As expected, several zinc mines had to be shut down in the past few years due to depletion, and now the warehouse inventory levels of the base metals have been steadily declining for several years, the market is finally waking up and starts to look at zinc companies again, as the zinc price has been trading above $1/lb ever since July last year and is currently trading at a multi-year high of $1.33.

Unfortunately, due to the low zinc prices of the past decade, not a lot of explorers wanted to invest in zinc exploration as they wouldn’t get any love from the market. This means that as the demand for zinc is still increasing, the world needs to look for new zinc projects to be brought online in the next few years. Darnley Bay Resources (DBL.V) is one of those companies hoping to fill the supply gap. The company acquired a past-producing zinc asset in receivership and will publish a new PEA within the next few months.

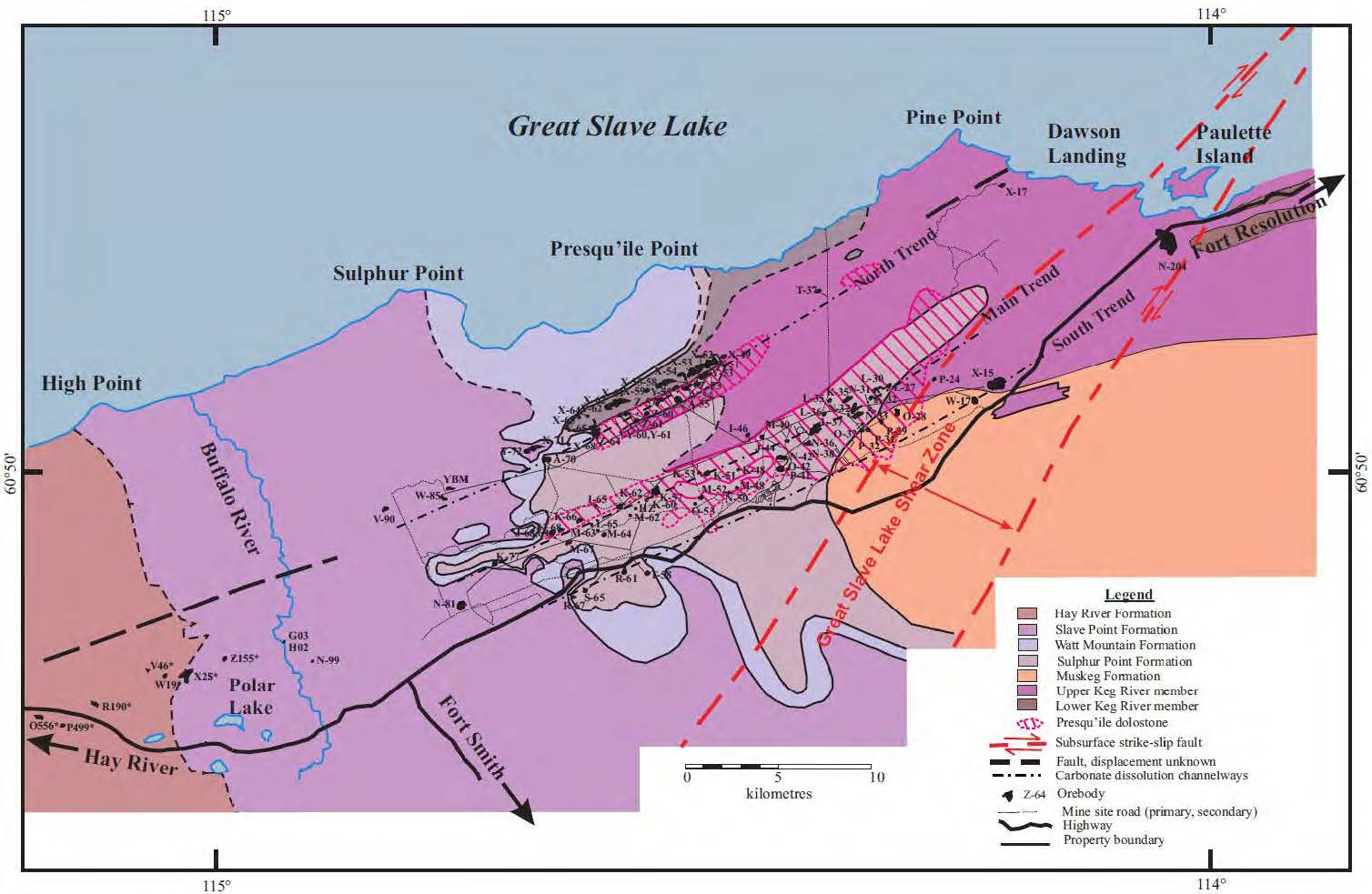

Darnley Bay acquired the Pine Point zinc project in a bankruptcy sale

In October last year, Darnley Bay entered into an agreement with the court-appointed receiver of Tamerlane Ventures, and by December it took possession of the Pine Point zinc project, located less than 50 kilometers to the east of Hay River, NWT.

The project isn’t just one big zinc-zone, but actually consists of 46 zinc-lead deposits over a total strike length of almost 70 kilometers. Of these 46 deposits, ten have been the subject of a NI43-101 report, compiled for Tamerlane Ventures back in 2014.

