Most mining CEO’s seem to think their own project is the best project in the world, but in Core Gold’s (CGLD.V) case, it’s easy to see why the claim is being made. After taking over Dynasty Metals & Mining (which was essentially a failed company) in 2016, CEO Keith Piggott started to immediately turn things around. Laborers got paid, a new mine plan was executed on a high grade open pit operation at Dynasty Goldfields rather than the erratic veins of the Zaruma underground mine, and historic debts are being paid off. On top of that, the company continues to invest in its infrastructure and has plans to reach a steady state production rate of 50,000 ounces per year from next year on.

Most mining CEO’s seem to think their own project is the best project in the world, but in Core Gold’s (CGLD.V) case, it’s easy to see why the claim is being made. After taking over Dynasty Metals & Mining (which was essentially a failed company) in 2016, CEO Keith Piggott started to immediately turn things around. Laborers got paid, a new mine plan was executed on a high grade open pit operation at Dynasty Goldfields rather than the erratic veins of the Zaruma underground mine, and historic debts are being paid off. On top of that, the company continues to invest in its infrastructure and has plans to reach a steady state production rate of 50,000 ounces per year from next year on.

You might remember Piggott from Goldgroup Mining (GGA.TO), where he discovered, drilled and tried to get the Caballo Blanco gold project in Veracruz going. Political games prevented this and although we remain convinced about that project’s potential, the acquirers of the project haven’t been able to develop the project either.

We remember a conversation we had with Piggott at the 2015 PDAC conference, where he brought up Ecuador as ‘the last frontier’. Indeed, Ecuador had just opened up to foreign investment in the mining sector, and although we were a bit wary at first, Keith Piggott jumped in with both feet and has been building a lot of goodwill and credit in the country ever since. An excellent testimony to this is the fact Core Gold is operating the ONLY open pit gold mine in Ecuador…

Reviving a failed company: an open pit, and a bigger mill

To fully understand the story of Core Gold, we have to go a few years back in time. In 2016, Dynasty Metals & Mining was about to go belly up, as it was unable to make an underground mine with an average grade of in excess of 10 g/t work. A pity, not just for its shareholders, but also for its contractors and laborers which hadn’t been paid for months. Until Keith Piggott entered the scene.

To identify why Core Gold could be successful, we first have to understand why Dynasty failed.

We believe the issues encountered by Dynasty were all boiling down to two issues: the capacity of the processing plant and the decision to pursue mining at the Zaruma underground mine.

Let’s start with the latter. Although the gold-bearing veins at Zaruma were pretty rich (the NI43-compliant resource at Zaruma contains 6.3 million tonnes at an average grade of just over 12.5 g/t gold), the veins appeared to be erratic, and Dynasty was never able to make it work.

Rather than breaking their heads over an underground vein deposit, Core Gold switched gears and decided to use the existing Portovelo processing plant to process the ore from the Dynasty Goldfields project. Low-hanging fruit, indeed, as this open pit operation has a resource estimate with an average grade of 4.5 g/t gold (surprisingly, the grade reconciliation based on the head grades delivered to the mill is pretty strong, indicating the resource estimate appears to be very reliable). After accounting for some mining dilution (some waste rock gets scooped up by the excavators as well), the average head grade of the rock delivered to the mill is approximately 3.2 g/t. So when CEO Piggott described the Dynasty Goldfield project as ‘this is dreamlike’, we understand where that’s coming from: there aren’t a lot of open pit mines delivering a head grade of in excess of 3 g/t to the mill.

Instead of chasing the high-grade veins at Zaruma, Core Gold opted for the ‘easier’ mine plan and this is paying off right away with a consistent production rate of 20-25,000 ounces per year (and a FY 2018 production guidance of 22,000-26,000 ounces of gold).

A second issue was the Portovelo plant. Whilst a mine plan to chase high grade veins could have worked if Dynasty would have had a better grade control system in place, the current capacity (750 tonnes per day) of the mill is a bit on the lower end of the spectrum to make sure an open pit mine 120 kilometers away remains profitable. The only way to solve this issue is by expanding the plant.

The gold production rate should increase sharply once the Portovelo mill upgrades will be completed

Core Gold realizes this and is working to get everything in place to expand the capacity of the Portovelo plant from 750 tonnes per day to 2,000 tonnes per day. Almost tripling the capacity of the plant will unlock additional economies of scale whilst allowing the average recovery rates to increase to 90-92%.

