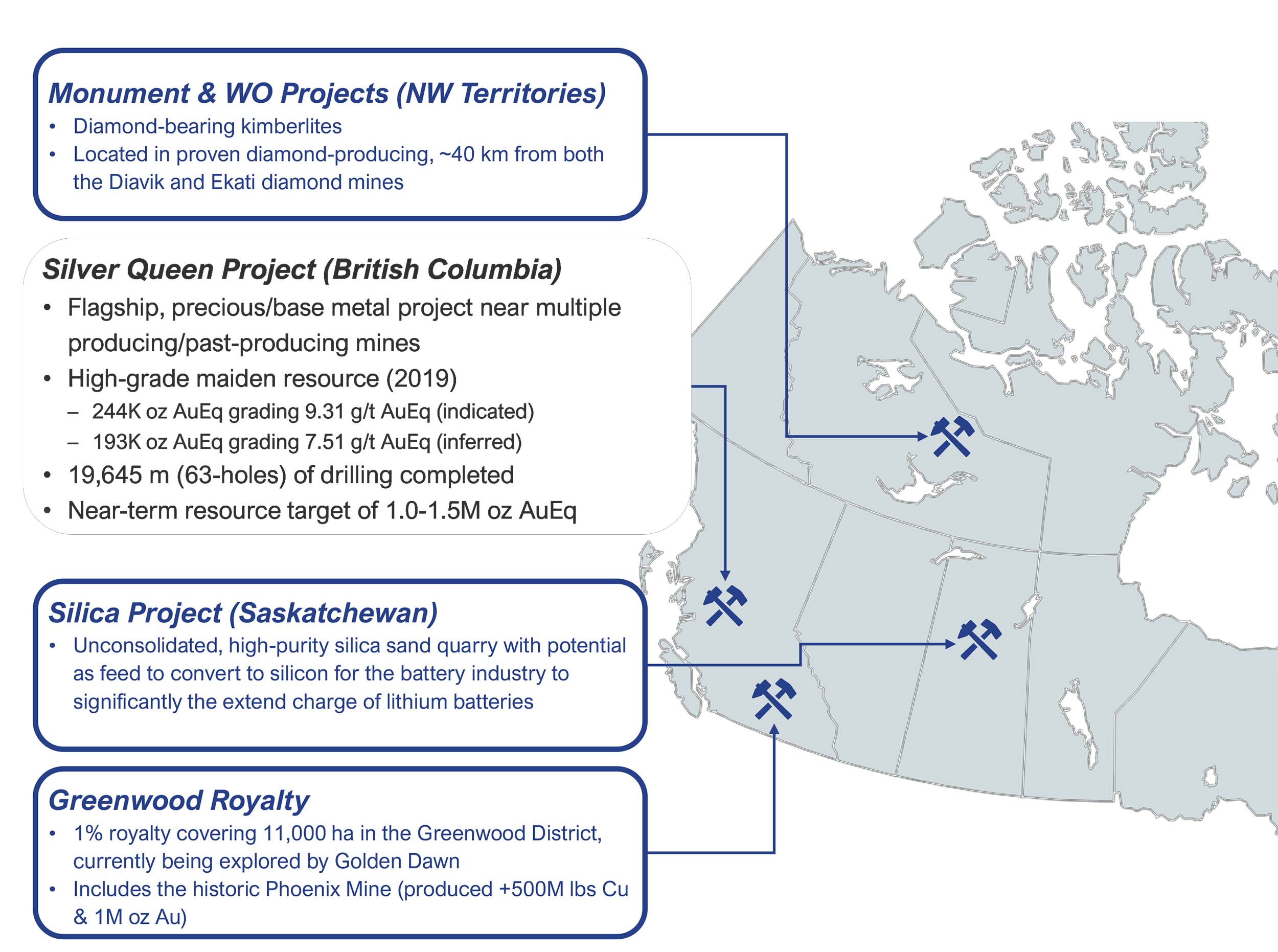

Equity Metals (EQTY.V) has been delivering on every single promise since the company was recapitalized by the Manex Resource Group, who took over the remnants of New Nadina Resources. The sole focus of Equity Metals has been on the Silver Queen project in the Stikine Terrane. The company came out of the gate with a gold-equivalent resource of just under half a million ounces in the combined indicated and inferred resource categories and has been drilling the Silver Queen project ever since.

