Whilst it’s understandable that some of the more marginal cobalt plays have left shareholders and investors somewhat disillusioned in recent markets, it’s frustrating to see how companies that do have good strategies with strong teams and exciting projects are being sold off as well. M2 Cobalt (MC.V) appears to be one of those companies; despite making really good progress on its Uganda-based exploration projects, its share price has lost approximately 60% since reaching a high of C$1.00 in January 2018.

Although a C$0.50 placement recently became freely tradeable, this placement isn’t the culprit as M2 Cobalt’s chart has been declining steadily since the end of February. Seeing the share price drop from C$0.90 on February 27th to just C$0.34 today is painful, as in excessof C$40M has been wiped off M2 Cobalt’s market cap. Based on the 62.8 million shares that are currently outstanding, MC now has a market capitalization of just C$21M, with approximately C$5M in cash on hand (which will be deployed in 2018 as part of an extensive exploration program).

However, for those new to the story or who haven’t pulled the trigger yet, we have the impression the risk/reward ratio has improved since M2 Cobalt started trading again in January. One thing’s for sure: the share price didn’t slide because the exploration results disappointed. Let’s have a look at the achievements of M2 Cobalt in the four months it has been trading.

Bujagali

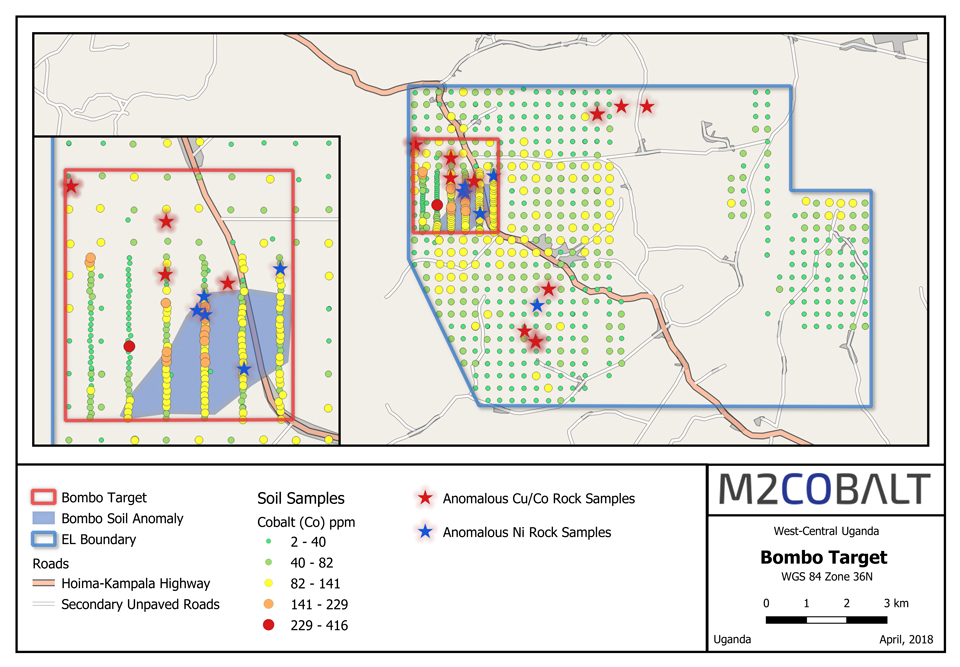

Let’s start with Bujagali, where a surface sampling program has identified several large high-priority targets. One part of the Bujagali property, the Bombo target, was subject to an extensive sampling program, and this immediately paid off with the discovery of a large nickel-cobalt-copper anomaly.

The sampling program unveiled 91 samples which had an average grade of in excess of 101 ppm Nickel, with 13 samples returning values of in excess of 0.1% Nickel. And it definitely is a polymetallic target, as no less than 86 samples returned cobalt values of in excess of 100 ppm cobalt.

A good start, and M2 Cobalt immediately started an ‘infill sampling program’, which has been completed. Taking more samples should help the company to fine-tune the high priority trenches it is currently digging and focus drill targets to improve the odds of finding a significant mineralized body. But with several samples returning in excess of 0.1% cobalt on surface, it’s clear this 900 by 1200 meter zone represents a serious anomaly.

