Although not as sizeable as in North America or Australia, Europe does have a mining scene. There are several large open pit copper mines in Spain while there are gold and base metals mines in Scandinavia as well.

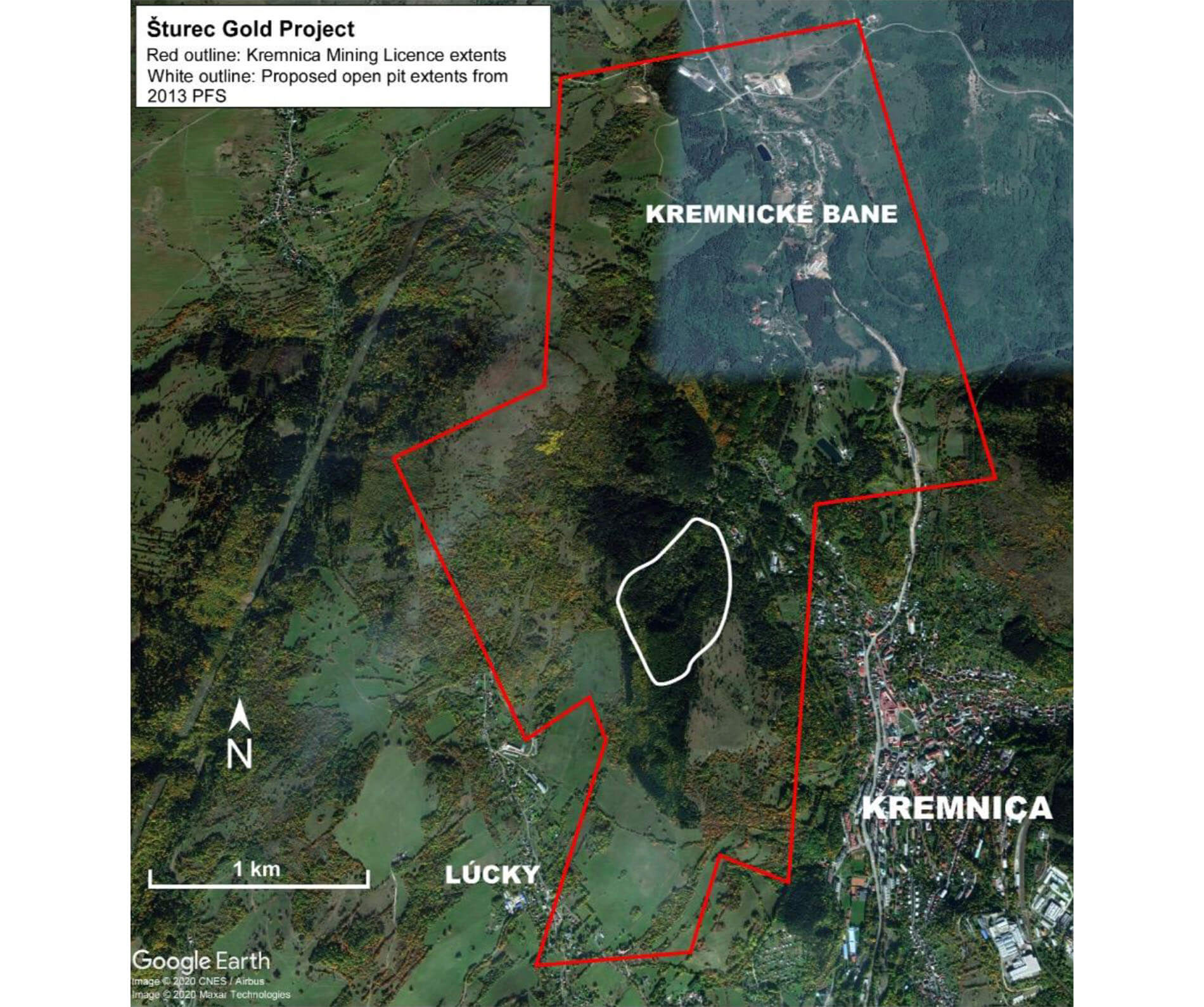

MetalsTech (MTC.AX) was able to acquire the Sturec gold project in Slovakia right before the COVID pandemic and despite the pandemic, the company was able to put some boots on the ground and recently completed a drill program which should result in a resource update before the end of this month. Once owned by the Slovakian Government and several publicly listed exploration companies, the Sturec project has been around for a while, but this Australian company appears to have a clear path forward with an emphasis on securing the social license from the local communities while adhering to all best practices on the environmental front. The Sturec gold mine has historically produced over 1.5 million ounces of gold and 6.7 million ounces of silver worth close to US$3B at today’s metal prices.

While the ink of the updated resource will still be drying, MetalsTech will get the drill rigs turning again to provide yet another resource update and a scoping study before the end of the year.

The Sturec Gold project: in the final straight line to a resource update

MetalsTech acquired the flagship Sturec gold project in 2019, when the market wasn’t too interested in gold stories. This allowed MetalsTech to scoop up the project almost for free: after paying an initial A$30,000 in cash to acquire an option, it had to pay just A$720,000 in cash to purchase the project outright, subject to very high hurdle performance based milestones on a certain amount of ounces in the ground (rather than a revenue based royalty). There are no royalties on the mine (other than a standard 1.5% NSR attributable to the Slovakian government).

An ultra cheap acquisition, considering the project had already been thoroughly explored resulting in a historic JORC (2004) compliant resource.

