Sierra Madre Gold and Silver (SM.V) is the newest Mexico-focused silver and gold exploration company on the TSX Venture Exchange. After closing an initial financing round in June 2020, the company didn’t waste any time and pursued an IPO financing late last year. Despite completing the IPO-related sub receipt financing in late October, Sierra Madre went through the lengthy process of TSX-V listing, but is now really off to the races.

This new company combines a proven team that pretty much put Prime Mining (PRYM.V) on the rails, with a Nayarit-based gold and silver project with a known resource and known metallurgy. With C$15M in cash in the bank, Sierra Madre Gold and Silver appears to be perfectly positioned to prove up the value of its flagship Tepic project and this year’s drilling activities should result in an updated resource estimate before the end of this year.

The project was gathering dust on a shelf but the current climate is ideal for Tepic

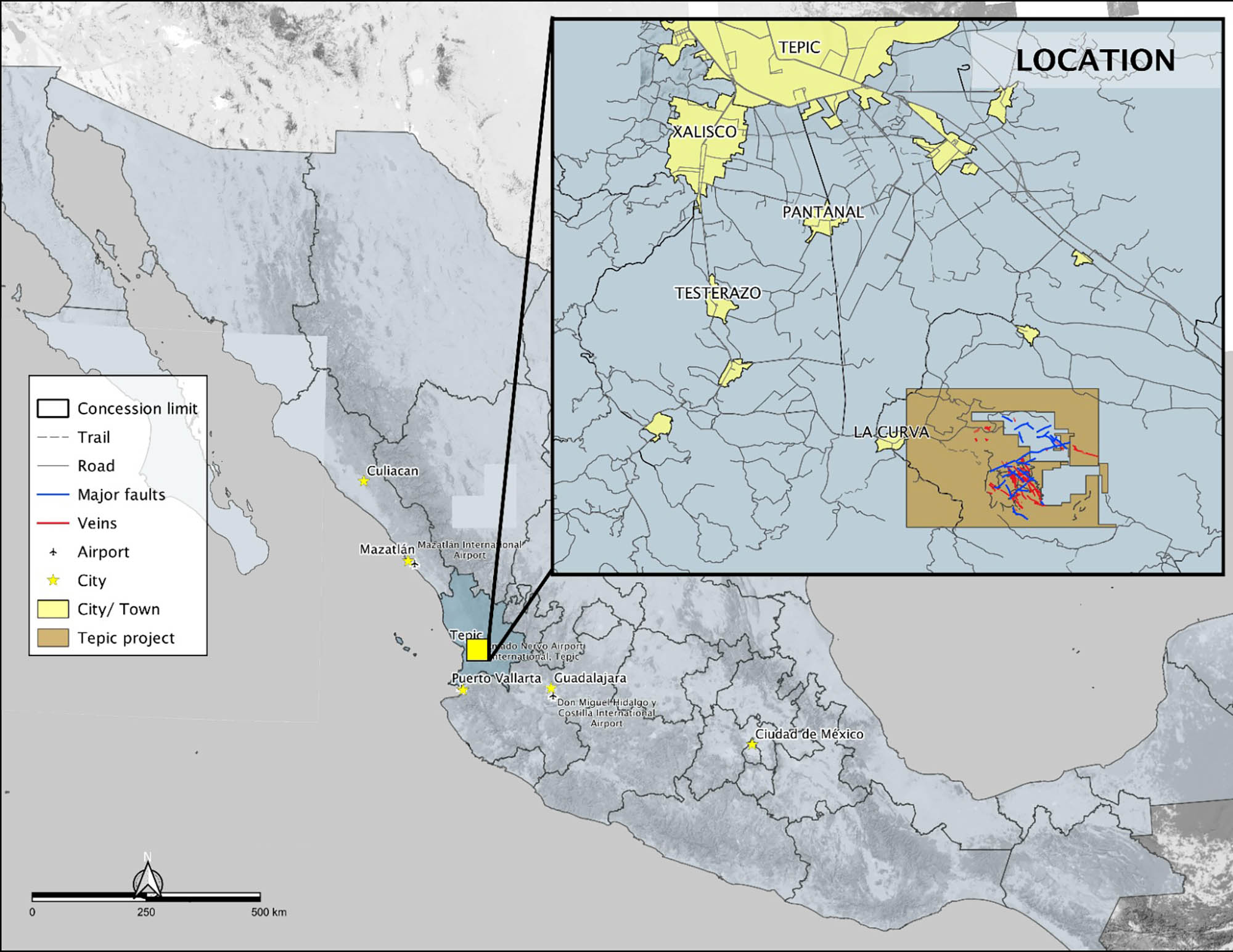

The flagship Tepic project is located in Nayarit, just about 30 kilometers south-southeast of the capital (which is also called Tepic). The close proximity to the state capital ensures excellent access to existing infrastructure: the project is just about 3 kilometers from paved roads while the Tepic airport offers services to Mexico City. Just a little bit further away (about 150 kilometers) is the Puerto Vallarta airport and as that airport serves the main tourist hub with regular connections to even European destinations (in a pre-COVID era, that is), it seems to be easy enough to get in and out of Nayarit.

The previous owner, Cream Minerals, completed in excess of 31,000 meters of drilling in 149 holes between 2002 and 2011, and the property has pretty much been ‘forgotten’ since the silver price moved away from its all-time highs around the $50 level. Cream Minerals had a market cap of over C$100M during these highs.