Most of the attention was focusing on the Camp Vein Zone and Equity Metals is now getting ready to publish a maiden NI43-101 compliant resource estimate at Camp Vein where it has outlined a near-term exploration target of 1.5 million tonnes with an average grade of 500 g/t AgEq. This could add in excess of 20 million silver-equivalent ounces to the Greater Silver Queen resource estimate and on a gold equivalent basis, this would put the company close to the ‘magical’ mark of 1 million ounces.

Although Equity Metals has done everything by the book, its share price is back to square one as the current level of 13-14 cents is almost exactly where the company was trading in the summer of 2020. Sure, there have been some spikes in the share price throughout the past two years, but the bottom line is that the company still has a market cap of just C$15M while being so much more advanced than when it came out of the gates.

Recent exploration results

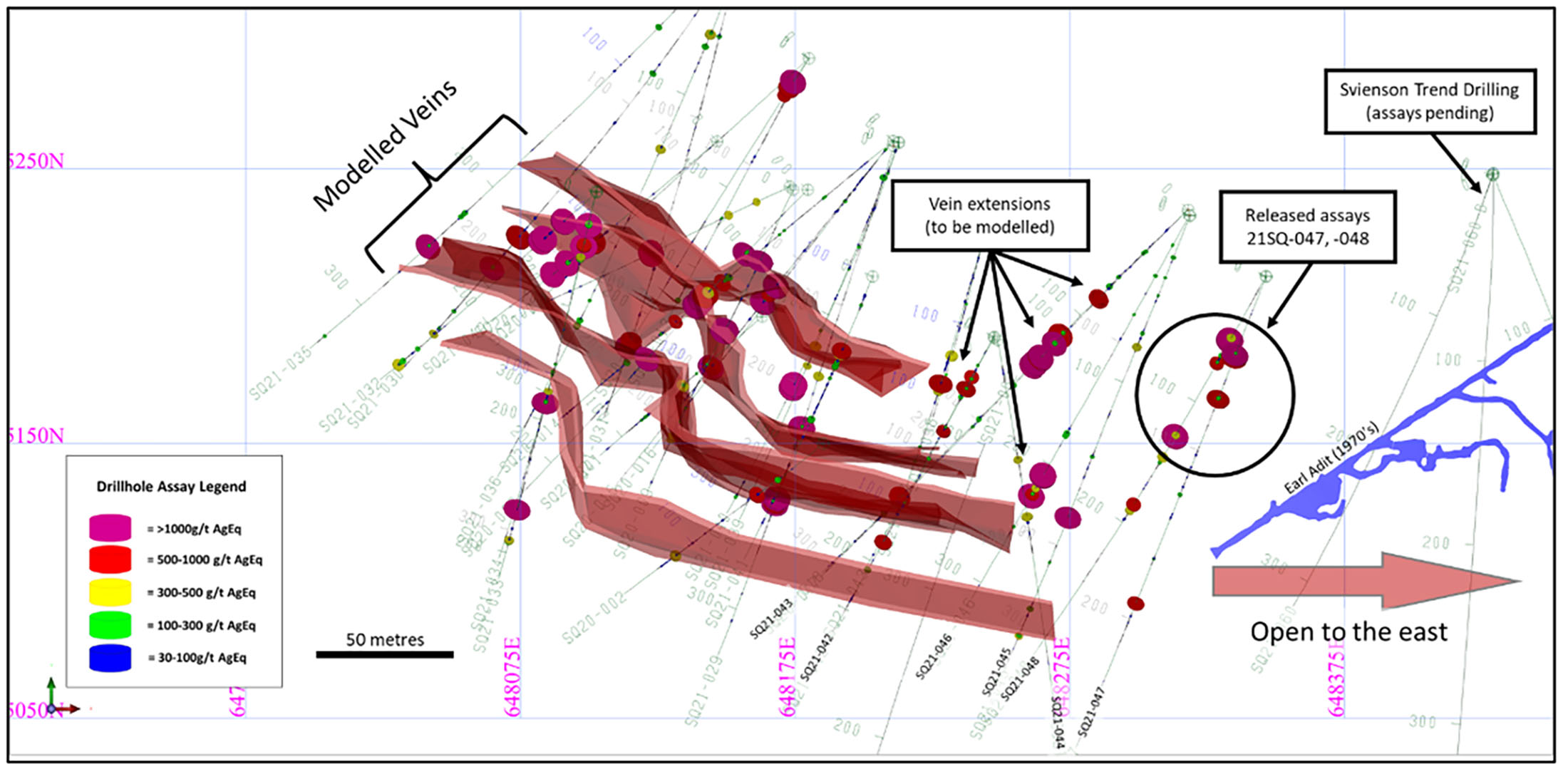

In your update released on January 16th you released the assay results of an additional few holes drilled at Silver Queen’s Camp Vein target. All holes continue to intersect mineralization and in some cases there’s even ultra high-grade mineralization. Hole 40 and 49 come to mind with grades exceeding 1,000 g/t silver with grades exceeding 3,000 g/t in hole 49. The intervals remain pretty narrow, which is to be expected as this simply is a narrow vein system. But how should investors interpret your drill results, considering there will be quite a bit of mining dilution going forward?

Let me say first that we typically highlight the higher-grade intercepts to attract the attention of the investor. These often sit within broader mineralized intervals which carry what is generally considered a “minable grade” and are often high-grade mineralization as well.