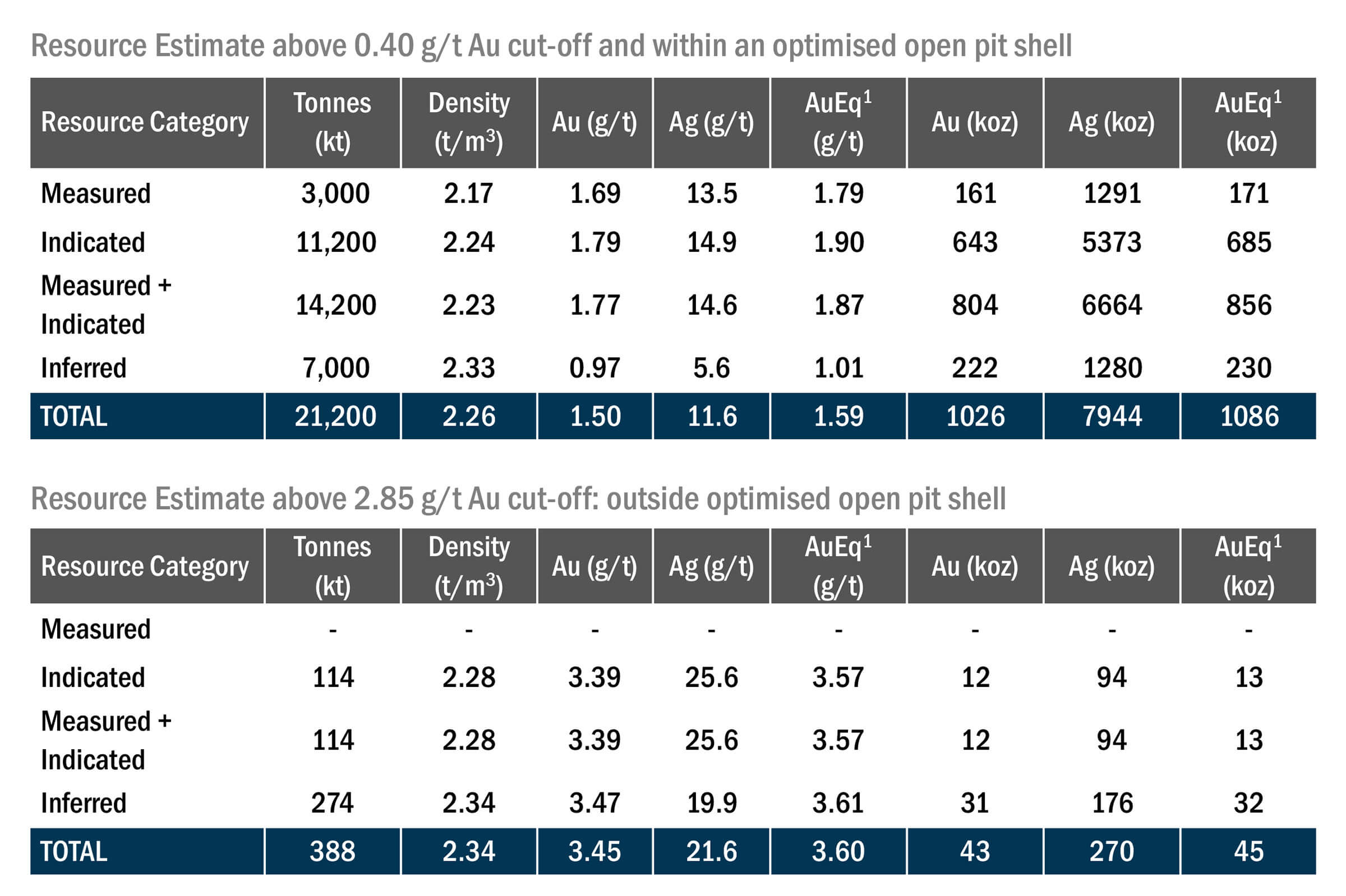

In April 2020, MetalsTech completed an independent JORC Resource compliant to the latest 2012 standard equal to 21.2Mt @ 1.50 g/t Au and 11.6 g/t Ag, containing 1.03Moz of gold and 7.9Moz of silver on an open cut scenario with a further 388kt @ 3.45 g/t Au and 21.6 g/t Ag containing 43koz of gold and 270koz of silver on an underground basis.

