The gold price seems to be hanging in there and doesn’t have any issue to remain above the $1500 level. In a previous report a few months ago we had a look at Bravada Gold’s (BVA.V) Wind Mountain gold project in Nevada and tried to come up with a (simplified) cash flow model to see how the economics of the project would evolve if we would use updated parameters and an updated gold price.

Since then, the share price has barely moved although the Wind Mountain project should clearly be viable at this point. We sat down with CEO Joe Kizis to discuss Wind Mountain, the other projects in the asset portfolio and the company’s plans for 2020.

Sitting down with Joe Kizis, CEO

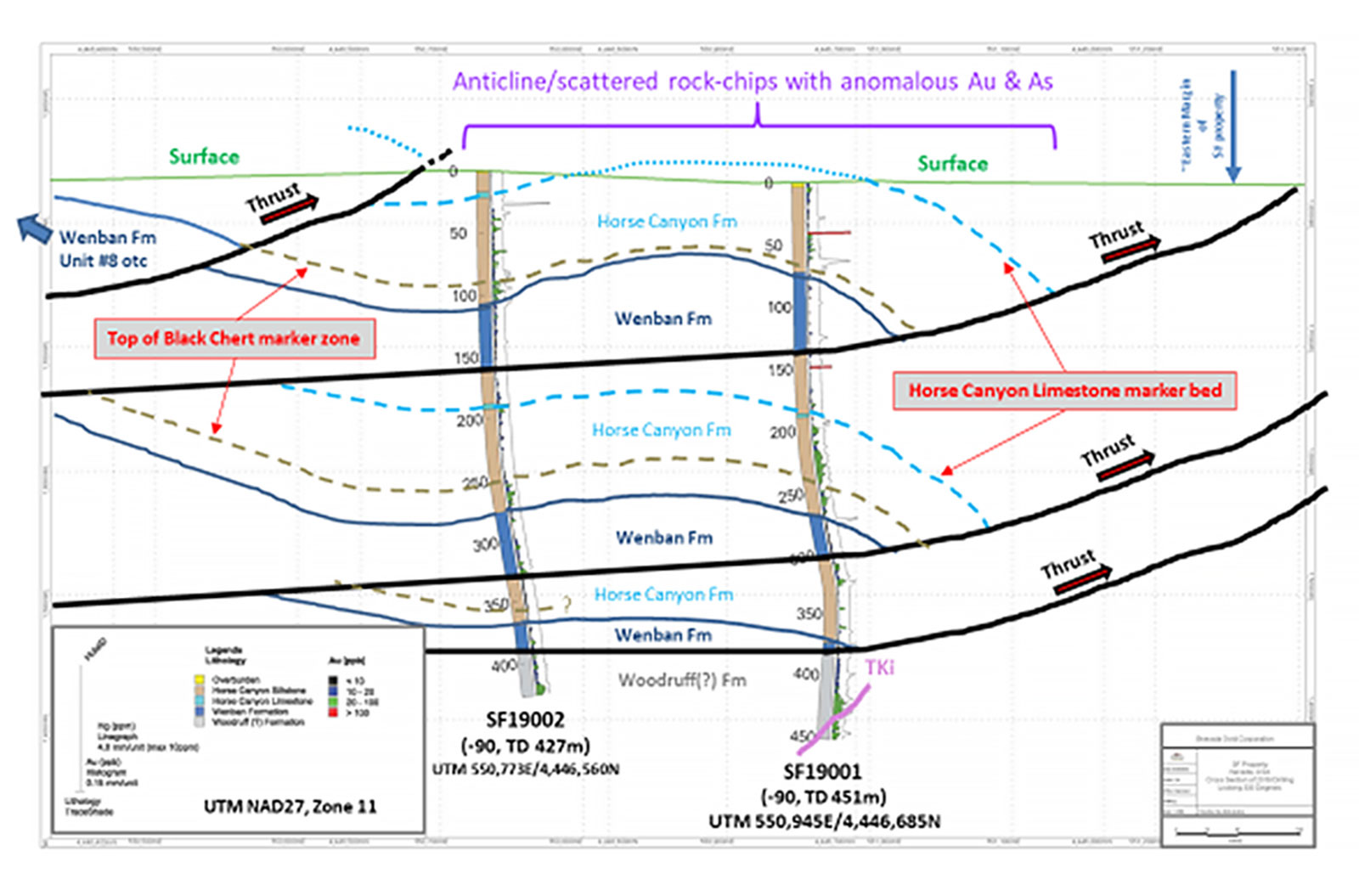

Bravada has been quiet since the drill results on the SF property were released. Only two holes were drilled and anomalous gold values were detected, but perhaps the market expected more from the small drill program. Could you perhaps paint a background picture for the two-hole drill campaign? What made you decide to drill the holes in those two spots and how has your interpretation of the SF Property changed?

The two relatively deep, proof-of-concept reverse-circulation holes were designed to test our geologic and structural interpretation and to verify that a gold system exists on the claims with the ultimate goal of making a new discovery. We located the first hole where we had the best surface geochemistry. The second hole was to the west, down dip of the low-angle faults we postulated to be controls on mineralization and, thus, possibly closer to the source of the gold-bearing fluids. Exposure is very poor at SF, so geology was largely interpreted from less-definitive float mapping (compared to mapping outcrops if they existed).

The two holes intersected two (and possibly three) low-angle faults, which resulted in three repeated slices of the favorable Horse Canyon/Wenban formations. Basically, tectonic forces pushed the favorable host rocks over themselves.

This is a very favorable setting because it demonstrates that several layers of good host rocks exist, as well as several possible fault-related channel ways for gold-bearing fluids. Interestingly, the two holes helped to clarify that the first hole’s stronger geochemistry at surface (the reason we chose that location) is due to a “hanging wall anticline” (a fold related to a low angle thrust fault) at that location. The anticline tends to accumulate and trap gold-bearing fluids, somewhat analogue to an oil trap.