This also means Core Gold will have to ramp up the mining rate at Dynasty. The Ecuadorian mining law allows mid-scale companies to extract 1,000 tonnes per day per concession as part of its plan to get the industry going. So technically, Core Gold will have to mine from three different concessions to make sure it remains compliant with the small scale mining law (this shouldn’t be an issue as Core Gold continues to discover more veins on the properties). Another option further down the road could be to re-open the Zaruma mine to ‘fill the mill’, but we have the impression this isn’t high on Core Gold’s priority list. A third option would be to use the ore from the newly discovered Linderos project and truck it to the Portovelo plant as well.

Portovelo Mill and Plant

It’s also interesting the deal with the contract miner, Green Oil (which operates the mine in return for 40% of the gold sales and 10% of the silver sales) is expiring in H1 2019. As Core Gold will have to make sure it can mine the full 2,000 tonnes per day (and preferably a bit more to make sure there’s a stockpile readily available), it will have to either start purchasing its own equipment or re-negotiate the deal with Green Oil (to reduce the contractor fee).

Expanding the mill will cost money, and that’s why Core Gold is planning to enter into a $15M credit facility with Credipresto, a Mexican lender associated with Javier Reyes, a director of Core Gold and a former director of Goldgroup Mining as well, so his ties with Keith Piggott appear to be pretty strong. According to the use of proceeds of the $15M credit facility, US$7.5M will be used to repay (historic) debt and boost the working capital position.

The effective execution of this credit facility has been delayed as Investabank/Credipresto needs senior security over the assets, but due to the local subsidiaries still being subject to a repayment schedule, this seniority could not yet be granted. We hope to see a solution sooner rather than later, as that $15M would provide a very welcome boost to the working capital, and allow Core Gold to aggressively advance its project portfolio on all levels.

Paying off the historic debt: a key component of getting the operations back on track

There are two golden rules when doing business in South America: make sure you keep the local communities informed about every step you intend to take. And pay your staff.

Frankly speaking, Piggott and his team inherited a mess. The laborers hadn’t been paid for seven months, whilst a local subsidiary of the company, Elipe SA, was on the brink of losing its mining concessions. Piggott was immediately on top of this and negotiated a payment schedule to extinguish the debt. The original agreement called for monthly payments with a US$3.8M balloon payment in June.

This would have been tough to achieve, and Core Gold elected to renegotiate the repayment schedule to ensure it would be able to live up to its promises. Fortunately, the government-appointed representative has been willing to cooperate, and agreed to a new repayment schedule. This will cost Core Gold more money, but allows it to spread its payments out in time. Core Gold is also buying more time, as the June-August payments will be 3 times $400,000 (compared to $650,000 per month in Q1), giving Core Gold some more room to breathe.

It’s important for Core Gold to ensure it can meet the payment schedule as technically, the government representative might just take the assets away and monetize them to ‘fill the gap’. That’s a worst case scenario but given A) Core Gold has been a loyal and credible payer since the new management came in and B) the government representative has agreed to the new payment schedule, we are confident both parties will continue to cooperate. Elipe’s creditors will get their money, whilst Core Gold continues to be allowed to keep its concessions (and mine them).

Additional upside will come from the exploration properties. About Linderos and Copper Duke