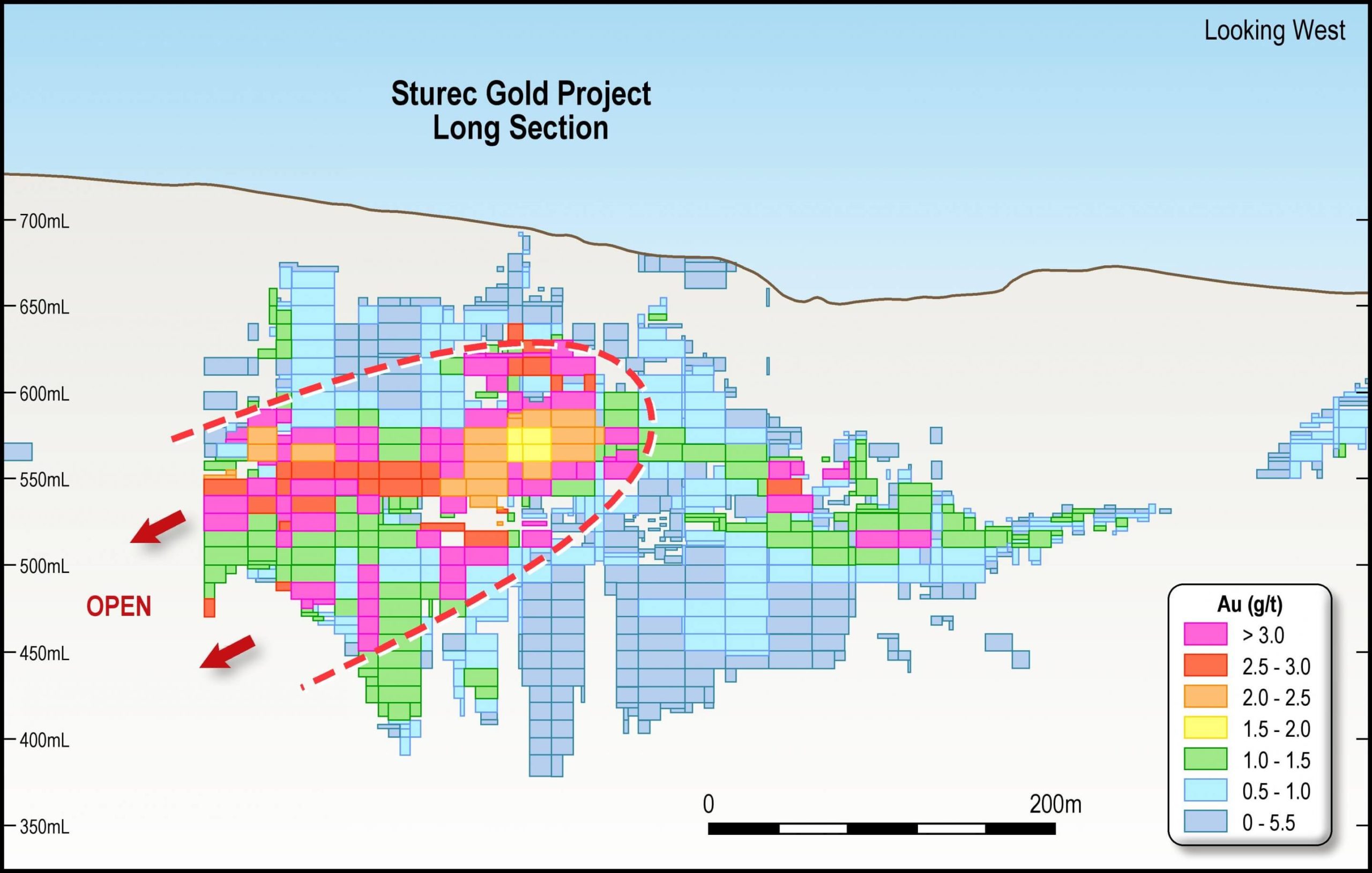

The resource estimate above will be irrelevant very soon as MetalsTech is working on an updated resource estimate which should be released around mid-June. The updated resource will be moving away from looking at Sturec as a large open pit gold mine as MetalsTech will further develop the project using a new angle.

The previous operators only looked at Sturec as a very large open pit mine, with a large environmental footprint. While that’s a valid development plan, MetalsTech will actually focus on developing a low environmental impact initial underground mine with potential for a smaller low strip ratio open cut operation in later mine life years. The underground areas should carry a higher grade which will allow MetalsTech to shrink the daily production rate to achieve critical mass, thereby sharply reducing the initial capex (likely to less than $100M) while keeping the local communities happy as the ecological footprint of an underground mine will be very low. There is also an opportunity for MetalsTech to build the mine in stages, making the capital and funding requirements more manageable if the mining sector becomes volatile in the future.

That also is one of the main reasons why MetalsTech was able to acquire the project on the cheap: the previous operators were so focused on a large open pit mining scenario they didn’t even consider looking at the project as an underground mine to start with and that’s what sets MetalsTech’s approach apart from the previous operators. Sure, you could look at Sturec as a ‘recycled’ project. But this will effectively be the first time ever the project will be advanced as an underground mine and that’s a whole different angle that has its merits.