Also, we are typically reporting multiple high-grade intercepts in each hole which reflects the “stacked” nature of the Camp Vein system in which multiple veins intercepts can be traced over the full 250 metre strike of the currently drilled Camp Vein target. So it is not just a single 1.5 metre to 5.0 metre thick vein that we are drilling and modelling, but several veins with a more substantial cumulative thickness.

A quick way for readers to evaluate the drilling is to utilize silver grade*thickness (multiply the Ag g/t grade * intercept thickness in metres). Something on the order of 350gram-meters Ag per tonne could be considered mineable in many underground mining situations and a 500gm/t Ag value could likely be quite profitably mined. Therefore, a 1000g/t Ag intercept over 0.5m = 500g*m/t Ag and should be included in vein modelling for Mineral Resource estimate purposes.

I just noticed this morning on Miner Deck’s “Top silver intercepts for the week”, that Equity had the highest reported intercept this week and the eighth highest intercept on a grade thickness basis. When looking at the list, we are in pretty good company.

The Camp Vein seems to have been thoroughly drilled so far. What’s the average drill density, and how will this impact an upcoming resource estimate? Will we see a substantial portion of the resources in the measured and indicated categories, or is it still too early for that?

We have tried to drill the Camp Vein target at nominal 50m spacing which is reasonably aggressive spacing for a vein deposit. It is a little early to speculate on resource categories, however I suspect that much of the potential resources will be in the inferred category, at least initially.

