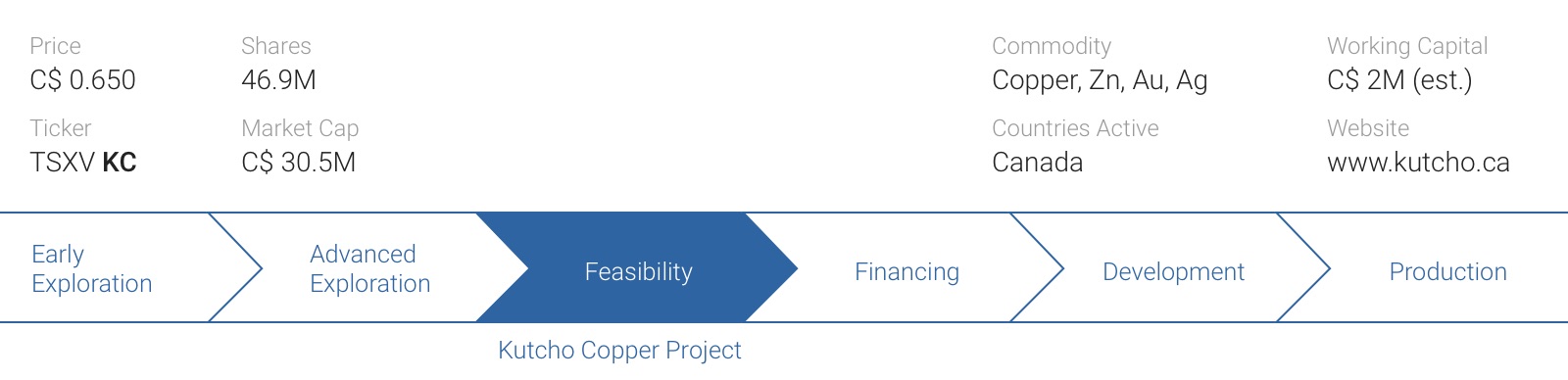

Sometimes larger companies lack the ambition to develop smaller non-core projects, which could be an opportunity for a smaller outfit. That’s exactly what happened with Capstone Mining (CS.TO), which had no intention to develop the Kutcho copper-zinc project in British Columbia. Desert Star Resources (DSR.V) which has been renamed in Kutcho Copper (KC.V) now the suspension has been lifted, struck a deal with Capstone Mining to outright purchase the Kutcho project in a cash and stock deal.

With the copper and zinc prices on the rise, this could be the perfect timing for Kutcho Copper to advance the project through the feasibility stage and permitting phase. The company has a three-year development plan which should see it increase the total mineable reserve and the NPV. It’s important to note Kutcho Copper is expected to be fully funded to execute this three-year plan.

Stay in touch with our weekly newsletter and when we publish a report. Unsubscribe at any time.

The background of the Kutcho Copper Project

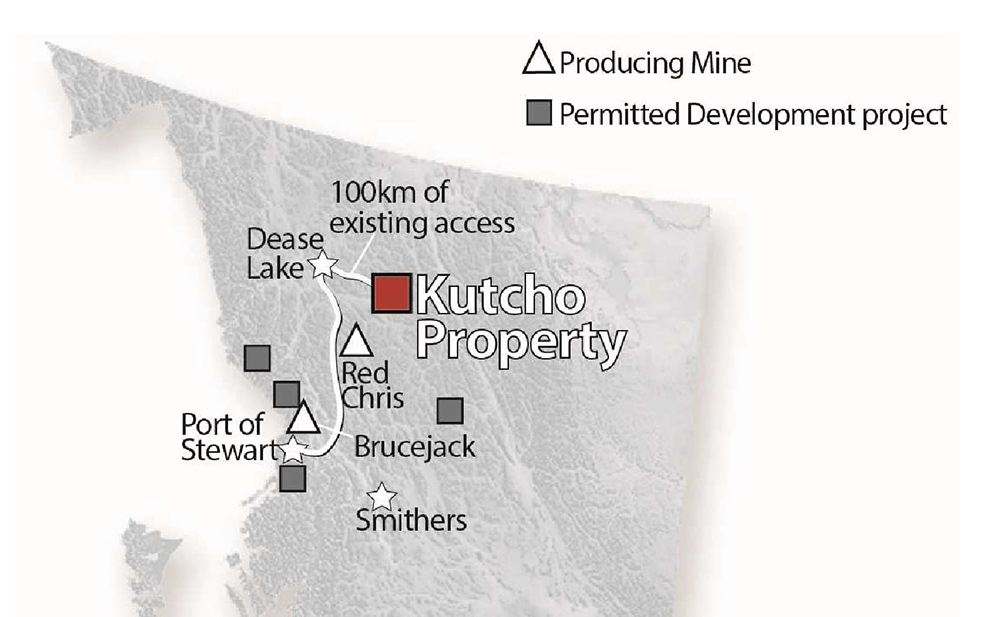

Kutcho Copper’s flagship project will be the namesake Kutcho project in British Columbia. The property is located approximately 100 kilometers away from Dease Lake through a seasonal (winter) road. Only 4X4 vehicles are able to use the road during the summer months and this means the company will likely truck in its full-year supplies in the winter months per truck, and to fly necessary supplies over per plane to a 900 meter long gravel airstrip just a few kilometers away.