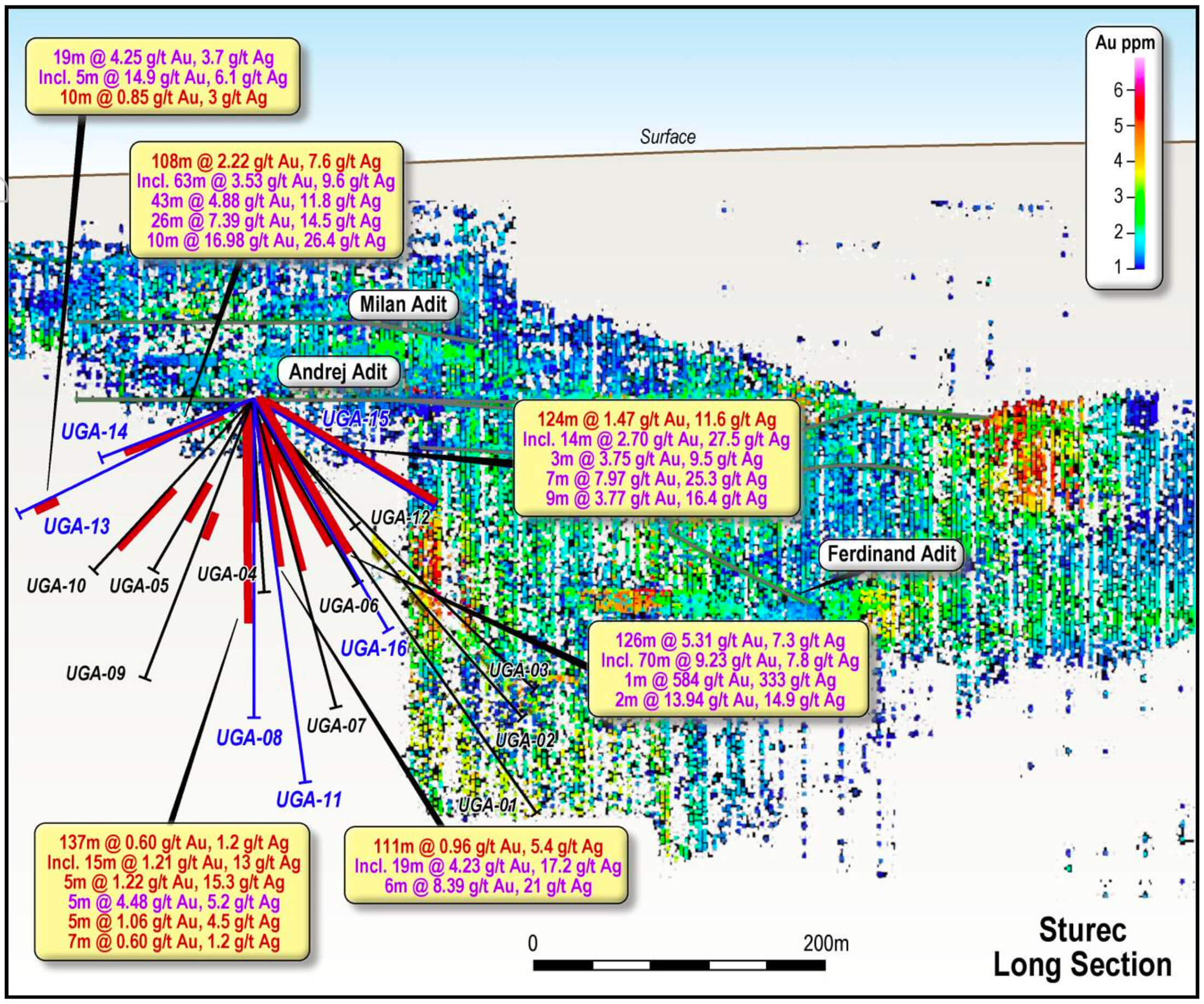

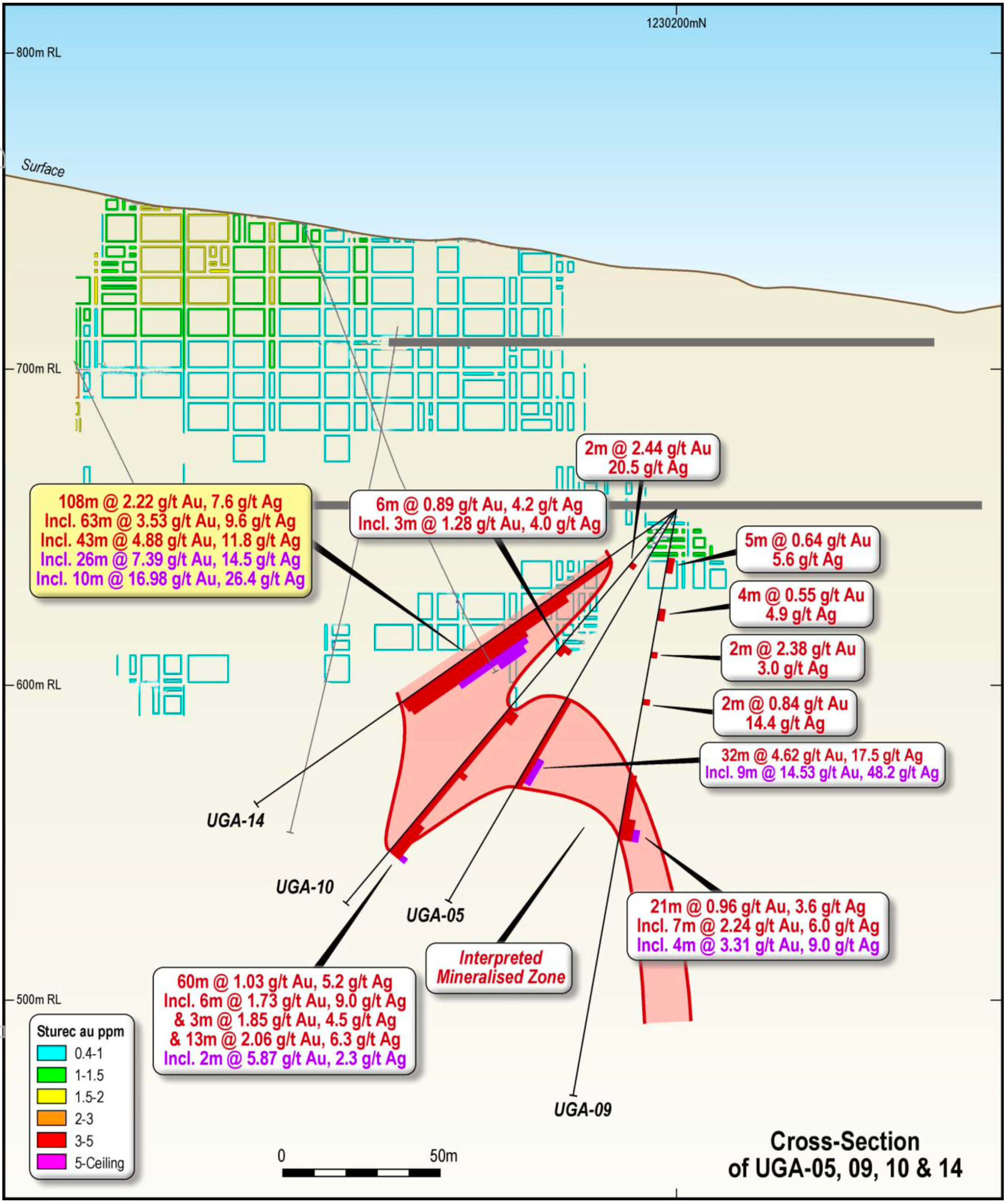

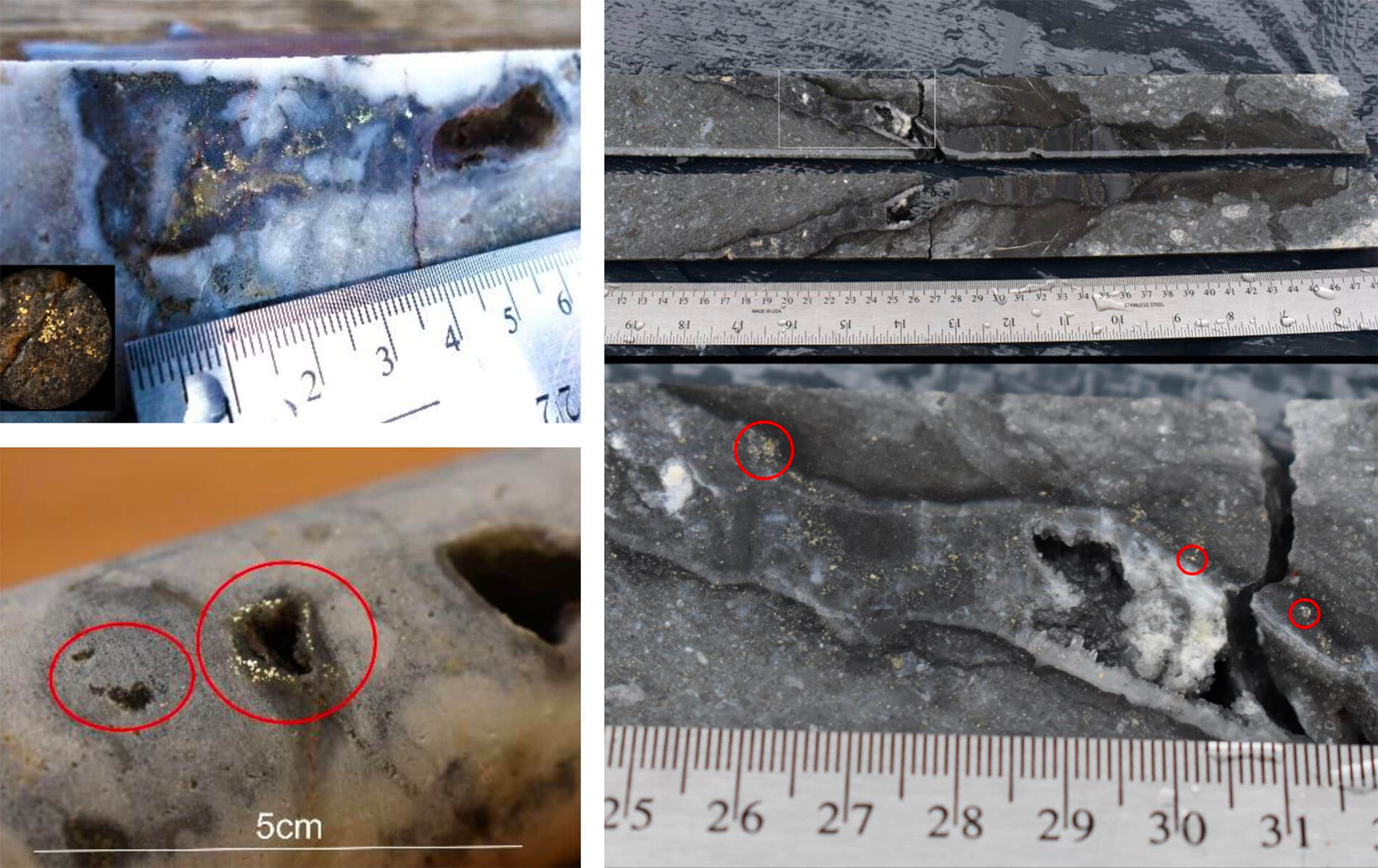

Focusing on the higher grade underground zones gained a lot of credibility during the 2020 and 2021 drill program as the drill bit intersected high grade and even ultra high-grade gold mineralization at Sturec. The most recent exploration update for instance included the highest grade gold intervals ever encountered at Sturec with a headline result of 70 meters of 9.23 g/t gold. Granted, this was predominantly caused by a 1 meter interval of 584 g/t gold and 2 meters of 13.94 g/t gold, which means the residual 67 meters contained just about half a gram of gold per tonne of rock, but in an underground mine scenario MetalsTech will be able to mine the juiciest intersections (like the for instance the 2 meters containing 13.94 g/t gold). And of course, some of the other holes contained more consistent high-grade mineralization with for instance 7 meters of 7.97 g/t in hole 15 followed by 9 meters of 3.77 g/t gold just 22 meters below that 7 meter interval. All these intervals should meet the economic cutoff grade which we estimate will be around 2.5-3 g/t gold for an underground resource.

