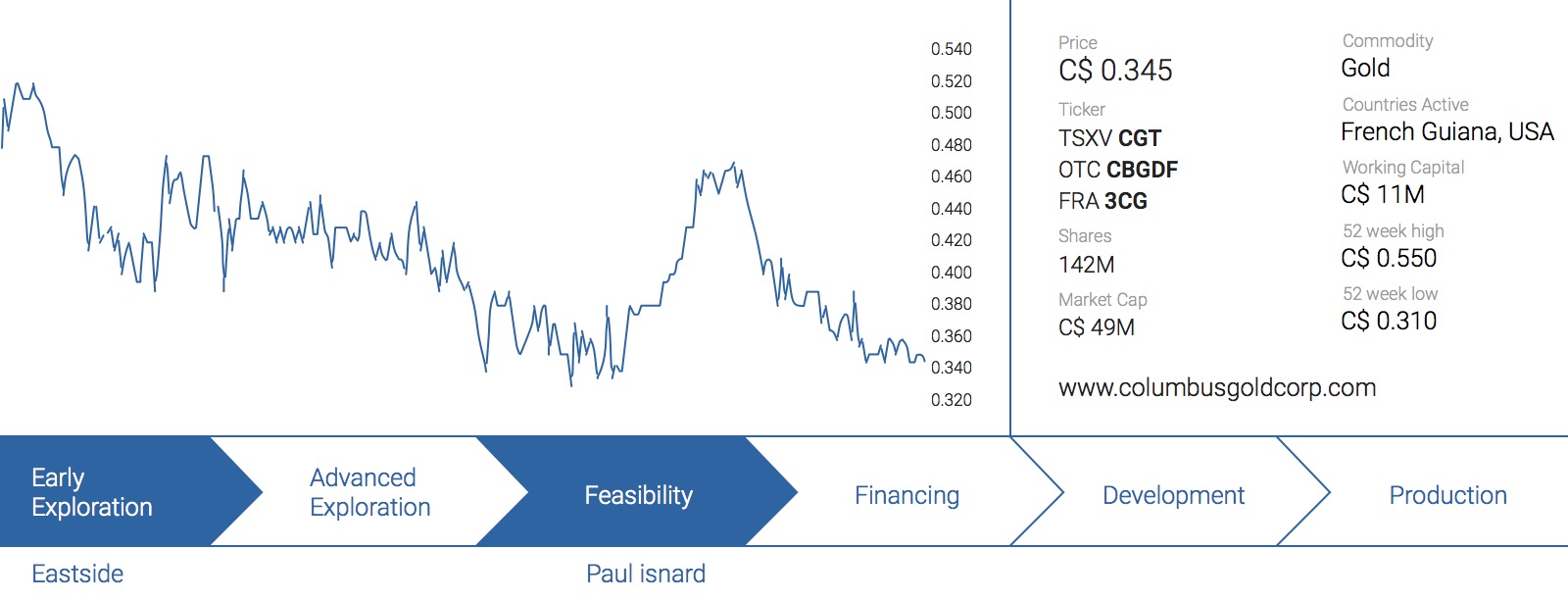

We have been supporting Columbus Gold (CGT.V) for several years now and have seen its share price move up all the way from C$0.20 to in excess of a dollar in 2011, only to fall back down to earth in the summer of 2013 (undeservedly so!). The share price has now been consolidating in a trading range of C$0.35-0.40 per share, and we believe this clearly undervalues Columbus based on the progress made to date, and more specifically the recently received US$6M for selling a 5% equity stake at the project level in the Paul Isnard Gold Project to joint venture partner Nord Gold. Once again Columbus was able to finance the company’s activities with limited to no dilution (lets talk about that later in this update). Also interesting in the recent transaction is that Nord Gold is taking over as operator of the asset immediately. All this adds up to a clear intent to own this project outright, as we predicted the moment Nord Gold was announced as Columbus’ joint venture partner.