The acquisition terms are actually very straightforward (the receiver probably really wanted to get it off its books and recoup a part of the losses). To secure the option, Darnley Bay had to pay C$50,000 in cash and issue 1.15 million shares to KSV, the court-appointed receiver. Upon the final acquisition of the property, an additional C$2.95M had to be paid in cash, whilst an additional 23.85 million shares had to be issued to KSV, for a total acquisition cost of C$3M and 25 million shares. Using a valuation of C$0.20 per share (which is where Darnley Bay priced its most recent hard dollar private placement at), Darnley Bay paid a total consideration of approximately C$8M to acquire 100% of the asset.

Pine Point is a historic producer, and exploration actually already started before the second world war when Cominco started to explore the tenements and started to sink a shaft in the property. The company discovered almost 100 different zinc-lead deposits, but it took another few decades until 1964 before large-scale production started after Cominco completed a resource estimate with 21.5 million tonnes of 11.2% ZnPb, which is a good average grade.

As said, the project isn’t just one large pit, but Cominco actually started to mine 50 separate open pits as well as two underground deposits over a 35 kilometer long trend. In the subsequent 23 years after starting to mine in 1964, Cominco processed a total of 64 million tonnes at an average grade of 7% zinc and just over 3% lead for a total zinc production of almost 10 billion pounds.

