Lithium hasn’t been the ‘flavor of the month’ for several years now which means companies that weren’t serious about their ventures into the space or only had mediocre projects have exited the sector. The majority of the companies that are still around do have the assets that could be sought after once the pendulum swings into the other direction and lithium becomes more attractive again.

Cypress Development (CYP.V) was convinced about the merits of its project as a positive Preliminary Economic Analysis in 2018 confirmed the project was viable at a high-singe digit lithium price and as the company’s consultants were able to further optimize the flow sheet in the past 18 months, the project economics now look even more robust. The technical report of the pre-feasibility study has now been filed which allowed us to have a deeper dive into the economics.

The Clayton Valley project – a brief background

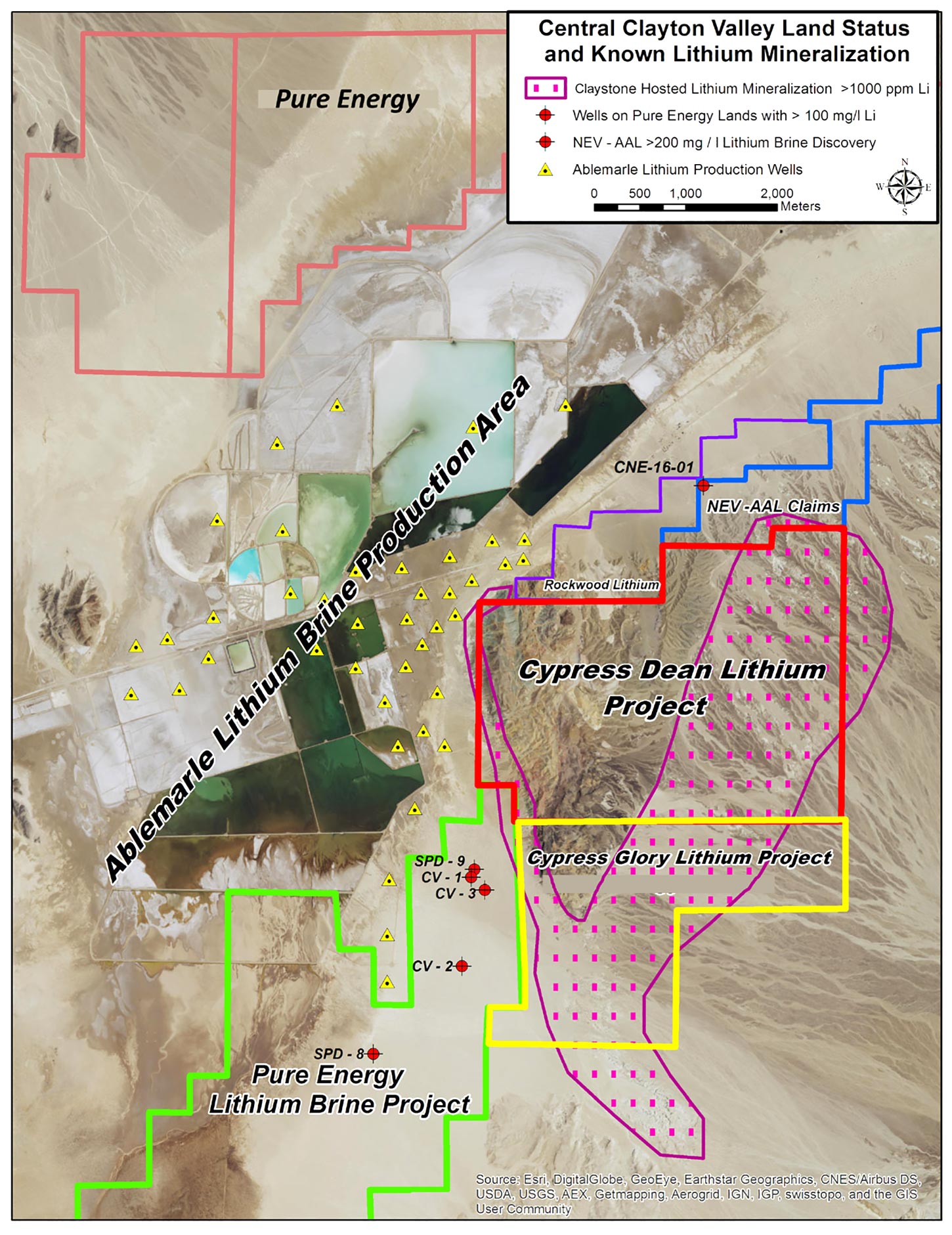

The Clayton Valley lithium project originally consisted of 139 placer mining claims and 178 overlapping lode mining claims for a total surface area of just over 5,400 acres. Clayton Valley is located almost just 60 kilometers southwest of Tonopah, which acts as a regional center for the mining industry in Nevada.

The project is also immediately adjacent to the Silver Peak lithium mine, currently operated by Albemarle (ALB) after its acquisition of Rockwood Holdings. Silver Peak is a classical evaporation-based lithium mine clearly visible on satellite images.

The Pre-Feasibility Study improves the economics

Before diving into the results, we would like to highlight the two main drivers of the improved economics.

The key element that has been a tremendous help in improving the economics is the average recovery rate. Since the PEA (which used a recovery rate of 81.5%) was completed, Cypress relentlessly worked on boosting those recovery results as it realized the key to rapidly improve the economics lied within those recovery results. After conducting additional metallurgical tests in 2019 the recovery rate was already boosted to 83% (+1.5%) but after yet another round of testing, the recovery rate was boosted to 86%. This is a pivotal point for the Clayton Valley project as Cypress will be able to recover 5.5% more lithium carbonate from the same amount of rock. Additionally, the acid consumption increased by just 1%, from 125 kg/t in the PEA to 126.9 kg/t in the PFS.

Secondly, an infill drilling program has confirmed the average grade of the Clayton Valley resource while converting virtually all inferred resources into measured and indicated resources. The indicated in-pit resource used for the PEA contained 200 million tonnes at 1,105 ppm lithium with an additional 107 million tonnes at 1119 ppm in the inferred category (for a combined 304 million tonnes in both categories). The resource used for the pre-feasibility now contains 594 million tonnes in the measured and indicated resources (+95%) at an average grade of 1073 ppm (-3%).