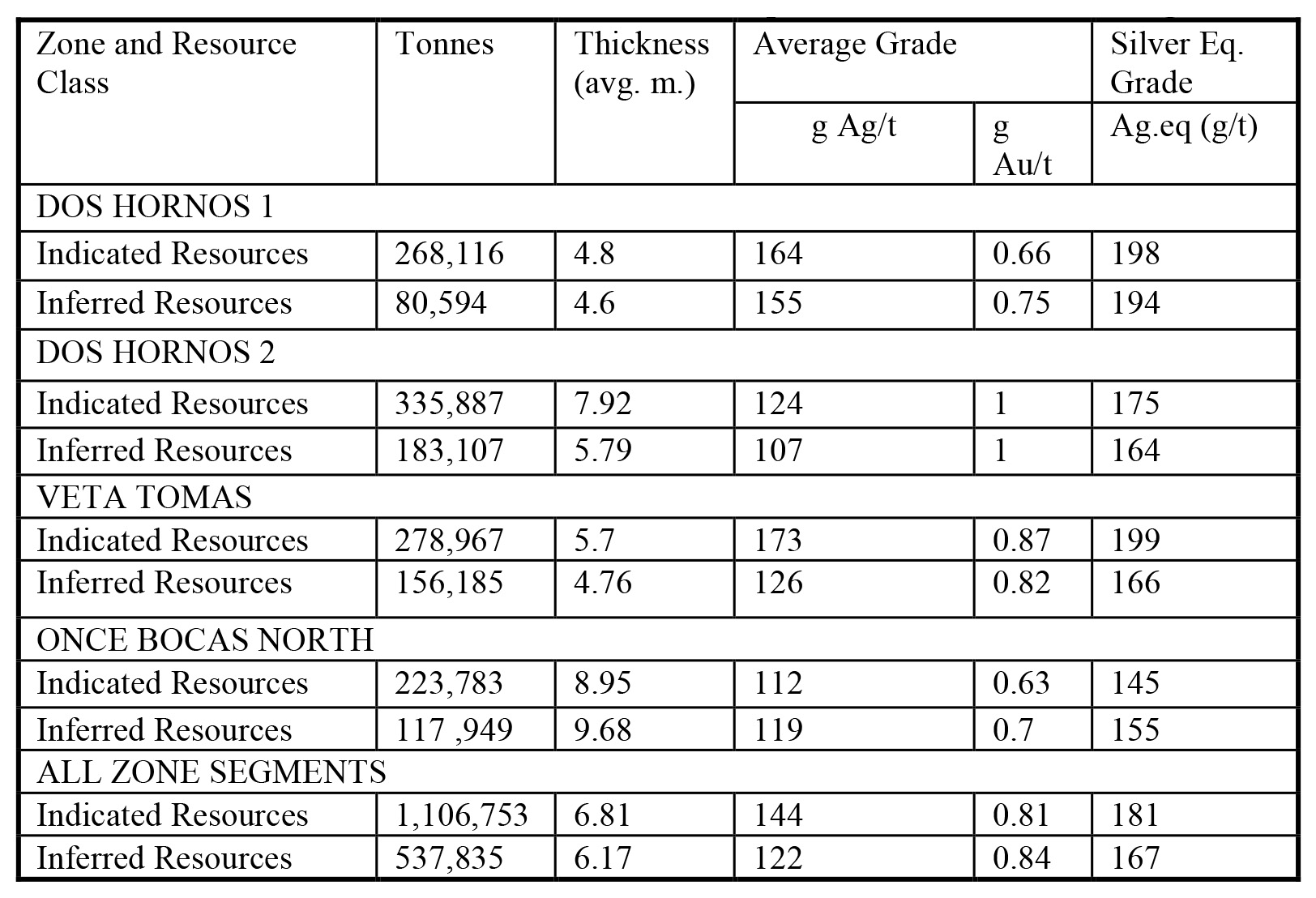

The numerous drill holes and abundance of available drill data helped the previous owners to report on several historical resource estimates but none of those estimates really delivered one ‘core’ resource estimate: as the silver price was very volatile back in the day, pretty much every calculation contained a version with a low cutoff grade and a version with a higher cutoff grade. Sierra Madre is using the most recent resource calculation (from 2013) which used a 75 g/t AgEq cutoff grade for all the mineralized zones on the Tepic project.

The indicated resources contain about 5.1 million ounces of silver at an average grade of 144 g/t, while the 538,000 tonnes in the inferred resource category are hosting an additional 2.1 million ounces of silver for a total of 7.2 million ounces of silver. Additionally, there are about 30,000 ounces of gold in the indicated resource category and about 15,000 ounces in the inferred resource category. On a silver-equivalent basis (using a 70:1 silver:gold ratio), the 2013 resource is hosting about 10.3 million ounces silver-equivalent.

A good start, and it should be clear this is just the beginning for Sierra Madre Gold & Silver. The company has plenty of cash to hit the ground running with an aggressive drill program which should increase the current resource and improve the confidence in both the resource as well as the metallurgical test results.

The ongoing exploration program should add a lot of value

Sierra Madre isn’t wasting any time and drilling has already started on the Tepic project. The company is fully permitted to drill 67 holes and in this first phase exploration program, a total of 21 holes will be completed. This drill program is currently in full swing and as we expect Sierra Madre to provide assay results in batches rather than reporting on every single hole coming in, we are expecting the first batch of drill results to be released in June.

The reason for drilling just 21 holes while the company is permitted for 67 holes is quite simple: the rainy season will start soon and it’s easier to just wrap up a first phase drill program, analyze the data and get back in the field after the rainy season rather than fighting nature forces. According to the Wikipedia page of the city of Tepic, about 80% of the annual rainfall actually falls in the months of July-September with an average rainfall of about 15 inches in July alone (in the 1951-2010 era). So while drilling is theoretically still possible, it likely wouldn’t be a very efficient drill program when you’re battling potentially torrential rains.

This means we will likely see the assay results of all 21 holes being released throughout the summer with the second batch of up to 46 holes to be drilled in Q3 2021. However, Sierra Madre also recently announced a 2,700 metre trenching program over multiple new discovery zones, which will operate during this rainy season and provide steady news flow.