The Tamerlane PEA is outdated, but contains valuable information

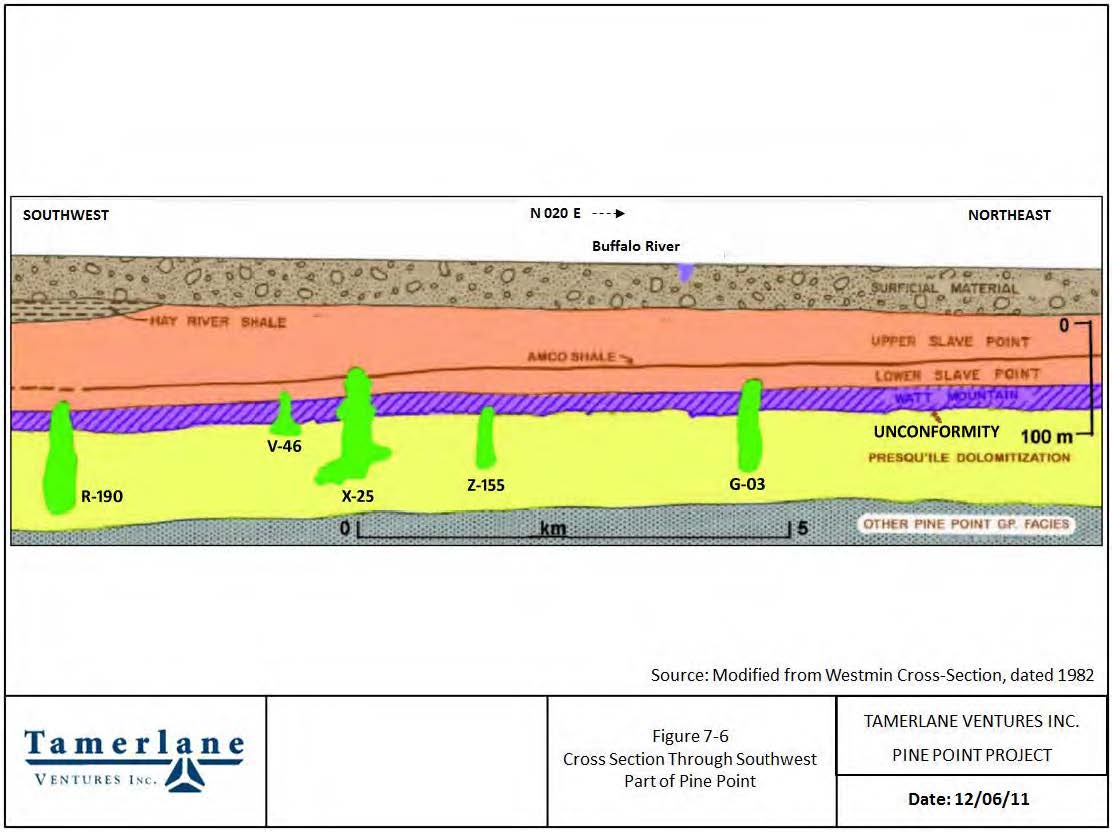

Approximately three years ago, Tamerlane Ventures commissioned an updated technical report on the Pine Point project which included a mine plan based on one underground and nine additional open pit zones. The original plan was to truck a pre-concentrated lead-zinc product (after using Dense Media Separation on-site) from these cluster pits to the mill on the proposed mine site, located at the R-190 underground mine near the Territorial Highway.

As the property had been in production for 50 years before the technical report was completed, Tamerlane’s consultants had a lot of information to go forth on. Cominco had drilled a total of 1.31 million (!) meters in almost 20,000 drill holes, so Tamerlane (and now Darnley Bay) have access to approximately $300M worth of drilling at today’s costs (and $150M in historical expenditures)

Using a zinc price of $0.95/lb and a lead price of $1/lb, the after-tax NPV8% of the property, based on mining between 3000-7000 tonnes per day, came in at C$112M (using an USD/CAD exchange rate of 1:1) with an IRR of 35%. Another important feature of Pine Point is the excellent quality of the zinc and lead concentrates. The 2014 study indicated the average lead grade in the lead concentrate would reach up to 72%, whilst the average zinc content in the zinc con would be 62%. This would be absolutely fantastic, considering the accepted zinc levels for ‘clean’ concentrates are 48-52%. Delivering a 62% concentrate could result in a premium pricing, as it would allow the zinc smelters to blend the high-quality concentrate from Pine Point with lower value concentrates (for instance Nevsun Resources’ is still unable to produce a commercial grade zinc concentrate as its zinc con has an average grade of just 40%). Blending a 40% con with a 62% con would result in a better feed stock for smelters.

On top of that, Darnley Bay thinks it will be able to add 5-8 additional zinc deposits to the mine plan, which would increase the mine life and have a positive (but relatively small, due to discounting) impact on the Net Present Value of the property. That’s clearly positive, but the main contributor to a higher net present value in the upcoming PEA will obviously be the cheaper Canadian Dollar. Back in 2014, Tamerlane’s consultants used an USD/CAD exchange rate of 1.00 to calculate the economics of the property. With a current exchange rate of 1.30, some of the local costs will be much lower than in the 2014, whilst the recalculated NPV – keeping all other parameters unchanged – would increase drastically from C$112M. To demonstrate the leverage on this project, for every 10 cent move in lead and zinc prices, the NPV Increases by US$46 million