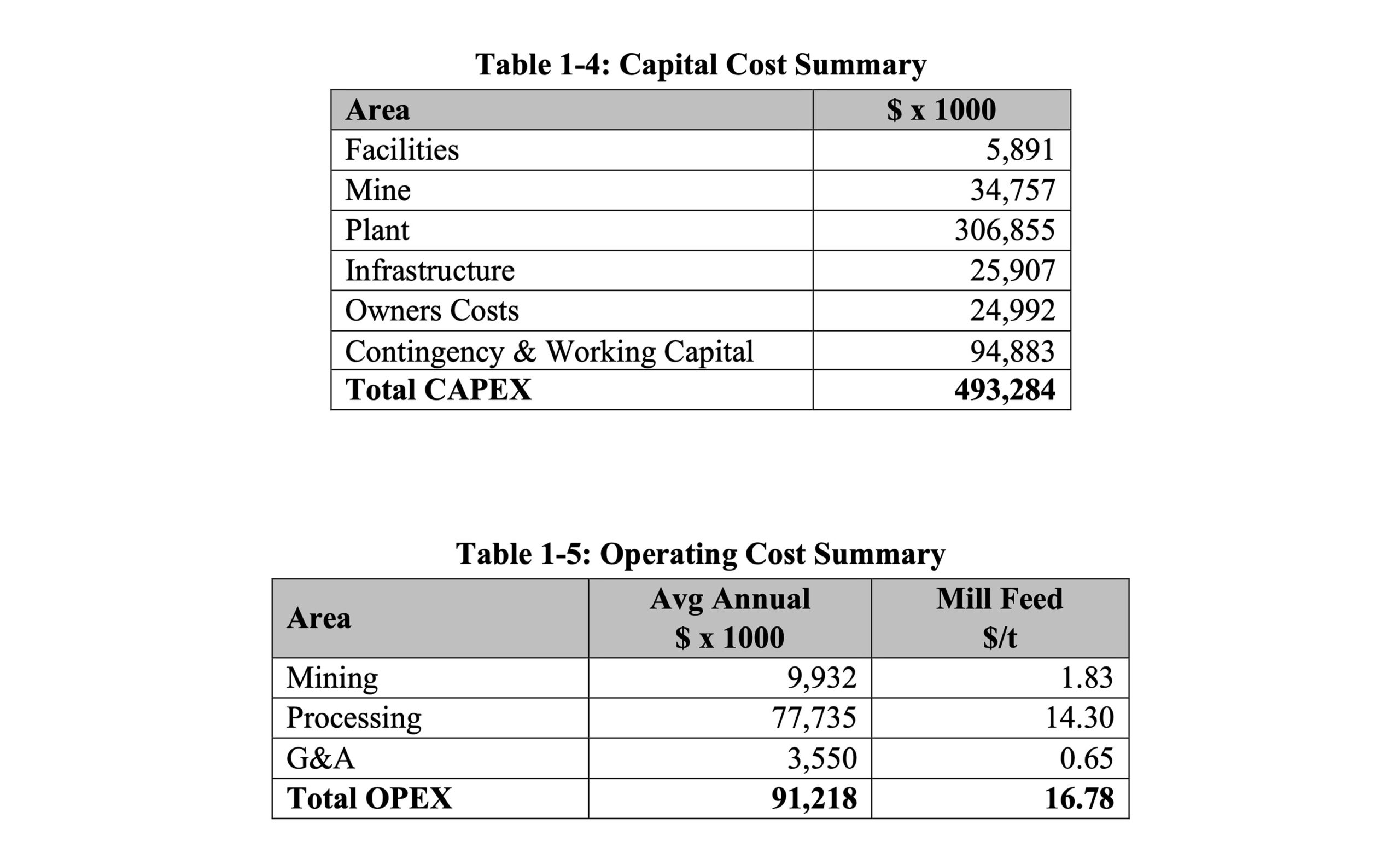

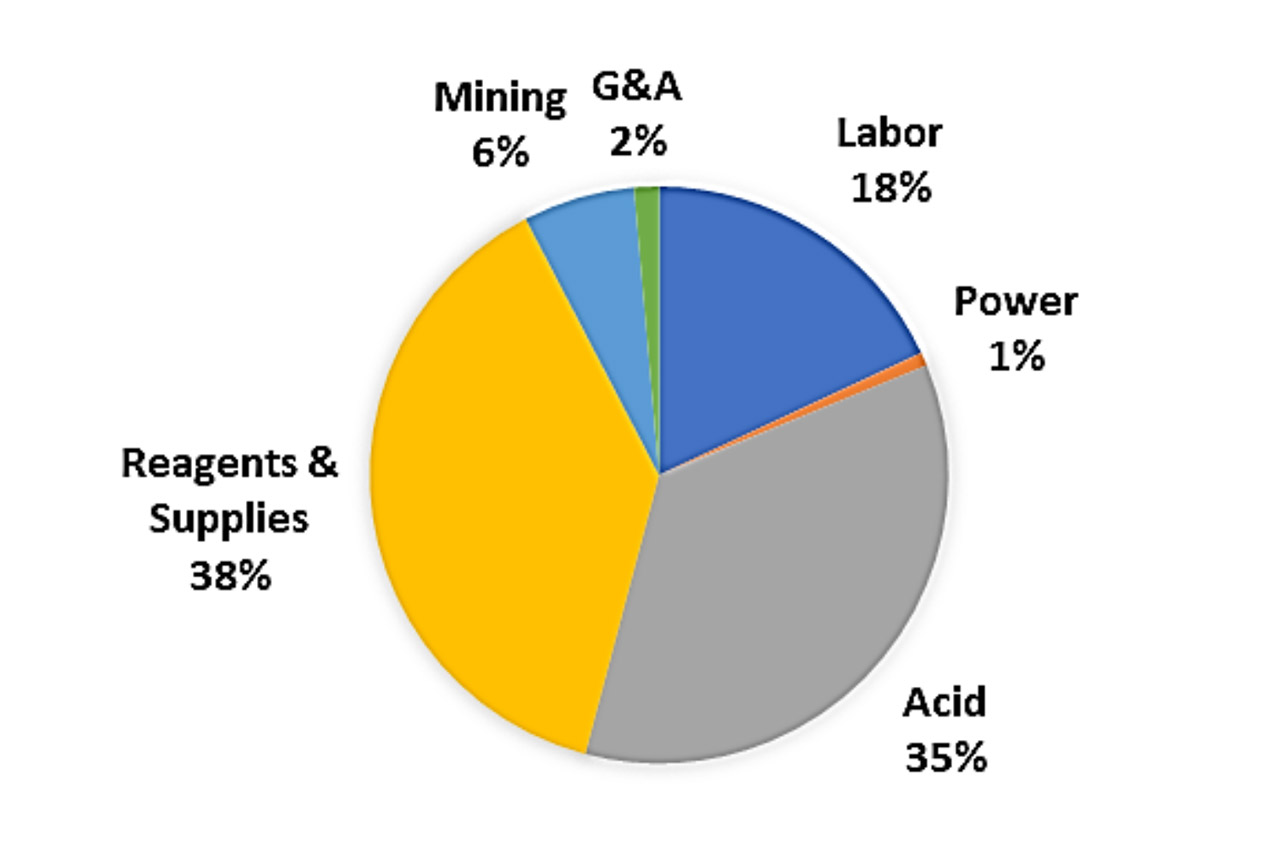

The initial capex is now budgeted at US$493M, but this includes almost $95M in contingency and the construction of a $102M acid plant to produce sulfuric acid on-site. Additionally, the operating cost has been budgeted at just below $17/t and the processing cost is obviously the biggest cost as it represents almost 90% of the total opex per tonne of mill feed.

There still are some possibilities to further improve the economics. According to the pre-feasibility study, the acid plant will have surplus power (elemental sulfur will be burnt in order to produce 2,500 tonnes per day of sulfuric acid thereby generating 27,500 MW of heat-related power) and Cypress could potentially look into selling the surplus power by putting it on the grid. This won’t move the needle too much, but every dollar of by-product revenue obviously helps.

The acid cost remains a key component of the total production cost as 35% of the $16.78 per tonne is directly related to the use of acid, and that’s why keeping the acid consumption low (to just over 125 kilos per tonne of mill feed) is a key component.

The mine plan envisaged in the pre-feasibility study assumes a production rate of 64% of the nameplate capacity in Y1 followed by 98% in Y2 which should allow Cypress to hammer out all the initial start-up problems new mines can encounter (very few mines reach the commercial production phase without the need to further finetune some of the processes).

