Rogue Resources (RRS.V) has recently released a PEA on its Silicon Ridge silica project. We discussed the results of the PEA and the next steps with President & CEO Sean Samson.

About Silica

- Most readers won’t be very familiar with Silica, could you perhaps explain what type of commodity it is, and what it’s being used for?Silica is most commonly found in nature asquartz, and is often the major constituent of sand. Though very prevalent in nature, deposits with very good quality silica and minimal impurities (iron (Fe), aluminum (Al2O3), titanium (TiO2), etc) are very rare. Good quality silica has a broad spectrum of applications, ranging from microelectronics, glass, ceramics, silicon metal and fillers through to basic building materials.

- How does the price-setting of silica happen? Are there annual sale contracts at fixed prices? How can producers know what kind of price they will get for their product?

Silica pricing is indeed opaque and producers are required to find their own buyers—that is what we’re deep into doing right now. The business varies by size and sophistication of buyers and sellers but for the large volume, multiyear demand, pricing is driven off of multiyear contracts, often with inflation escalators.

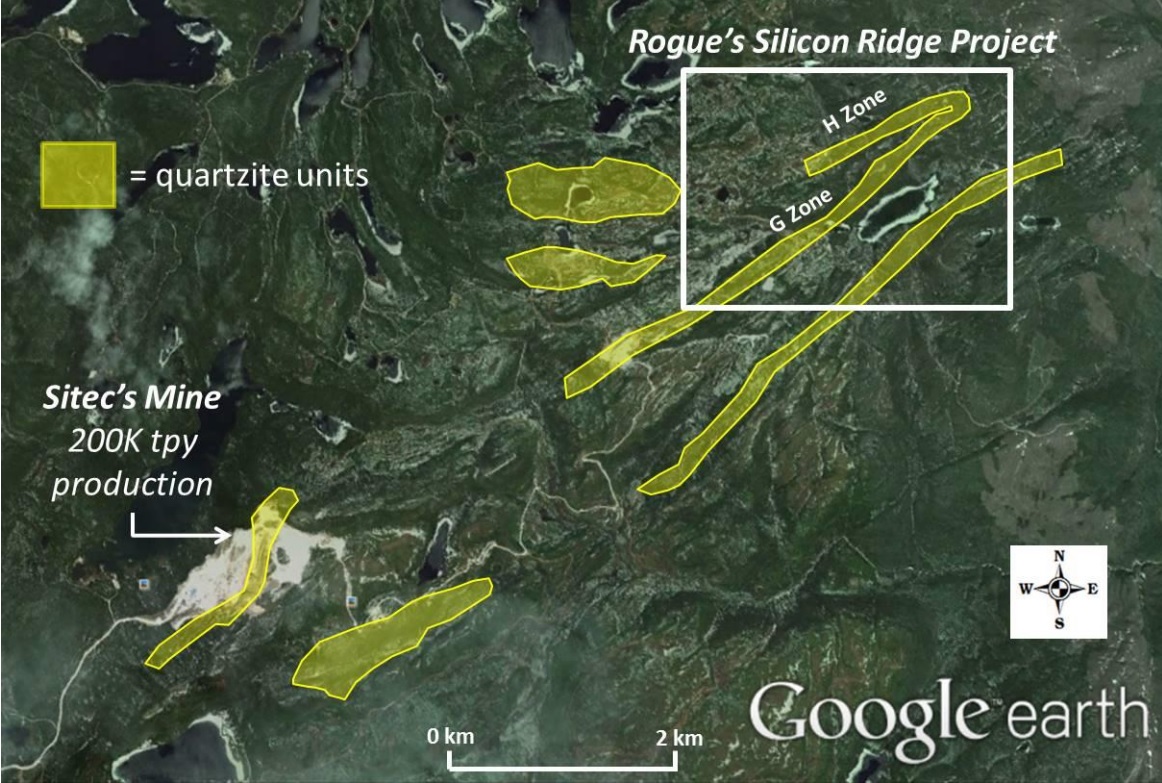

- There’s another silica mine which has been in production for several decades just a few kilometers down the road from Silicon Ridge. Is the average end-product similar to what you are aiming to produce? What kind of economics does the Sitec mine have?

We intend to build a simple crushing plant like our neighbours and we will be mining the same trend, so we suspect that the end-product will be similar. Although Sitec is privately owned, we know that they have had a multi-generational operation that we suspect has had similar profitability to what we are targeting. Their end-user mix, as best we can understand, is silicon metals (ferrosilicon and metallurgical grade silicon), and quartz countertops. We intend to target those plus, glass and other fillers.

The PEA

- The initial capex is quite low at C$13.1M, but the after-tax NPV10% is just C$23.8M. Have you considered increasing the output from 200,000 tonnes per year to 300,000-400,000 tonnes per year? Or perhaps, as a more direct question, why did you settle on a first base case scenario of 200,000 tonnes per year?

There is very good potential upside in the project to try and increase the production. Operationally we will have minimal constraints– the contract miners can bring in added capacity and on the processing side, we will design and build to have some flex capacity plus potential to easily add additional capacity.

There are a couple major reasons that we started with the 200K base case:

1- This level of permit for this size quarry is the most straightforward and we wanted to start with this and as we develop our relationship with the regulators, we will look to increase our production rate. We probably won’t wait too long before studying the impact of a potentially increased production rate and we think we will have a pretty good idea of what will be required even before we finish commissioning the currently planned 200,000 tpa phase.

2- The market. We want to make sure that we can successfully place this much product into the market, across our various target verticals. As we gain comfort that the market can continue to absorb additional high quality supply like ours, we’ll look to increase production after going through the required permitting process. Out of the gate we wanted a conservative base case and we’re pleased with the economics it gave us in the PEA. This potential capacity increase is pure upside.

