tier one” referred to “what others might call ‘company maker’ deposits . . . that contribute disproportionately to global production of a commodity due to their size and character.”

- Albanese and Elliott learned that the Mozambique Government had rejected RTCM’s barging proposal in December 2011 and January 2012, respectively. Rio Tinto never formally submitted a revised or updated barging proposal, and by April 2012, it had been warned by the Government of Mozambique that, if it persisted in raising the subject of barging, it risked losing its mining licenses altogether.

- At the time of acquisition, Rio Tinto assumed that between 12 and 15 million tons of coal per year could be shipped by rail from the coal tenements in the Moatize Basin to a port on the Indian Ocean. But within a few months, the company came to understand that the existing rail line had a maximum capacity of six million tons of coal per year, and that only 32 percent of that capacity, i.e., a little less than two million tons, would be available to Rio Tinto on a shared basis.

- At acquisition, Rio Tinto expected that RTCM would be cheaply transporting and selling more than 40 million tons of coal per year; a few months later, it realized that it had less than five percent of the assumed transportation capacity—and could thus sell less than five percent as much coal as anticipated at the time of acquisition.

- By January 2012, as RTCM evaluated the potential resources post acquisition, it determined that they would in fact have to be written down by closer to 80 percent, to less than three billion tons—a substantially greater write-down than had been anticipated at the time of acquisition

- Between late 2011 and early 2012, RTCM created a ground-up valuation model that, when completed, generated valuations ranging from approximately negative $3.45 billion to approximately negative $9 billion. […]Even those negative valuations rested on aggressive assumptions. The negative valuations assumed that a largely-untested coal tenement called “Minjova” would contribute hundreds of millions of tons of coal production to the overall project.

And to sum it all up:

The author has no position in Rio Tinto. Please read the disclaimer