Every completed hole gives MetalsTech a tonne of data to work with and by refining the raw data from the 2020 and 2021 drill programs, follow-up drill programs will be able to zoom in on the high grade intersections to put an underground mine plan together.

The gold is clearly still there at Sturec and we wouldn’t be surprised to see the global resource come in at around 1.5 million ounces gold equivalent. But the underground and higher-grade resource will be more important as that will be MetalsTech’s sole focus. And all recent drill results seem to lend more credibility to the underground thesis.

What about the cyanide ban in Slovakia?

The main complication at the Sturec gold project isn’t the geology nor the grade. A few years ago, Slovakia introduced a ban on the use of cyanide which means MetalsTech will have to pursue a slightly different approach. Rather than using cyanidation as the final step of the recovery process at the project site, MetalsTech will be working with a simple gravity and flotation flow sheet whereafter it will be able to sell the concentrate for further processing abroad. Poland would be an option, as it’s just a few hours away and the trucking cost to haul high-grade concentrate would be negligible in the greater scheme of things. But there are several options on the table as a small-scale mine nearby is selling its concentrate to a West European buyer.

So while the ban on the use of cyanide appears to be a major deterrent, there is a good workaround as the aforementioned gravity + flotation flow sheet results in a recovery rate of up to 88% for the gold and about 60% for the silver. Using cyanide could bump this up to 97-98%, but that would also come at a higher initial capex. And at the current gold price, recovering 88% of the gold and saving tens of millions in initial capex (assuming the cyanide ban could even be overturned) clearly is the most optimal scenario.

By complying with the cyanide ban, MetalsTech is also showing its goodwill to the local population as ultimately, obtaining the social license and the go-ahead nod from the local communities will likely be important elements of the permitting process further down the road. And another reason why we certainly appreciate MetalsTech’s approach is because it’s not minimalizing the cyanide ban. The company isn’t aiming to overturn the ban and isn’t stubbornly going ahead with an open pit mine design. MetalsTech clearly communicates about the cyanide ban in its corporate materials and isn’t even trying to sweep it under the rug as a fait-divers. The company seems to be upfront and honest about its quest to become a good corporate citizen of the local communities and an underground cyanide-free mine will go a long way to get the nod of approval from the local communities.

So while the cyanide ban certainly is annoying, it is not a dealbreaker for the project as it stands. Perhaps selling a concentrate (or trucking the concentrate to Poland for further processing) is a bit unorthodox, but based on the currently available data, it’s a scenario that would clearly work in the current gold price environment.

Going forward: more drilling, and a scoping study

An updated resource is around the corner, and that resource will merely be a starting point for MetalsTech. The company is anticipating to start drilling again in the next few weeks and has earmarked about A$1.5M for wildcat drilling and about A$2M for additional step-out drilling.

The latter portion of the upcoming drill program is pretty straightforward: the A$2M program will consist of further step out drilling along strike to grow the resources further as well as infill drilling to further increase the confidence in the gold resource while we also expect the company to drill a few deeper holes to test the mineralization at depth. After all, that’s where we think the low-hanging fruit is to rapidly expand the underground resource again. The June resource update will remain limited to the areas within 300 meters from surface, but the mineralization obviously doesn’t end at that arbitrary depth. Punching a few holes below the known mineralization will help to add a few million tonnes to the resource before the end of the year.

