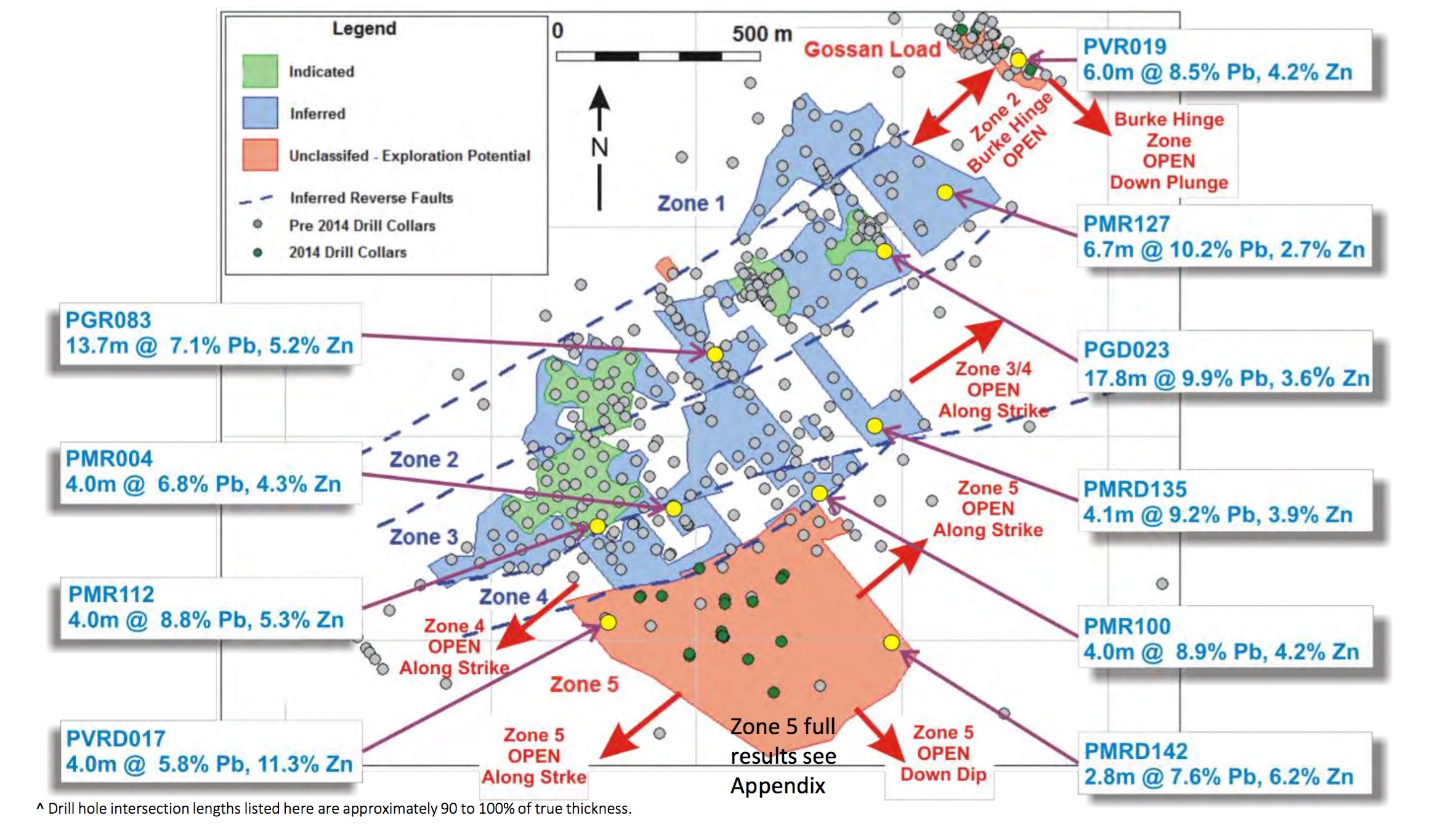

Vendetta Mining (VTT.V) has now finally released an updated resource estimate on its Pegmont lead-zinc project, and whereas we were aiming to see 7-8 million tonnes of sulphide in the resource, Vendetta outperformed our expectations with a total resource estimate of 11.9 million tonnes, of which 10.2 million tonnes were catalogued as sulphides with an additional 1.7 million tonnes of transitional rock.

It’s perfectly acceptable to include the transitional rock in the resource estimate because even though the recovery rate of the transition zone is just 19.3% for zinc, a very acceptable 80.5% of the lead could be recovered which makes it a no-brainer to process the rock anyway. Using the company’s first-pass recovery rates, the 1.7 million tonnes in the transition zone will result in the recovery of 160 million pounds of lead and 20 million pounds of zinc for an additional gross recoverable value of US$190M or US$112/t (before taking payabilities and operating expenses into account).

We are also surprised to see 8.3 million of the total tonnage is contained in a pit-constrained zone which will make it really cheap to mine. No strip ratios have been shared (we believe the strip ratio to be high but reasonable relative to the high rock value), but by using a pit slope of 55% and a pit outline using $0.90 lead and $0.95 zinc, the pit outline seems conservative to us. Open pit mining will be very cheap and based on the recovery rates for the sulphide zone, the recoverable value per tonne of open pit sulphide rock (assuming no silver will be recovered/payable) will be US$155/t (with a payable value of US$140/t using the current spot price for lead and zinc) thanks to the high recovery rates for the lead mineralization. Open pit mining will only cost you a fraction of this, resulting in superior returns and a payback ratio of very likely less than one year (a 1Mt operation at the average grades and recovery rates provided by Vendetta Mining and a high single-digit strip ratio will result in a pre-tax and pre-royalty operating cash flow of approximately US$75-85M (with a 10% margin of safety depending on the strip ratio) should Vendetta use one of the available mills in the region.

Not only is the resource estimate much larger than we expected, more of those tonnes could be mined via an open pit making the economics super-appealing as it will speed up the permitting process allowing Vendetta to start mining the open pits whilst completing the permitting process for the underground part of the mine plan. And finally, whereas Vendetta’s management team was aiming to ‘pick the best 10 million tonnes from a 15 million tonne resource estimate’, we now feel comfortable to say Pegmont hosts more than the originally eyed 15 million tonnes.

With this resource estimate, Vendetta can now focus on increasing the average grade of the deposit and to fine-tune its metallurgical test work, but it now appears Pegmont is shaping up to be large enough to be developed as a standalone operation although using one of the nearby mills (either South32’s (ASX:S32, S32.L) Cannington mill or the Chinova mill) will obviously result in even better ROI’s.

Go to Vendetta’s website

The author has a long position in Vendetta Mining. Vendetta is a sponsor of the website. Please read the disclaimer