The lithium market has been very volatile lately and we have seen the prices of lithium carbonate spike to in excess of $75,000/t, a level we didn’t even expect to see in our wildest dreams. The lithium price has recently started to move downwards but that’s not really an issue. As you may remember, the base case scenario used by Century Lithium (LCE.V) for the pre-feasibility study used a price of just $9,500/t.

While we expect the capex and opex to increase in the upcoming feasibility study, the lithium price increase since the publication of the pre-feasibility study has greatly outpaced the opex and capex increases. We estimate a 50-75% increase on all levels (capex, opex and lithium price) will still result in a 30-70% increase of the after-tax NPV8%. And considering a base case lithium carbonate price of $20,000/t appears to be the ‘new normal’ (this also is the price used by American Lithium in its recent PEA on a similar deposit, but certain brokerage houses are more bullish and use a LCE price in the mid-$20,000 range as did Lithium Americas (LAC, LAC.TO) when it ran the numbers on its large Thacker Pass deposit in 2022)we are confident the upcoming feasibility study will show a higher NPV and IRR notwithstanding the anticipated capex and opex increase.

A look at the lithium market

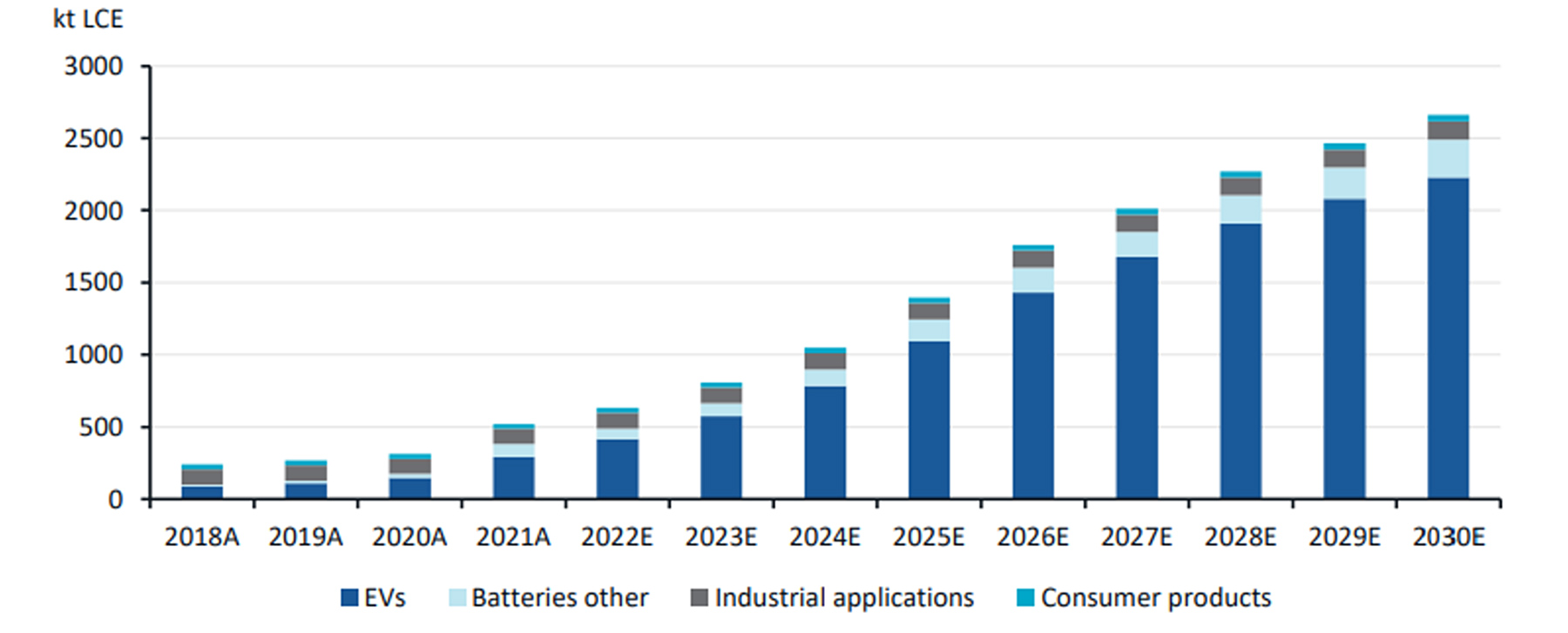

While most readers don’t need a lithium ‘primer’ as the importance of the metal for the EV industry is well-documented, perhaps it is useful to briefly summarize the recent events in the space. The demand for lithium will increase, there is no doubt about that. And a recent report published by Canaccord Genuity indicates the demand for lithium will quintuple by the end of this decade. Even if this is too optimistic and too aggressive, even expecting ‘just’ a 100% increase in the demand for lithium carbonate equivalent will put severe pressure on the supply chain as it basically requires dozens of new mines and projects to come online.

The anticipated demand increase is not new information. But the new element that is pretty interesting is the new Critical Minerals Act, published in March by the European Commission. Not only is lithium deemed to be a ‘strategic’ metal, it has now been earmarked as a ‘critical’ metal. And the list of critical metals has not been compiled by a bunch of politicians but is based on several different parameters including the economic importance, the substitution index, the supply risk and the import reliance of a metal. The appendix of the Critical Raw Materials Act looks more like ‘advanced economics’ rather than bureaucrats filling pages.

The document, and more importantly, the explanatory memorandum, is a very interesting read. According to the official proposal, the European Commission expects the annual demand for lithium to manufacture batteries to increase by a factor of 8,800% by 2050. On top of that, the EU is pointing at China as part of the so-called concentration risk: with about 56% of the refined lithium coming from China, the EU is clearly worried about having sufficient access to the metal and that’s the main reason why lithium is included in the list of critical metals.

The bottom line is straightforward: lithium is here to stay. And while the lithium price may be volatile in the next little while, the bigger picture is clear. The demand will continue to increase and it will be up to the developers of lithium projects to rise to the task.

What should we expect from the upcoming feasibility study?

