Kore Potash (KP2.AX, KP2.L) had released the results of a pre-feasibility study conducted on the Dougou Extension (‘DX’) project, which is anticipating to produce 400,000 tonnes per year of MOP over an initial 18 year mine life at an FOB production cost of just below $87/t. Using a MOP (‘Muriate of Potash’, Potassium Chloride) price of US$422/t, the project will generate almost US$120M per year in EBITDA and US$95M per year in free cash flow resulting in an after-tax NPV10% of US$319M and a payback period of just over 4 years.

These updated economics represent a substantial improvement compared to the scoping study which anticipated a 15% higher capex but a 5% lower opex, but the main reason for the improved economics is the used potash price. Whereas the potash price in the first six years of the DX mine life is budgeted at $344/t (approximately 5% lower than in the scoping study), the potash price used in years 7-18 is substantially higher at $456/t. Granted, the high discount rate minimizes the impact of the high potash price on the NPV so we can probably say the improvement of the economics is ‘real’, although we would take the $450+/t potash price from year 7 on with a grain of salt.

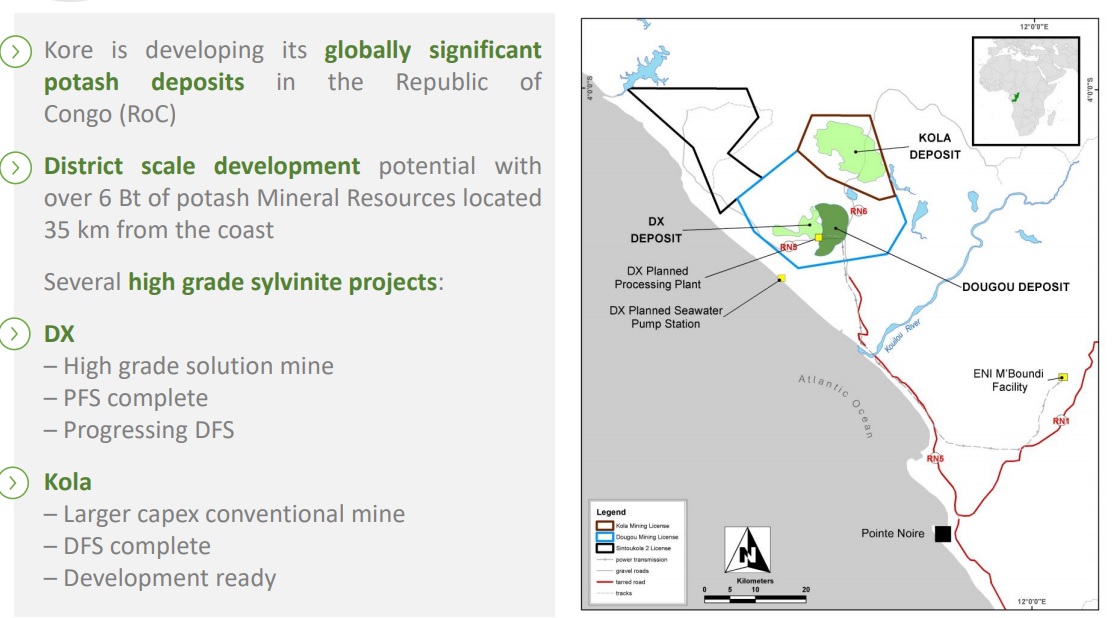

Also keep in mind the pre-feasibility study is solely based on an 18 million tonne reserve which is just a fraction of the 145 million tonnes in total resources (down from in excess of 230 million tonnes).

Disclosure: The author has no position in Kore Potash.