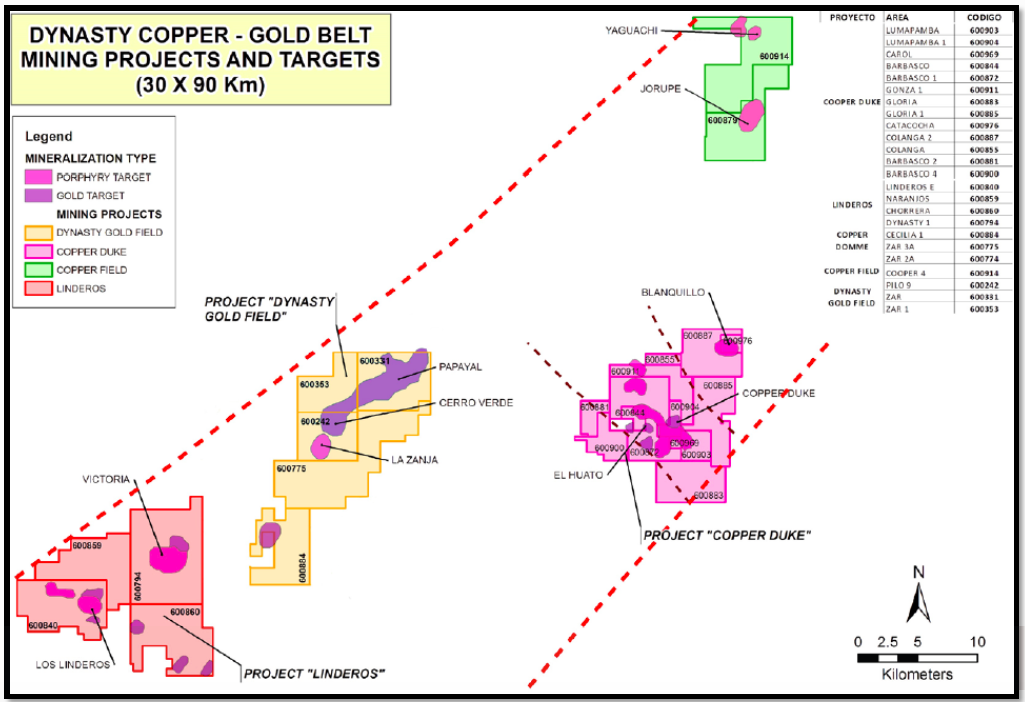

Although we feel the Dynasty Goldfields project (and the mill) by itself already underpin the current valuation of the company, we would like to draw your attention to the two exploration projects in CGLD’s portfolio; Linderos (which could provide additional mill feed for the Portovelo plant) and Copper Duke (which could host an exciting copper-gold porphyry system).

Linderos

The Linderos gold project is a new discovery, made by Core Gold in 2017 as part of a regional mapping and sampling program. Core immediately followed up on the assay results by a trenching program where the results confirmed the existence of a large-scale gold system.

The total strike length of the main mineralized zone now appears to be well in excess of 1 kilometer, but as a second parallel zone has now been discovered as well, all bets are off. Core Gold has applied for a drill permit as the Linderos project has the potential to add a million ounces of gold or more to the ‘greater Dynasty Goldfields’ project area.

The gold-bearing layer on surface appears to be fully oxidized, which is another important advantage as it indicates the project could be brought into production as a heap leach project. That being said, we aren’t sure how the permitting process for a heap leach mine in Ecuador would work, so it’s perhaps more likely we will see the Linderos project being used to provide mill feed to the Portovelo plant. Perhaps a simple concentrator (at a mid-single digit cost price) could be a good addition to make sure the economics of trucking Linderos rock to the Portovelo plant would make sense.

Having now received its drill permits Core Gold is presently commencing an initial drill program using 20 by 50 meter spacings to figure out the potential depth of the mineralization.

Copper Duke

Linderos sounds exciting and could be a nice addition to the existing Dynasty Goldfields operations, but what really excites us is the Copper Duke exploration project.

