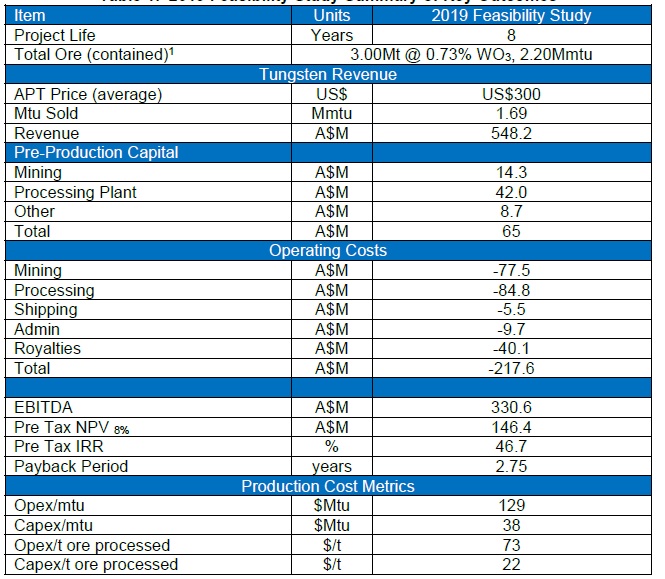

King Island Scheelite (ASX:KIS) has now completed an updated reserve estimate on its Dolphin tungsten project, and used this new reserve estimate as starting point for a feasibility study which envisages producing 3,500 tonnes of WO3 concentrate per year.

The average recovery rate is anticipated to be 77% which means that the current 3 million tonnes at 0.73% WO3 will result in a total recoverable tungsten production of 1.69 million MTU. The total anticipated revenue is A$548M, which is the equivalent of US$384M or US$227/MTU.

The Dolphin project indeed is quite small but due to the exceptionally low initial capex (A$65M) and opex (A$129/MTU), the margin of almost A$200 per produced MTU is really good despite an average strip ratio of approximately 10 over the entire life of mine, peaking at 20 and 17 in years 2 and 3 of the mine life. The total cumulative EBITDA is estimated at A$331M which means that after deducting the initial capex, the total undiscounted and pre-tax cash flows could be estimated at A$275M. The pre-tax NPV8% and IRR are respectively A$146M and 47%. Unfortunately no after-tax results were published.

Go to King Island’s website

The author has no position in King Island Scheelite. Please read the disclaimer