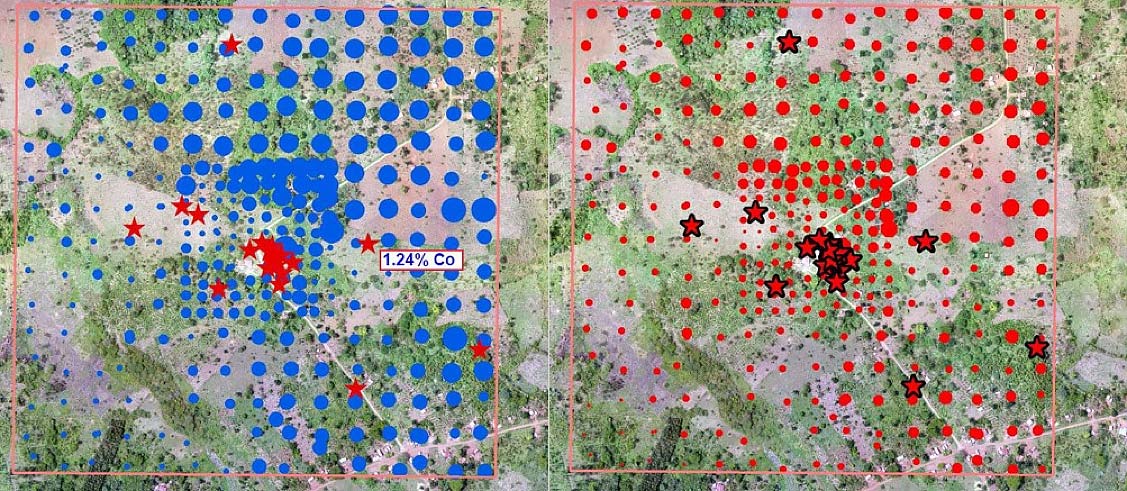

But just one week later, M2 Cobalt surprised us again when it announced the discovery of a second large anomaly. Another extensive soil and rock sampling program at its Waragi target outlined a clear cobalt-copper target (there doesn’t seem to be any nickel associated with this discovery). As you can see on the next image, this anomaly is very clearly defined as the high-grade cobalt rock samples coincide with the areas where the highest grade cobalt occurrences in the soils were encountered…

The two sets of assay results indicate there’s something there (the stars indicate a concentration of high-grade samples). We actually like this target even better than Bombo due to the abundance of high-grade cobalt samples:

Of course, we are the first ones to admit this is ‘just a sampling program’, and the real proof will be in the pudding. But we don’t think anyone will deny that this is a really juicy exploration target. M2 Cobalt seems to be sharing that opinion, as the company has already mobilized its trenching crews to immediately start a trenching program on both the Bombo and Waragi targets.

These trenches are 30-90 meter long and will help the company to get a better understanding of the stratigraphy, and will allow M2 Cobalt to check how the mineralization behaves at depth. The M2 Cobalt website already contains pictures of the trenching program, and just yesterday, the company confirmed it completed 21 trenches. Assays are still pending, and will be used to pinpoint the targets for a late summer drill program.

We expect to see initial trenching results throughout June as well as results from further infill sampling at both Waragi and Bombo and additional sampling results from across the remaining 3 licenses at Bujagali as ground crews expand the work program. Remember the above targets were discovered on the first 2 license areas explored under the current work program.

Kilembe

At Kilembe, M2 Cobalt has completed its airborne geophysical survey which will help M2 to make a high priority list of VMS targets on its Kilembe licenses. It will be interesting to see which ‘signature characteristics’ of deposits similar to the past-producing Kilembe copper-cobalt mine will show up. Based on statistics from other similar deposits globally, the company anticipates discovering a number of buried sulphide deposits similar to the deposits which comprise the historic mine.

Once the results of this airborne survey are interpreted, M2 Cobalt will very likely immediately start a focused geochemical / sampling program to prepare for trenching / drilling. VTEM surveys have the potential to significantly speed up exploration programs.

The Company has indicated that it has identified several anomalies and is currently finalizing interpretation on these. As it has been a while since we saw an update on M2’s exploration programs, as with Bujagali, we are expecting to see ongoing news-flow relating to the Kilembe properties over the next several weeks. A first update was released yesterday, when M2 Cobalt confirmed the discovery of two anomalies on the Kilembe properties. Those anomalies were discovered in the aerial survey, which consisted of 3,075 line-kilometers, and on top of those two high priority anomalies, an additional 184 ‘lower priority’ anomalies were detected. This gives M2 Cobalt plenty of information to deal with, and the company will undoubtedly follow up on this in the next few months.