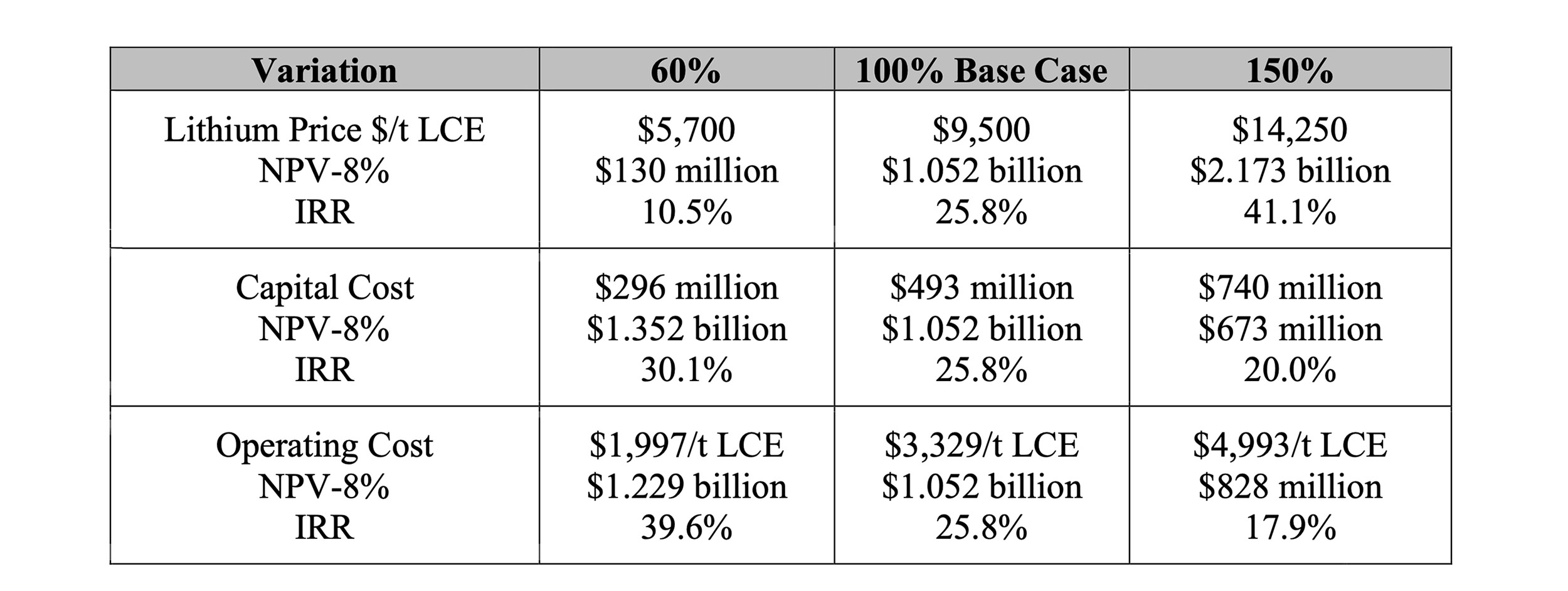

Unfortunately, the technical report didn’t contain a more detailed breakdown of the sensitivity analysis as we would have been very interested in seeing the NPV and IRR using a lithium carbonate equivalent price of $8,000/t (as some sort of mid-point between the base case scenario of $9,500 lithium and the worst-case scenario using a lithium price of $5,700/t.

