Columbus Gold’s (CGT.TO) partner Nord Gold completed a Bankable Feasibility Study on the Montagne D’Or Gold project in French Guiana at the end of April. This study confirms the viability of the gold project even at $1200 gold (and lower), and as Columbus Gold has now also announced plans to spin-out its Nevada assets into a new company, this is a good moment to review Columbus’ recent achievements.

Reviewing the results of the feasibility study

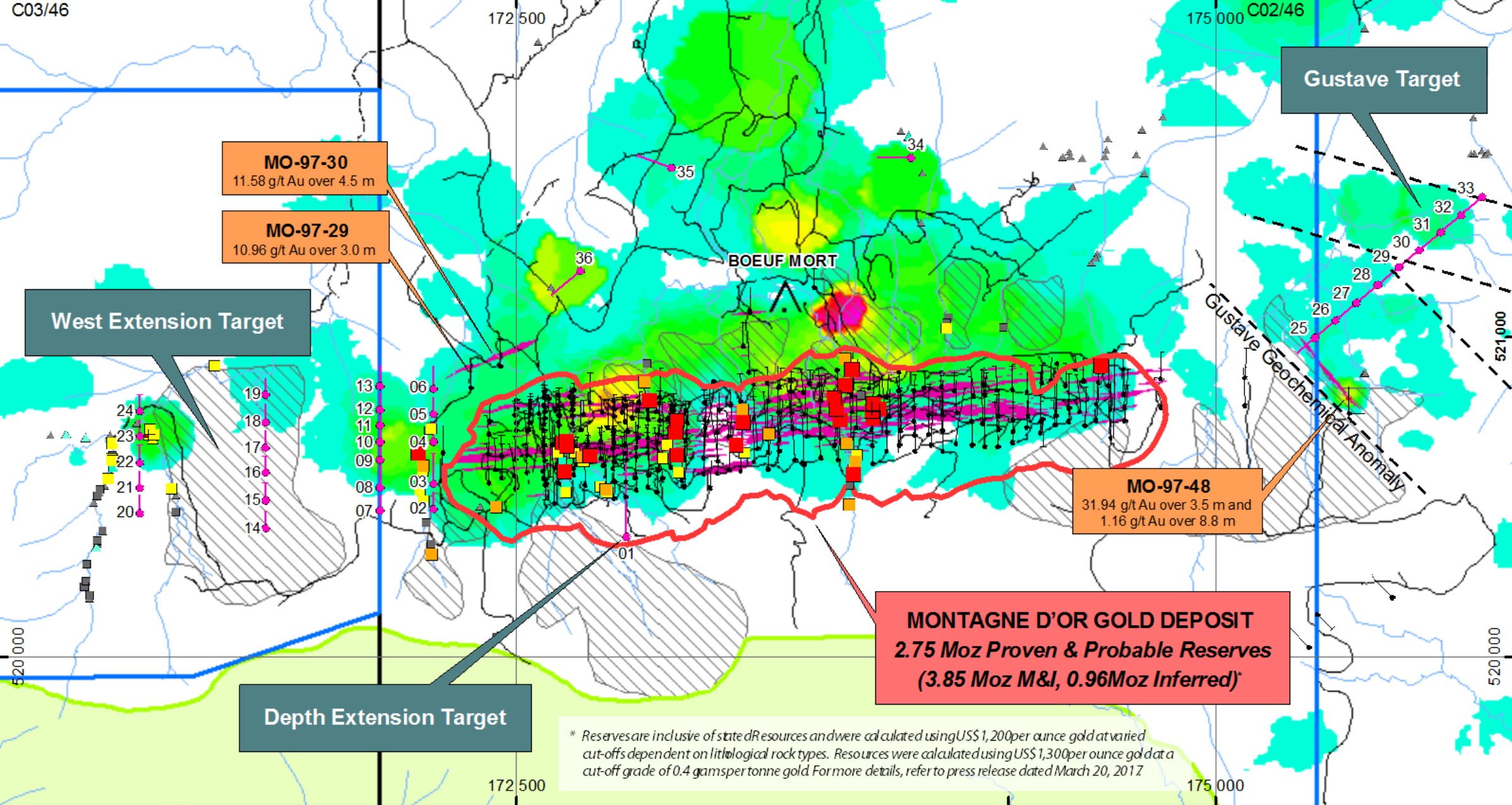

We have been keeping track of Columbus Gold for several years now so we won’t bore you with the history and the location of the Montagne D’Or gold project in French Guiana. After accepting Nord Gold as a joint venture partner, both companies have put the pedal to the metal which resulted in the completion of a bankable feasibility study.