Insiders are buying more stock

What we perhaps like most about M2 Cobalt is that its management and board doesn’t just ‘talk the talk’, but also ‘walks the walk’. Over the past few weeks, we have seen some serious insider buying. We have added all stock purchases (as filed on SEDI) from April 1st until June 1st in the table here below:

And they continued to buy more stock in June:

As you can see, four insiders have spent in excess of C$90,000 on buying more stock, at a substantially higher price than where M2 Cobalt is currently trading at. It’s always great to see insiders buying more stock as writing cheques from their own money is a good sign as it indicates they think the company’s share price is too low.

The cobalt price has only increased since our initial report

Just as a brief reminder, we’d like to refresh your memory about cobalt as a commodity, and the cobalt sector as a whole.

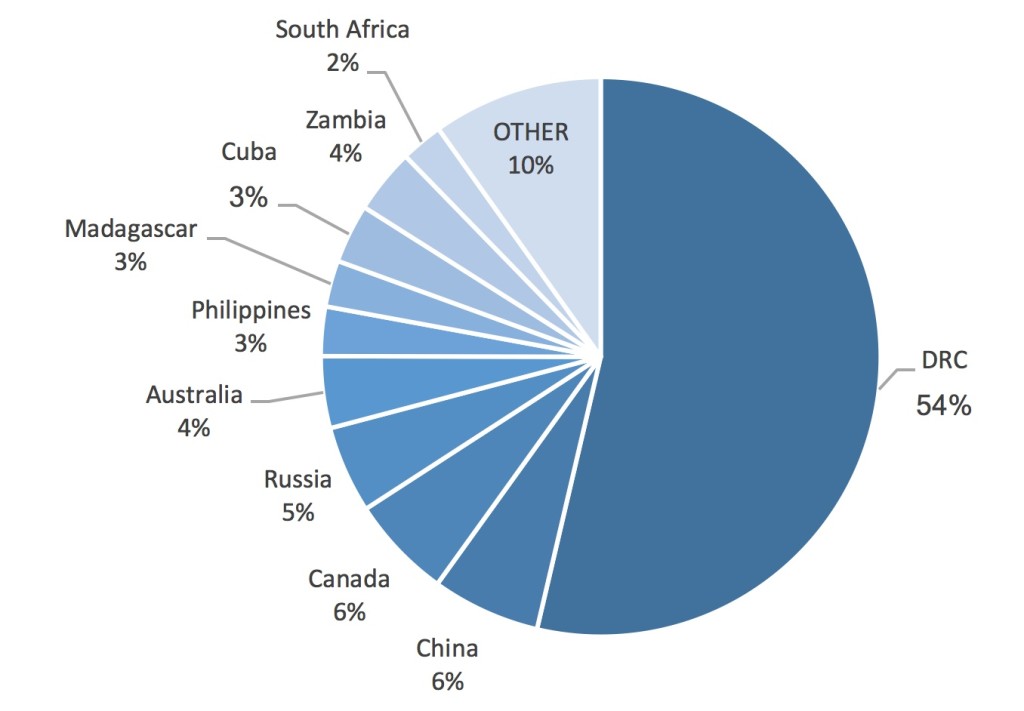

The EV sector is booming and demand for the main components of the batteries used to power these vehicles continues to increase. The main issue with cobalt is that the world supply is relying on an uninterrupted supply from the Democratic Republic of the Congo (DRC), which accounts for approximately 2/3rd of the world production of cobalt, a figure which is forecasted to grow.

Needless to say this is a dangerous situation as the DRC isn’t the most stable country in the world (understatement), so the supply chain could easily be disrupted. Combine an uncertain supply with booming demand, and you’ll understand the end users of cobalt would love to diversify their supply sources.