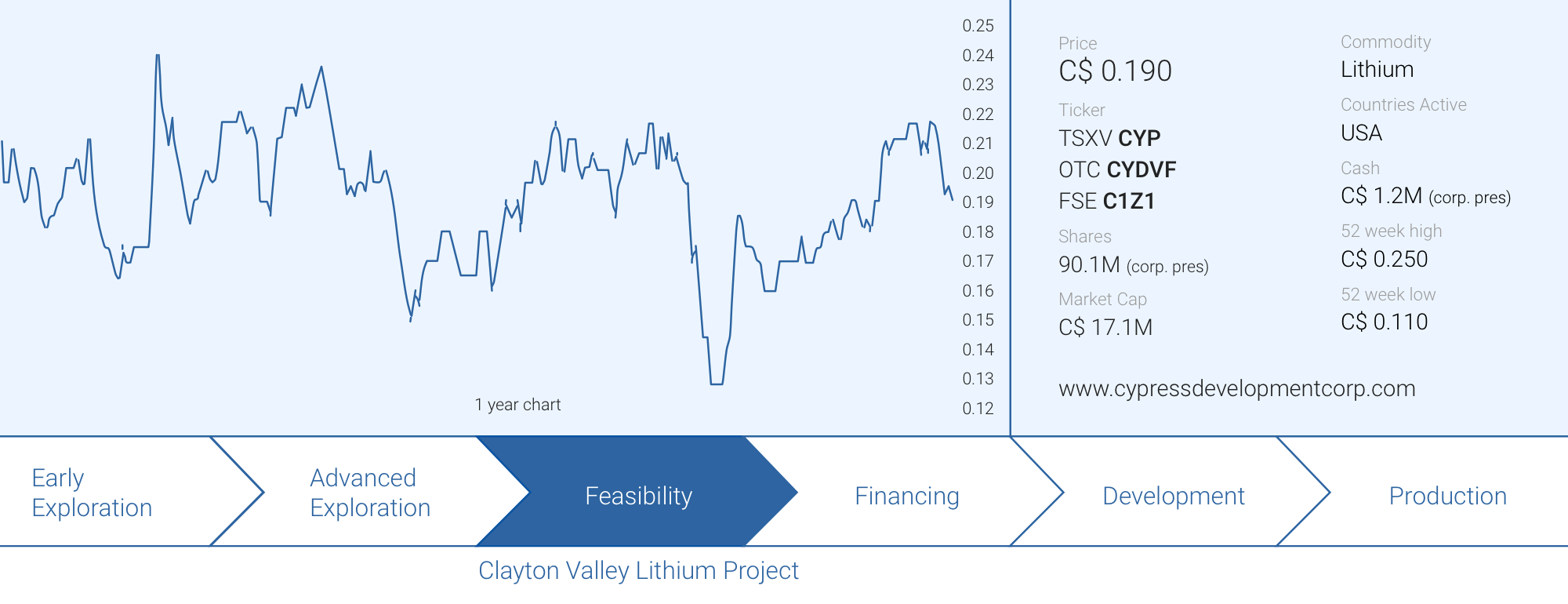

Cypress still has in excess of C$1M in working capital

Cypress has been spending its cash wisely as the company doesn’t want to dilute at the current levels. In the first quarter of the year, only C$240,000 was incurred as operating expenses while an additional C$150,000 was capitalized for a total cash outflow of around C$0.4M.

The low burn rate hardly is a surprise. Cypress hasn’t been drilling as the company was focusing on getting its pre-feasibility study across the finish line. The low burn rate also means Cypress still has a decent chunk of cash in its treasury. As of the end of March, Cypress had C$1.1M in cash on the balance sheet and working capital of just over C$1M. We expect the company’s working capital position to be roughly unchanged.