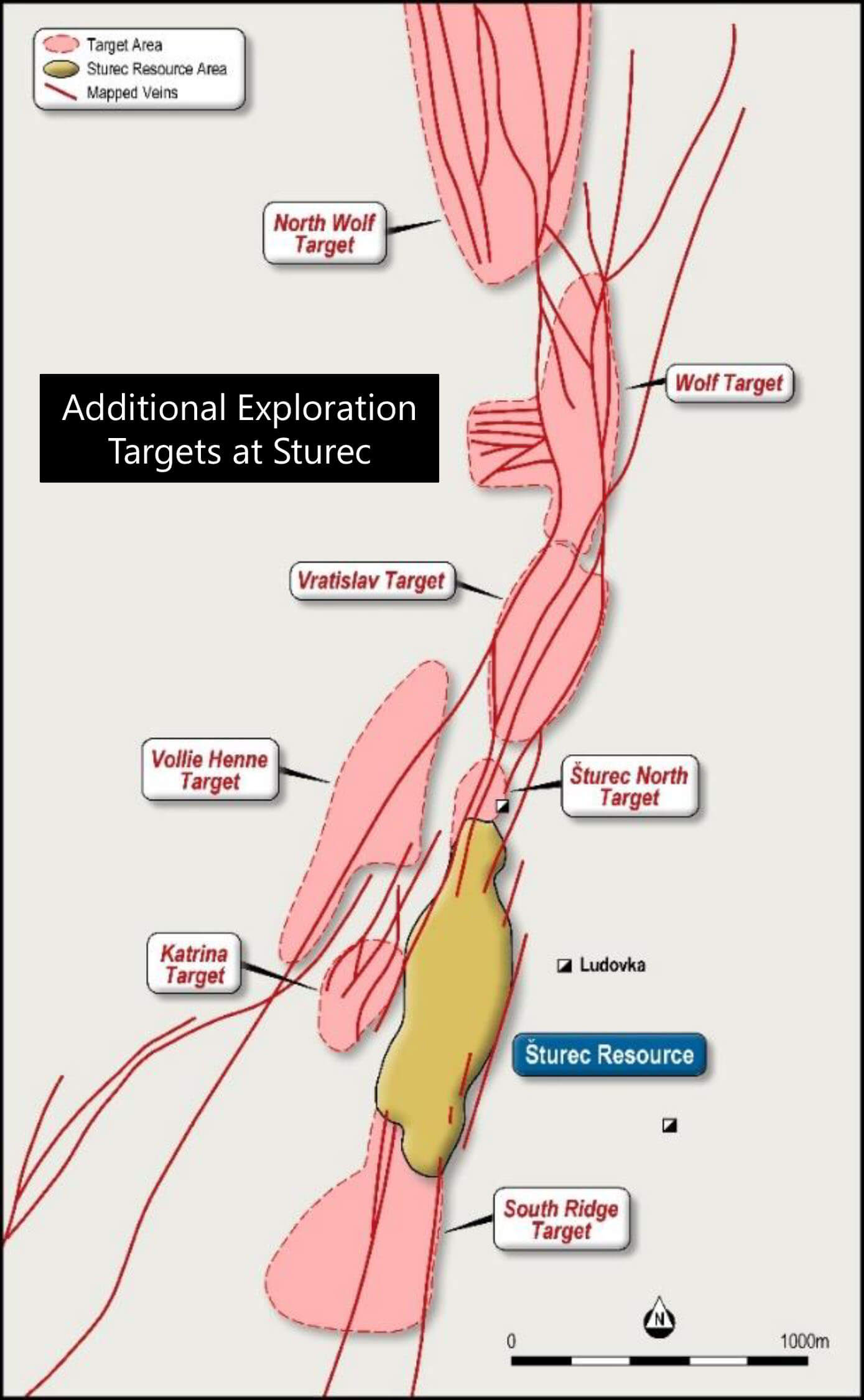

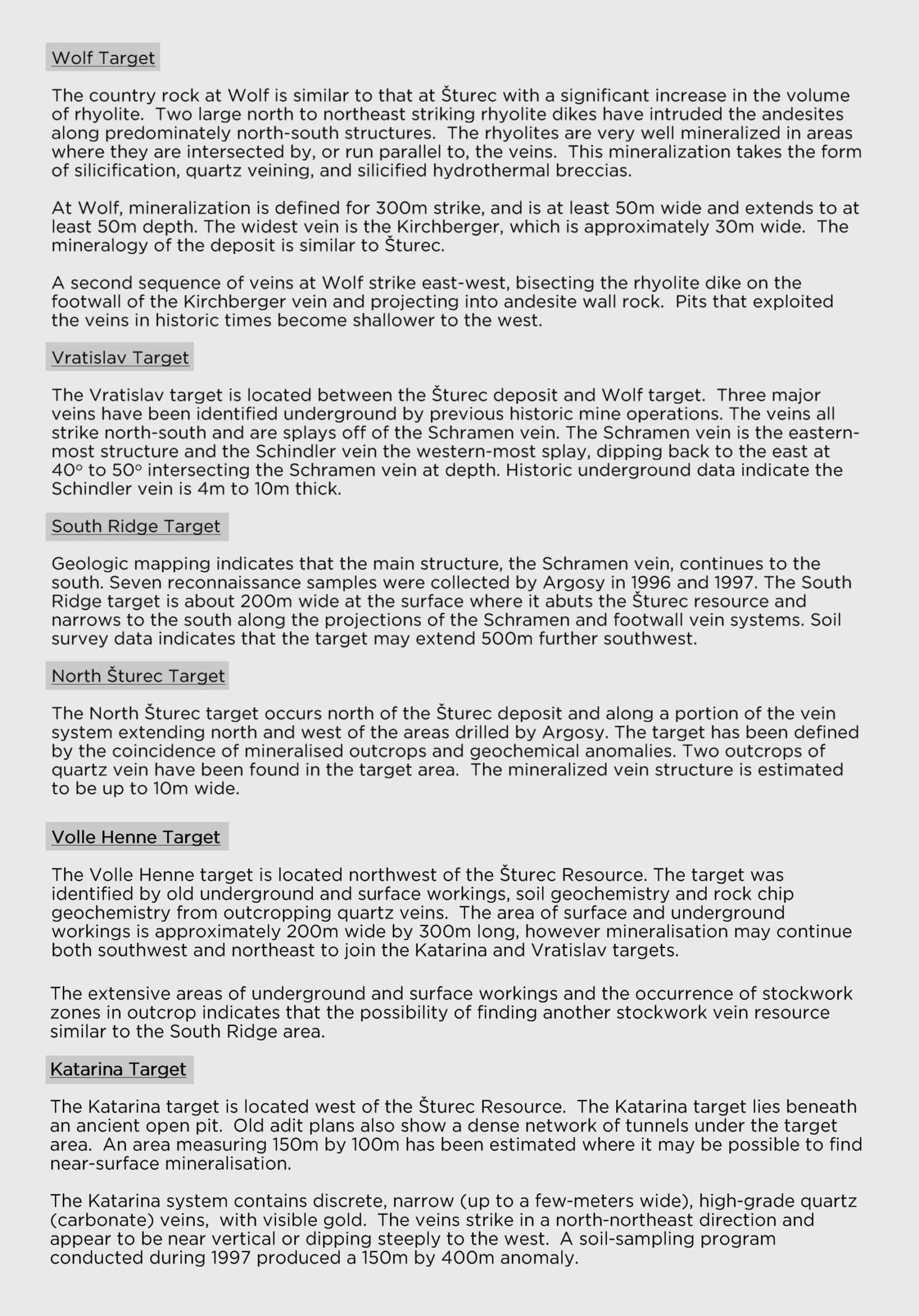

The wildcat drill program will be interesting to follow as well. The term ‘wildcat’ obviously doesn’t mean MetalsTech will be drilling based on dowsing rod generated targets. As you can see on the image below, the areas surrounding the gold resource at Sturec appear to be inviting for additional exploration.

As you can clearly see on the image above, the Sturec resource area is just a small portion of the total prospective land package on the project. At the Volle Henne target for instance, which is just a few hundred meters northwest of the resource, a historic channel sampling program detected 40 meters of continuous ultra high-grade mineralization. Clearly an indication the gold mineralization is widespread on the Sturec land package, and drilling some of these targets will provide more detailed information which could then be used by the MetalsTech technical team to further refine and define its drill targets at Stores.

And as you can see on the image above, there are plenty of exploration targets and the main details of all targets (which obviously won’t all be drilled right away) were nicely summarized in the acquisition press release:

The drill data gathered from this summer’s drill program will then be analyzed and likely used to put yet another updated resource estimate together, which will then be the basis for the scoping study (a little more advanced than what’s known as a Preliminary Economic Assessment in Canada, but not yet pre-feasibility stage). That scoping study should provide a lot more details on the mine plan, the anticipated capex (which we anticipate will likely be less than $100M as it’s a simple gravity and flotation process) and the economics of the mine.

This means the next few months will be packed with updates from MetalsTech: a resource is around the corner, we should continuously see assay results throughout the summer which should subsequently result in an updated and upgraded resource and scoping study in November.

MetalsTech will have almost A$7M in cash after an excellent deal on its lithium portfolio

Any company who’s committing to a decent-sized drill program obviously needs cash. While MetalsTech currently has less than A$1M in cash, it is expecting an A$6M cheque any day now.

As the focus of the company is now clearly on the Sturec gold project, it was able to monetize the legacy lithium assets in Canada. Those assets will be spun out from MetalsTech into a new entity called Winsome Resources (Proposed ASX Code: WR1) and coinciding with this spinoff, MetalsTech is selling a royalty on the lithium exploration projects and that cash will be retained in MTC.

