Oroco Resource Corp. (OCO.V) is ticking all the boxes ahead of a company-defining drill program in 2021 which will hopefully convert a substantial portion of the plus 1 billion tonnes of rock in the historical resource estimate into a fully NI 43-101 compliant resource estimate.

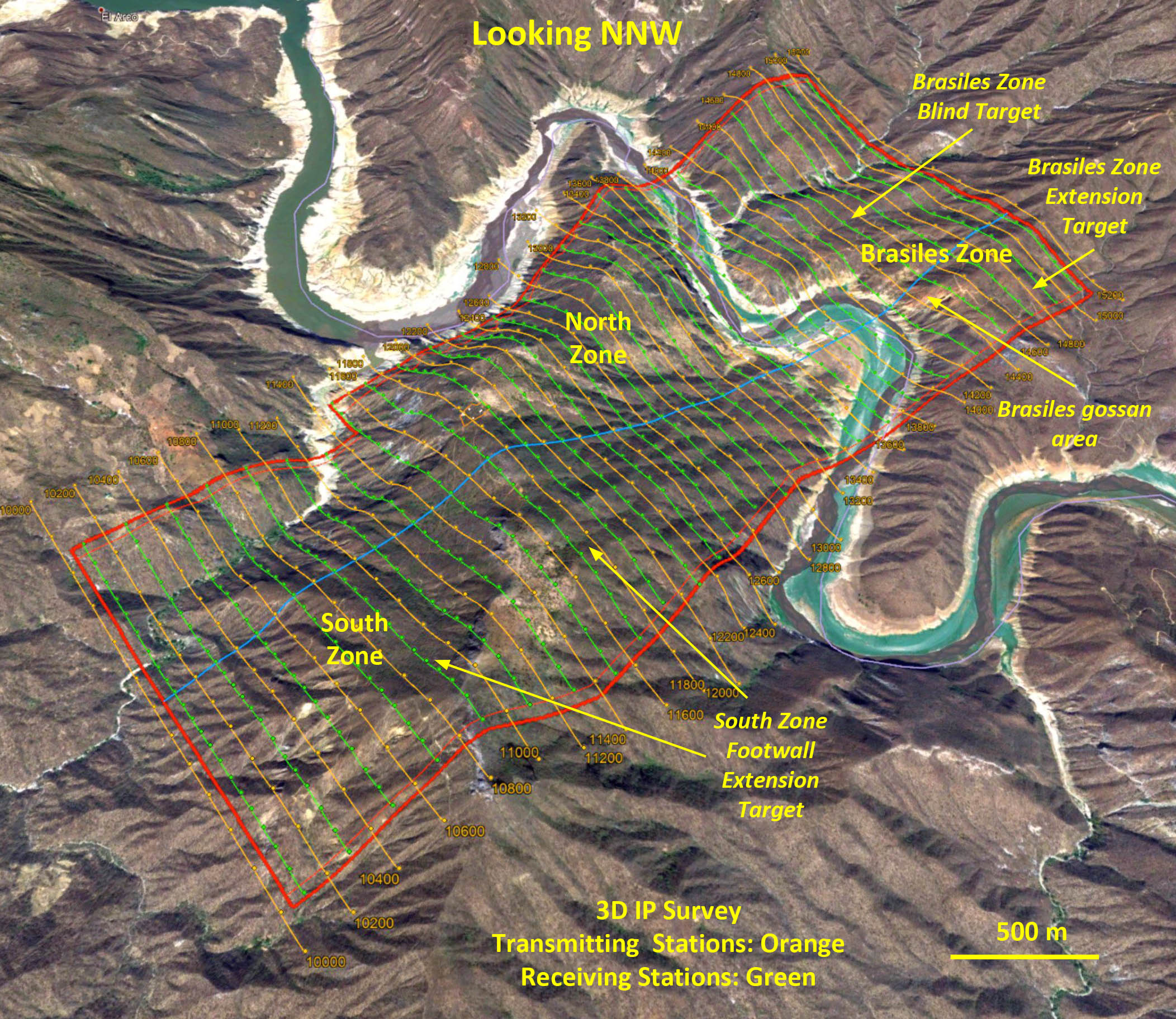

The company recently raised in excess of C$7M in a placement priced at C$0.60 and the preliminary results of the IP survey over the South Zone, which is currently in progress on the South, North and Brasiles zones have now been released. It’s still early days but it is very encouraging to see the IP survey seems to confirm (with chargeability anomalies within and beyond the area defined by historical drilling) the size of South Zone. More IP results are underway, and Oroco is gearing up for a substantial multi-rig drill program in 2021.