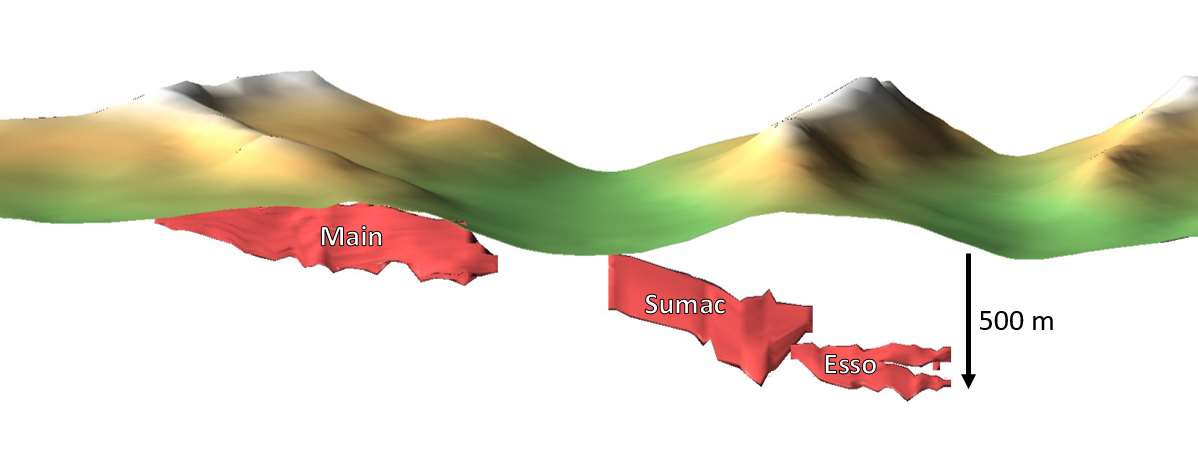

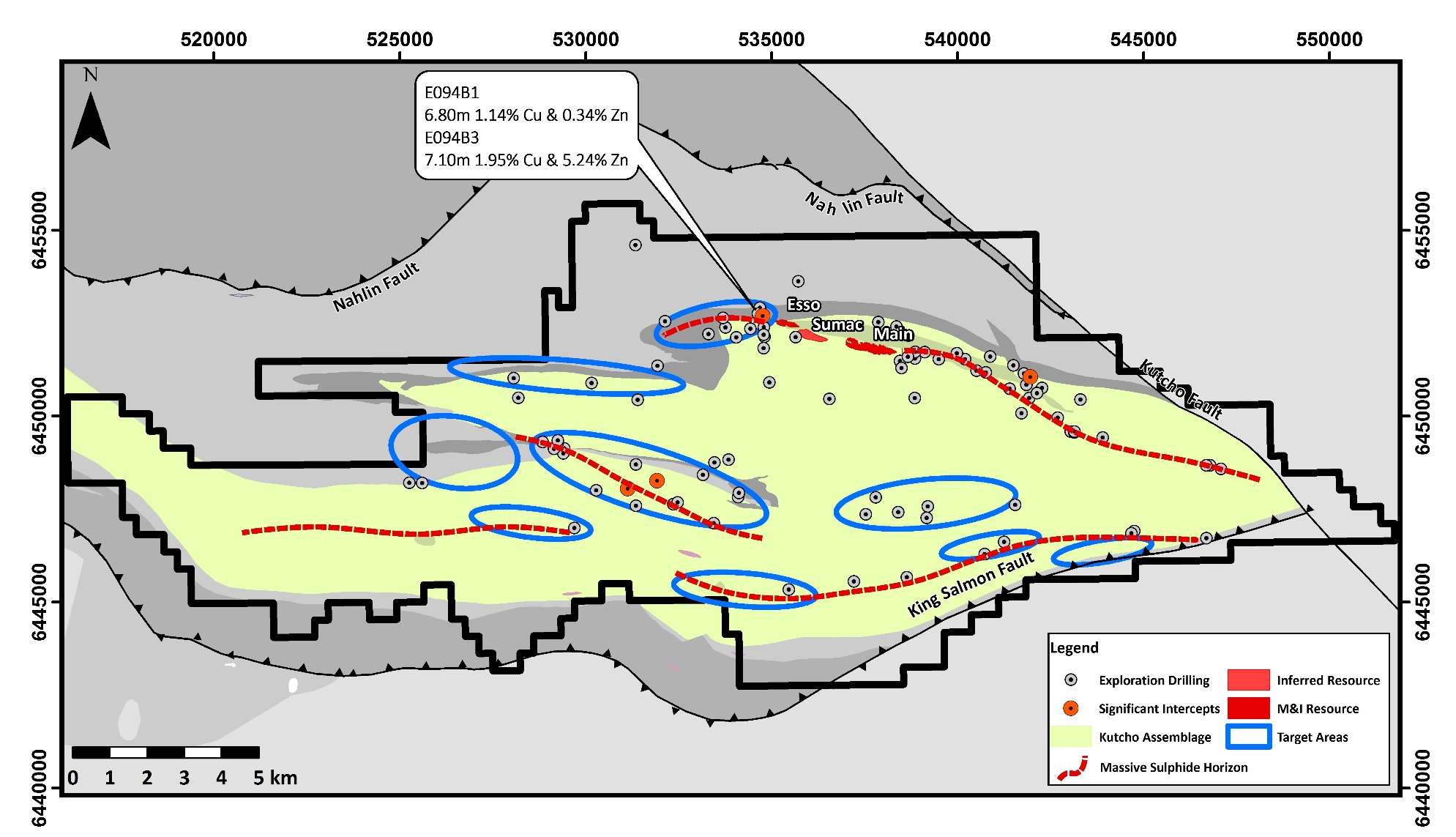

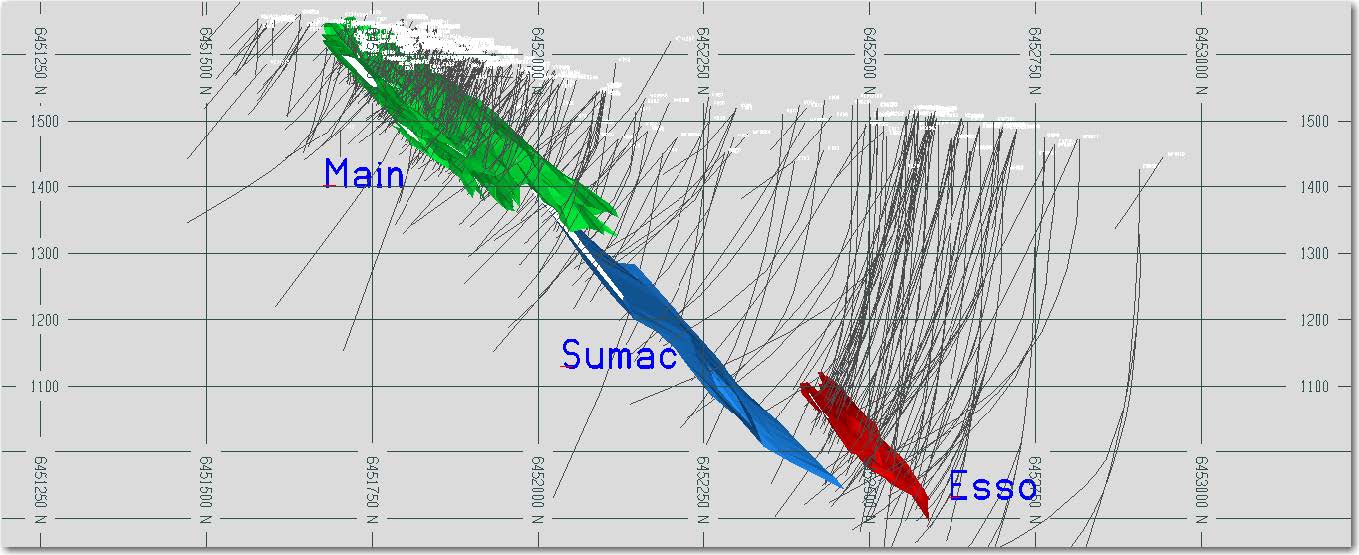

The project consists of three main zones; Main, Esso and Sumac, of which the latter isn’t even included in the mine plan yet. The mining activities will start at the open pit component of the Main Zone (where mineralization starts at surface and extends to a depth of 250 meters). The open pit will provide construction material for the infrastructure on the mine and processing site and will be used as paste backfill as well.

The Main deposit has a total ‘strike’ length of approximately 1.5 kilometers, and gets pretty close to the Esso deposit which is less than 2 kilometers away. It’s important to realize the environmental footprint of the project will be relatively limited as in excess of 50% of the tailings will be put back in the underground mine and in the open pit, reducing the needs for a large tailings management facility (which should also make it easier to get the project permitted).