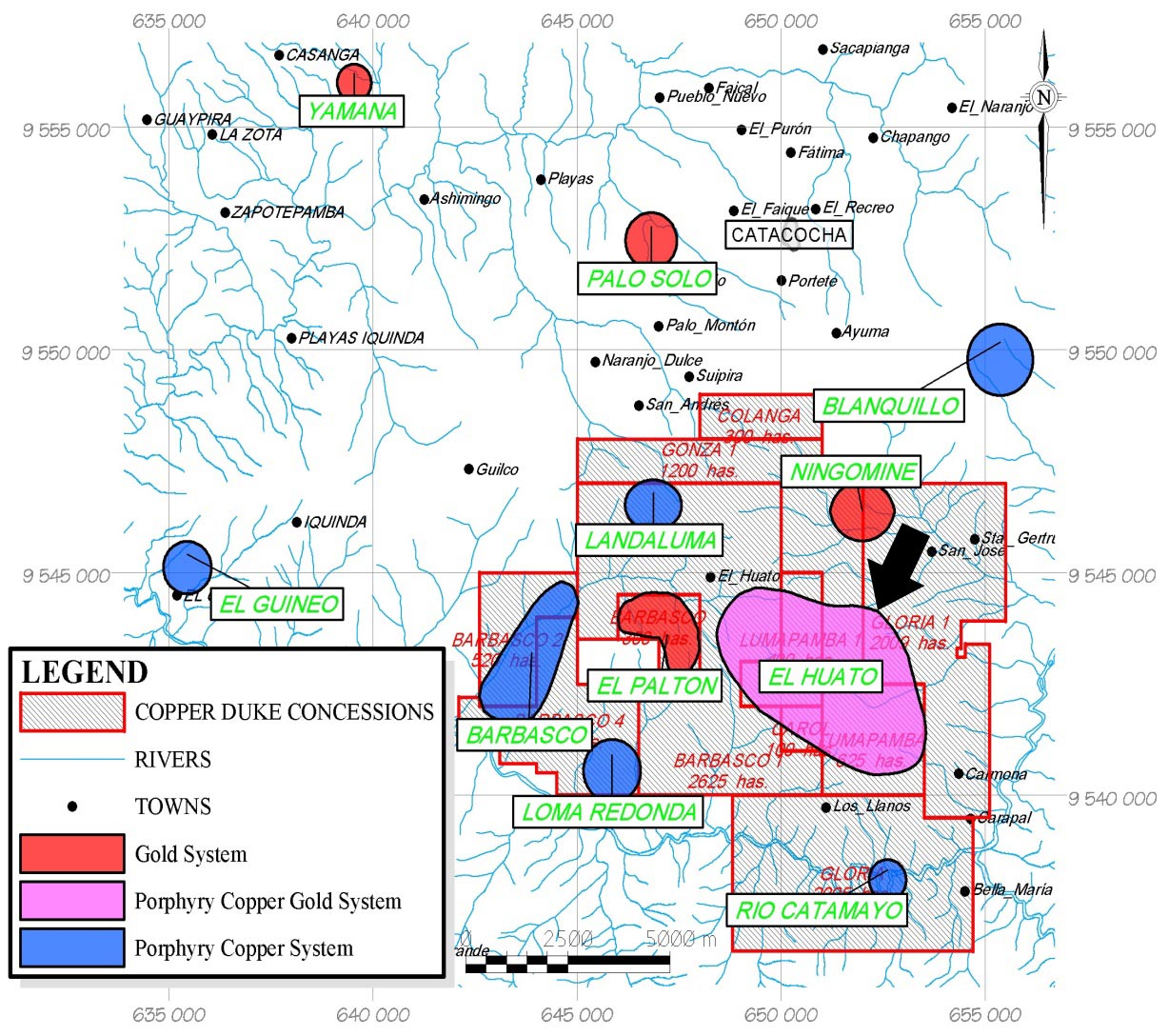

Copper Duke is located within hiking distance (less than 20 kilometers) from the Dynasty Goldfields zone and consists of 100 square kilometers divided over 13 mineral concessions. Although this is one of the more exciting drill-ready copper-gold porphyry exploration targets in Ecuador, very little work has been done to advance the property.

Core Gold’s first objective was to get the operations up and running and generate cash flow. As everything seems to be going according to plan on the gold production front, Core now has the time (and financial flexibility) to start a thorough exploration program at Copper Duke.