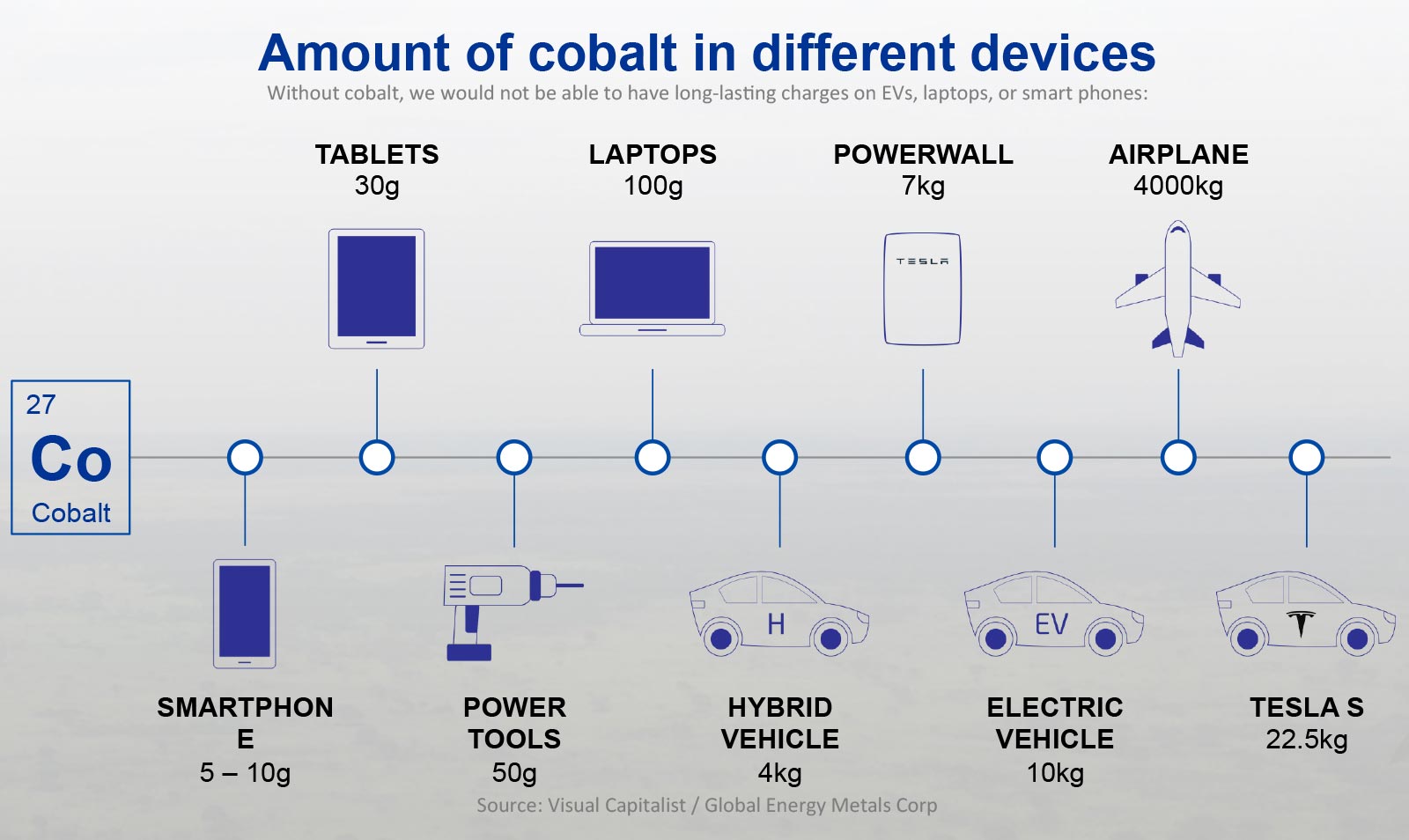

Images can tell more than words and the next few charts don’t need any additional explanation.

There’s only one conclusion; the world needs more (viable) cobalt projects to make sure the supply deficit doesn’t disrupt the battery sector.

And the cobalt price? It just continues its run as the metal is currently trading at approximately $82,000 per tonne ($37.20 per pound), 10% higher than on January 1st.

Conclusion

As of at the end of March, M2 Cobalt still had a working capital position of approximately C$6.0M. Although we expect the company to have spent at least an additional C$1M on exploration and overhead by now, it’s clear the current market cap remains underpinned by a healthy cash position representing approximately 7 cents per share.

With a current market capitalization of C$21.4M (C$0.34 X 62.82M shares), M2 Cobalt appears to be more attractively priced than ever before. Nothing has changed since January when M2 Cobalt raised C$8.5M at a significantly higher share price, except for the fact M2 has now made several highly promising discoveries with additional assay results due any week now. And those who are ‘in the know’ have been buying stock at much higher prices than where M2 Cobalt is trading at today.

Disclosure: M2 Cobalt is a sponsor of this website, we have a long position. Please read the disclaimer

Pingback: M2 Cobalt Featured on CaesarsReport.com | Investing News Network