View PDFThe developments at Paul Isnard

Back in late 2013, Columbus Gold was attracted the Russian senior producer Nordgold (“Nord”) as a partner for the Paul Isnard project whereby Nord could earn a 50.01% stake in the project after spending at least $30M in the property and completing a Feasibility Study (“FS”) by 2017. In March 2014, after extensive due diligence (and other groups still looking to get involved with the asset), Nord Gold signed the definitive agreement beating other potential partners. Since then, Nord and Columbus together have been focused on accelerating on alllevels to get this asset to Feasibility Stage.

Nord hasn’t wasted any time and spent $16M on the property in 2014 (including a US$4.2M cash payment) and was up to approximately $US25Mby the end of 2015 (according to Columbus’ management team). The ongoing infill drill program, ongoing power studies and engineering studies to complete the FS three to four months ahead of schedule (end of 2016 instead of H1 2017) leads us to believe Nord will incur between US$34 to $38M in Paul Isnard-related expenses by the end of this year. This clearly indicates Nord won’t be walking away anytime soon. The Paul Isnard would increase Nord’s annual production by nearly 30% in one year, thus a key strategic development project in their pipeline. At completion of the FS, Nord would now have 55.01% of the asset.

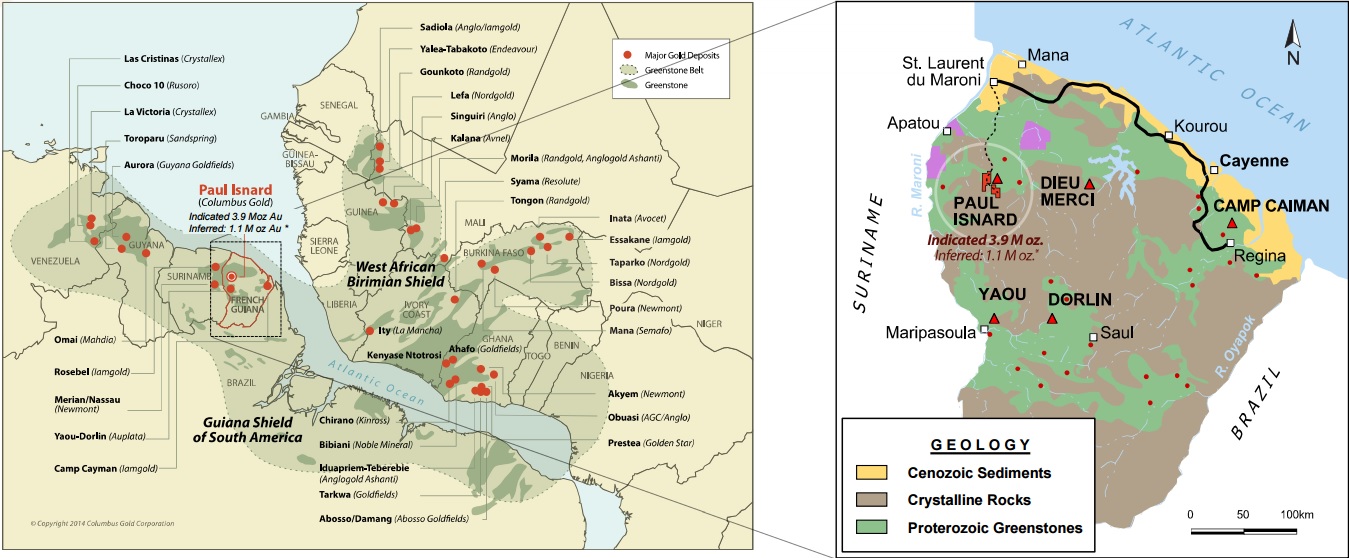

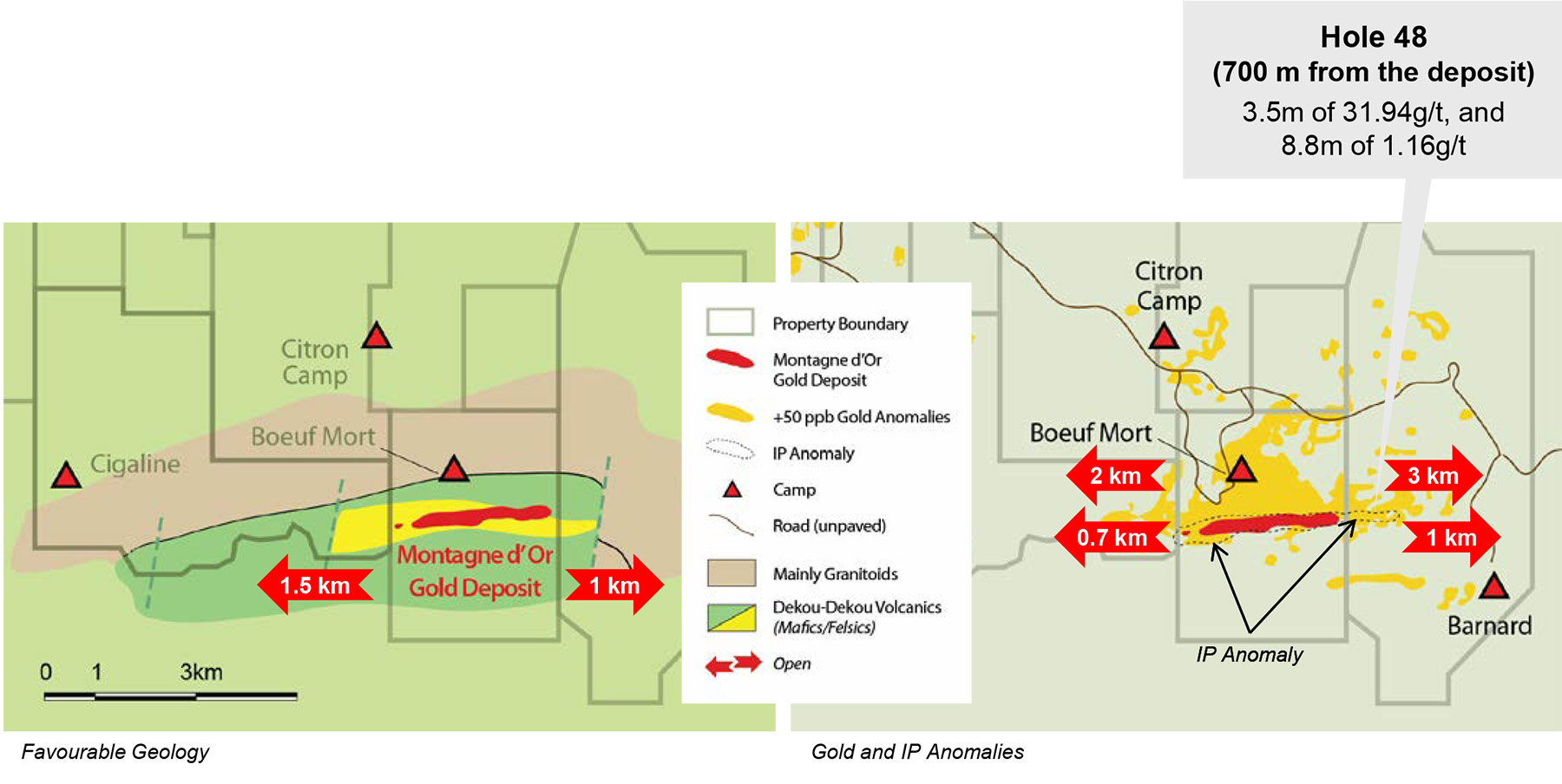

Just as a reminder, the Montagne D’Or project (also called ‘Paul Isnard’, our preferred name) currently contains 5 million ounces of gold, of which 78% is located in the indicated resource category. With a strike length of 2,300 meters and having been explored to just 250 meters below surface, we remain committed to our exploration target of 8 million ounces at Paul Isnard but given the current climate in the gold sector and the fact the project has already reached the ‘critical mass’ to start thinking about developing it, the focus has moved towards infill drilling rather than expansion drilling. The positive side of the infill program and size of the asset is the capital required to put this asset into production.

Across the border in Suriname, Newmont Mining (NEM.TO; NEM) is building the Merian project for close to a billion dollars, where the grade is ~1.2 g/t. Building a large project like this for this amount of capital with a lower quartile grade usually runs into problems BUT sitting across the border in French Guiana, Paul Isnard’s head grade is nearly double the grade at around 2.0 g/t and will cost US$325M to $US350M, or nearly 1/3 of Merian.