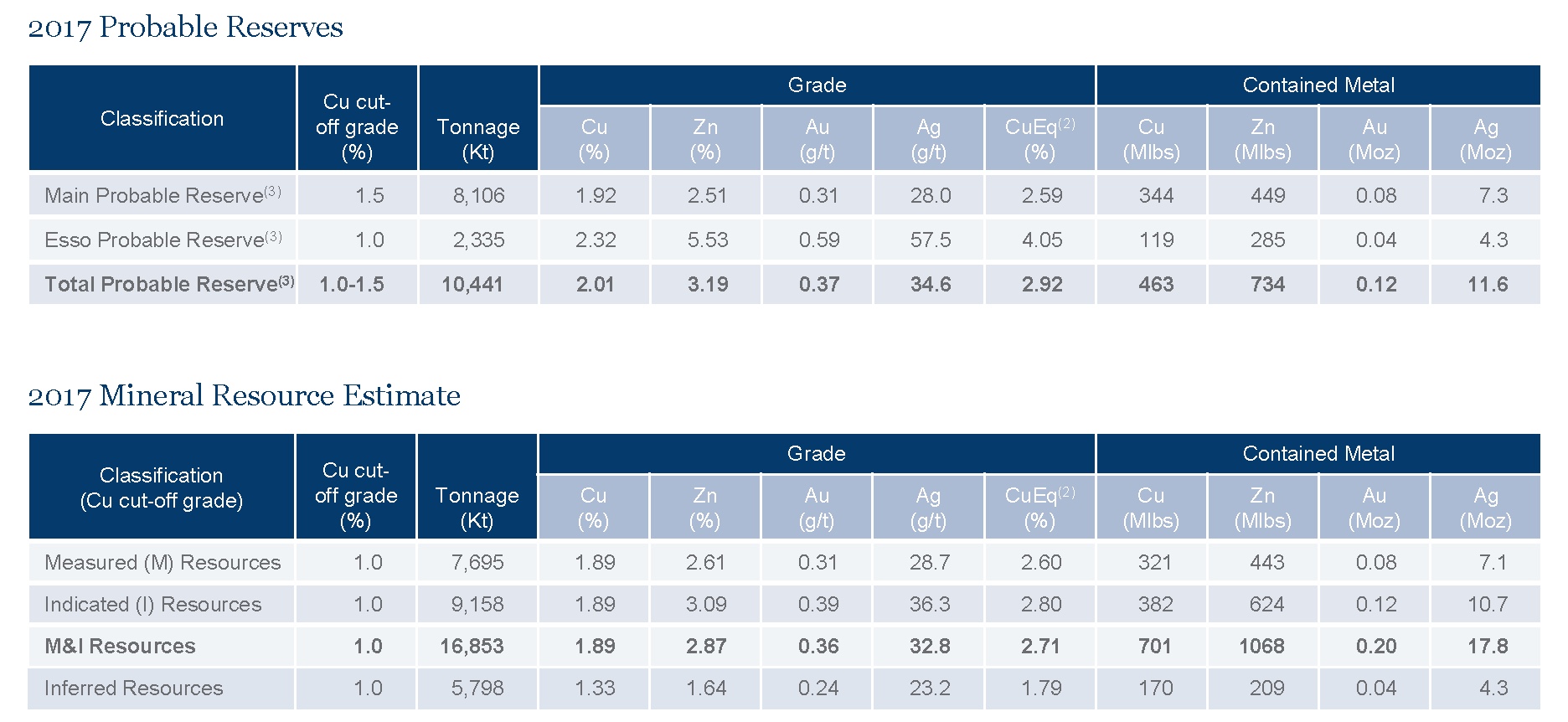

The project currently contains a total of 16.85 million tonnes in the measured and indicated resource estimate for a total of 701 million pounds of copper, 1.07 billion pounds of zinc, 17.77 million ounces of silver and 195,000 ounces of gold. The inferred resource estimate hosts an additional 170 million pounds of copper, 209 million pounds of zinc, 4.3 million ounces of silver and 45,000 ounces of gold in 5.8 million tonnes.

What’s really interesting here is the fact that despite a global resource of 22.7 milion tonnes, only 10.44 million tonnes (46%) were included in a probable reserve estimate with an average grade of 2.01% copper, 3.19% zinc, 1.1 ounces of silver per tonne and 0.37 g/t gold. Needless to say there’s a very clear potential to convert more resources into reserves in the not so distant future (see later).

The acquisition terms and funding mix

The acquisition agreement of the copper project appears to be very straightforward. Kutcho Copper will pay C$28.8M in cash and issue shares upon closing, giving Capstone Mining a 9.9% stake in Kutcho Copper.

It’s not always easy for a junior company to come up with C$28.8M in cash, but Kutcho Copper has all its bases covered. Just weeks after announcing the agreement to acquire the project, it had already struck a deal with Wheaton Precious Metals (WPM.TO, WPM) which will provide a streaming deal, a convertible debenture and an equity cash injection. If anything, it shows the streamers are willing to go to great lengths to secure streaming deals, and we might see similar deals in the future.

As part of the original agreement, Wheaton Precious Metals agreed to invest up to US$65M into Kutcho Copper in return for 100% of the payable gold and silver production (until 5.6 million ounces of silver and 51,000 ounces of gold will be delivered. After these thresholds have been met, Wheaton will be entitled to 2/3rd of the precious metals production). An initial US$7M (C$9M) will be advanced upon reaching certain ‘milestones’ during the feasibility process with the remaining US$58M becoming available during the effective construction phase of the Kutcho Project.

This first agreement was quickly followed by an even better deal for Kutcho Copper as Wheaton subsequently agreed to backstop a C$20M convertible debenture (maturing 7 years after the closing date) as well as C$4M in equity to make sure Kutcho Copper is fully cashed up to complete the feasibility study and permitting process.

And there’s an additional kicker. Should Kutcho Copper increase the throughput of its plant from 2,500 tonnes per day to 4,500 tonnes per day within the first five years after declaring commercial production (which is very likely, see later), Wheaton Precious Metals will wire an additional US$20M to Kutcho Copper whilst none of the other parameters will change (the production cap of the gold and silver ounces before reverting to a 2/3rd delivery scheme after the 5.6Moz silver and 51,000 ounces gold have been delivered).

The updated pre-feasibility study shows very attractive economics

Kutcho Copper has released the results of a pre-feasibility study it commissioned during the acquisition process. This gives us a much better understanding of how the project will be developed, and in which areas the study and economics could still be improved.

