Canyon Resources (CAY.AX) has released the results of a scoping study it conducted on the Minim Martap bauxite project in Cameroon where it’s planning/hoping to bring the large 892 million tonne bauxite project into production. The 892 million tonnes have an average grade of 45.1% Al2O3but there also is a higher grade core zone of 431 million tonnes at 48.8% Al2O3 and some distinct zones where the grade exceeds 50%.

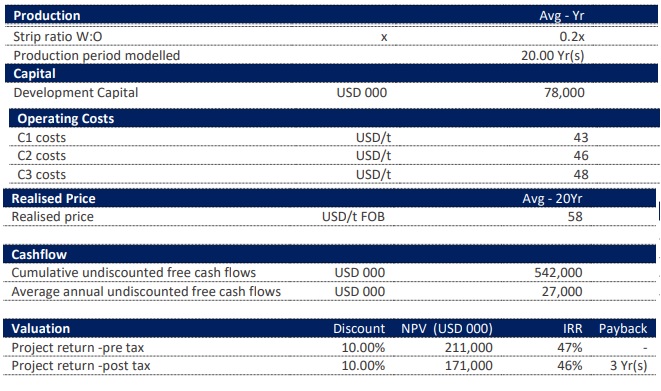

The scoping study appears to be very much ‘back of the envelope’ and will have to be confirmed by the pre-feasibility study which should be ready in the next few months. The study is eyeing a 3 million tonne per year operation that could be built for a capex of US$78M and result in a production of 49.9% material at a C1 cost of US$43/t and a C3 cost of US$48/t. Canyon anticipates a sales price of US$58/t FOB Douala and an average annual free cash flow of US$27M or US$9/t. Over the eyed initial 20 year mine life, this should result in an after-tax NPV10% of US$171% and an Internal Rate of Return of around 46%. Canyon expects to be in a position to commence construction in 2022 which should result in commercial production in 2023.

With a C3 cost of US$48/t and an anticipated sales price of US$58/t, this will be a low-margin operation and we would first like to see how Canyon got to the anticipated sales price of $58/t before we get too excited considering the Bauxite Index is currently priced in the low-$50 per dry metric tonne – although the benchmark price is based on a lower aluminum content per tonne. The concept of producing DSO Bauxite makes sense but we need to make sure the economics make sense as well. The Stage 2 study could benefit the project as the operating expenses could be reduced due to the inclusion of the Kribi deepwater port which should allow Canyon to reduce the production cost.

Disclosure: The author has no position in Canyon Resources.