Life of Mine average annual production for Merian is 300koz to 400koz, whilst Paul Isnard will produce almost 300,000 ounces of gold on an annual basis as well. So the project has almost twice the grade, 1/3rd of the capital cost and will produce almost as much as Merian.

Additionally, the recently-purchased 5% stake by Nord Gold will also reduce Columbus’ capital requirement by approximately $17.5M should both partners decide to jointly develop the asset.

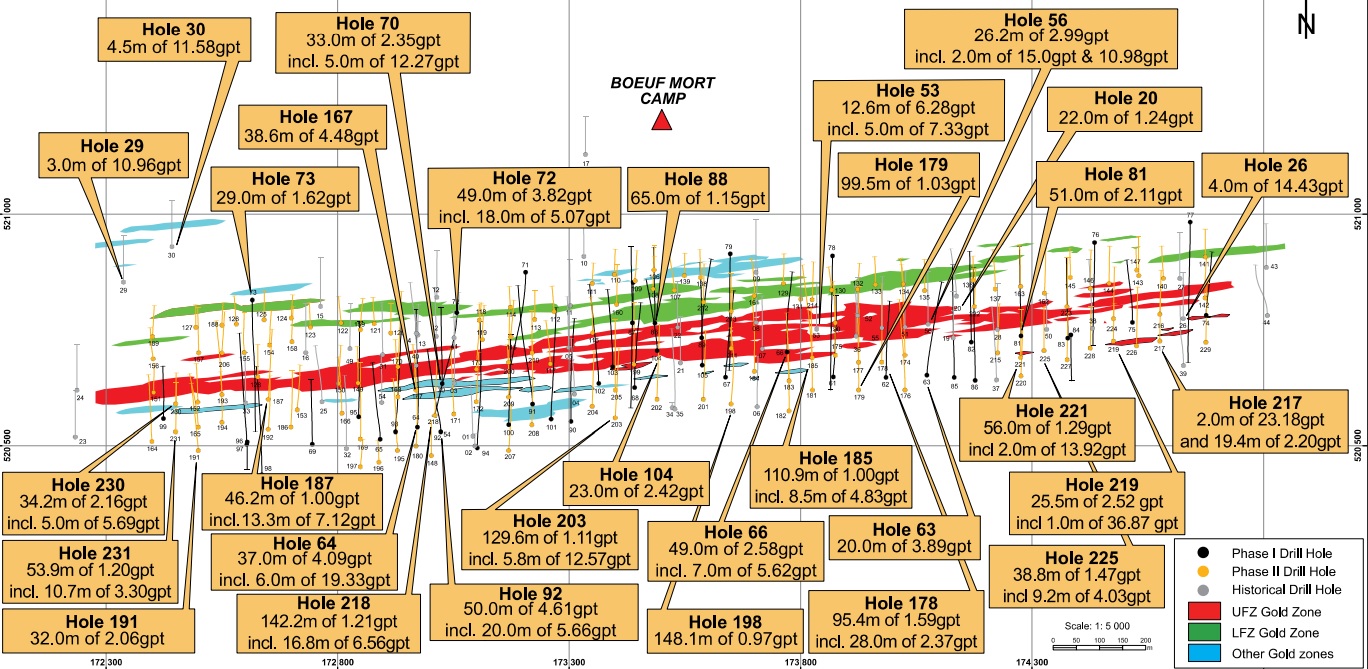

The infill drill program has been pretty successful to date. Drill results that have been released so far are all confirming the continuity of the currently known mineralization including 40 meters at 1.95 g/t and 21 meters of 2.47 g/t. Even though we didn’t expect to see anything else but decent gold grades, it’s always great to see the expectations being confirmed.

As the infill drill program in 2015 was aiming to reduce the spacing in between holes to a grid of 50 X 25 meters, we would expect a substantial part of the indicated resources to be upgraded to the measured category with an additional reduction in the inferred resources. This will increase the credibility of the resource estimate and will ultimately be beneficial to the feasibility study at Paul Isnard, which should be completed in 2017.