In a first stem, MTC will receive A$6M in cash from the sale of a 3% gross revenue royalty to Lithium Royalty Corp, a North American royalty company backed by behemoth natural resources and energy investor Riverstone Holdings LLC. Subsequent to receiving the A$6M (which is expected any day now), MTC will call for a shareholders meeting to vote on the plan to spin off the lithium assets in Winsome Resources, where after MTC shareholders will also receive 45 million free shares of Winsome. Based on the current share count of MetalsTech, this represents about 1 new share of Winsome per 3.4 shares of MetalsTech owned. Chairman Moran confirmed this spinout would happen in the most tax efficient way possible.

The value of Winsome Resources will be underpinned by LRC committing to an A$3M financing at A$0.20/share. So on a pro-forma basis, owning one share of Metaltech should result in a pro-forma Spinco distribution of almost A$0.06/share. Great, but we consider this to be just the icing on the cake as the cash inflow from the royalty sale is by far more important.

While Winsome Resources and the lithium projects fall outside the scope of this report, the key element to remember is the A$6M cash inflow from the royalty sale. That cash will allow MetalsTech to complete an A$3.5M drill program in the second semester, complete a scoping study based on yet another resource update. And it’s quite likely the company will likely still end the year with about A$2M in cash.

Additionally, there are approximately 12.4 million options with an exercise price of A$0.25 expiring in July. While the options are currently slightly out of the money, it’s not unreasonable to expect a stronger share price on a resource update which could put the options in the money and add A$3.1M in cash to the treasury upon exercise.

Conclusion

MetalsTech has a lot going for it. The sale of the royalty on the lithium assets was brilliant and spinning off the lithium assets in a new company will help MetalsTech to keep the story straightforward and simple as a gold story in Slovakia. While the cyanide ban in Slovakia is a disappointment, there are several other options and trucking a gold concentrate to Poland for further processing and refining appears to be a viable option.

The resource update should be out shortly and we hope to see a global resource of 1.2-1.5 million ounces with an underground component of about half a million ounces, ideally at a grade of around 2.8 g/t or higher. That underground component will drive the economics of the project as MetalsTech isn’t planning on developing an open pit mine. While half a million ounces doesn’t sound like much, it will be a solid base to further increase the resource with the Summer 2021 drill program.

With a market capitalization of A39.2M and almost A$7M in cash, the risk/reward ratio at MetalsTech appears to be promising as the NPV of an underground mine development scenario should be a multiple of the current market cap. Now it’s up to MetalsTech to continue to aggressively advance the Sturec project!

Disclosure: The author has no position in MetalsTech. MetalsTech is a sponsor of the website. Please read our disclaimer.