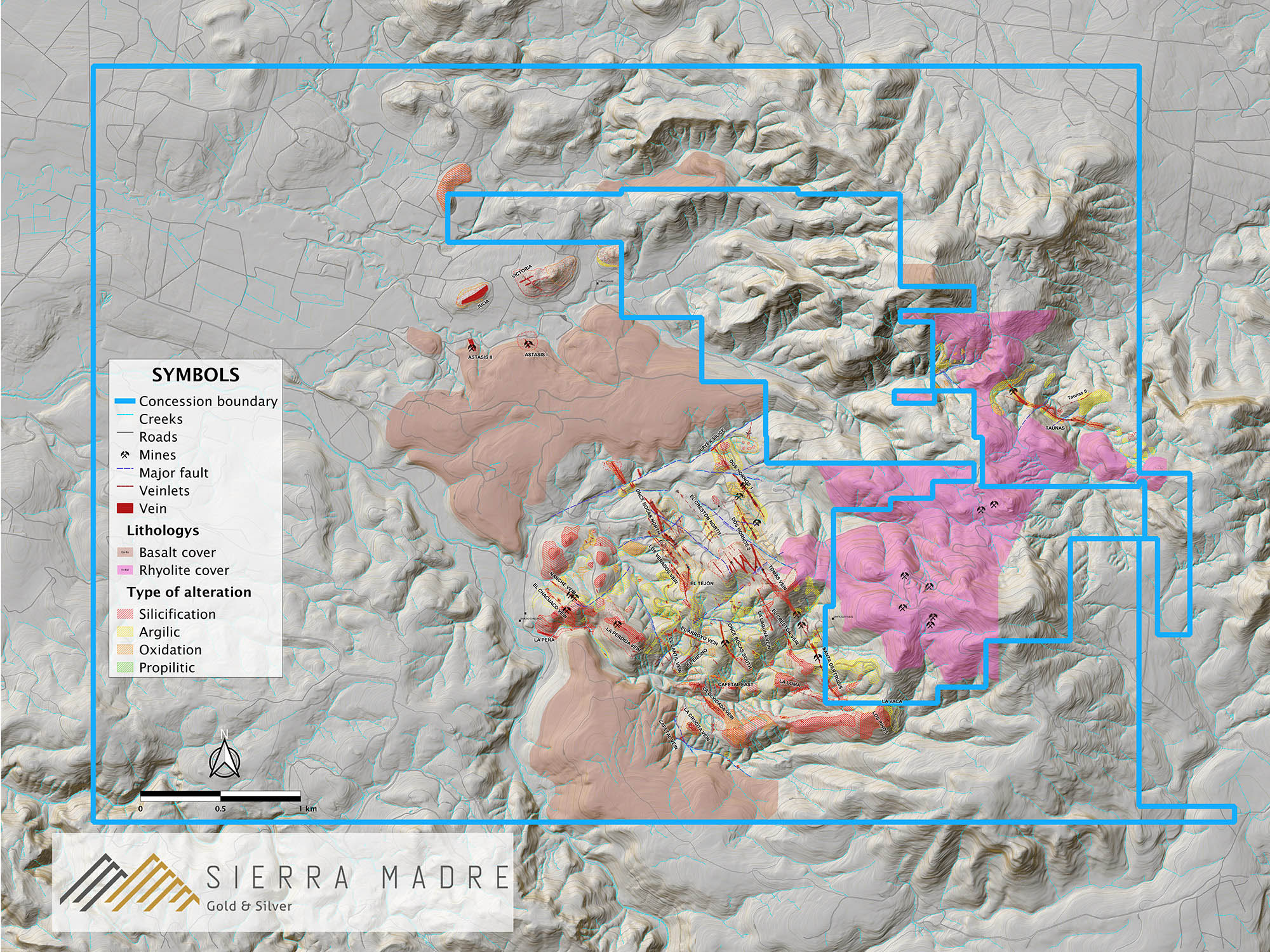

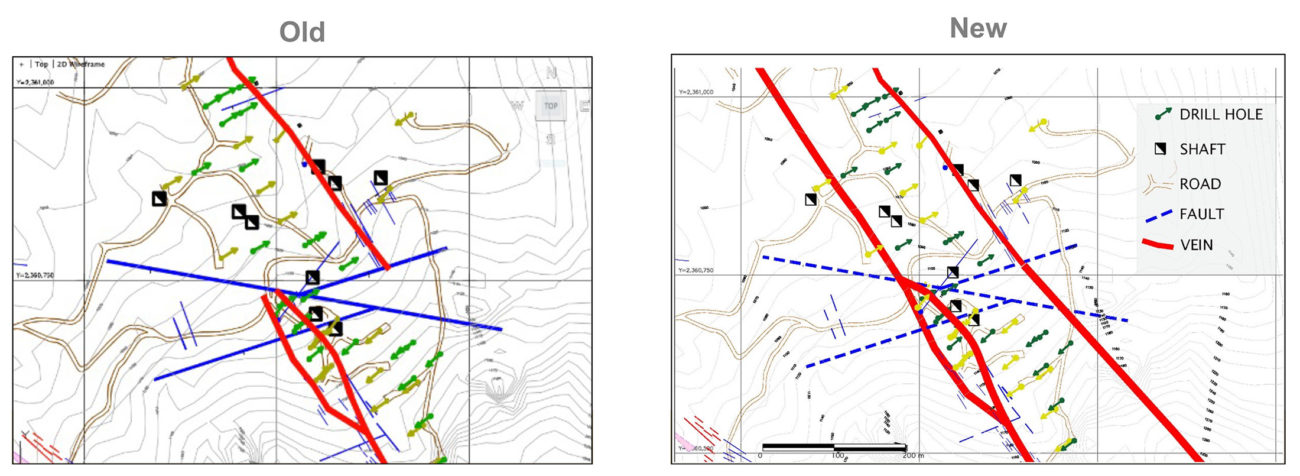

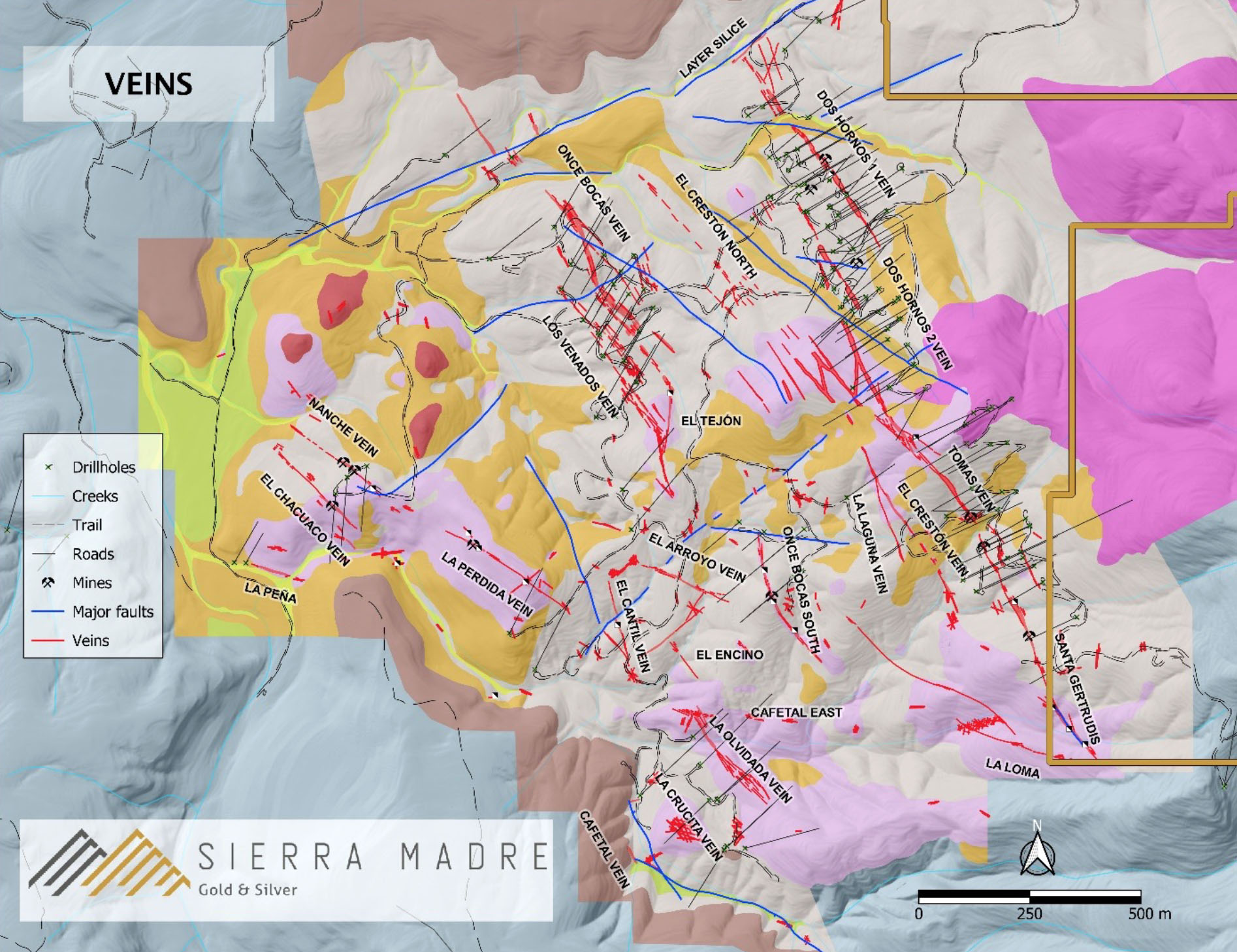

The phase 1 drill program will try to confirm the new exploration theory which is moving away from the historical interpretation of multiple faults which led the previous operators to think the Dos Hornos breccia veins were cut off. The image below shows the new structural interpretation of the mineralization which appears to be much more continuous than previous owners seemed to think.