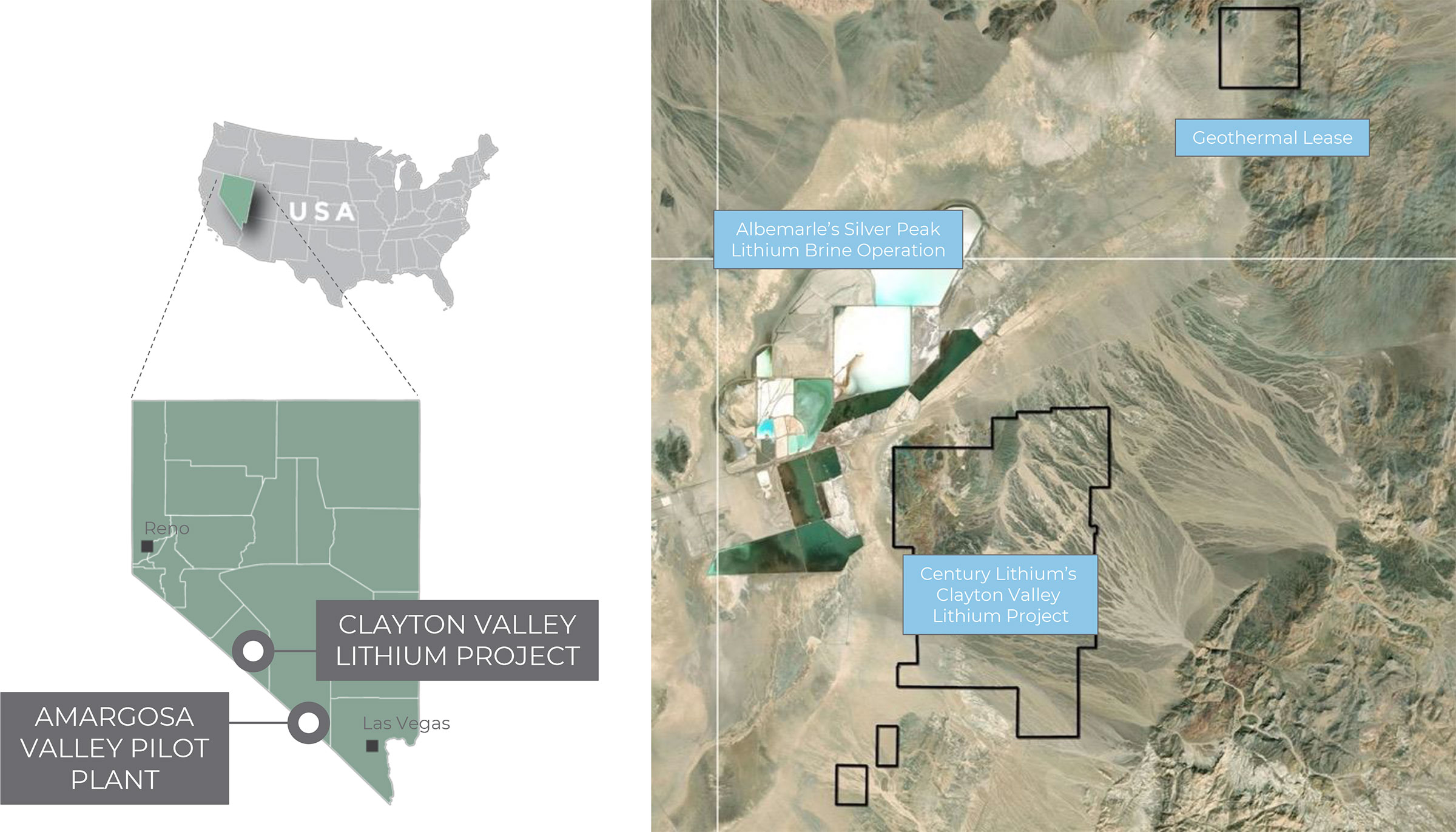

Since the publication of the pre-feasibility study, the company continues to further de-risk the production process (and thus, the asset). As you may remember, in Q3 2022, the company has achieved an important milestone as the pilot plant has confirmed it is possible to produce battery-grade lithium carbonate from the clay-hosted lithium deposit at Clayton Valley.