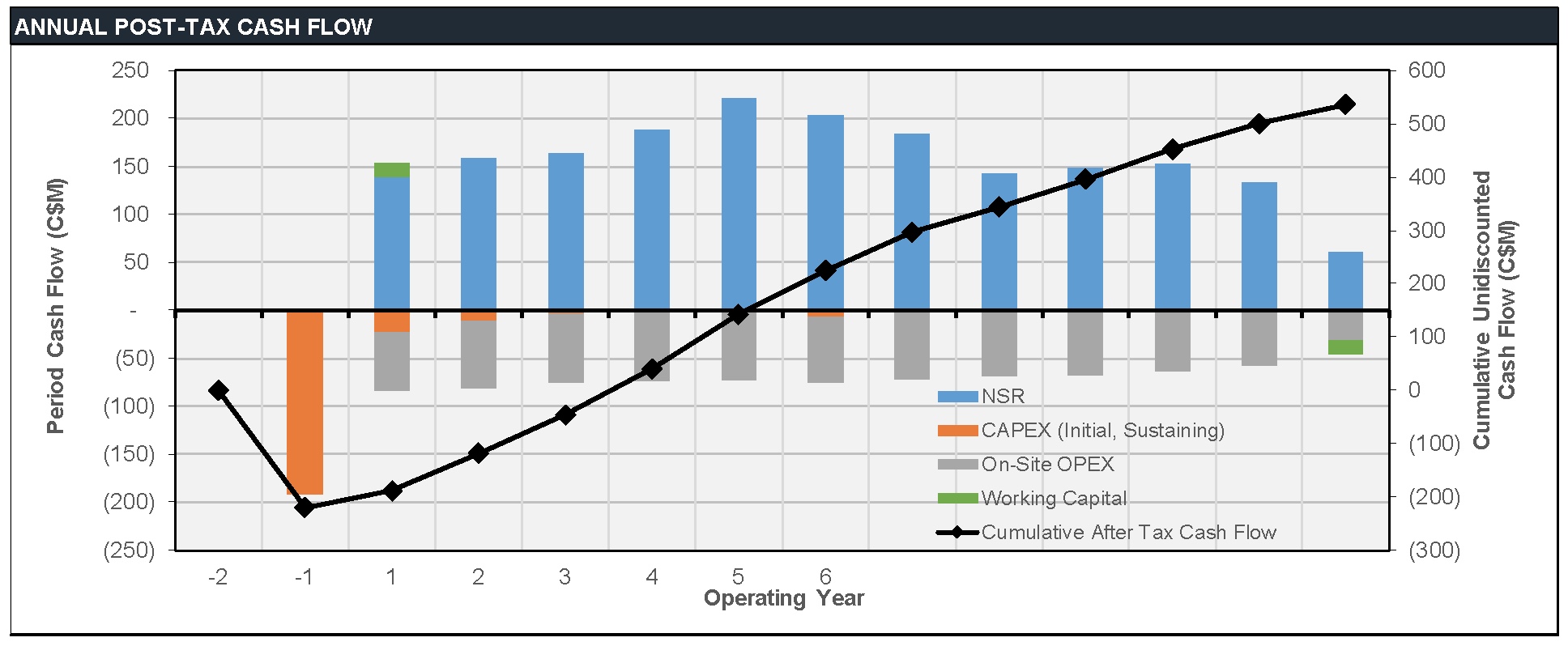

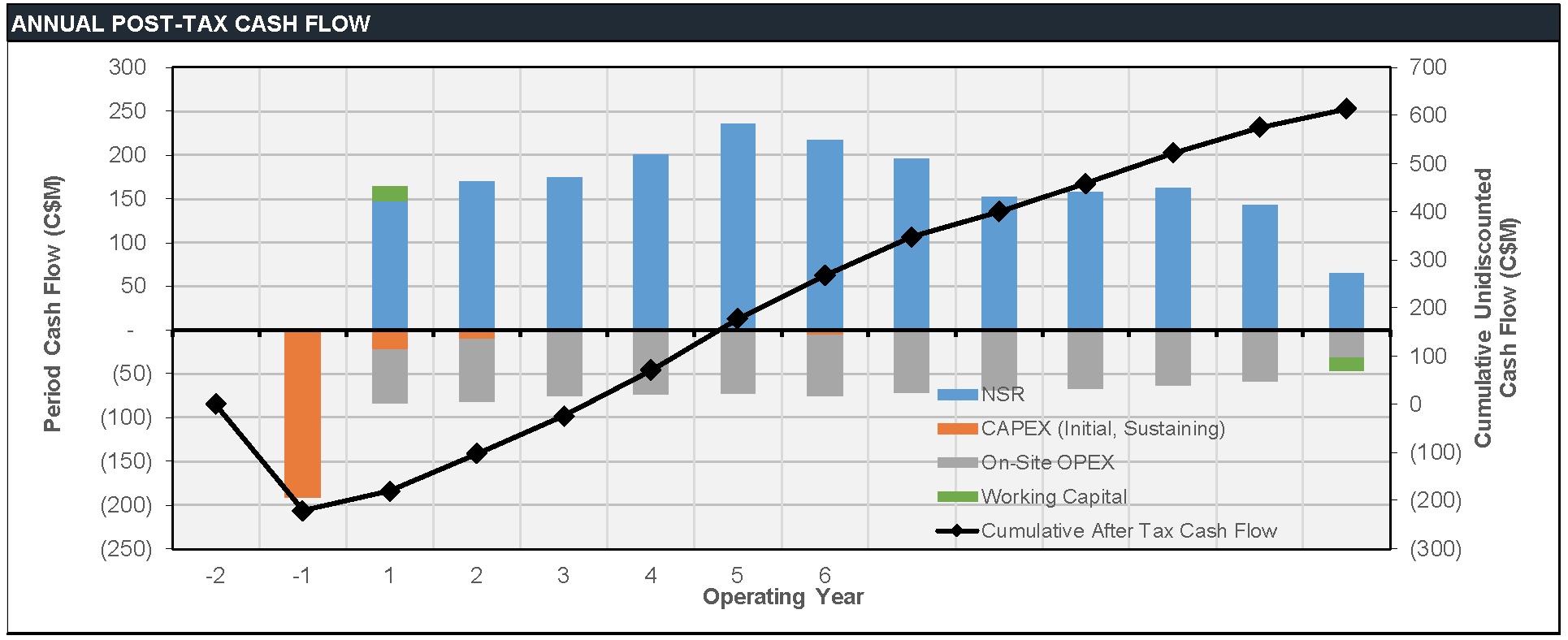

The base case scenario uses a 2,500 tonnes per day production scenario, and the initial capex to build this plant is estimated at just below C$221M, which includes a 15% contingency. This capex includes a pre-stripping expense to remove waste from the open pit part of the Main Zone. Also keep in mind the capex was based on an USD/CAD exchange rate of 1.33. As the exchange rate is currently just 1.29, it’s not unlikely the initial capex (and opex) will be slightly lower than anticipated as some of the materials will be sourced in US Dollar. According to our back of the envelope calculations, applying the current exchange rate on the economics of the project would result in a NPV increase of C$35-50M (on an after-tax basis). Please note, these are our own assumptions and interpretations, and aren’t the company’s official expectations nor guidance.

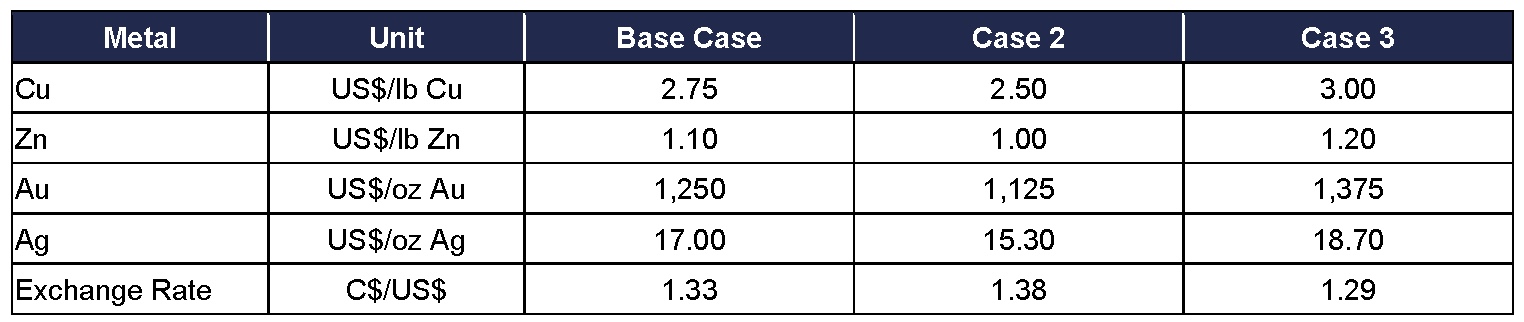

Kutcho Copper’s pre-feasibility study has been based on three different scenarios using different parameters, as you can see in the next image.

It’s refreshing to see the company’s base case scenario is actually relatively conservative. There’s a substantial margin of error (and safety) as Kutcho Copper uses $2.75 copper (11% below spot) and $1.10 zinc (24% below spot) for its calculations. Using these numbers, the Kutcho copper project boasts an after-tax NPV8% of C$265M and an after-tax IRR of almost 28%. Technically, this excludes the impact from the streaming agreement with Wheaton Precious Metals, but we don’t expect any material changes in the fully-loaded Net Asset Value, as the lower revenue from selling the gold and silver at a discount will be compensated by a lower dilution factor to fund the initial capex.