We must remember that the infill drilling is predominantly focused on the western portion of the deposit where the higher-grade starter pit will commence. As we continuously see positive results from this zone, it makes us more comfortable on the initial payback of the project, or overall general return from the initial first few stages of the pit as this starter pit will allow the project to increase the cash flows in the first few years of the mine life.

The Feasibility Study at Paul Isnard might be better than expected

Nord and Columbus Gold have already released a Preliminary Economic Assessment (PEA) at Paul Isnard, and even though the project is viable at US$1100 gold, there was no real ‘wow’-factor in the PEA. That is, until you start to dig a bit deeper and start to incorporate updated parameters in the study.

One of the key aspects of the study and operation wefound very interesting is the head grade of the deposit into the mill. At a head grade 2.0 g/t Au for the first 10 years, it makes the operation one of the highest grade open pits in all of the Americas. The PEA really was a first pass and the level of accuracy of the expected costs hasn’t really been narrowed down. The capex of the processing plant, for instance, was estimated with an accuracy level of just 50%, indicating the final number might be quite a bit different from the US$136.7M used in the report. In fact, the entire PEA was built around an accuracy level of +-40% and as the mining sector hasn’t been performing well lately, the effective capex might very well come in at the lower end of the expectations considering the pressure on the prices of mining-focused equipment and infrastructure.

Additionally, Columbus has recently announced it has engaged Brussels-based Tractebel (a sub-division of Engie, a 40B EUR energy and utility conglomerate) to prepare a study to focus on the potential connection of the Paul Isnard project with the national power grid in French Guiana. According to the company, this would reduce the total power costs by approximately US$0.09/kWh (to US0.11/kWh) which would be a 45% reduction in the power cost (which is quite substantial, considering the total cost of power would be $6/t, which is 41% of the total production cost per tonne).

If Columbus would indeed be able to reduce its power costs, the total savings could be almost $50 per produced ounce of gold. Of course, linking the project to the power grid will have an additional cost, but based on our preliminary expectations this should be a double-digit number (we would be aiming for $75-90M) with a payback period of around 7 years. This doesn’t mean Columbus Gold will be able to remove the diesel-powered generators from the initial capex, as those will very likely have to stay in place as some sort of back up plan.

It will be very interesting to see the trade-off of committing to the additional capex to connect the project with the power grid versus the opex savings throughout the mine life. And there’s only one golden rule here, the longer the mine life at Paul Isnard, the better the returns on investing in the grid connection. We think that if the additional capex remains limited to just $80-90M, Nord will undoubtedly opt for the grid connection as the undiscounted LOM cost reduction would be $70M (in the 13 year mine life scenario).

We are also interested to see if the government subsidizes part or all of the grid connection noting the employment created at the mine site (up to 700 to 1000 full time), taxes generated and over all expenditures at the project of ~US$2.2B over the life of the mine. It will be one of the most significant projects in French Guiana in over 20 years and of significant importance to the overall economy.

Additional cost savings are quite likely as SRK (who completed the feasibility study) has budgeted $25M for road upgrades, which seems to be a pretty conservative estimate. On top of that, the final outline of the open pit might have a considerable impact on the scope of the project and the economics. Saprolite drilling could add more ounces to the mine plan and reduce the total amount that will have to be spent on pre-stripping activities.

There’s one thing that isn’t working in Columbus’ favor and that’s the currency exchange rate as the PEA already took a relatively favorable EUR/USD exchange rate of 1.06 into consideration.

The recent 5% sale puts a fair value on the project, much higher than Columbus’ current market value

Columbus Gold wanted to top up its treasury to make sure the market wouldn’t start to bet against the company and instead of issuing new shares, it reached a deal with Nord Gold whereby the latter will acquire an additional 5% stake in Paul Isnard for a cash payment of US$6M.

This proves two things. First of all, Nord Gold is still very keen to continue to work on Paul Isnard and apparently was quite eager to increase its stake in the project (which strengthens our belief Nord Gold will eventually want to consolidate the full ownership of the project). Secondly, the value of the project is increasing, despite the lower gold price. In the original deal, Nord Gold could earn a 50.01% stake by completing US$30M in exploration expenditures to advance the project, which implies a price of US$3M per 5% stake. As the additional 5% in the project has now been sold for US$6M, Nord Gold has been willing to double the value it’s assigning to Paul Isnard, undoubtedly caused by the higher resource estimate, exploration potential and the completion of a PEA, which proved the economics of Paul Isnard.