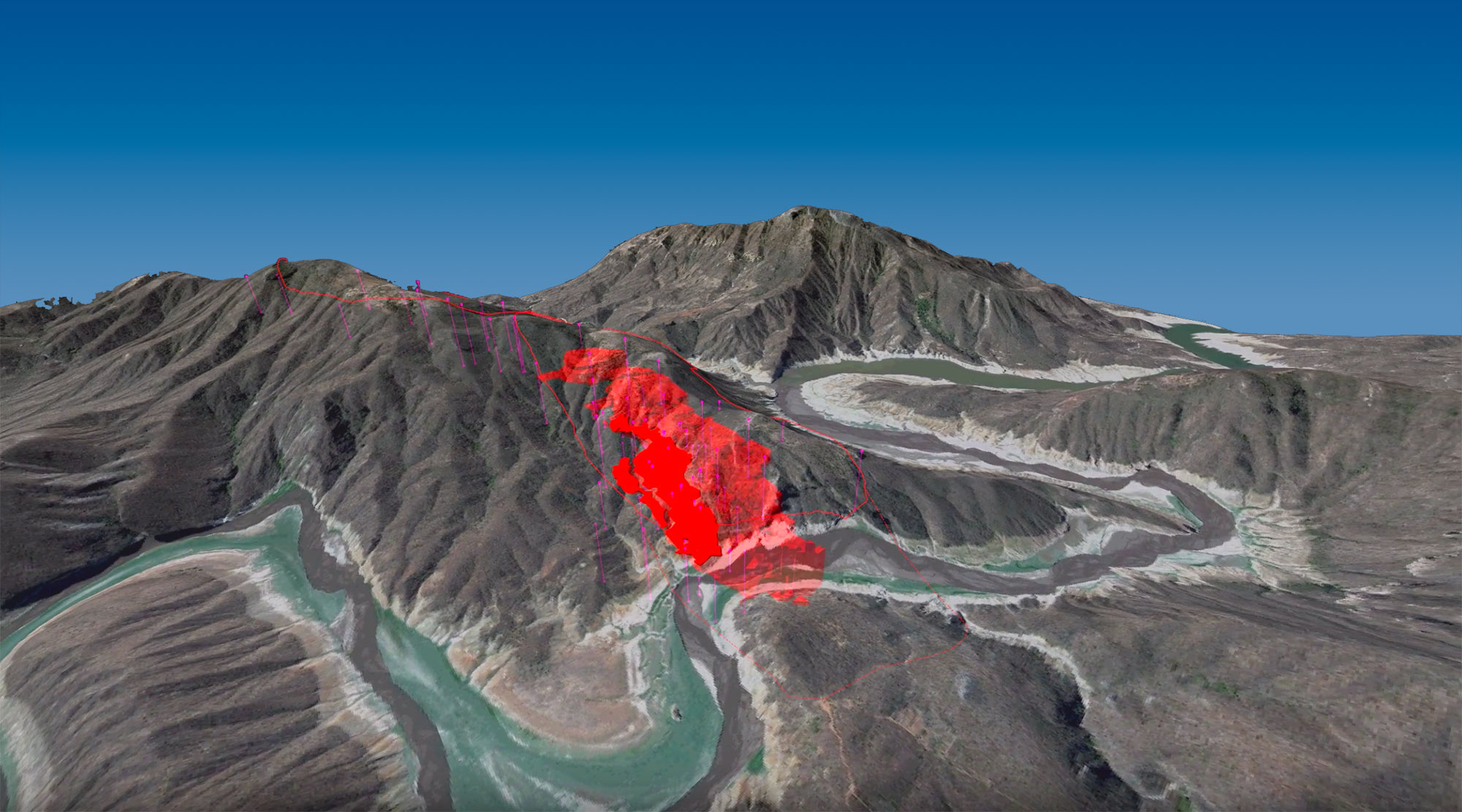

The preliminary results of the IP survey

The press release earlier this month only discussed the preliminary interpretation of the results of the IP survey that have already been received. As a reminder, Oroco has engaged a Saskatchewan-based company to complete an IP survey on 10 square kilometers of land, and that will take time. The company has received data from roughly 25% of the total area that will be the subject of the survey, and more results will be received over the next few weeks and months as the IP Survey has reached a 40% completion rate. Considering that the completion rate was reached since the start of the program in September, we hope the contractor will be able to finish the job before Christmas, but there are no guarantees during these difficult COVID-19 times.

