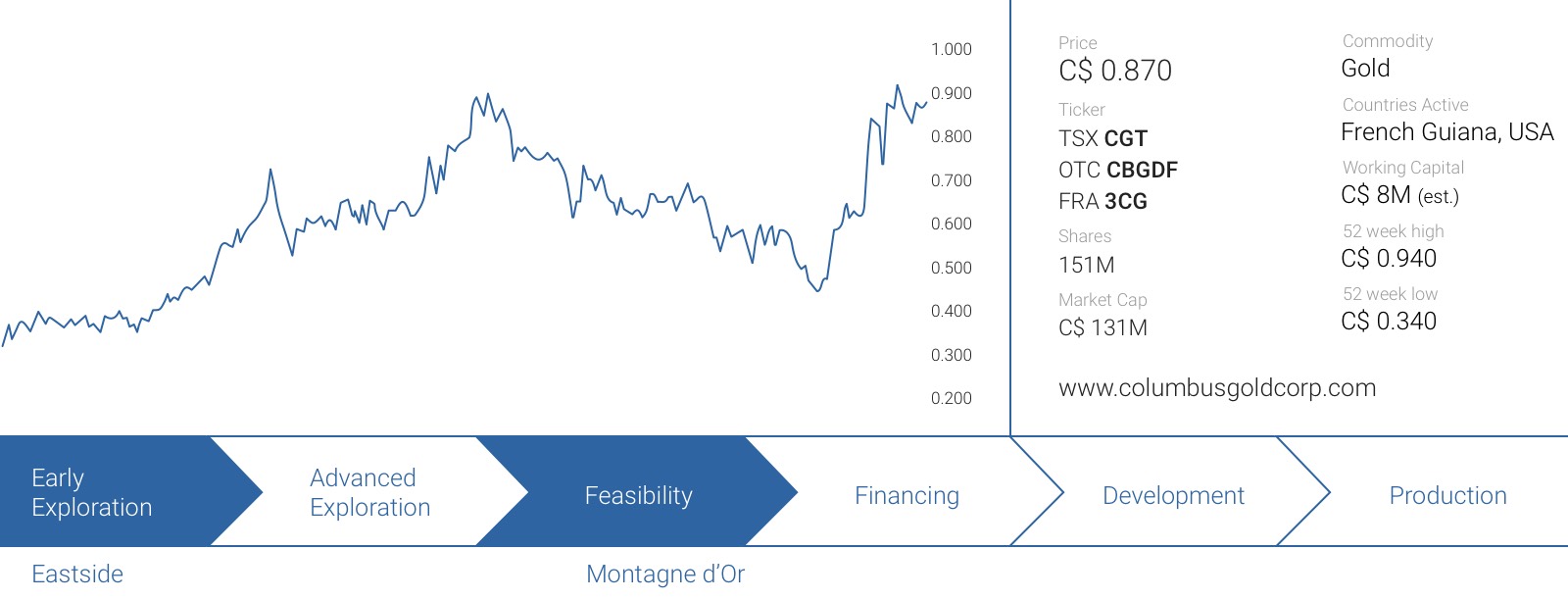

Columbus Gold (CGT.TO) is now looking forward to seeing the results of the Bankable Feasibility Study on its Montagne d’Or gold project in French Guiana. That feasibility and the likely subsequent sale of its remaining 44.99% interest are very likely the main catalysts of this company, but let’s not forget about its Eastside project in Nevada.

After making the original discovery in 2013, Columbus Gold started a substantial drill program which resulted in a maiden resource estimate on the property. This was a game-changer as Columbus Gold was pretty much a one-trick pony with the advanced-stage Montagne D’Or project and a portfolio of early-stage exploration projects in Nevada. This has now changed, as the company is now zeroing in on one million in-pit ounces in the mining-friendly state.

The maiden resource estimate at Eastside’s Original Target looks promising

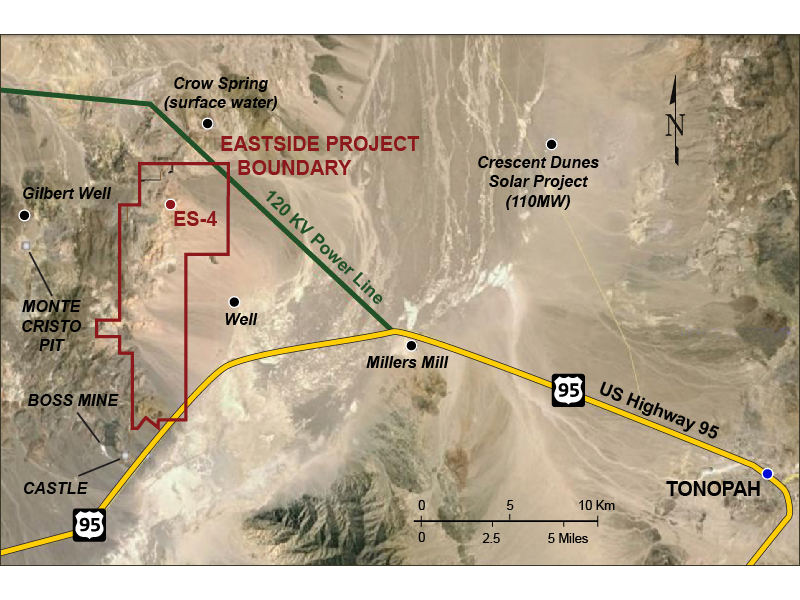

As a brief reminder, the Eastside project is located in the southwestern part of Nevada, less than 40 kilometers west of Tonopah, with highway 95 and a 120 kilovolt power line running right through it (which obviously is a huge advantage).