If we’d now use this C$8.6M as base case valuation for the project, Columbus’ remaining 45% interest (well, 44.99% to be correct, assuming the transaction closes) would have a value of almost C$76M. If you’d apply an additional 25% premium for completing the feasibility study (increasing the confidence in the project), Nord Gold shouldn’t have any issues to pay (at least) C$95M for the remaining 45% of the project it won’t own after it completes the earn-in phase. Of course this excludes any movement in the gold market over the next year. If gold moves upwards, it’s pretty obvious the value of the Paul Isnard project will increase exponentially.

And this is exactly why we were excited (and jubilant) when Nord Gold was announced as the company’s joint venture partner. Nord Gold is an extremely profitable company with a very smart management team. As the company is involved in just a few projects outside of Russia, it is able to focus on those specific operations and has really been able to outperform based on the expectations. Nord Gold never goes on an acquisition spree, but targets just a few companies per decade with projects that have the potential to be a long-term producer. Nord Gold got into bed with Columbus Gold when Paul Isnard had a resource estimate of 1.9 million ounces and has increased the total resources to 5 million ounces, but we think there’s much more ‘gold in them thar hills’.

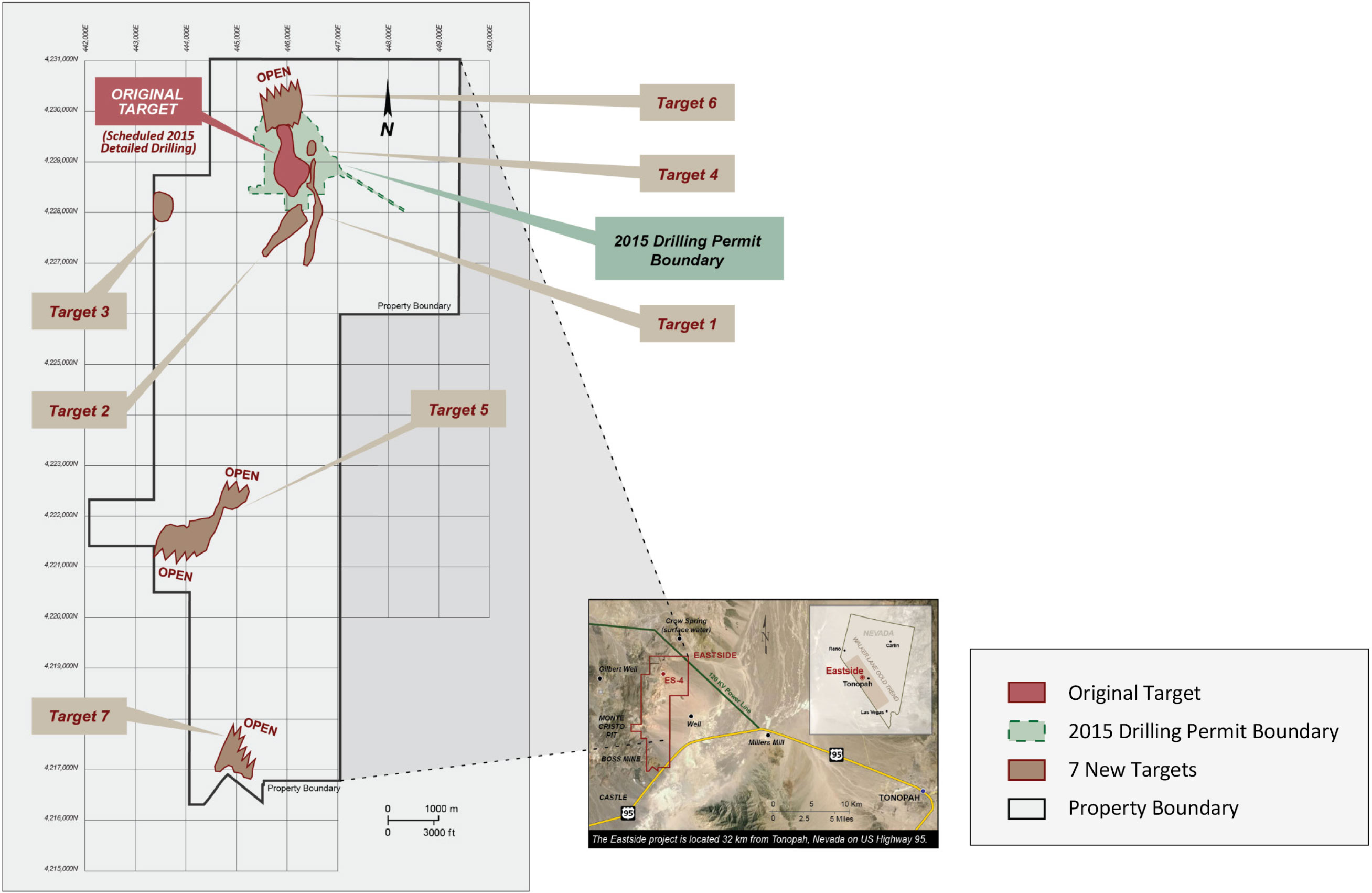

Eastside is shaping up to be humongous, and Columbus will chase a higher-grade area at depth

The sale of the 5% stake will increase Columbus’ cash position to almost C$10M (as the Company has also received a first payment of C$75,000 in cash from the sale of the Mogollon project), and this will put the company in a comfortable position to continue its exploration activities at Eastside, Nevada.

The 2015 drill results at Eastside were very impressive as they have now confirmed the existence of a significant mineralized system and footprint, which could be mined as a bulk tonnage heap leach operation like the neighbouring Round Mountain a few kilometres to the north west, which is the largest heap leach gold mine in the world (keep in mind no official technical studies have been completed to determine the viability of Eastside).