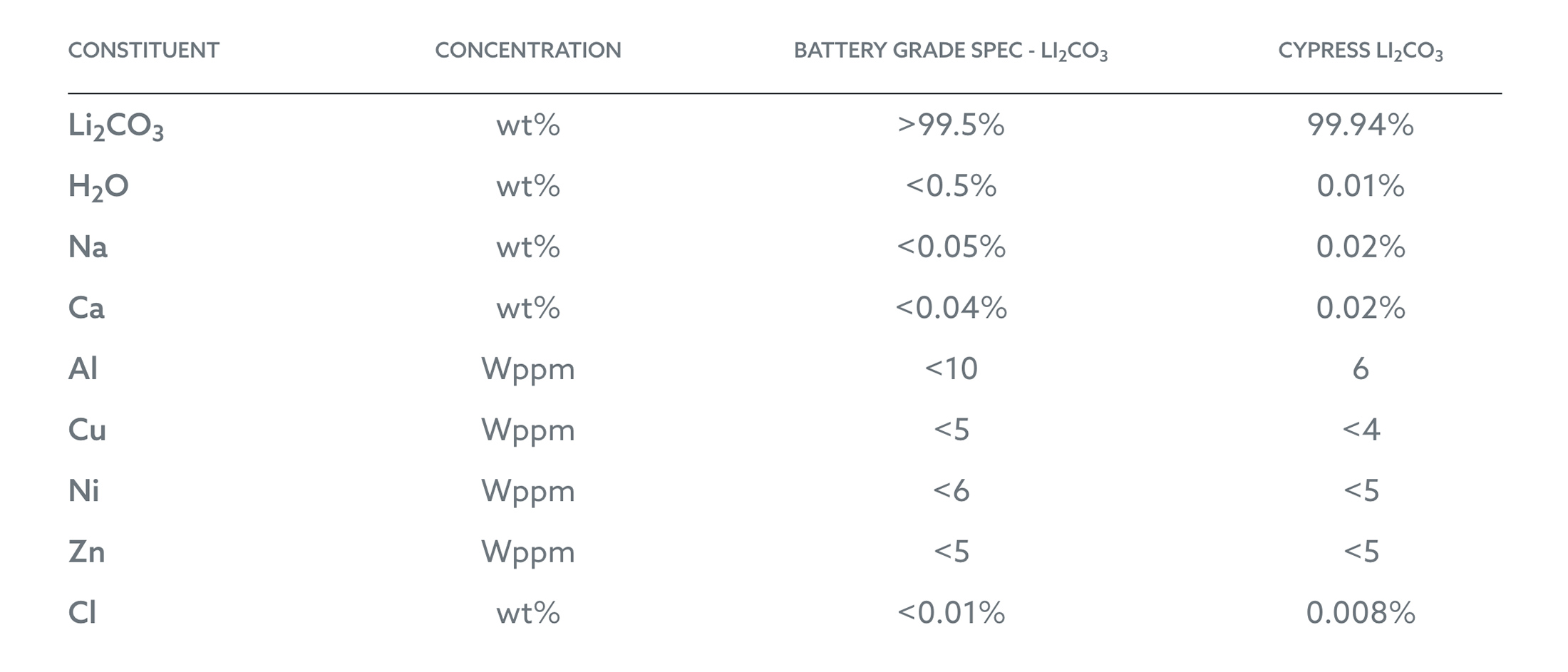

According to the recent test work, the Lithium Carbonate reached a purity of 99.94% which is indeed sufficient to qualify as battery-grade lithium (which requires a minimum grade of 99.5%). That’s important as technical-grade lithium commands a lower price compared to battery-grade lithium carbonate. The confirmation of the production of battery-grade lithium is also important for the upcoming feasibility study and given the strong lithium price (despite the recent price decreases), we expect the feasibility study to be better than the pre-feasibility study.

Without any doubt, metallurgy is the key risk and key component to make Clayton Valley work. The results of the 2022 met work is very encouraging while Century Lithium recently also announced it is collaborating with Koch Technology Solutions to apply the Li-ProTM process for direct lithium extraction (‘DLE’) at Century’s Clayton Valley project. The results of this program will enable Koch to provide engineering and cost data to Century Lithium for a full-scale installation of the DLE plant in Century Lithium’s Project.

As you may remember, Century purchased a license to the Lionex DLE process in the second quarter of last year and Koch Technology Solutions has acquired the exclusive rights to the technology which has now been incorporated and integrated in Koch’s own Li-Pro process. With this new agreement in hand, which extends beyond the use of the Lionex process, Century and Koch can now work together to further refine the production process as the Li-ProTM process could add value to the flow sheet. Century has received the Koch components and equipment, integrated them into the pilot plant, and begun testing utilizing the new equipment. These tests are operating independently from the feasibility study which means that any potential positive impact will provide additional icing on the cake at Clayton Valley as the outcome of the test work will not yet be included in the upcoming feasibility study.

And that brings us to the most important catalyst for this year: the feasibility study. We think this will be a company-shaping event as we expect the feasibility study to confirm the strong economics outlined in the pre-feasibility study.

Does this mean the feasibility study will mirror the pre-feasibility study? Absolutely not. It goes without saying Century Lithium will be plagued by the same inflationary impact we see throughout the mining sector. In the past three years since the pre-feasibility study was published the price of steel and labor has gone up tremendously.

While the company has not published any guidance as to what we might expect, we can reasonably expect a 50-75% increase in the total capex as well as a 30-50% increase in the operating expenses. Please note these are our own assumptions and are not the company’s official point of view. Century Lithium will likely not comment on price increases until the feasibility study is published. That’s only fair to make sure all investors have equal access to the same information, but we like to be prepared and are using a mid-double-digit price increase across the board.