So, back to the recently reported initial results, which focused on the South zone. All data is still being analyzed and interpreted, but there are some preliminary takeaways that could be very important for the company.

The survey was focusing on a 2,000 by 1,200 meter area of the South Zone and looking at the current size of the IP anomaly of 1,000 by 600 meters, the anomaly is sizeable. Very sizeable. Throw in the fact the IP survey has detected chargeability highs at depths up to 600 meters, we may be talking about some serious tonnage here.

Even if one would run the numbers based on 1,000 X 600 X 300 meters, we are talking about 470 million tonnes of rock (using an average density of 2.60). Expanding this to 1,000 X 800 X 450 meters (still way less than the depths of 600 meters mentioned in the press release), the tonnage of the IP anomaly on the South Zone is rapidly approaching 900-950 million tonnes. A massive target.

Don’t get us wrong. The numbers quoted above are just a conceptual tonnage based on the size of the anomaly. There’s absolutely no certainty every single tonne will contain copper values exceeding the economic cutoff grades, and there’s even less certainty every single tonne will end up in a mine plan – that’s just not going to happen. As such, the size of the anomaly mentioned in the Oroco press release should be taken at face value. It’s a humongous mass of rock and we will only know for sure what Santo Tomas’s South Zone is hosting once the assay results from the 2021 drill program are coming in. Until then, readers are cautioned to interpret the South Zone as hosting a historical resource defined by 4,223 meters of drilling in 14 holes (not all of which intersected mineralization) and current IP anomalies defining a target of a target with several hundreds of millions of tonnes of rock that may or may not be mineralized.

What does this mean for the size of the project?

This clearly is an intriguing start. Although the importance of an IP survey should not be exaggerated until we see the assay results, there are some important takeaways here.