We think it’s fair to use ‘Case 3’ as ‘our’ base case scenario. The copper price used isn’t outrageously high, and the zinc price is still substantially lower than the current spot price. The higher gold and silver price will increase the (negative) impact of the streaming deal, but again, we don’t mind ‘losing’ a few tens of millions of dollars in the NPV if it allows Kutcho Copper to reduce the potential dilution. The US$65M streaming deal will very likely reduce the dilution factor by 90M shares if we would assume a construction funding priced at C$1/share. So whilst the streaming agreement will have a negative impact on the NPV of the project, it might actually have a positive impact on the NAV/share as the share count will be lower as the proceeds from the streaming agreement will reduce the upfront share dilution.

The next table summarizes the after-tax results of all three scenarios. As you can see, the Kutcho copper project would still be a valuable asset under the conservative scenario (using $2.50 copper).

Should these economics be confirmed in a bankable feasibility study, we don’t think Kutcho Copper will have any trouble securing funding to build the mine as even at $2.50 copper and $1 zinc, the after-tax IRR is a very respectable 24%.

But there’s much more additional upside potential

We would really like to emphasize the outcome of the pre-feasibility study doesn’t tell the entire story. The study was based on a 12 year mine life assuming a 2,500 tonnes per day processing scenario for a total ore production of 10.4 million tonnes (10Mt underground and 400,000 tonnes open pit) for a total of 464 million pounds of copper and 735 million pounds of zinc (pre-recovery and pre-payability adjustments).