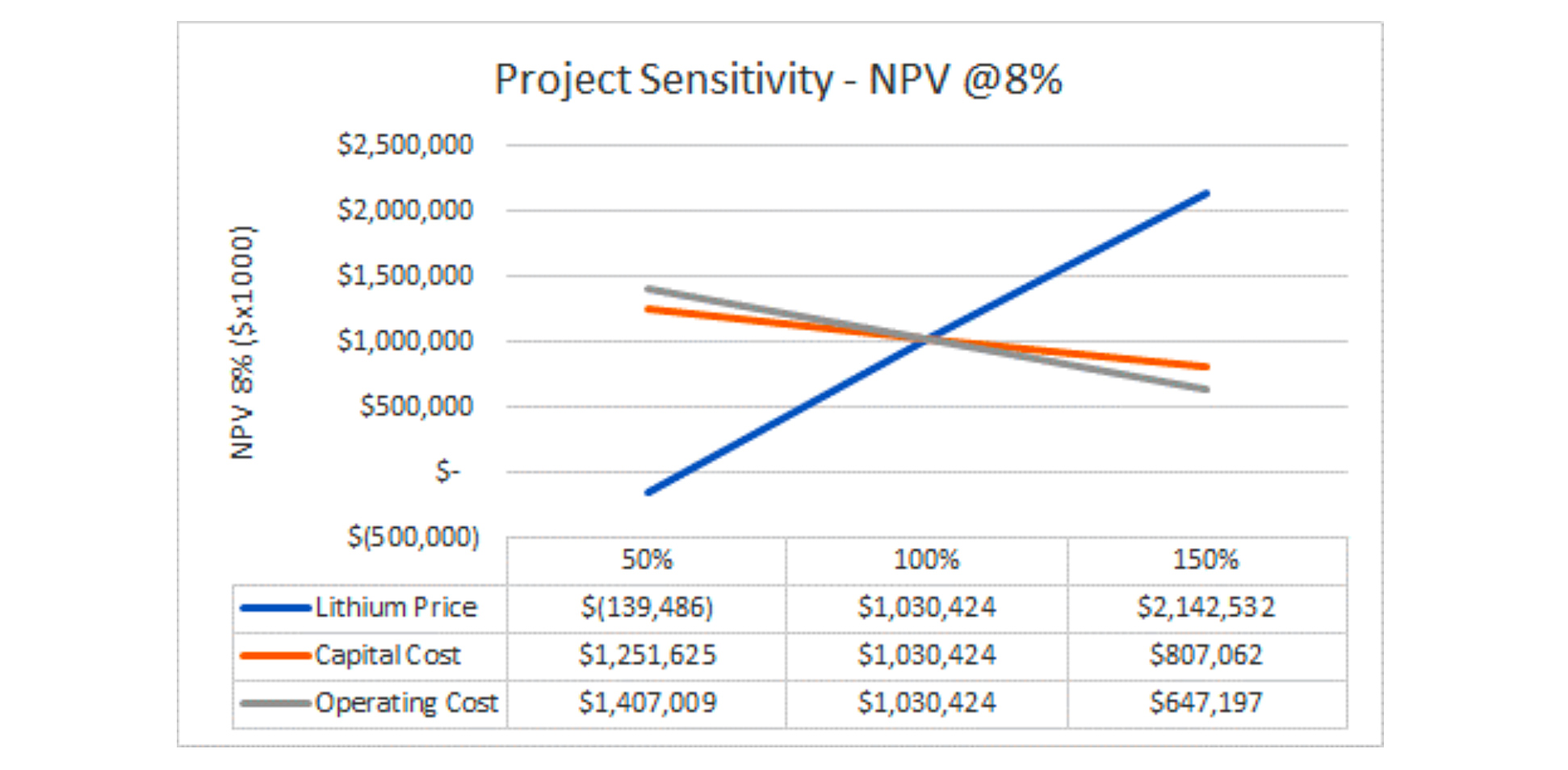

We don’t even have to speculate too hard as the pre-feasibility study contained a sensitivity analysis showing exactly what we are focusing on: the impact of a 50% cost increase across the board.

The image above shows that a 50% higher capex and opex would reduce the after-tax NPV8% by $223M and $383M respectively. On a combined basis, the total after-tax NPV8% would decrease to less than $500M. But again, that is based on a base case scenario of $9,500 per tonne of lithium carbonate. The image above also tells us that a 50% increase in the lithium price ($14,250/t) would add in excess of $1B to the NPV. Which means that a simultaneous increase of the opex, capex and lithium price by 50% will likely still generate a net increase of the after-tax NPV8% by 50%.