This study was based on a total reserve estimate of 2.75 million ounces of gold and will see the Montagne D’Or mine produce an average annual production of 237,000 ounces of gold in the first 10 years of the 12 year mine life. The cash cost is anticipated to be $666/oz with the all-in sustaining cost coming in at less than $750/oz. The initial capex has been estimated at $535M resulting in a net expenditure of $361M after taking $174M in tax credit refunds into consideration.

A capital intensity of $1,500 per ounce of annual production is very reasonable, and this allowed the company’s independent consultants to calculate an after-tax NPV5% of $370M and an after-tax IRR of 18.7%.

Whilst that’s ‘okay’ for a large project (keep in mind the total resources at Montagne D’Or contain 4.8 million ounces of gold with the potential to add more gold to the resources and reserves, so the mine plan based on the 2.75 million ounces should be seen as just the starting point. As less than 60% of the total resources have been incorporated in the mine plan, we are extremely confident Montagne D’Or will produce much more gold than the 2.57 million ounces in the mine plan.

For starters, the company is not allowed to use a single ounce of the inferred category in the mine plan, even though Columbus’ entire 960,000 ounce inferred resource is located within the planned resource pit shell. We would expect that a simple drill program would allow Columbus Gold and Nord Gold to upgrade a substantial part of these ounces into the measured and indicated category where after they could be incorporated in an updated mine plan. This would actually have a double positive impact; not only would the mine life increase by several years, converting ‘waste’ to reserves will reduce the amount of waste that will have to be hauled out of the pit.

Columbus and Nord Gold are considering an infill drill program which would allow the partners to upgrade a substantial part of that 960,000 ounces to the measured and indicated status. The impact of an upgrade should not be underestimated. Assuming an AISC of $800/oz of the ‘upgraded’ ounces, a conversion of 500,000 ounces would result in an undiscounted pre-tax cash flow of US$200M at $1200 gold. And this could be just the start, as Columbus Gold is also exploring on two potential targets along strike to the west and east of Montagne D’Or. Adding 2 years to the mine life using a gold price of $1250/oz would – according to our calculations based on the official economic model – add US$130-140M to the after-tax NPV5%.

Adding ounces definitely equals adding value and we have very little doubt Montagne D’Or will still be producing gold well after its initial 12 year mine life. As we mentioned before; whereas a feasibility usually is an end point for most companies, it’s merely a starting point for Columbus Gold and its partner Nord Gold.

But of course, we can’t also be blind for the ‘risks’ here. First of all, a discount rate of 5% might be a bit optimistic and it’s too bad the company hasn’t provided a NPV calculation using a discount rate of 7% or 8% (as the next step, a 10% discount rate, is too high. After all, even though French Guiana is located on the South American continent, the geopolitical risk isn’t higher than in mainland France).

A second ‘issue’ might be more important. The results of the feasibility study were based on an EUR/USD exchange rate of 1.05. In the past few weeks and months, the Euro has (re-) gained a lot of strength and momentum versus the US Dollar and is currently trading at approximately 1.15.

Whilst that’s great for European consumers trying to buy USD-priced goods, Columbus’ situation is the exact opposite as it will need more Dollars to convert to Euro’s to end up with the same Euro-amount. Using an exchange rate of 1.16 would result in an after-tax NPV5% of $235M which is approximately $135M lower compared to the base case scenario. Shareholders of Columbus Gold should actually be cheering for a stronger Dollar as a weaker Euro would boost the economics of the project (in USD).