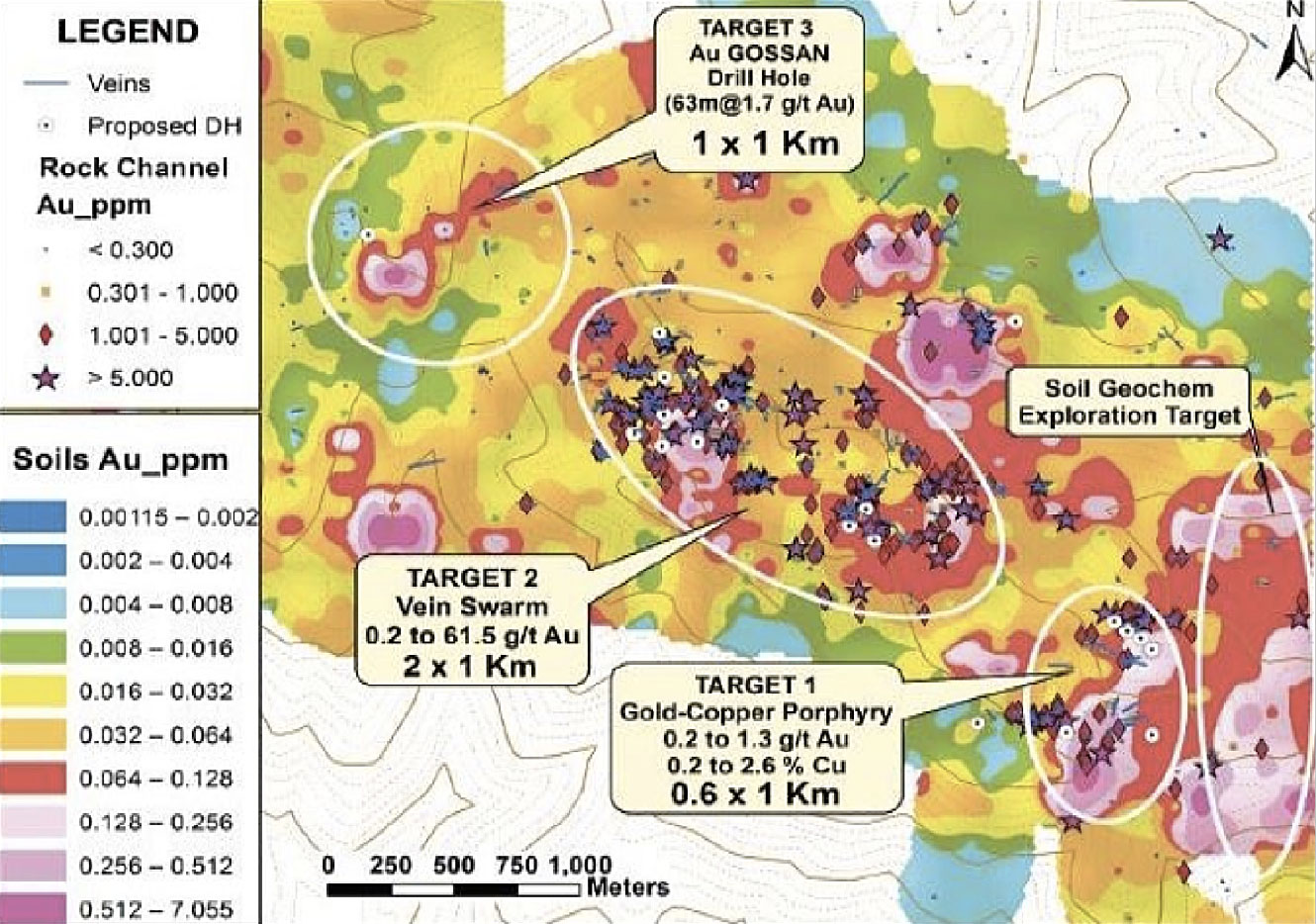

It recently received the final permits for a 15,000 meter drill program, and it won’t be easy to determine where to drill first considering there are plenty of high-priority drill targets on the property. The El Huato target (highlighted by the yellow arrow on the previous image) is the main target, but even this zone is sub-divided in several large mineralized footprints. As you can see in the next image, El Huato itself consists of 4 interesting zones, of which ‘Target 2’ appears to be very intriguing given its size (2 square kilometers) and previous sampling results.

Surprisingly, the El Huato target was already discovered 50 years ago, but very little work was done in the subsequent decades before Core Gold’s predecessor picked up the concessions and completed a sizeable sampling program in 2006 and 2007. The results of these sampling programs are highlighted on the previous image as well, and the gold (and silver) mineralization appears to be wide-spread. And it’s not just gold. A subsequent trenching program also confirmed the presence of copper, as a trenching interval of 15 meters containing 2.9% copper is hardly anything to sneeze at.

And this wasn’t just a ‘lucky hit’. The previous image contains a bunch of assay results from the same trenching program, and you can clearly see the high copper values (we highlighted).

These sampling and trenching results also grabbed the attention from Ian Telfer, 11 years ago. In 2007, Dynasty Metals entered into an agreement to sell the Copper Duke project to a shell which was advised by Ian Telfer. Telfer’s comments speak for themselves:

But there’s another side note here. That shell was valuing the Copper Duke project at a stunning C$51M (85M shares outstanding at a 60 cent valuation), which is indeed more than Core Gold’s current market capitalization…

Rather than trying to sell the project again, Core Gold’s new management team decided to keep it, and seems to be determined to drill it off, in an attempt to define a world class epithermal copper-gold porphyry deposit. A ‘new Cascabel’ would be nice, but let’s not forget this is an early stage exploration project, so Core Gold will have to spend a lot of blood, sweat and tears (and money) to advance the property.