After drilling 136 holes for a total of almost 37,500 meters (of which 24,000 meters were drilled in 2015 and 2016), Columbus wanted to see what exactly it was sitting on, and it engaged an independent consultant to calculate and publish a maiden resource estimate on Eastside.

Using a cut-off grade of 0.15 g/t gold, Eastside hosts just over 35 million tonnes of rock at an average gold grade of 0.57 g/t and 3.5 g/t silver. That’s an acceptable grade for a Nevada-based heap leach project (Rye Patch Gold (RPM.V)) is for instance advancing a heap leach project with an average grade of just 0.45 g/t). It will be important to see the expected strip ratio for this zone, as this will have an impact on the total mining cost, and thus directly on the required grade to be profitable.

But here’s the interesting thing. According to Columbus’ sensitivity analysis, even if you would increase the cut-off grade by 67% to 0.25 g/t gold, you would still have 571,000 ounces of gold and 3.1 million ounces of silver. That’s just 13% fewer ounces, but the average grade increases by 42% to 0.81 g/t gold. MDA expects the total cost per processed tonne to be approximately $17 (keep in mind this excludes the mining cost for the waste rock, which is estimated at $1.35/t), which is attractively low. Even if you would apply a higher strip ratio of 6:1, the total production cost would still be approximately $25/t.

That won’t be enough to be profitable at $1200 gold in the base case 0.57 g/t scenario (where the gross rock value is just $22/t), but emphasizes the importance of A) the higher grade zones within the pit and B) the importance of the strip ratio, and we expect Columbus to try hard to optimize all aspects of the resource.

The resource estimate at the Original Target is just the first step, and Columbus Gold has outlined several high priority drill targets on the Eastside property which it intends to drill this year. We are specifically looking forward to see the so-called Target 5 being drill tested this year, and Columbus Gold has received a drill permit to complete 12 holes on this specific zone.

Screengrabs from the Eastside Gold Project youtube video

The acquisition of the adjacent historical resource is a good move

A few weeks ago, Columbus Gold announced it was able to acquire an existing historical resource containing 272,000 ounces gold, literally adjacent to the Eastside land claims. These 119 claims increase the total surface area of the Eastside project to almost 70 square kilometers, which is prime real estate given the existing infrastructure surrounding the asset.

The historical resources consist of three zones totalling 11.2 million tonnes of rock (we can’t call it ‘ore’ yet without a NI 43-101 resource estimate) at an average grade of 0.82 g/t gold which is substantially higher than the existing grade on the in-pit resource on the northern part of Eastside, so we do think this transaction does add a lot of value. Considering Columbus Gold has issued 1.75 million new shares to Seabridge Gold (SEA.TO, SA) to acquire 100% of the property (with NO cash payments at all), the company is essentially acquiring this historical resource for just US$5 per ounce in the ground, which is undoubtedly cheaper than discovering the same amount of gold.

We would also expect the strip ratio of these new zones to be lower as well, given the previous drill results which encountered 52 meters at 1.37 g/t gold at Castle (starting at just 64 meters down-hole) and 17 meters of 5.4 g/t gold at the Berg zone starting within 20 meters from surface.

This bodes well for the potential of the new claims, and Columbus Gold believes there’s a ‘good potential’ to increase the gold resource there, which, once converted into a NI 43-101 resource estimate, would push Eastside over the ‘magic’ 1 million ounce mark – with more to come!

The C$5M bought deal will be spent on Montagne d’Or as well

Columbus Gold has entered into a bought deal agreement with Beacon Securities to raise approximately C$5M in a straight share, no warrant deal. Even though the company still had C$3.6M in cash in the bank, it wanted to top up its treasury in anticipation of its Eastside and Montagne d’Or drill programs in 2017.

Some readers didn’t like the discount to the market price, but the offering was completed close to the VWAP price of the previous trading weeks, whilst the lack of a warrant reduces the overhang and the future pressure on the share price associated with warrant exercises.

The funds will immediately be used to start an exploration program on the Montagne d’Or gold project in French Guiana, where partner Nordgold is currently completing a feasibility study, which should be ready for publication this quarter. This feasibility study will be focused on the existing resources and reserves, as Nordgold didn’t want to waste any time with a regional exploration program.

However, Columbus Gold would obviously like to know what else Montagne d’Or might host (as this could help with a potential future sales process – keep in mind Nordgold has always acquired the project stake of any minority partner it had in its history). Proving up the value of the ‘greater Montagne d’Or region’ will be an important step to add more ounces to the mine plan at a later stage, which will boost the mine life.

Conclusion

The feasibility study at Montagne d’Or will be ready for publication within the next few weeks (Nordgold has until March to complete the study); we do expect the BFS to be slightly different than the Preliminary Economic Assessment. We wouldn’t be surprised to see the CAPEX increase due to the inclusion of a proposed transmission line connecting the project to the local power grid and the OPEX to increase from the AISC of $711 reported in the PEA. This could be perceived as ‘disappointing’ by the market, but keep in mind a PEA has a larger margin of error, whilst the results of the feasibility study will be much more reliable. We would like to see an after-tax NPV (6%) of in excess of $325M, and an IRR of in excess of 20%. Also keep in mind the feasibility study will be based on the reserve estimate, and will exclude the additional resources which could be included in the mine plan at a later stage.

The next few months will be very interesting as Columbus will undoubtedly attract a lot attention with an updated ‘tangible’ value for Montagne d’Or and a new drill program in full swing in Nevada.

The author holds a long position in Columbus Gold. The company is a sponsor of this website. Please read the disclaimer