But as we previously mentioned, the total resources at Kutcho contain approximately 22.5 million tonnes of rock if you lower the cutoff grade to 1% copper (this reduction from 1.5% to 1% increases the tonnage whilst the total impact on the average copper (-equivalent) grade is very minimal). Not all of these tonnes will ultimately end up in the mine plan, but it looks like at least 5 million tonnes could be added to the mine plan just by reducing the cutoff grade.

Not only would this increase the total tonnage in the mine plan by 50%, it will also extend the mine life and perhaps more importantly, it would create an excellent platform for Kutcho Copper to seriously consider expanding its processing capacity to 4,500 tonnes per day. An increased throughput should increase the economics of the project as you’re unlocking synergy advantages and economies of scale and keep the mine life pretty much unchanged.

And there’s more. Although a resource of 22.5 million tonnes already is very respectable, Kutcho Copper can’t rule out additional resource increases. Both the Main Zone and Esso Zone remain open down dip, and Kutcho Copper estimates it could add 1.3-3.6 million tonnes to the resources, potentially extending the mine life. On top of that, we shouldn’t forget the total size of the land package consists of approximately 17,000 hectares (170 square kilometers) with several massive sulphide horizons.

On top of resource expansion, we also expect advanced metallurgical test work to increase the recovery rate of the zinc, and an increased amount of zinc reporting to the zinc concentrate rather than the copper concentrate (which increases the value of the zinc). For every 1% increase of the zinc recovery rate, the total pre-tax undiscounted cash flow will increase by C$5M.

