Bluestone Resources (BSR.V) is still very successful in its attempts to convert as much of the resources into reserves as possible, and the ongoing drill program continues to confirm the presence of high-grade gold (and silver) mineralization at Cerro Blanco. The assay results of three more holes were released and with 3.3 meters of 14.05 g/t gold and almost 46 g/t silver starting at a depth of just 69.4 meters as well as several narrower intervals such as 1 meter of 24.3 g/t gold and 2.3 meters containing 25.4 g/t gold (with a really nice silver kicker of almost 8 ounces of silver per tonne of rock), it’s clear the drill program is quite successful.

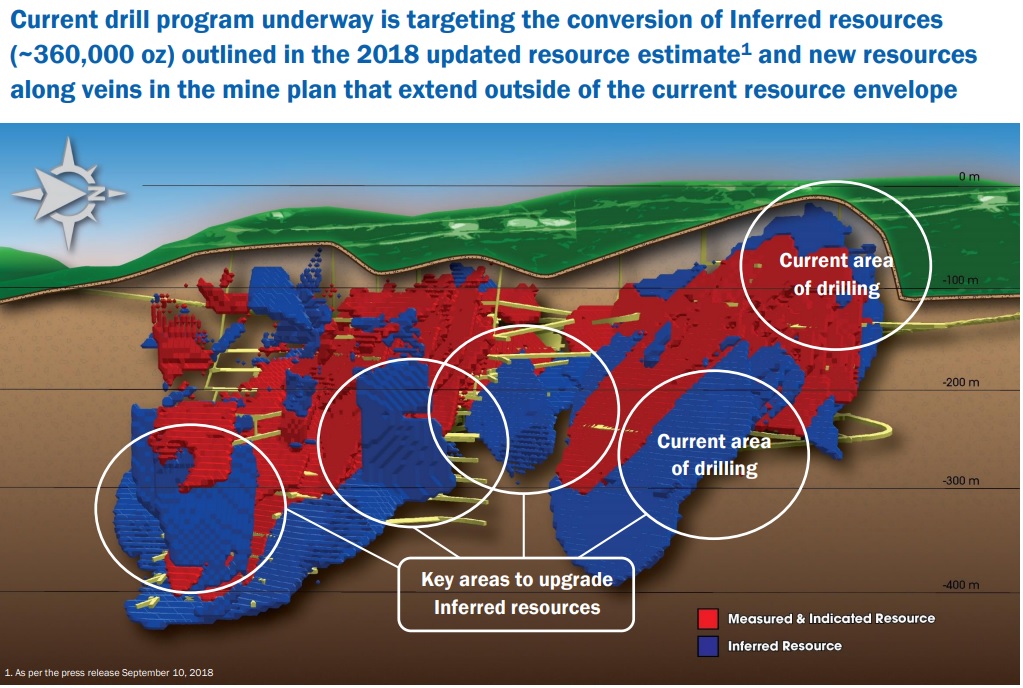

The average width and grades of the holes remains very consistent with the management expectations, and should further increase the confidence in the resource and reserve estimate at Cerro Blanco. Although these drill results could convert additional resources into reserves, these potential new reserves haven’t ended up in the feasibility study, which was completed earlier this week. Considering the high-grade nature of the project (1.2 million ounces at 10.1 g/t gold in the measured and indicated category as well as 360,000 ounces at 8.1 g/t in the inferred resource category), the project appears to be technically very sound, but Bluestone will continue to have to fight the negative perception surrounding Guatemala these days.

