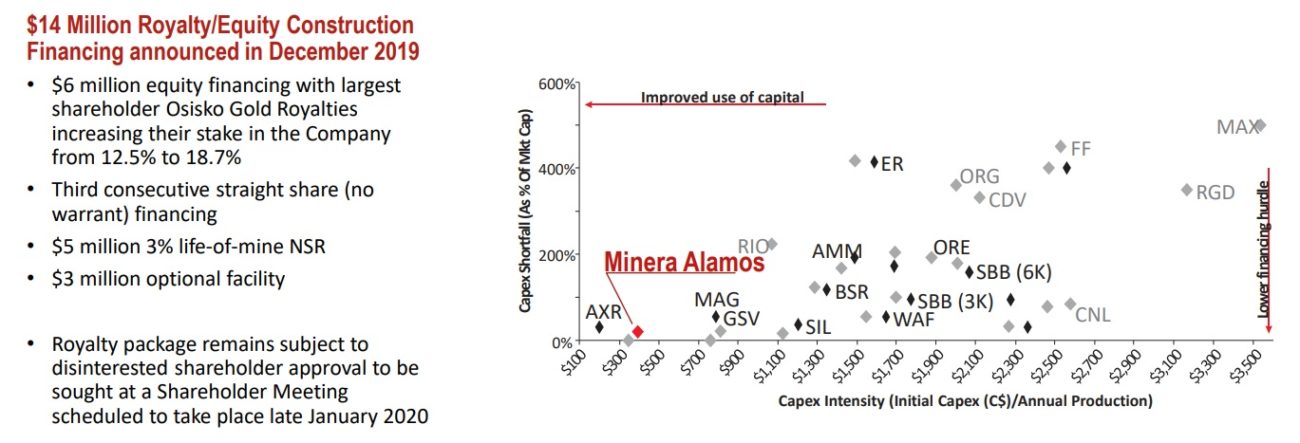

Minera Alamos (MAI.V) has entered into an agreement with Osisko Gold Royalties (OR, OR.TO) whereby the latter will make up to C$14M available to Minera so it can start building the Santana gold mine in Mexico.

The C$14M funding package will consist of three components. A first C$6M will be injected as an equity investment whereby Osisko will purchase 30 million shares at C$0.20 as part of its anti-dilution right. In a way, we should be happy Osisko is exercising that right now, at 20 cents instead of a few months ago when the stock was barely trading at around 10-12 cents as this clearly keeps the dilution limited. This also is the third consecutive financing where Minera Alamos doesn’t need to issue a (half) warrant to sweeten the deal and this will help to avoid creating a warrant overhang that kept the stock at around 10 cents in the first half of the year.

Osisko is obviously more interested in royalties and streams, and a second C$5M will be injected through the sale of a 3% NSR on the Santana project in Sonora. Based on the current gold price, Minera will only need to deliver just over 2,600 ounces for Osisko to recoup its payment, which means the total payable gold production required to ‘make Osisko whole’ is just over 75,000 ounces of gold. Yes, Osisko should make a tonne of money on this royalty as the mineable resource (non-NI43 compliant) is a multiple of that. And that’s fine. After all, Osisko is taking a leap of faith here by supporting the Minera management and its plans to develop a non-NI43 resource without a published mine plan.

On top of the C$11M equity and royalty package, both parties also included an ‘optional royalty’ feature whereby Minera can draw down an additional C$3M from Osisko in return for a temporary (36 month) additional 2% NSR. Should Minera draw down on the optional royalty, it will have to deliver a minimum 660 ounces of gold per year (220/oz per year per C$1M tranche which represents a 0.667% NSR) during the three year period. This optional royalty provides financing flexibility to ensure the Company has sufficient financial runway as it enters construction, however, we would expect Minera to explore other options before executing on the optional royalty.

The financing deal doesn’t really come as a huge surprise as Osisko Gold Royalties has been supporting Minera Alamos for quite a while now. Minera Alamos may actually be the first company where the ‘incubator model’ really works as Osisko had to step in and ‘rescue’ Barkerville themselves. With exposure to Minera Alamos on two levels (equity and a royalty), Osisko stands to gain from the development and production success at Santana although on pure dollar terms they will likely make more from their equity exposure than the other value drivers which has them very much aligned with other shareholders.

Minera Alamos is now fully funded to complete the construction of Santana and have enough working capital on hand to ‘survive’ the period between the completion of the construction activities and the gold being recovered from the leach pad and sent off for further processing. The market reacted positive on the financing package and this, combined with the 30M shares to be issued to Osisko, have just put Minera Alamos over the C$100M market cap threshold.

Disclosure: The author has a long position in Minera Alamos.