The share structure and management

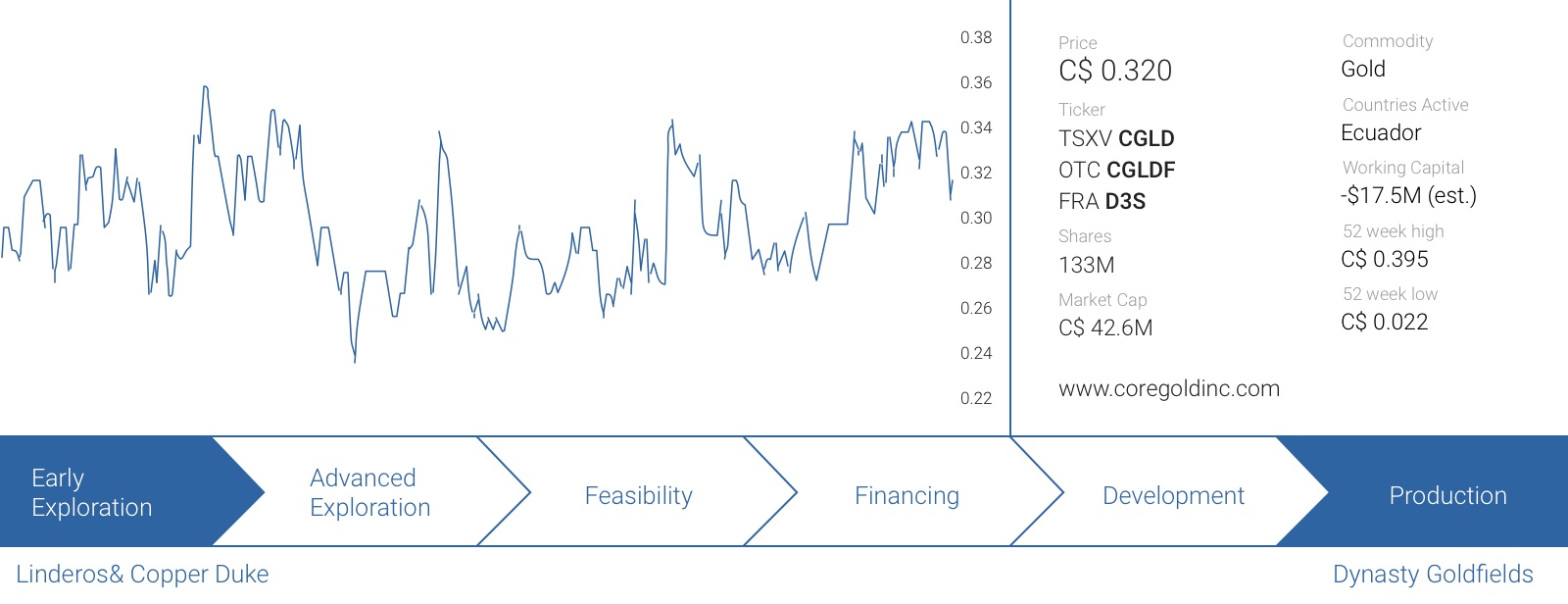

As of at the end of March, Core Gold had a total of 121.7M shares outstanding, but this increased after successfully closing a financing, raising C$3.3M by issuing 11.02M new shares at C$0.30 per share. This brings the total share count to approximately 133M shares, but also allowed Core Gold to further strengthen its balance sheet with the cash infusion.

It was refreshing to see Core Gold’s management and board invested even more of their own cash in the company. As you can see in the next table, Javier Reyes and Keith Piggott invested substantial amounts of money in Core’s 30 cent placement. Their interests are now very much aligned with the interests of shareholders, and that’s exactly what you’d want to see in a company.

Skin in the game, that’s what shareholders like to see.

We only see one issue, and that’s the fact the previous CEO of Core Gold still has a large share position and continues to sell stock. He doesn’t flood the market, but appears to be a ‘willing seller’ that will have to be crossed out at some point.

Keith Piggott – Director, President & CEO

Mr. Piggott initially made his name by developing innovative mining systems in the copper & cobalt mines of Zambia at Luanshya, and at Chibuluma, Chambishi and Kalengwa as Mine Superintendent. He then operated an exploration company in Australia and Papua New Guinea, identifying the gold cap of the Ok Tedi copper ore body, which was then dealt to BHP, which recovered two million ounces of gold in the first three years of production. Over the past 30 years, he has started and produced (mostly through companies that he has controlled) numerous gold/silver, tin, tungsten, rutile/zircon open pit and heap leach mines in Australia and Mexico utilizing innovative technology to maximize profits. He sold his Australian operations in 1987 to concentrate on developing metallurgical technologies, one of which is a patented dry processing for heavy minerals, which is used today in Australia and Mexico. For the last twelve years, he has focused on gold production in Mexico and on exploration opportunities for near-term gold/silver production in Mexico and Latin America. He has launched two Mexican gold mines which have each been in continuous production for twelve and five years, respectively. Mr. Piggott graduated in Mining Engineering from the Camborne School of Mines in the UK and from the Executive Development Program at the London Business School.