And given the recent developments in the lithium sector it is now completely unthinkable the base case scenario will use $9,500/t and even the $14,250 used in the ‘optimistic’ scenario in 2020 now appears to be outdated. We now anticipate most lithium companies, including Century Lithium, to start using a base case scenario of $20-24,000/t (in line with the LCE prices we have seen other companies use in the past twelve months). While that is more than double the base case price used in 2020, it still is a discount to the current spot price which is currently approximately $30,000/t. Century Lithium has not provided any guidance on the lithium price it plans to use but we would expect to see a similar long-term price used in the NPV calculation.

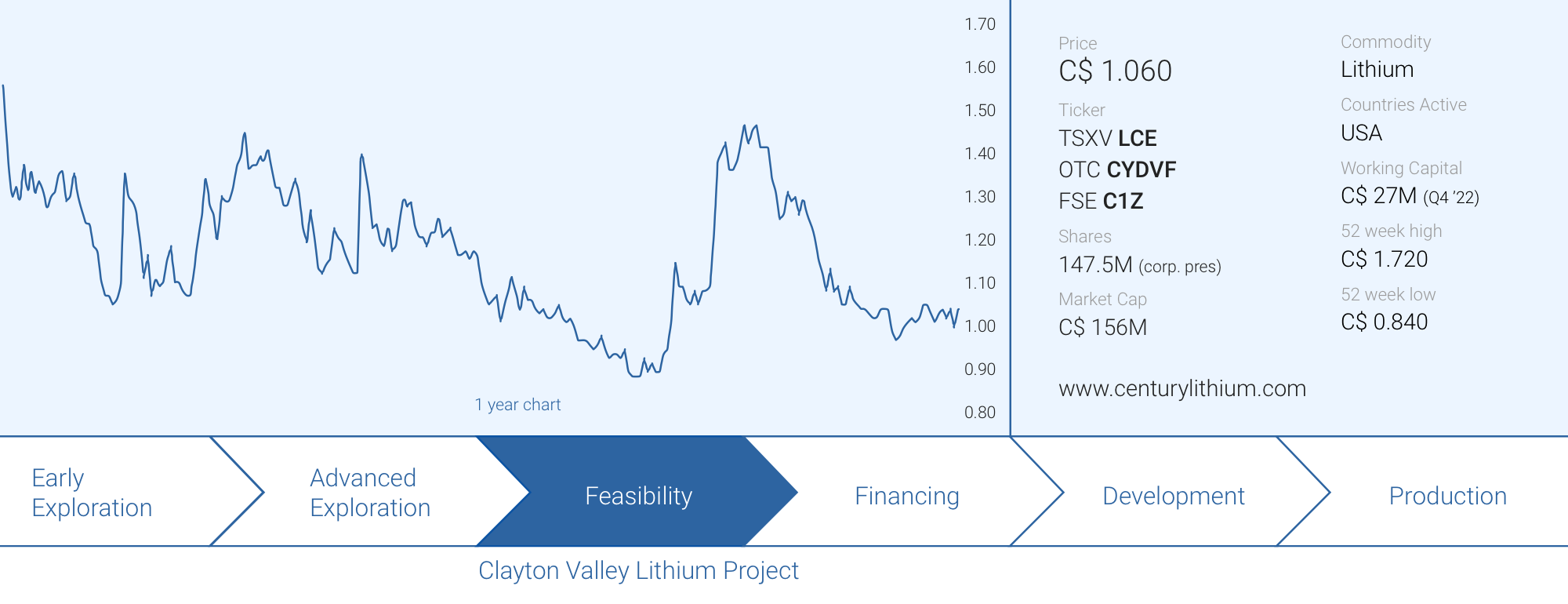

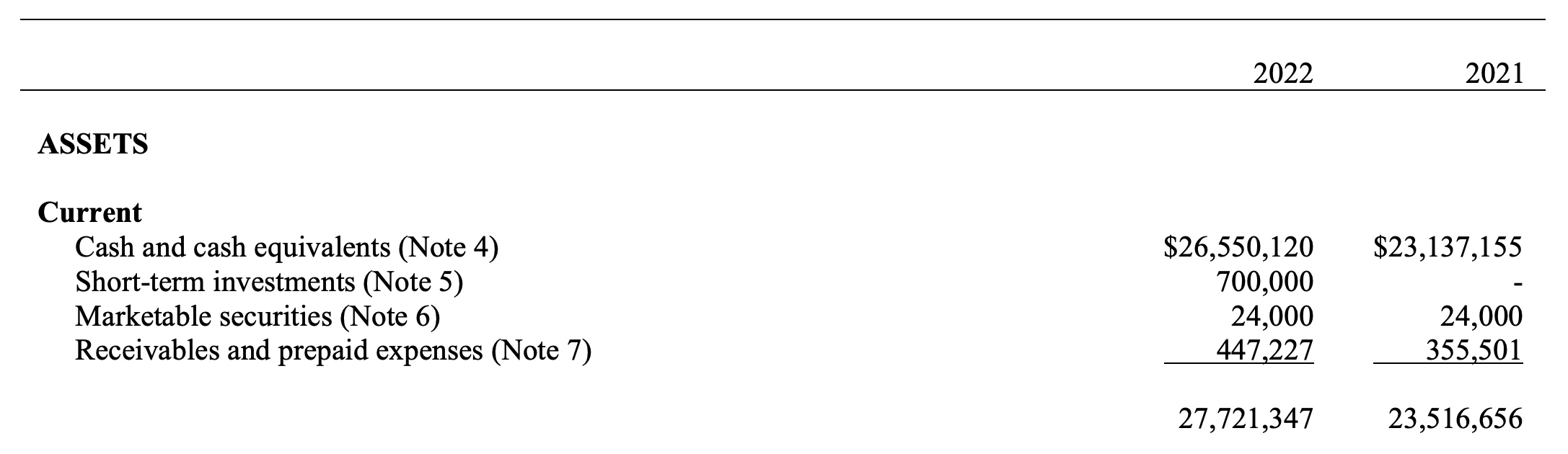

It goes without saying we are anxiously yet patiently awaiting the outcome of the feasibility study. Fortunately, Century Lithium is fully cashed up and it ended Q4 2022 (the most recent financial statements available on SEDAR), with C$27.7M in current assets and just C$773,000 in current liabilities for a net working capital position of C$27M. Around C$15.6M was held in cash while Century also invested C$11M in GICs with a 120 and 180 day term so that should yield a few ten thousand dollar in interest income.

Having a cash-rich balance sheet is a blessing in this environment. In the fourth quarter alone, Century (formally Cypress) recorded a C$246,000 net interest income, which was an acceleration from the less than C$100,000 in the entire first