What’s next for Montagne D’Or and French Guiana?

Columbus Gold has started a regional exploration program around the planned open pit at Montagne D’Or and we expect the company to release assay results shortly. This will tell us a lot about the potential western and eastern extensions of the open pit, and the potential to add more ounces to the resources and the mine plan.

Columbus and Nord Gold will also have to agree on an exploration plan. Both companies are about to enter into a 44.99-55.01% joint-venture, and Columbus Gold will have to sign off on the annual programs. As far as we know, no joint follow-up exploration programs have been announced yet, and it’s also something we’re looking forward to hear more about.

We were also relieved to see Emmanuel Macron being the new president of the French Republic. Not only is he obviously a better choice than an far-left or far-right opponent, he actually has first-hand experience with the Montagne D’Or project as he has toured the property in 2015 in his capacity as Minister of Economy. You can read the newspaper articles and a brief TV report about this visit on Columbus’ website.

One newspaper has interviewed Macron asking him if he believed if Columbus’ project would be a good example of a renewed interest in the French mining sector, to which Macron responded with “Yes!” (including the exclamation mark), followed by “yes, you could say France will open new mines” later in the interview.

Needless to say we are very encouraged by these words as it will undoubtedly make it easier for Columbus Gold to secure the necessary approvals.

Columbus Gold will spin its Nevada assets out to create more shareholder value

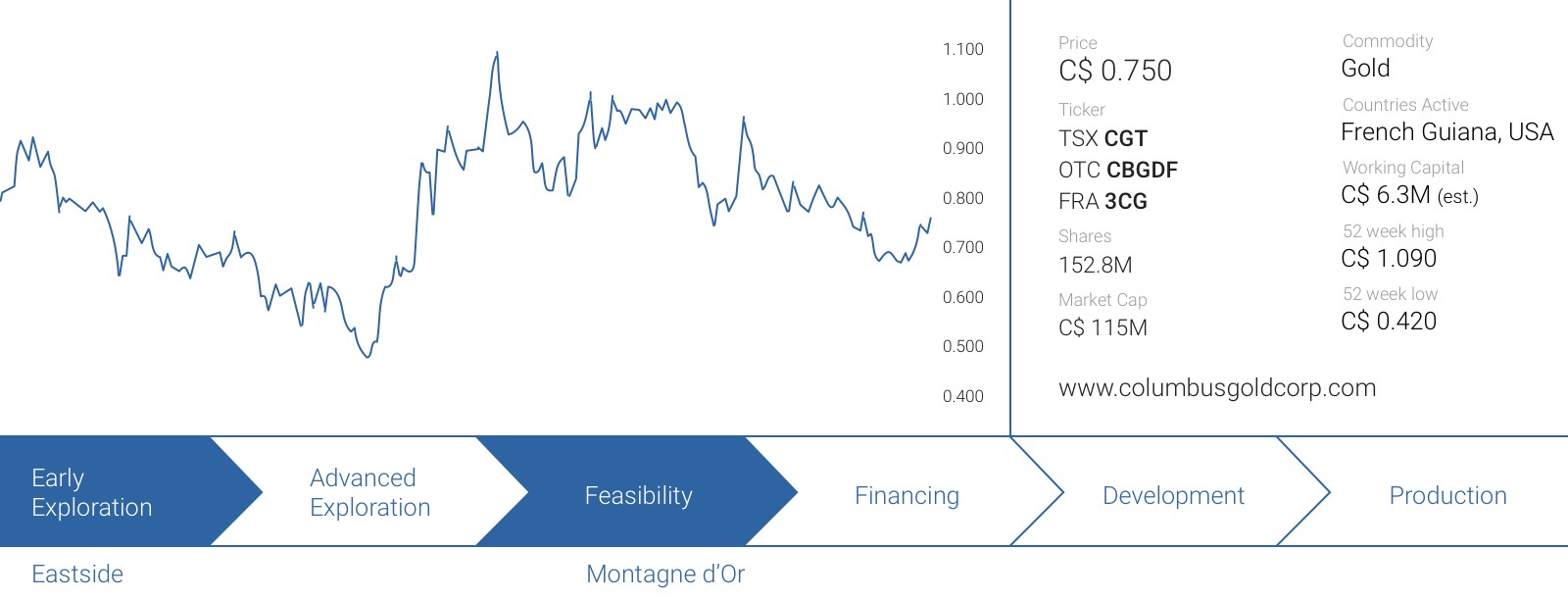

As Columbus’ current market capitalization of C$113M already is substantially lower than the value of its stake in Montagne D’Or, the Nevada properties are basically being thrown in for free as the company doesn’t seem to be getting any value for them.

This will change after the summer as Columbus Gold is in an advanced stage of its plan to unlock this hidden value for its shareholders. The company will spin its Nevada assets out in a new entity which will be called Allegiant Gold and will be listed on the TSX Venture Exchange as a separate entity.

Columbus Gold plans to share more details when it sends out its management information circular, but based on our talks with CEO Robert Giustra in Vancouver in the past few weeks we have the impression Columbus will opt for a three-part structure whereby the CGT shareholders will receive a substantial part of Allegiant Gold whilst Columbus Gold will retain a minority position as well.

On top of that, Columbus Gold will want to make sure Allegiant will be well-capitalized to aggressively explore its Nevada properties, so the spin-out will very likely be accompanied by a substantial capital raise as well.