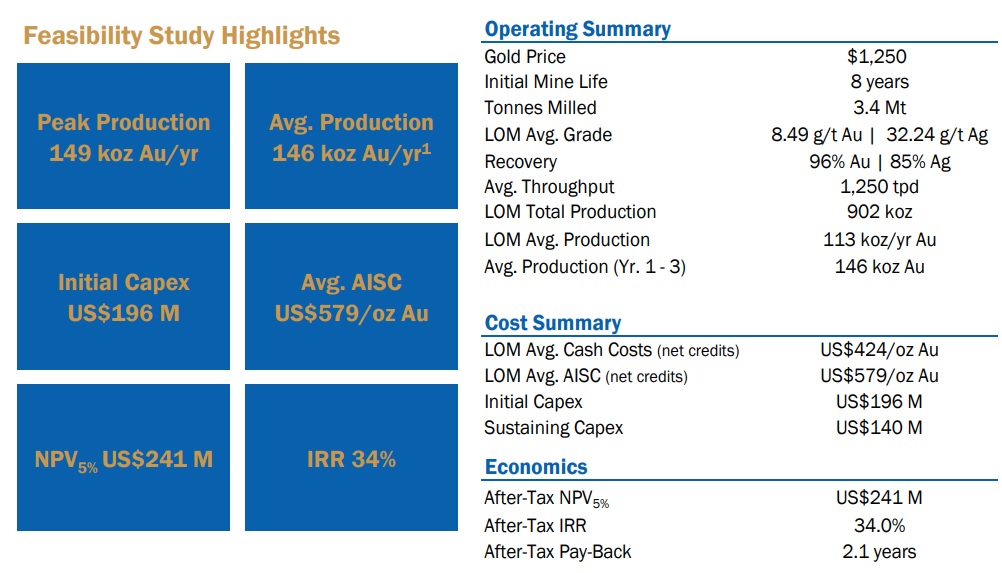

The feasibility study might help. The full report still has to be filed on SEDAR, but the preliminary press release is quite positive. Based on a total proven and probable reserve of 940,000 ounces of gold (at 8.5 g/t and 32.2 g/t silver), the project is expected to generate an after-tax NPV of US$241M (using $1250 gold and $18 silver). Unfortunately Bluestone has used a discount rate of just 5% for this project, and we think this is way too low to incorporate the risks of doing business in Guatemala. Additionally, we would be very surprised to see Bluestone securing debt funding at a cost below 5% which strengthens our view a discount rate of 8-10% should have been used. We still expect Bluestone to sell the property/company before making a construction decision, but we would have expected to see at least a sensitivity analysis showing how the NPV changes by using a higher discount rate.

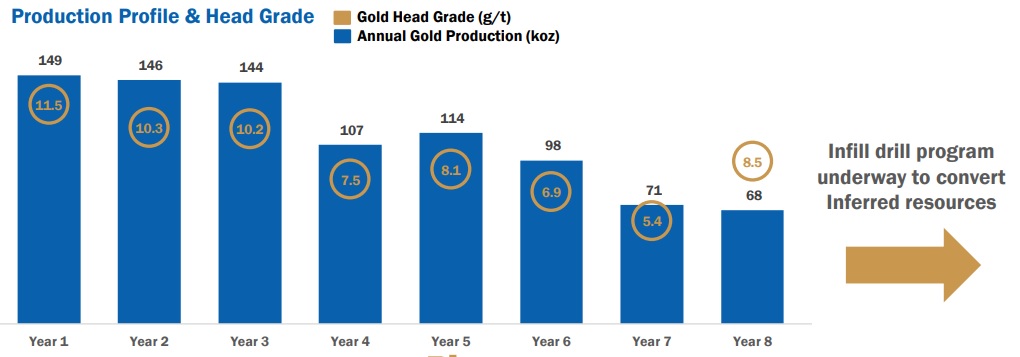

The mine plan calls for a throughput of 1,250 tonnes per day which should result in an average gold production of 113,000 ounces per year, with an average production rate of 146,000 ounces per year in the first three years of the mine life (which obviously boosts the NPV and IRR). The initial capex is estimated at US$196M, and after including the expected $140M in sustaining capex, the AISC per produced ounce of gold is approximately US$579/oz, confirming the healthy margins of the Cerro Blanco project. Using a gold price of $1300/oz, the after-tax NPV5% would increase to US$271M while the Internal Rate of Return would increase to 37%.

With in excess of 350,000 ounces of gold excluded from the reserves and mine plan, there’s additional upside potential at Cerro Blanco, and an extended mine life could reduce the impact of a higher discount rate on the Net Present Value of the project.

Go to Bluestone’s website

The author has no position in Bluestone Resources. Please read the disclaimer