The drill programs will consist of Reverse Circulation holes. Not only because this is substantially cheaper with an anticipated all-in cost of less than US$100/meter, but also because this will be a major help to figure out if the historical grades may have been underestimated due to the poor recovery of the drill core. While we obviously have to be cautious at this stage of the exploration program, there seem to be elements that make a 15-30% grade boost for the gold credit quite realistic. The potential underestimation of the silver grade will likely have a lower impact.

We will obviously have to wait for the assay results to come in and the company’s technical team to piece everything together, but if the average gold grade could for instance be boosted from 0.82 g/t to 1 g/t, the additional 0.18 g/t would boost the gross rock value per tonne by US$10 and add tens of millions of dollars to the top-line revenue (assuming the tonnage will increase from the 1.64 million tonnes in the historical resource estimate). Again, a grade bump in both the silver and gold levels is no certainty, but it’s definitely something we will be keeping an eye on as it could change the entire perception of the project.

The 67 hole drill program will work the project on two angles: resource expansion by rapidly adding tonnes to the existing historical resource estimate by reinterpreting the mineralized structures on the project, while the RC drill program should further increase the confidence level in the gold and silver grades.

Tripling the resource strike length potential could provide more low-hanging fruit

When Sierra Madre started their work program at Tepic, only a small portion of the project had been mapped. The historic resource sits in a close cluster of four vein structures; Dos Hornos 1 and 2, Tomas and Once Bocas North. The total strike length of these veins was 3.5km. OnceBocas South wasn’t included in the most recent resource estimate, but the previous resource, which was issued 6 months earlier, included this vein and increased the resource to 18.2 million ounces of silver equivalent.

