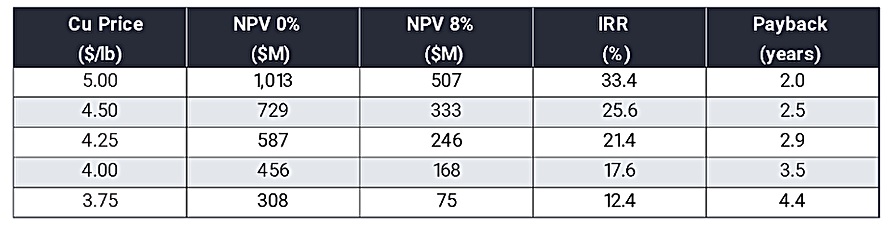

Highland Copper (HI.V) released the results of its updated feasibility study on the fully-permitted flagship Copperwood copper project in Michigan. As expected, the economics of the project are strongly correlated to the copper price as the project likely won’t generate a positive NPV at $3.50 copper but ends up with an after-tax NPV8% of almost US$250M at a copper price of US$4.25.

The relatively low NPV and IRR is caused by the high initial capex of approximately US$391M (and even closer to US$450M if you’d exclude the anticipated pre-production revenue of US$34M). The mine will produce approximately 65 million pounds of copper and just over 100,000 ounces of silver per year over an initial 11 year mine life at an operating cost of US$1.83 per pound.

With an after-tax IRR of less than 18% at $4 copper it won’t be easy to attract funding to actually build this project but Copperwood is one of those projects offering an interesting call option on the copper price. At US$4 copper it’s unlikely the project will make any money for Highland’s shareholders but at a copper price of $5 per pound, the after-tax NPV8% exceeds US$500M.

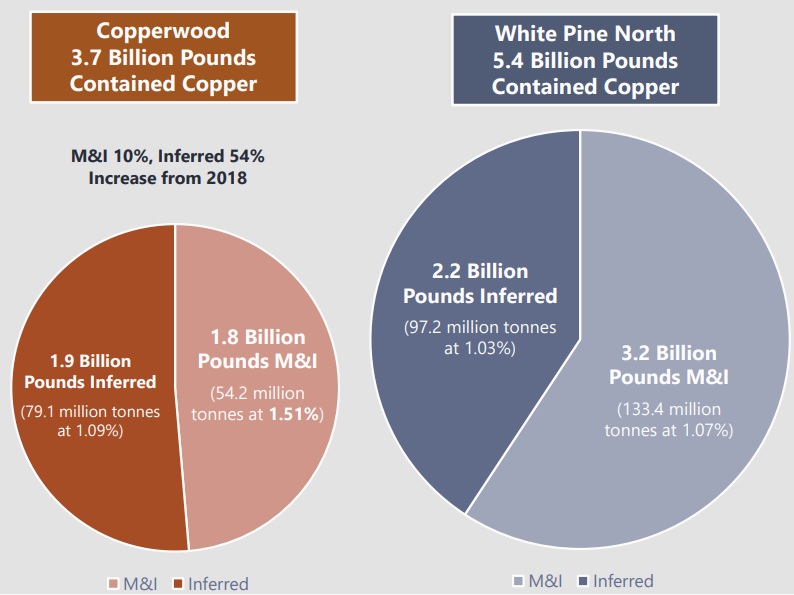

There are two other important elements here. First of all, less than 1 billion pounds of copper of the global resource of 3.7 billion pounds across all categories made it into the reserves category and was eligible to be included in the mine plan. Adding a few hundred million pounds of copper will help the economics of Copperwood (although the discounting factor will play a role as well). But the much larger White Pine North project which contains 5.4 billion pounds of copper and is currently going through the permitting process could be a game changer.

Disclosure: The author has no position in Highland Copper. Please read our disclaimer.