Gregg J. Sedun, LLB – Lead Director

Mr. Sedun is an independent venture capital professional based in Vancouver, Canada with 27 years of mining & industry-related finance experience. Upon graduating with a Bachelor of Law Degree (LLB), he practiced corporate finance/securities & mining law in Vancouver until retiring from law in 1997. Thereafter, he founded two private venture capital firms, including Global Vision Capital Corp., where he continues to carry on venture capital investing as President & CEO.

Mr. Sedun has been involved as a director and/or founding shareholder in a number of successful companies including Diamond Fields Resources Inc. (Founding Director) which was acquired by Inco in 1996 for $4.3 billion in the largest takeover of a junior mining company in Canadian history; Adastra Minerals Inc. (Founding Director) which was acquired by First Quantum Minerals in 2006 for $275 million; and Peru Copper Inc. (Founding Shareholder), which was acquired by Chinalco in 2007 in an all-cash $840 million takeover. Mr. Sedun currently serves on the Board of Directors of several publicly-listed natural resource companies.

Doing business in Ecuador. Easier than five years ago?

‘But, it’s Ecuador’. That’s a reaction we hear quite often. And admittedly, at first, we weren’t fully convinced Ecuador was serious about its intentions to become a mining destination in 2013.

2013 was an important year for the mining sector in Ecuador as this was the first time there was a clear distinction (and different permitting processes) between small-scale, mid-scale and large operations. And the law is actually pretty straightforward. A small-scale permit allows the extraction of up to 300 tonnes of material per day per concession (at a royalty rate of 3%) whilst a mid-scale permit allows for the extraction of 1,000 tonnes per day per concession with a 4% royalty payment due to the government.

There now is a clear system in place, and considering companies like Solgold (SOLG.L) haven’t encountered any resistance against their aggressive exploration plans in Ecuador (where it’s outlining a major copper-gold discovery), we are definitely giving Ecuador the benefit of the doubt. And it helps when the CEO of the company effectively lives in Quito, Ecuador.

Conclusion

One thing is pretty certain: Keith Piggott and his team saved Dynasty Metals & Mining and rebranded it to Core Gold whilst the company is slowly making progress on all fronts. Piggott inherited a disastrous balance sheet and a company on the brink on losing its licenses. The first thing Piggott did was starting to pay the workers, which was long overdue. The situation has normalized now, and the laborers appear to be very happy with the current work circumstances. If Teranga Gold and Golden Star Resources receive PDAC awards for corporate social responsibility, there’s no reason why Core Gold shouldn’t be nominated for a CSR award at one of the next editions of the PDAC Awards.

The next 12 months will very likely be a transition year. We hope Core Gold is able to sort out its US$15M Credipresto loan, as that will jumpstart all of its plans: the production capacity will be expanded, which will generate more cash flow, which could then be used on exploration programs. After all, Ecuador still is ‘elephant country’ as the lack of exploration and foreign investment over the past few decades makes this one of the ‘last frontiers’ which haven’t been thoroughly explored yet.

Core Gold is aiming to produce 50,000 ounces of gold per year at an operating cost of just $750/oz. Even if we would apply an all-in cost of $900/oz, at $1300 gold, Core Gold will be generating C$25M in net (pre-tax) cash flow on an annual basis. This would allow it to quickly clean up the balance sheet, settle every single dollar of historical debt, and spend several millions of dollars per year on exploration in the subsequent few years.

It’s now up to Piggott and his team to deliver on their promises, but we feel this might be a turning point for Core Gold as not only is the company on the brink of generating strong free cash flows, with the Linderos and Copper Duke projects, it has two very exciting exploration properties in its pipeline. And every single one of the mining/exploration assets (in combination with the Portovelo processing plant) could actually warrant the company’s current C$43M market capitalization.

Disclosure: Core Gold is a sponsor of this website, we have a long position. Please read the disclaimer