Geochemistry of samples from the two holes shows long intervals of anomalous gold and pathfinder elements, particularly certain base metals. The two holes are located on the eastern margin of the claims, and our interpretation is the low-angle faults and favorable rock package should be tested down-dip to the west, which should be closer to the source of the gold-bearing fluids. Magnetic and possibly gravity and IP geophysics will be useful in next-phase targeting.

We are considering bringing in a JV partner to further advance SF.

In a previous report, we checked how the Wind Mountain economics would evolve using the current gold price. Turns out, the economics of Wind Mountain look pretty good at $1500 gold. Do you have any plans to focus some efforts on Wind Mountain to perhaps try to increase the resource to extend the anticipated mine life beyond the currently planned 7 years, where after the PEA could be updated?

I consider the “feeder” target that we’ve developed south of the existing oxide resource to be the strongest target that Bravada has in its portfolio at this time. Highland also has excellent targets, and OceanaGold will continue testing that property as part of their earn-in. But the existing oxide resource at Wind Mountain would be much more valuable as a “starter pit” to a higher grade deposit that we postulate to exist in the feeder, so I would put our effort into an initial proof-of-concept drill test of the feeder target prior to expansion drilling of the existing resource.

Success at the feeder target would be a major gamechanger for Bravada, making the ratio of risk to reward for this target very favorable.

Given how the markets appear to behave right now where smaller outfits still have issues to attract attention, do you feel there still is money available for pure exploration projects, or would falling back on a slightly more advanced project like Wind Mountain be the ‘safer’ choice?

My feeling is for a junior explorer to have a significant success searching for gold in Nevada, it has to find either a very large, moderate-grade gold/silver deposit that makes money as an open-pit operation (say +3MM oz Au at +1g/t) or a high-grade gold/silver deposit that makes money as an underground operation (say +1/2MM oz AuEq at +7g/t).