Your total measured and indicated resources contain almost 10 million tonnes of high-grade SiO2. Was the decision to cut the mineable resource off at 4 million tonnes based on the 20 year mine life, or were pit constraints the big issue? How easy would it be to maintain the 20 year mine life but to increase the annual output? Would this A) be feasible in the mine plan, and B) would you have any idea what the corresponding capex increase would be?

The full Resource is pit-constrained, so we do plan to mine the 10 (M&I) + 5 million (Inferred) tonnes over time. The PEA was mainly run for 20 years / 4 million tonnes because of the diminishing returns due to discounting the future cash flows. It’s worth noting that the global, non-constrained Resource was more than 75 million tonnes, so sourcing material shouldn’t be a problem).

The corresponding capex for a capacity increase above 200,000 tonnes per year would obviously be less capital intensive because of the fixed/variable split in the upfront spend. I don’t have a detailed estimate but we’d already have site infrastructure and the mining is all on a unit cost so we’d be looking at increases only in adding additional secondary crush, rinse and sort capacity. It would be a lower per tonne capex than the already low intensity of the per tonne capex in the PEA.

- How does the used price of C$88.8/t compare with the prices received by the nearby silica mine?

Our neighbours are private so it’s all a guess but based on the industry verticals we think they are selling into, our estimate is a conservative price compared to what we think they may receive. Again, we wanted our first economic assessment to be conservative, so our estimated revenue per tonne is also erring on the cautious side.

- Considering there’s a producing mine nearby, would it be safe to assume the environmental permitting process will be quite straightforward, despite the occurrence of the Woodland Caribou which enjoys a special protective status?

We (and our advisors) anticipate a straightforward permitting process and are working very closely with the Québec ministries on all sensitivities, including the Woodland Caribou. Rogue plans to be operating for generations so we want to start on the right foot with the regulators.

- How will you market your end-product? Will you try to have one large customer, or several smaller ones?

We anticipate having 2-5 customers for our material, and hope for diversification by industry vertical. Our marketing strategy is to target unit profitability, with the best blend of anticipated price compared to capital and operating expense required for production.

- How will you try to finance the equity portion of the initial capital expenditures?

The equity portion of the capital expenditures will likely be financed via the market through a private placement in conjunction with an advancement decision. We will plan to maximize non-dilutive financing, trying to tap into friendly debt and/or supplier or buyer financing.

Corporate

- You have recently raised cash at C$0.10 to boost your cash balance to approximately C$1.5M. How far will this get you?

Some of our main shareholders were interested in investing further into Rogue and a decision was made to increase our treasury which resulted in the recent raise at C$0.10. Our current treasury is sufficient to meet the needs of the Company until after the development decision has been made for the Silicon Ridge Project and well into 2017. A majority of the costs related to the PEA and metallurgical work have been prepaid and further payments have been included in our budgets. We continue to monitor spending very closely and minimize corporate expenses where possible to make every dollar count.

- After completing the private placement, Rogue’s share price fell by approximately 50%, and you have recently completed a 10:1 share consolidation which is generally seen as a very unpopular move, why did you decide to go ahead with a 10:1 reverse split and what will be the advantages in the longer term?

- Our share price fell by approximately 50% prior to the closing of the most recent financing and it was completed at a healthy premium to the share price. The drop in the share price continued even though the company continued to de-risk and advance the project as outlined by management.

A decision to execute the reverse split of 10:1 was taken after a great deal of consideration and review: trading patterns, shares issued and the potential to finance the Silicon Ridge project all played a role in our decision to roll back the stock. While unpopular with some, the roll back will provide the Company greater flexibility moving forward and we believe will benefit all shareholders as we advance the Silicon Ridge project, attract new investors and grow the Company. We will only begin to unlock real value for investors when we can successfully finance, build and operate Silicon Ridge for a profit and I know that the reverse split put us closer to that goal.

- The undiscounted after-tax free cash flow is expected to be C$81M which compares quite favorable with the current market capitalization of Rogue Resources. What are the next steps to unlock and monetize this value?

We do currently represent a deep, deep value in comparison to our planned economics.

To try and monetize that value we intend to keep following the Plan we laid out in February of this year, and the next steps include some Further Analysis on the Project (optimized mine plan, procurement strategy, etc) but our primary focus is now to get partnerships with Market Participants- offtake(s), sale order(s), etc.

Ours is shaping up to be a very nice little quarry business and when we confirm buyers this value proposal should make everything more ‘real’ for investors as offtake agreements would ratify and validate the technical merits of our project. I don’t know how to move our market value other than to keep advancing our Plan and introduce and repeat our investor story as broadly as possible.

- Should you have to raise C$4-5M in equity to fund a part of the initial capex, will your current large shareholders be prepared to write some cheques, or are you preferring a ‘strategic’ joint venture with for instance an end-user of your silica?

To finance the Silicon Ridge Project, our PEA says we’ll need to invest ~$13M for the upfront capex. We plan to initially tap into non-dilutive sources for these funds, including government sources, the contract miner we choose and also the end-user of our silica.

After we tap these pools, we will go to the public markets for the rest, including an equity raise. I know that our current large shareholders remain very supportive of the company and will likely participate to reserve their share but we have also been cultivating relationships with other high net worth and small institutional investors. Some of these new investors have struggled to gain a position in our tightly held stock to date so in the event of a project financing we know we can get them in for the size they want.

At the end of the day, we intend to finance the project with the least dilution possible and through a variety of sources, to keep the NPV/share as high as possible.

Go to Rogue’s website!The author has no position in Rogue Resources. Please read the disclaimer