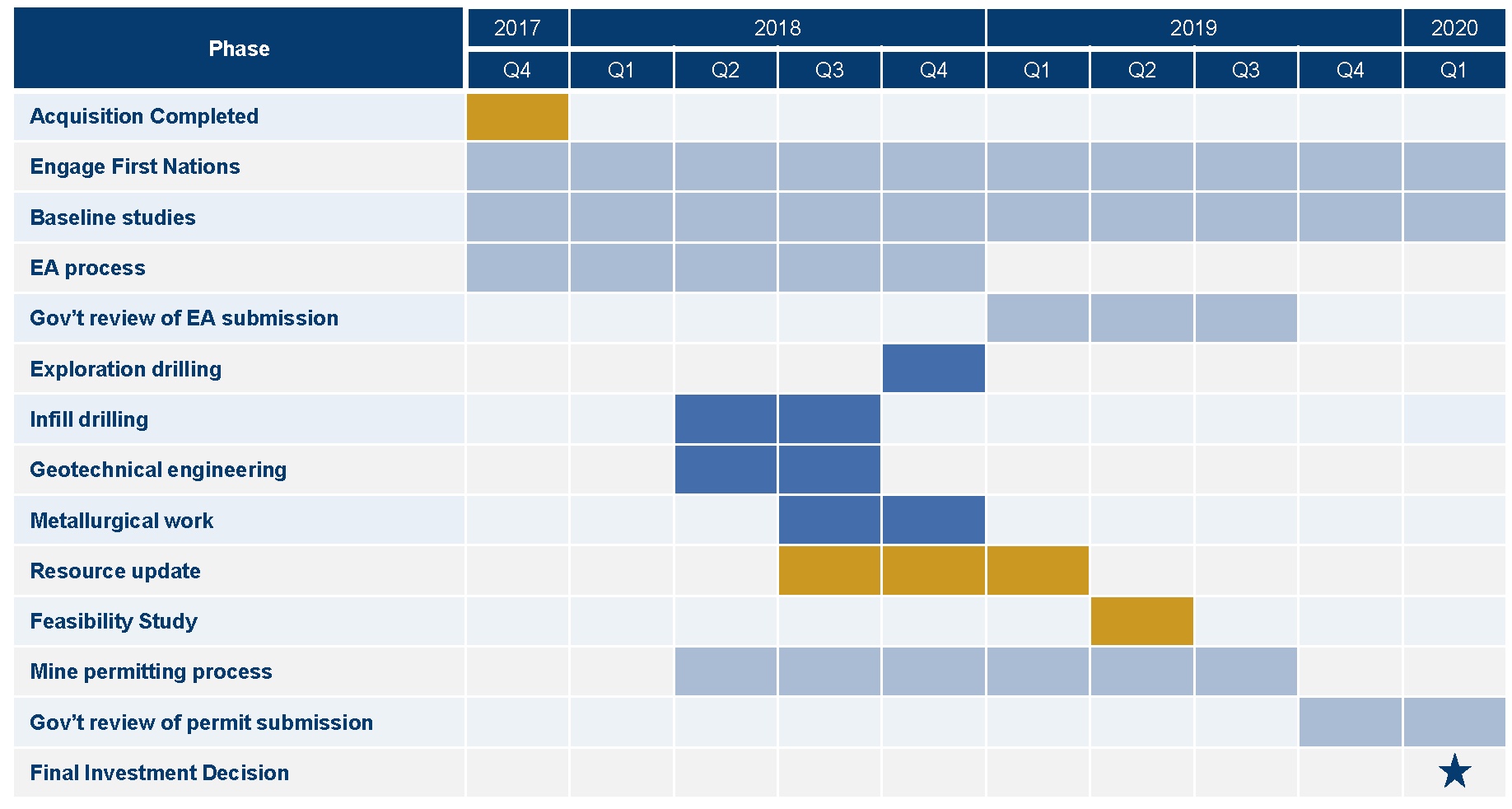

The plans for the next 12 months

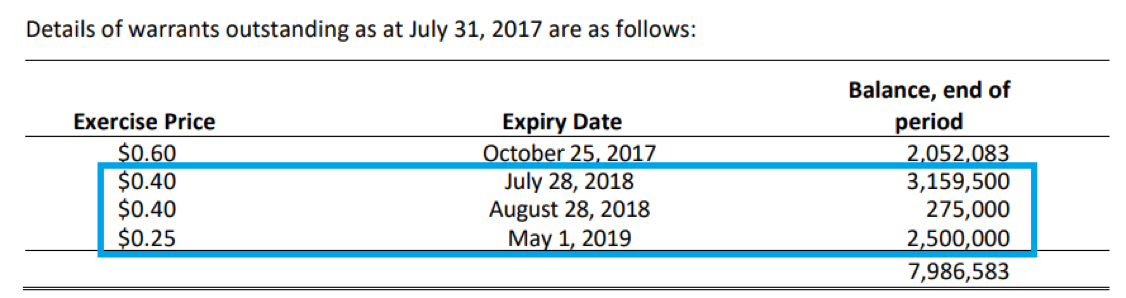

Kutcho Copper has outlined a C$12M investment budget for the next 24 months to complete a feasibility study and the permitting process by the end of 2019. This C$12M will be fully funded by the existing C$4.2M working capital position as well as the expected C$9M payments from Wheaton Precious Metals along the way. Whilst we cannot exclude a small capital raise to top up the treasury just to be safe (although we would hope the C$1 warrants will be ‘in the money’, providing an additional cash inflow on top of the lower priced warrants which will be exercised), Kutcho Copper appears to be fully funded to complete both processes.

Kutcho Copper will immediately start with the baseline studies to prepare for the environmental permit, whilst it will also complete more expansion and infill drilling in 2018, as well as more extensive metallurgical test work. As mentioned before, increased recovery rates and a higher ratio of zinc reporting to the zinc concentrate (rather than the copper concentrate) will improve the economics.

An updated resource estimate is expected in Q1 2019, which will be the basis for an official feasibility study in the second quarter of the year.

Capital Structure

After completing the C$14.7M private placement, Kutcho Copper will have 46.9M shares outstanding, and 69M shares on a fully diluted basis as well as C$20M in debt. Approximately 6 million warrants are currently in the money and will expire within the next 18 months.

Assuming all warrants will be exercised, Kutcho Copper will receive a total cash inflow of almost exactly C$2M. This will increase the total available liquidity to C$13M, strengthening our view that the company won’t need to raise more cash to complete its planned C$12M investment to see the project through the permitting and feasibility stage.

Management team

Vince Sorace – President, CEO & Director

- 25 years experience in capital markets having raised over $100M in equity financing

- Prior roles include Founder, President & CEO of various private and public resource companies

Allison Rippin Armstrong – Vice President, Community & Environment

- 20 years in permitting, regulatory processes and environmental compliance in Canada

- Prior VP of Sustainability for Kaminak Gold

Stephen Quin – Director

- 30 yrs experience in mining & corporate affairs

- Current pres., CEO & director of Midas Gold

- Former pres. & CEO of Sherwood Copper and former pres. & COO of Capstone Mining

Bill Bennett – Director

- Former BC gov’t MLA for 16 years

- Named BC Mines Minister 3 times

- Led improvements to BC Ministry of Energy &

- Mines permitting process; helped launch BC’s

Conclusion

Not only are we charmed by the Kutcho project, its economics and additional potential, we are perhaps even more impressed by the fact Kutcho Copper appears to be fully cashed up to execute on its plans to have this project permitted by the end of 2019 (but just to err on the cautious side, we will assume Kutcho Copper will need three years to complete all necessary steps).

The C$20M loan and C$13M net equity financing (after paying brokerage fees) will provide enough cash to fund the C$28.8M initial purchase price and end up with a few million dollars in working capital. As an additional C$9M will become available from Wheaton Precious Metals over the next few quarters, Kutcho Copper is in a very healthy shape. With an anticipated market capitalization of approximately C$30M (C$0.65 X 46.9M shares) and an enterprise value of C$50M, Kutcho Copper is trading at less than 0.2 times the anticipated (non-optimized) NPV/share (which excludes a potential reserve increase and mine life extension). We believe that as Kutcho Copper starts ticking the boxes along the feasibility and permitting time line, the company’s share price should start to reflect the true underlying value of the project.

If we would assume the addition of 5 million tonnes to the mine plan would increase the NPV by C$100M and apply a ratio of 0.4X NPV for a permitted project with a bankable feasibility study, Kutcho Copper’s enterprise value should be closer to C$150M. This won’t happen overnight, and it’s now up to Kutcho’s technical team and permitting team to unlock the value.

Stay in touch with our weekly newsletter and when we publish a report. Unsubscribe at any time.

Disclosure: Kutcho Copper is a sponsoring company. We have a long position. Please read the disclaimer