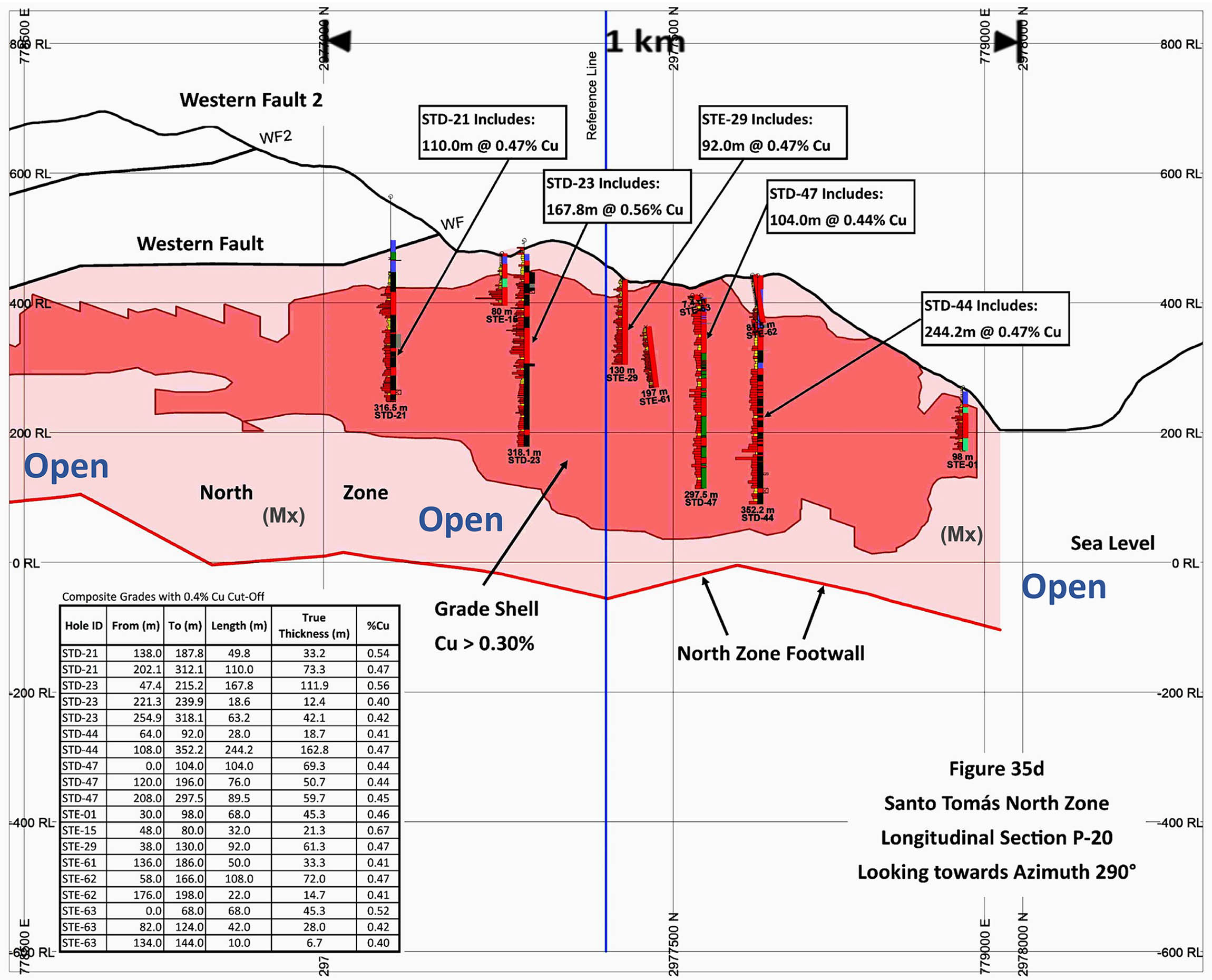

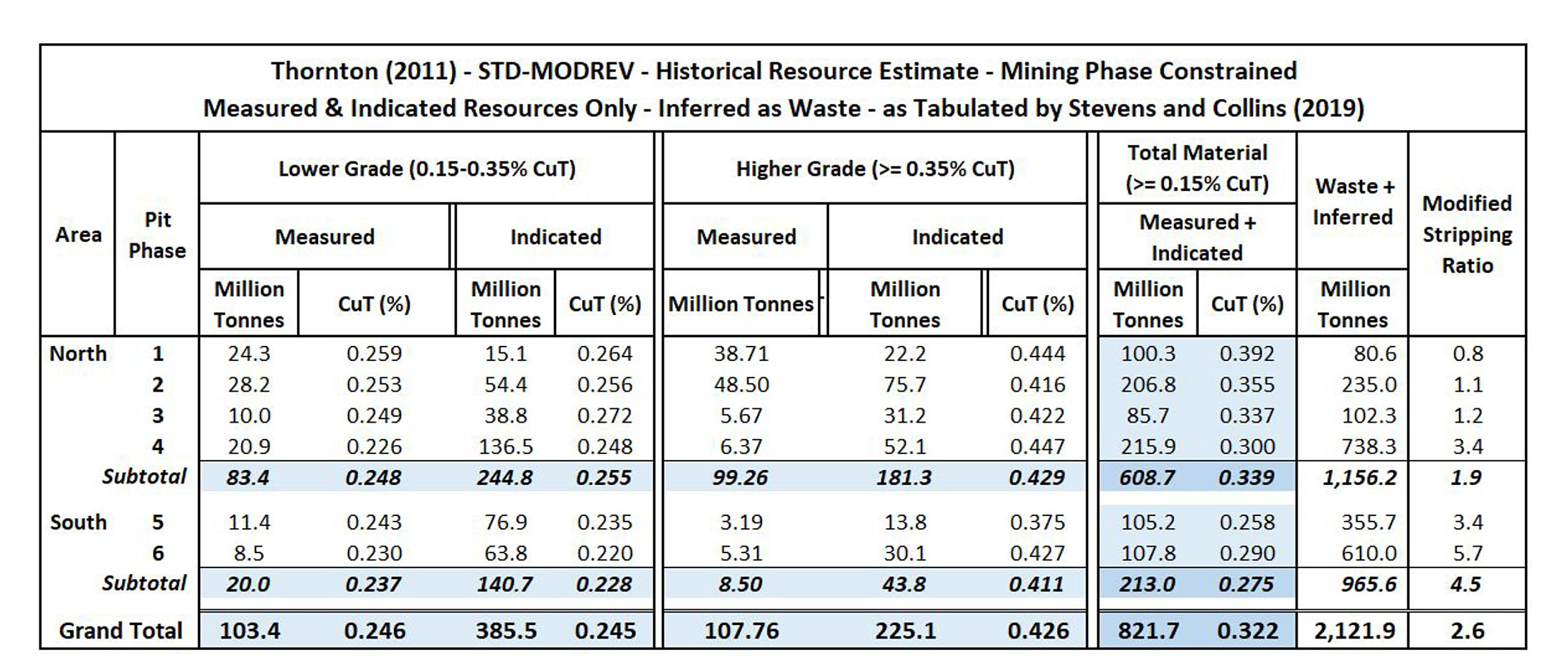

The South Zone accounted for 213 million of the 822 million tonnes of the entire measured and indicated resource at Santo Tomas while inferred resources were thrown on a pile with waste and represent an additional 966 million tonnes.

So in a way, the size of the anomaly, (even up to 920 million tonnes) isn’t surprising as the 2011 historical resource already ended up with 1.2 billion tonnes of rock of which some will be mineralized (either meeting or failing to meet cutoff grades) and some will be barren. So essentially, the IP survey validates the total size of the pit-constrained resource estimate (non-NI43 compliant), and drilling will figure out if the grade meets the cut.