Pure grass-roots exploration plays are still very difficult to finance, and the odds of success are relatively low for any individual play. Advanced exploration plays are definitely “safer” and looking for evidence of the targets I’ve mentioned above is critical to discovering a new deposit that will be meaningful to a junior (and to potential partners or acquirers).

For Bravada, Wind Mountain is my top choice and SF is my second choice for the large open-pit type of discovery. Highland is my top choice for the high-grade underground type of discovery, followed by Baxter and then East Manhattan. And as you remember, OceanaGold is earning into Highland.

How is OceanaGold progressing on the Highland joint venture? Would you know how much of the initially required US$4M to acquire a 51% stake in the project has already been spent?

OceanaGold spent approximately US$330,000 at Highland in 2019. They are preparing a report with full results and recommendations for 2020 at this time, although I was shown most of the results during our last Technical Committee meeting this past fall. The results of their CSAMT geophysics were very exciting because it appears to show a second graben beneath exposures of sinter on the eastern part of the property.

Graben-related structures are often important ore controls in Low-sulfidation gold/silver deposits. A previously identified graben lies to the west on the Highland property and is related to significant gold values in float samples previously collected. Bravada’s original 2002/2003 high-grade intercepts were from an area somewhat farther west of the western graben.

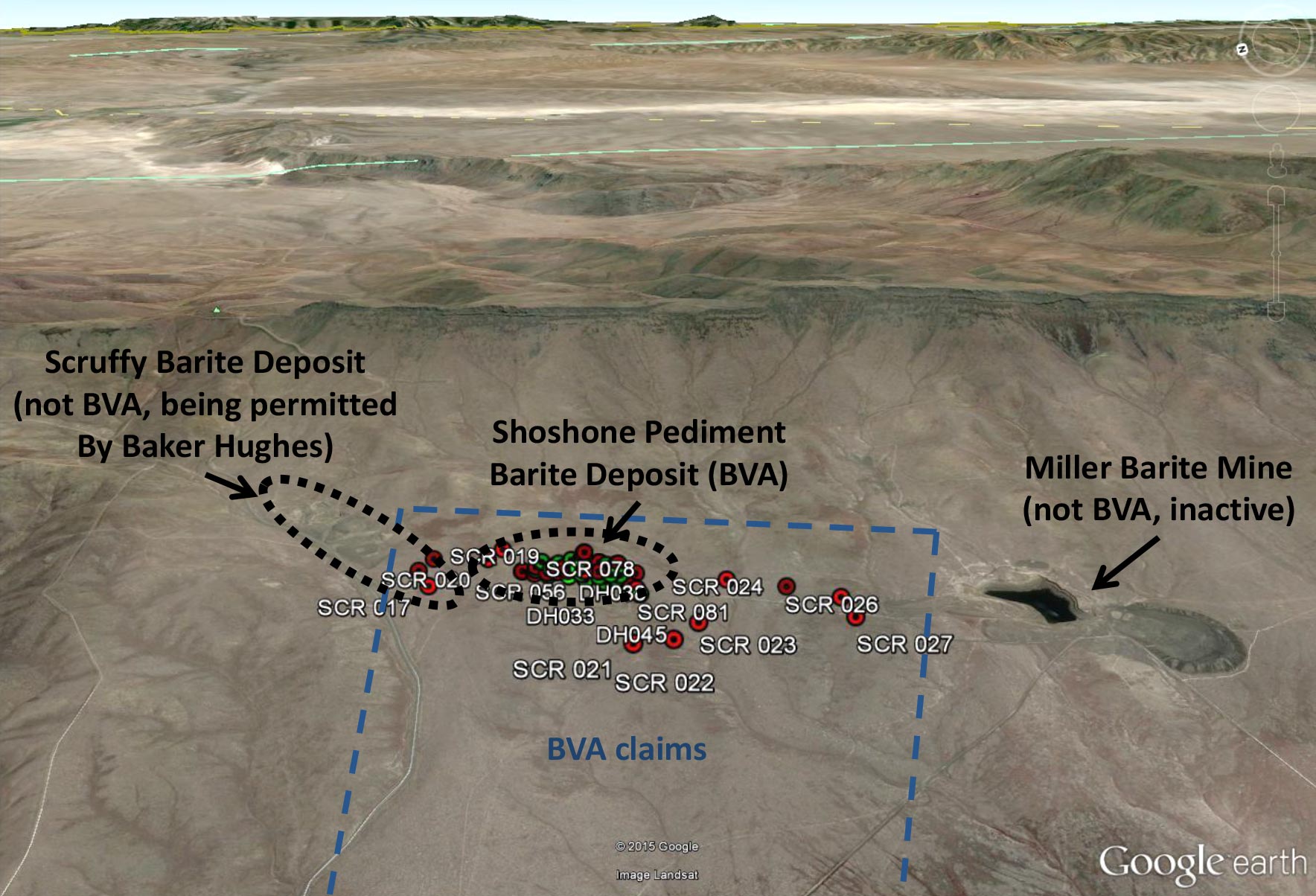

How is Baker-Hughes advancing the Shoshone Pediment? Is Bravada still on track to receive royalty payments later this year? Would the expected cash inflow of C$0.5-1M per year still be a valid guesstimate?

Baker Hughes has had delays getting their mining permit, which they originally expected late in 2019. Although we are not privy to specifics, the delay appears to be due to additional environmental test work now required by the government. Once their mine plan is available for public comment, Bravada will have a better idea when mining will begin and at what rate. My understanding is that Baker Hughes is anxious to begin mining because the Shoshone Pediment ore is better than the ore they are currently mining; however, the market for oil-field additives like barite will strongly influence the rate of mining and thus Bravada’s royalty stream.