The most recent exploration results are indicating there seems to be some sort of lower-grade mineralization on top of what could be a substantial higher-grade target at depth. We expect Columbus Gold to follow up on the deeper drill targets in 2015, and CEO Robert Giustra told us the company has budgeted a staged US$5M for additional exploration activities at Eastside. 2016 will be an important drill season for Columbus because all bets are off if a higher-grade zone at depth could indeed be confirmed.

Keep in mind Eastside could be massive as the mineralized area has now been traced and confirmed over in excess of half a million square meters and on top of that, it’s still open in all directions, indicating Columbus is already sitting on in excess of 100 million tonnes of gold-bearing rock.

We are quite excited about the potential at Eastside as not only has the gold mineralization now been traced over a substantial surface area, Columbus Gold still has several other drill targets to follow up on. Additionally, the Eastside project has access to state of the art infrastructure and on top of that, the nearby valley is known to have shallow water available.

Access to the property? No problem with a highway just 10 kilometers away. Power? Not an issue, as there’s a transmission line running right through the project. The location of Eastside sounds like a dream, and we’ll keep a very close eye on the results of this year’s exploration program because if a higher-grade zone could be defined underneath the currently known lower-grade mineralization, Eastside might be the discovery of the decade.

")

Conclusion

The lowest valuation we’d give Columbus Gold right now is C$95M (or $0.70/share). That’s not a number we are pulling out of thin air, it’s just a 25% premium on top of the most recent project valuation by joint venture partner Nord Gold. Keep in mind, Nord Gold has always bought out its minority partners in the past and by recently acquiring an additional 5% stake at twice the valuation of the earn-in deal, Nord is showing its commitment to the project and is willing to pay a fair price to consolidate the ownership.

Keep in mind this first target of C$0.70 per share is only based on the value of Columbus’ stake in the Paul Isnard project and doesn’t take the Eastside project into consideration at all, so the 70 cents really is the minimum minimorum for us. Robert Giustra and his team have been executing all plans at Paul Isnard for several years now, and we feel we’re nearing an apotheosis, and still think Nord Gold will acquire 100% of the asset within 12-18 months from now.

The author holds a long position in Columbus Gold. They are a sponsor of the website. Please read the disclaimer