We’ll know more once the detailed plans will be unveiled but we expect Columbus Gold to aim for a valuation of C$25-40M based on the number of projects, the safe jurisdiction and the advanced stage of Eastside where Columbus has confirmed a maiden inferred in-pit resource estimate of 654,000 ounces of gold and acquired claims with a historical resource containing an additional 272,000 ounces.

We believe spinning off the Nevada assets in a separate entity is probably the best decision as;

- It will unlock currently ‘hidden’ value

- It will allow Columbus Gold to spend the cash on its own balance sheet to advance the Montagne D’Or flagship project in French Guiana

- It will keep the ‘Columbus Gold’ entity ‘clean’ in case the company pursues a M&A-based exit strategy for its 44.99% stake in Montagne D’Or. Most shareholders would prefer an outright company sale versus an asset sale, and slimming down the CGT asset portfolio to just Montagne D’Or will simplify things.

The current financial status

As of at the end of March, Columbus Gold had a working capital deficit of approximately C$2.6M. Before you start to feel nervous, this was entirely due to Columbus having added the sale of Nord Gold’s stake in Montagne D’Or as a current liability. This is purely an accounting measure as there will obviously no cash outflow related to the effective sale of the stake.

Excluding this, Columbus’ net working capital position would have been approximately C$5.4M, with in excess of C$6.5M in cash. The cash position will obviously have decreased since March, but we expect Columbus to have ended Q2 with a comfortable cash position.

Conclusion

Columbus Gold has ticked all the boxes and now owns 44.99% of Montagne D’Or with a bankable feasibility study in its hands. We strongly believe this is just the start as the potential to add more ounces to the mine plan is sky-high. Even if we would use the current euro-dollar exchange rate and a slightly lower gold price ($1250 vs $1260), the NPV per share of Columbus Gold would still be C$0.86, without taking anything else into consideration.

That’s also why Columbus will spin out its Nevada assets in a separate entity. We believe that in this case, 1 + 1 will equal 3 as the market will give the Nevada assets a higher value on a standalone basis versus the current perception of the asset portfolio being ‘secondary’ to Montagne D’Or.

And just to show you how fast things can change; using an EUR/USD exchange rate of 1.05 and a gold price of $1400/oz (which we don’t think is an outrageous assumption), the NPV/share for Columbus Gold increases to approximately C$2 (post-tax but pre-dilution). Montagne D’Or is a great asset and whilst it will take some time to fully develop it (if no buyer comes along), it sure looks like it will be a mine one day. And it will be a mine which will produce more than the 2.57 million ounces in the current mine plan. That’s almost a guarantee.

The author has a long position in Columbus Gold. The company is a sponsor of this website. Please read the disclaimer