And finally, the PEA in the 2014 study assumed a TC/RC charge of $204/t for the zinc concentrate. Whilst that was a perfectly valid assumption back in 2014, the lack of zinc supply has forced zinc smelters to reduce the TC/RC charges. We are still waiting for more companies to disclose the TC/RC charges for the current year, but we would expect the 2017 charges to settle in the $150-180 area which could widen the margins for Darnley Bay. Additionally, recovering some of the Germanium contained in the deposits could also provide Darnley Bay with an additional by-product revenue, but we’ll have to wait for the updated PEA to see if Darnley Bay is able to take this into consideration.

The biggest issue seems to be the water inflow – how will Darnley Bay tackle this issue?

The main issue associated with the Pine Point deposits is the water inflow. The project is located just 10 kilometers from the Great Slave Lake, and Tamerlane researched several options to make sure the pits and underground mines don’t flood. Tamerlane has also drilled wells at several locations to test the groundwater flow, and engineering firm Thyssen confirmed to the company it would be able to control the water inflow.

The company’s original solution was to use ground freezing to block the water from entering the underground deposits. Ground freezing is a technique which has been used for decades in underground development, and has proven to be very effective in Canada’s underground uranium mines as for instance Cameco (CCU.TO, CCJ) has been using this to block the water out of their Athabasca Basin mines.

However, there’s another possibility to keep the water out, by using the grout technology, a technology which has been improved rather substantially in the past decade, but in order to avoid the initial capital expenditures associated with using grout or ground freezing, Darnley Bay will very likely focus on the open pits. Not only will it be a cheaper path towards a meaningful production rate, it will also allow the company to start developing the underground deposits by using the own internally generated cash flow from the open pit mining.

It’s important to note Cominco has never ‘lost’ a pit or equipment due to water inflow, so we do think Darnley Bay should be easy to control the water flows and protect the pit. Keep in mind the planning and interpretation of the water flows has also greatly improved since mining started more than 50 years ago, and we would expect any strategy to control water flows to be much more efficient now, compared to the sixties and seventies.

The timeline from here on

It’s really important to know the R-190 underground deposit as well as the mill, infrastructure and tailings area has already been permitted, and this will allow Darnley Bay to hit the ground running.

The company has engaged JDS Energy & Mining to complete a Preliminary Economic Assessment, which should be ready within the next few weeks. This PEA will give us a first ‘tangible’ overview of the up-to-date economics on the property.

The company has started to build a strong technical team, and has hired several key people (see the management section later in this report), as several high-flying individuals have joined the company. CEO Jamie Levy basically had to build the company from scratch and whilst we are sure this caused some headaches at the beginning, it allowed him to hire the people who could really help the project forward, rather than having to deal with some ‘legacy management’.

The fresh start and clean slate also attracted Lukas Lundin, Rob McEwen and Pat DiCapo to the story, as these gentlemen invested substantial sums of dollars into Darnley Bay Resources.

We would also expect the company to conduct some more drilling on the property and we’re looking forward to see the exploration plans for 2017. Darnley Bay raised C$5M in flow-through funds in the December-January financing, and this cash will have to be spent on the ground this year. Some of this money will be spent confirming additional deposits, while the rest will be used to explore a few areas of the property that have not yet been looked at. The company is also targeting to find additional high grade deposits like those that have been mined by Cominco. This should further boost the confidence in Pine Point as an asset, and pave the way to complete a feasibility study.

Whilst the focus is on the Pine Point zinc project, Darnley Bay still owns two other projects

Pine Point is the main (and actually only) reason Darnley Bay’s share price is performing this well. That being said, we can’t ignore the fact the company has secured options to acquire two other projects that have the potential to move the needle.

Darnley Bay has an option to acquire a 100% interest in the Clear Lake zinc project in Canada’s Yukon Territory. Previous operators have completed almost 20,000 meters of drilling on the property, and SRK estimates Clear Lake currently contains almost 8 million tonnes at an average grade of almost 9% Zinc-Lead (7.65% zinc, 1.08% lead) for approximately 1.3 billion pounds of zinc.