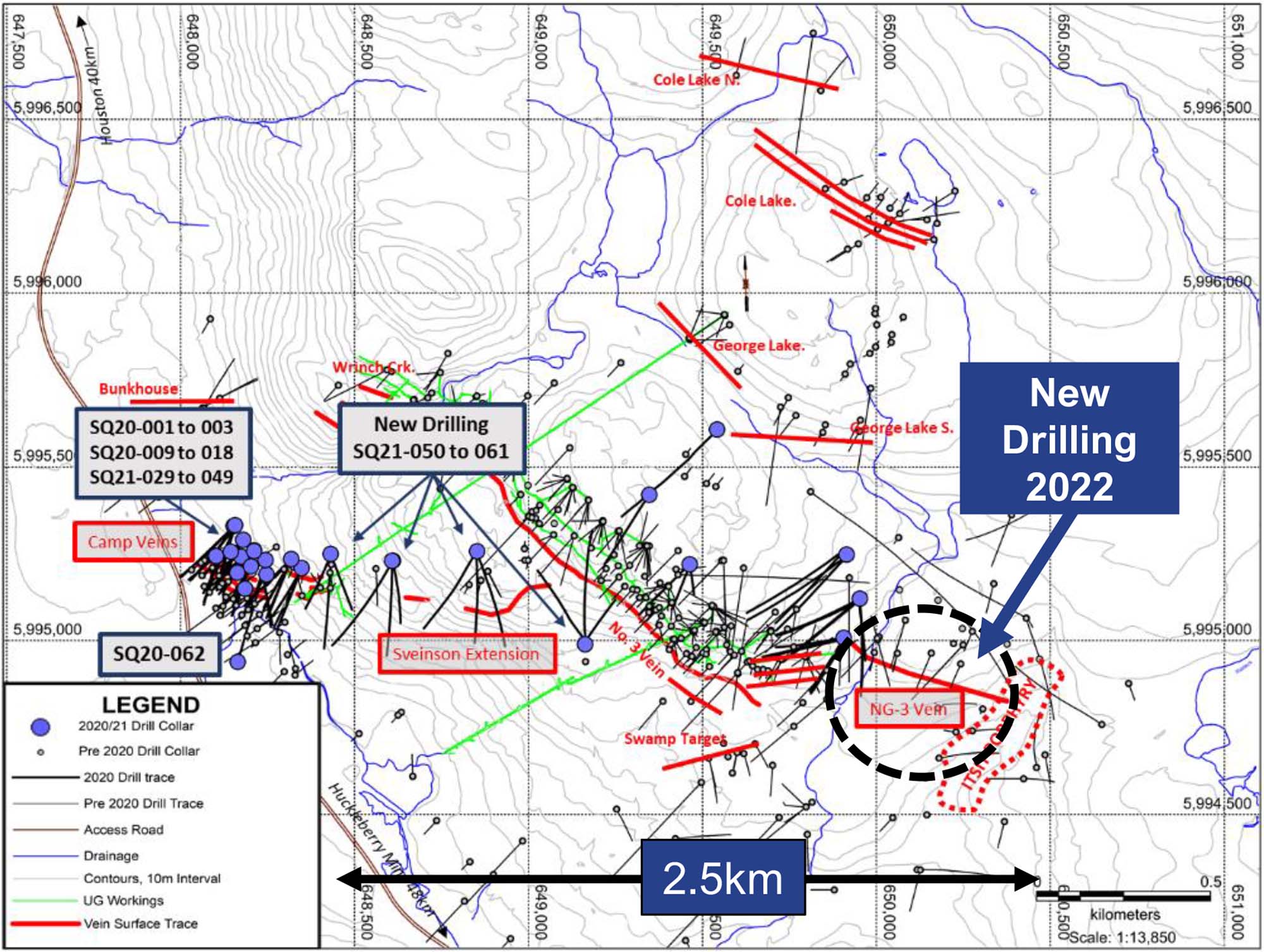

Is there a specific reason why the 2020-2021 drill campaigns predominantly focused on the Camp Vein? What are the plans to further advance the No 3 Vein?

There was substantial historic drilling on the on the Camp Vein (about 50 core holes) that had returned values very similar to what we have encountered in our drilling and we felt that it provided a good head start to quickly add new high-grade Mineral Resources at the Camp Vein. Previous workers were not able to resolve the vein geometry. We re-modelled the veins using some new concepts and have been guided by that modelling in our most recent drill targeting with some apparent success.