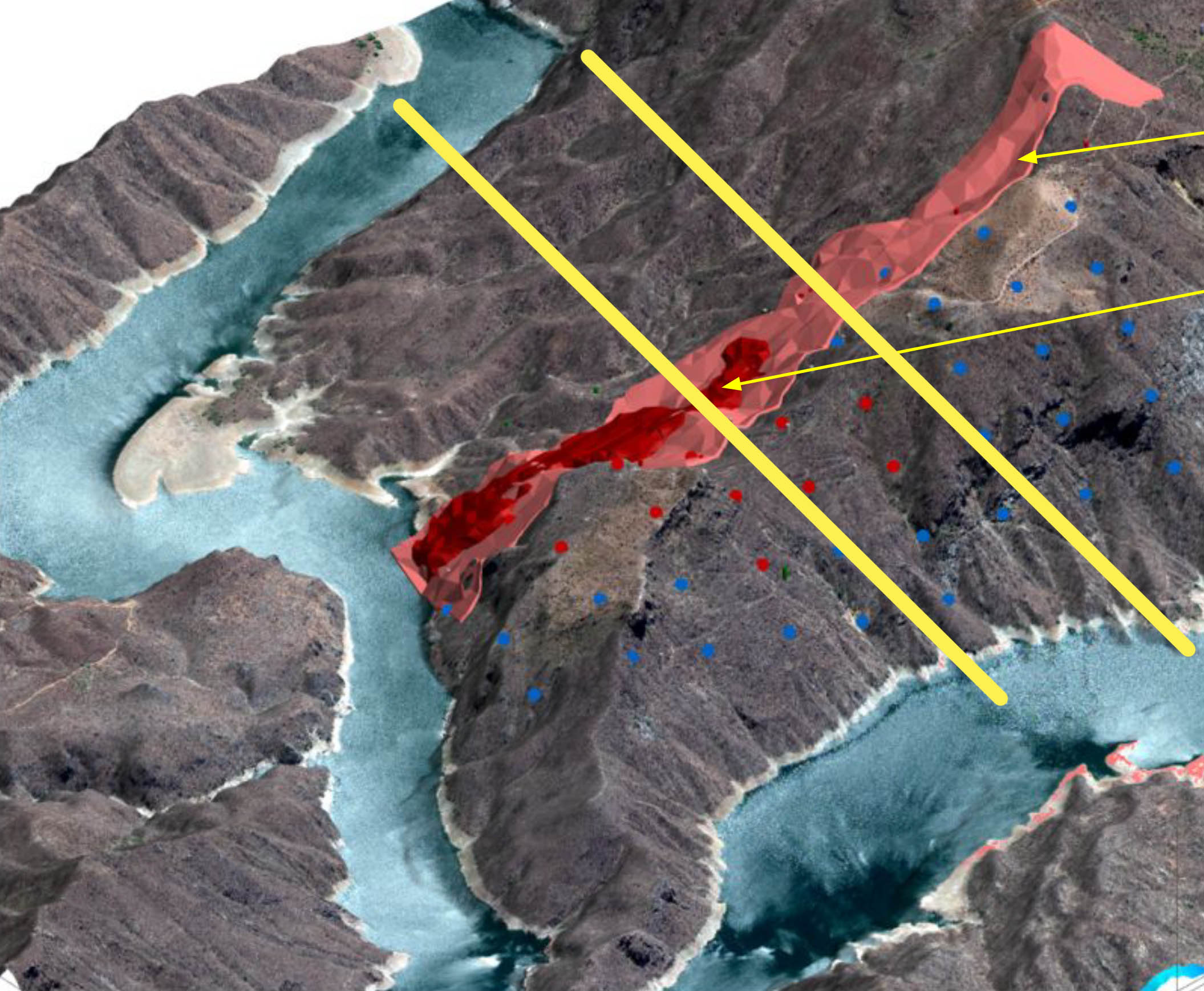

Secondly, we have not yet seen the IP data for the area between the North Zone and the South Zone – which is inferred to be barren (or only contains low copper values). While on the one hand, it would be interesting to have one large open giga-pit combining the North and South zones, there may be a silver lining here. Considering the mineralization appears to be continuing under the Fuerte river onto the Brasiles zone on the other side of the river, it’s not unlikely the river may have to be diverted for Oroco to bring more tonnes in the mine plan. Having a barren zone in between the North and South zone could mean that’s an ideal location for a tunnel to make the river ‘cut a corner’.

This would perhaps be the least drastic option to divert the river. Of course, this is just our own interpretation and clearly does not represent the company’s official point of view (let’s start with a compliant resource first, and a viable mine plan later on!).

The IP Survey is now focusing on the North Zone which contained in excess of 600 million tonnes in the measured and indicated categories of the historical resource estimate and subsequently, the company will cross the river and survey the Brasiles zone (where no exploration target or historical resource estimate has ever been compiled).

Oroco has C$8M in cash on the bank

As of the end of August (the most recent financials available), Oroco had a working capital position of approximately C$1.1M. Subsequent to the end of August, Oroco completed a substantial capital raise, issuing 12.1 million units at C$0.60 per unit to raise a total of just under C$7.3M. Additionally, Oroco also raised an additional C$950,000 through the exercise of 2.3 million warrants, and we estimate the company’s treasury to currently contain approximately C$9M in cash.

A strong position to be in, and we expect the warrants (which are all in the money right now) to continue to play an important role in Oroco’s plans to raise cash. There are approximately 3-3.5 million of the C$0.42 warrants outstanding which would bring in an additional C$1.2-1.5M in cash (these warrants have an acceleration clause and as far as we know, this acceleration has not been triggered by the company yet) while the 6.05 million warrants at C$0.90 issued as part of the September raise are also in the money and this could allow Oroco to see an additional cash inflow of in excess of C$5M.

However, a company should never fully rely on the warrant exercises, especially not when it wants to embark on a very substantial multiple-rig drill program in 2021. With a current market capitalization exceeding the C$250M and a share price trading more than twice as high as the C$0.60 level the previous raise was conducted at, Oroco Resource should be looking at additional possibilities to fill up its treasury. The C$8M it currently has in the treasury is a comfortable position to be in, but this would be an excellent time to add some dollars and pesos to the treasury in anticipation of a busy 2021.

Conclusion

The initial results of the first 25% of the IP survey that have been announced are interesting but we will obviously have to wait for the full dataset to fine-tune our expectations. The initial results seem to confirm the potential size of the South Zone and we hope to see a similar result for the North Zone. Brasiles will be the icing on the cake as that’s the area that offers additional resource potential on top of the historical resource estimate.

Of course, the proof will be in the (drill-) pudding. As Oroco is eyeing a multi-rig drill program in 2021 we expect the company to complete a drill program of several tens of thousands of meters. Not only will this put Oroco on track to put a NI 43-101 compliant resource together, but it will also go a long way to completing its C$30M earn-in into Santo Tomas.

Disclosure: The author has a long position but has recently sold some shares to exercise the C$0.42 warrants. Oroco is a sponsor of the website. Please read our terms & conditions.