Connected to this, how is Bravada’s treasury at this moment? As of the end of October, your cash position had decreased again to just over C$100,000 while the working capital position turned negative to the tune of almost C$700,000. It’s probably unlikely you can wait to re-finance until the Shoshone Pediment royalty kicks in. Will there be any catalysts or noteworthy updates to drum up investor interest?

We received a couple of reclamation bond refunds, and we have some overdue payments from a property that we are hoping to receive soon. We are showing several properties, which we hope to provide us with news and partial funding. We also have warrants in the money that will expire this year. With the somewhat better market conditions, we are also increasing our promotion activities in order to better get our story out to investors. Currently our cash position is below C$100,000.

Related to your financing needs. There are almost 7 million warrants with a strike price of C$0.05 that will expire later this year. Have you seen some of those warrants being exercised lately, and are you actively pursuing the warrant holders to exercise them to keep some money in the till?

We have not yet received any of the warrants exercised, and we will be discussing with those investors this month.

Your 5-year contract as a CEO is expiring in a few months (April 30, 2020). May we assume you would like to stay at the helm of the company and a contract extension is being negotiated?

Pending any unforeseen circumstances and approval by the board, I expect to stay on as President and Director.

What would you like to achieve with Bravada Gold in 2020?

I would like to see significant shareholder value created by open-pit type discoveries at the feeder target at Wind Mountain (1st priority) and SF (2nd priority), and underground type discoveries at Highland by OceanaGold. I would also like to find well-funded JV partners for Bravada’s other highly prospective projects like Baxter and East Manhattan.

Conclusion

Joe Kizis has been running a very tight ship at Bravada and the total cash outflow in the first quarter of its financial year (Q1 ended in October) was approximately C$215,000 including C$150,000 spent on the properties (C$115,000 was capitalized, C$36,000 was expensed). Excluding these expenses, the pure ‘corporate’ overhead cost is probably just C$60-70,000 per quarter and that’s very rare to see in this space.

Bravada Gold deserves some luck, either at the SF property or at Wind Mountain (or at the joint ventured Highland property) and it will be interesting to see which projects will be prioritized by Bravada in 2020.

Disclosure: The author holds a long position in Bravada Gold. Bravada Gold is a sponsor of the website.