The historic owners have identified three additional targets, but these targets have never been drilled even though one of the targets outcrops on surface as a gossan with a relatively high average zinc grade, which makes this a very interesting property.

Additionally, Darnley Bay also has an option to acquire 100% of the Davidson Molybdenum deposit. Even though Molybdenum isn’t ‘hot’ right now, Davidson could be seen as a call option on the future, as the deposit contains approximately 340 million pounds of molybdenum in the measured and indicated resource categories. At an average grade of 0.171% Mo, the rock value is approximately $30/t.

Whilst Davidson would most definitely not be viable at the current molybdenum prices, the asset could be fine-tuned and high-graded to improve the economics. Also keep in mind the property contains 3 million mtu of Tungsten, which currently has an in-situ value of approximately $600M. However, the tungsten price is set to increase in the next few years and if the price would increase again towards $350/mtu, the total gross value of the tungsten at Davidson could be $1B, and result in a credit of $3 per produced pound of molybdenum (obviously depending on the recovery rates and the payability of the tungsten).

Management

Jamie Levy, President, Chief Executive Officer and Director

Mr. Levy holds a B.A. in Economics from Concordia University, and has been involved in the financing and management of Canadian mining companies for 25 years. Prior to joining Darnley Bay in 2012, Mr. Levy was VP Trading at Pinetree Capital Management for over five years.

Kerry Knoll, Chairman and Director

Mr. Knoll has worked in the mining industry for 35 years, as a company founder and executive, and journalist. He co-founded several successful mining companies, including Blue Pearl Mining Ltd. (now Thompson Creek Metals Company Inc.), Glencairn Gold Corporation (now B2 Gold Corp.) and Wheaton River Minerals Ltd. (now Goldcorp Inc.).

John Key, Chief Operating Officer

Mining Engineer, 28 years with Cominco incl General Manager at Red Dog during major expansion and Polaris.

Halina McGregor, Chief Financial Officer

Chartered Accountant with extensive financial management experience, including former Chief Financial Officer of nickel miner Sherritt International, and gold producer Goldcorp Inc.

Patricia Mannard, Vice-President, Finance and Director

Ms. Mannard, B.A. (hons.), has worked in the junior resource sector for over 25 years gaining experience in corporate maintenance, accounting management and financial reporting. She is a founding officer of Darnley Bay Resources Limited and the longest standing director.

Tim Smith, Vice-President, Operations

Metallurgical Engineer with 38 years of experience, with senior management posts at Afton, Sullivan, Red Dog and Montana Tunnels.

Stan Clemmer, Chief Geologist

Geologist, with 38 years of experience managing projects for Cominco, Falconbridge, Rio Algom and Noranda, and recently Sabina.

Judy Dudley, Vice-President, Environment

Biologist with 30 years of experience in water quality, water resources management, permitting and environmental analysis.

Conclusion

JDS Energy & Mining is working hard to complete an updated Preliminary Economic Assessment on the Pine Point zinc project. This new PEA will be completely different from the 2014 technical report due to the weaker Canadian Dollar, the higher lead and zinc prices as well as the extra deposits that could/will be added to the mine plan. According to the old PEA, the after-tax NPV8% at $1.15 zinc and $0.95 lead was estimated at US$194M, which would be in excess of C$250M using today’s USD/CAD exchange rate.

That’s also the first target we would be aiming for, and should the updated PEA reveal an after-tax NPV8% of less than C$250M (US$195M), we would be quite disappointed.

The PEA will be just the first step, and from then on it’s up to Jamie Levy and his team to create more value for the Darnley Bay shareholders. With in excess of C$5M in the bank, Darnley Bay remains well-capitalized and should be able to make tremendous progress at Pine Point in 2017.

Disclosure: The author owns a long position in Darnley Bay, but the company isn’t a sponsor of the website at this time. Please read the disclaimer