semester of the year. And as interest rates continue to increase, Century Lithium will likely see its quarterly net interest income remain stable and earn close to C$1M per year on its cash pile (until it starts to use the cash, of course).

Conclusion

While we don’t expect Century Lithium to be immune to recent inflation-related shocks leading us to use a 50% increase of capital expenditures and operating expenditures, we actually expect the after-tax NPV8% to increase in the upcoming feasibility study as the lithium price increases are strongly outpacing the cost increases, the net result should be positive. Using a lithium carbonate price of $20,000/t we anticipate the after-tax NPV8% to come in between $1.5B and $2B. Using $22-24,000/t, the after-tax NPV8% should exceed US$2B.

Of course, that is just based on our back-of-the-envelope calculations (and definitely not the company’s official guidance) and the proof of the pudding will be in the eating (i.e. we will have to wait for the feasibility study to be published to see what the actual results are). But seeing how the company has made great progress in advancing the project and de-risking the flow sheet we don’t anticipate any major issues. The decreasing lithium price also doesn’t really worry us as the margin of safety is still pretty impressive: the current spot price of lithium carbonate is still about double the $20,000/t we believe offers an acceptable base case projection.

Disclosure: The author has a long position in Century Lithium. Century Lithium is a sponsor of the website. Please read the disclaimer.