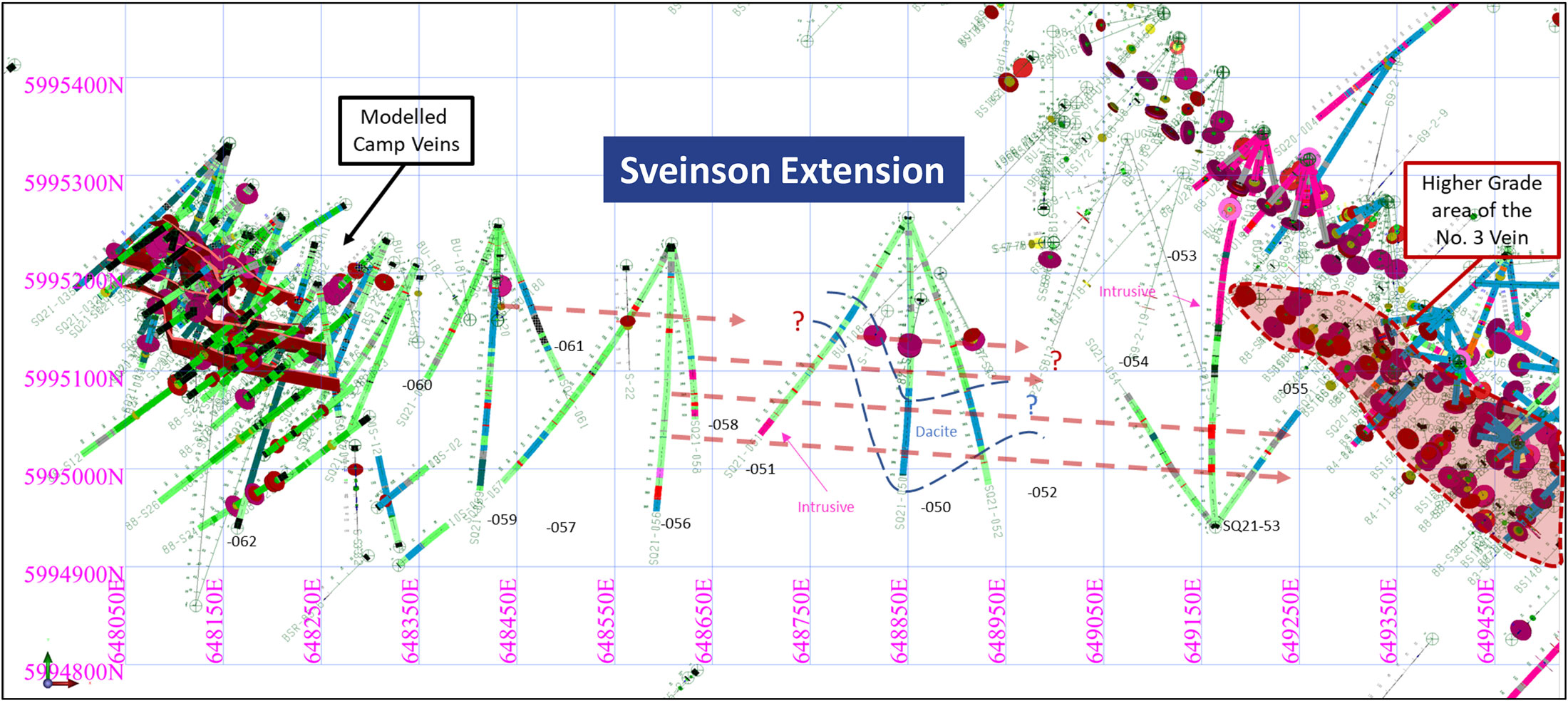

Let’s talk a minute about the Sveinson extension which is nicely located right in between the Camp Veins and the No3 vein zone. How did you come up with this target and what are your expectations/hopes for the 11 holes you drilled there? Will this be a high-priority drill target in the future or will you continue to focus the resources on the ‘better defined’ zones at No3, Camp & NG3?

Once we identified the potential east-west controls on the mineralization at Camp Vein, we noticed a similar orientation to high-grade historic vein intercepts throughout the property. These included some veins in historic workings from the 1970s located immediately to the east of the Camp vein and an area a little further east called the Switchback vein. A closer look at the topography indicated a broad east-west structural zone that can be traced eastward and included parts the Camp Vein, No. 5, Switchback, No. 3 and NG-3 veins, extending a total of 2.5 kilometers. The 1km segment of the structure between the Camp Vein and the No.3 Vein we now call the Sveinson Extension.

We have drilled an initial 12 wide-spaced holes from four drill sites on the Sveinson target with encouraging visuals that seem to suggest good continuity of several of the veins that we project through the structure. Based on these results we believe that there will be more drilling needed on this target area. Once we have the final results, we can make a decision on what will be the priority targets for drilling in 2022.

The plans for 2022

Your drill program will start any day now, and in your recent press release you mentioned there will be a specific focus on the NG3 vein which is located east of the No3 Vein. NG 3 seems to be running parallel to the No3 Vein, but what else can you tell us about NG3? What are you targeting there?