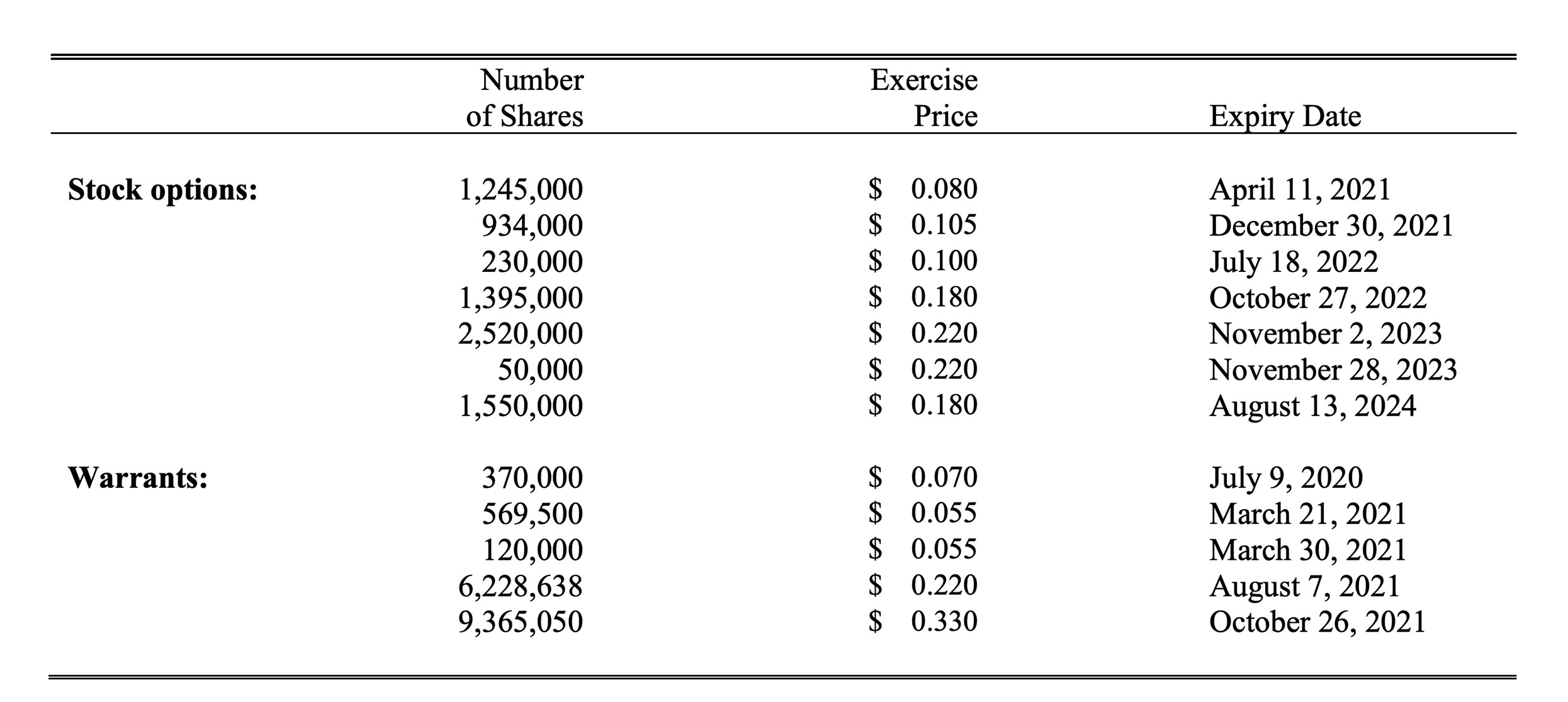

While Cypress doesn’t need to raise cash right now, its hands will obviously be a bit tied and it will have to tap the equity markets if it wants to continue to advance the Clayton Valley lithium project. Cypress also reached the point where a large chunk of its existing warrants will be ‘in the money’: there are 6.23 million warrants with a strike price of C$0.22 expiring in August 2021 (C$1.37M) while an additional 9.37 million warrants that will expire in October 2021 have a strike price of C$0.33 (for a total cash injection of C$3.09M if exercised).

In an ideal scenario those warrants end up being in the money and a gradual exercise of those warrants could help to continue to fund the company. Unfortunately, that ideal scenario may take a while as although the Cypress share price has reached the C$0.22 level, it would have to trade at a substantial premium before we can reasonably expect warrant holders to exercise their warrants.

As you can see in the image above, there indeed still are some 7 cent and 5.5 cent warrants outstanding. Those are now deep ‘in the money’ but even if those would all be exercised, the cash contribution to the Cypress treasury would be less than C$60,000, a negligible amount.

With the results of the pre-feasibility study now in hand, Cypress Development can now calmly explore its options to further finance the Clayton Valley lithium project. A private placement would be the easiest way to raise cash but perhaps there are strategic investors that are sufficiently impressed with the pre-feasibility study that are now willing to step up the plate to take a 9.9% or 19.9% stake in Cypress? Only time will tell.

Conclusion

The 2018 PEA already showed an interesting project but the additional work that has been completed on Clayton Valley in the past 18 months has moved the needle from ‘interesting’ to ‘robust’. Unfortunately, it appears to be standard in the mining sector to see an excellent PEA (as there are fewer restrictions to calculate the economics) where after the economics of a project usually deteriorates once the PFS and FS stages have been reached.

Cypress has done the opposite as the pre-feasibility study is actually stronger than the PEA despite being subject to more strict assumptions, and that is very encouraging. In its pre-feasibility study, the independent consultant recommends Cypress Development to move ahead with a pilot plant to confirm the process flowsheet and confirm the recovery rates and reagent (acid) consumptions in anticipation of a full feasibility study. Cypress has already made great progress in advancing the Clayton Valley Lithium project by boosting the anticipated recovery rate of the lithium and running a pilot plant will be another important step to de-risk Clayton Valley.

The project works brilliantly at $9,500 lithium, and Cypress Development appears to be in an excellent position to benefit from renewed interest in the lithium space once investors start to care about lithium again.

Disclosure: Cypress Development is a sponsor of this website. The author has a long position in Cypress Development.