As I mentioned above, the NG-3 vein represents the most easterly segment of the structure described above We have indications from historic drilling and Equity’s drilling from 2021 (SQ21-024 and SQ21-025) two veins along a 700 metres strike-length that remains open at depth.

Right next to the NG3 Vein, you have outlined a porphyry zone. Is that of any interest whatsoever at this point?

There is porphyry -style mineralization, known as the Itsit porphyry, on the east end of the NG-3 Vein target. At this point we like the high-grade nature of the veins sets that we are currently targeting and are looking at the Itsit porphyry as a secondary target. We will likely intersect porphyry-styled mineralization in this upcoming drill program and will maybe get a better sense of priority after this next set of drill holes.

You are targeting to publish a maiden resource estimate on the Camp Vein in the second quarter of this year. To be clear, this will be in addition to your existing resource which was solely based on the No3 Vein. Although regulations don’t allow you to publish a detailed guidance but what are you hoping for?

Our near- to mid-term target is to double the existing resource so nominally we would like to add about 1.5Mt of higher-grade mineralization. We might not achieve that in our initial Mineral Resource update but we have every confidence that the Camp Vein system can be expanded beyond what we have drilled so far and there are other veins that with time, can be incorporated into resource estimates for the project.

With an existing resource on the No3 Vein of just under 20 million silver-equivalent ounces in the indicated category (using today’s metal prices as conversion, without applying recovery and payability ratios) and an additional 17 million ounces silver-equivalent in the inferred resource category, odds are you will end this year with about 50 million silver-equivalent ounces across all categories with perhaps half that in the M&I resources. At what point will you feel sufficiently confident to pull the trigger on a Preliminary Economic Assessment?

It may be a little early to talk about a PEA. At this point we want to assess what we have in terms of an updated resource estimate and the potential to continue expanding the resource. We also need to do further metallurgical test work. These factors will dictate when we would transition the project into a PEA study.

Back in 2019, you reported the No3 Vein resource in gold-equivalents. With silver being a more dominant factor in the Camp Vein zone, are you looking to report future resource update in silver-equivalent?

I think in future we would likely report the resource in both gold equivalent and silver equivalent basis.

Are there any developments on the other projects in the Equity Metals portfolio?

We did a little bit of surface work on the Saskatchewan Silica Sand project last Fall to get a sense of the silica purity and completed a surface magnetic survey on the Monument project earlier in the year. But our main focus is the Silver Queen project.

The financial situation

What is your current cash position and what’s the exploration (and resource calculation) budget for 2022?

We have about C$2.5M in the bank. Of that is approximately C$1.4M in flow through funds dedicated for our current exploration while we also have approximately C$1.1M in ‘hard’ dollars. We plan to continue to be aggressive in exploration through 2022. I could see an 20,000 metres of drilling this year which could cost another C$3-4M in exploration expenses.

We notice there are about 8M warrants expiring in October and November of this year, with an exercise price of C$0.12. This could bring in about C$1M which would help to keep the treasury at a healthy level. Have you seen some of these warrants been exercised in the past few months?

We did see a number of warrant exercises earlier in the year. Not as much recently, but with continued good results and good news flow, I would hope to see further warrant exercises in the coming months.

Conclusion

Equity Metals has done everything right since the new management team took the reigns of the project. In the most recent financial year, which ended on August 31st, the company burned through C$3.16M in cash, of which C$2.6M was spent on exploration. An 82% conversion rate of exploration expenditures versus total cash burn is exceptionally high in the sector, especially for smaller companies that don’t have seemingly unlimited budgets and shows this management team is focusing on creating value by investing cash on the project rather than spending it on themselves.

Equity Metals is gearing up to publish a maiden resource estimate on the Camp Vein zone and this should push the total silver-equivalent resource on the project to or over 50 million ounces. As Silver Queen is and will always be a polymetallic deposit the silver value (or gold value) will always represent just a fraction of the total in situ value and the rock value as there will be several by-product credits.

While the independent consultants will be working on the report, Equity Metals plans to just continue drilling as there are plenty of other targets it wants to drill. Nor the Sveinson target nor the NG3 zone will be included in the upcoming resource calculation.

Disclosure: The author has a long position in Equity Metals and participated in the previous financing. Equity Metals is a sponsor of the website. Please read the disclaimer.