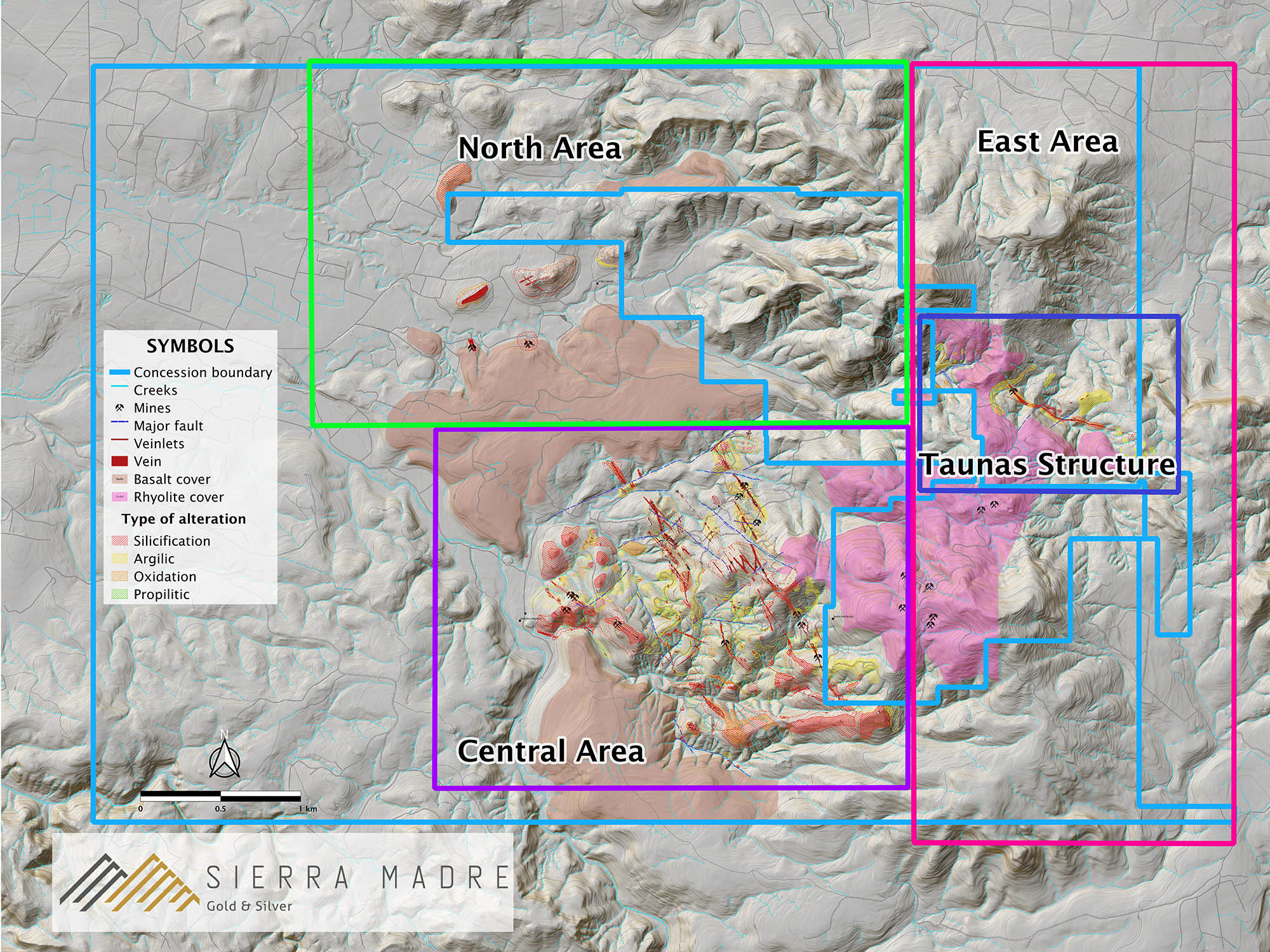

Fast forward to today and the strike length potential has more than tripled to over 11km. Most of the newly discovered veining is within the central area of the project, but 2 other highly prospective areas are now also ready for comprehensive work. The 2,700 metres of trenching will concentrate on these newly discovered veins and apparently this type of trenching can be included in a future resource estimate.

The acquisition terms are extremely favorable

Sierra Madre gold is able to acquire full ownership by making total payments of US$450,000 in cash to Cream Minerals. The structure of the cash payments is very favorable and the company already completed most payments while Sierra Madre still was a private company. The only remaining payments are US$50,000 in October and a final US$50,000 in April next year, and that’s it for the option terms.

By April 2022, the company will have to officially exercise the option which will trigger a final payment of US$1.5M or the grant of a 3% NSR which will be extinguished after making US$4M in royalty payments. Additionally, Sierra Madre could elect to issue the 3% NSR and gradually buy back the NSR at a rate of US$1M per 1%. So the choices are pretty straightforward: Sierra Madre either needs to pay US$1.5M in cash, or issue a 3% NSR which will ultimately cost the company US$3-4M but those amounts would only have to be settled further down the road.

With about C$14.6M (which is in excess of US$10M) in cash in the bank, we would expect Sierra Madre to elect the easiest way forward and simply pay the US$1.5M lump sump to earn an unencumbered full ownership of the project. It makes little sense to mess around with NSR’s that would have to be repurchased if you have the cash readily available. Obviously, a decision doesn’t have to be made right away and the final decision will be based on the updated resource estimate which should be published ahead of the decision date.

Sierra Madre is just a US$1.6M in cash payments away from acquiring full ownership of Tepic. The project is not subject to any other royalties. While the deal sounds suspiciously cheap, we need to remember when the agreement was signed: in December 2017, when silver was trading at just around $16/oz. This means the acquisition was quite well-timed and while the economics of the project may not be too impressive at $16 silver, the current silver price of in excess of $25/oz obviously changes everything.

The structure of the company is well thought out: the cheap stock is escrowed

While most companies have raised cash in different stages during the private life, the historical capital raises at Sierra Madre Gold & Silver were actually quite reasonably priced. The recent two financings were priced at C$0.15 in Q2 2020 (there was a C$0.10 round which was subsequently consolidated in a 3:2 share consolidation) while the much larger IPO capital raise was priced at C$0.50.

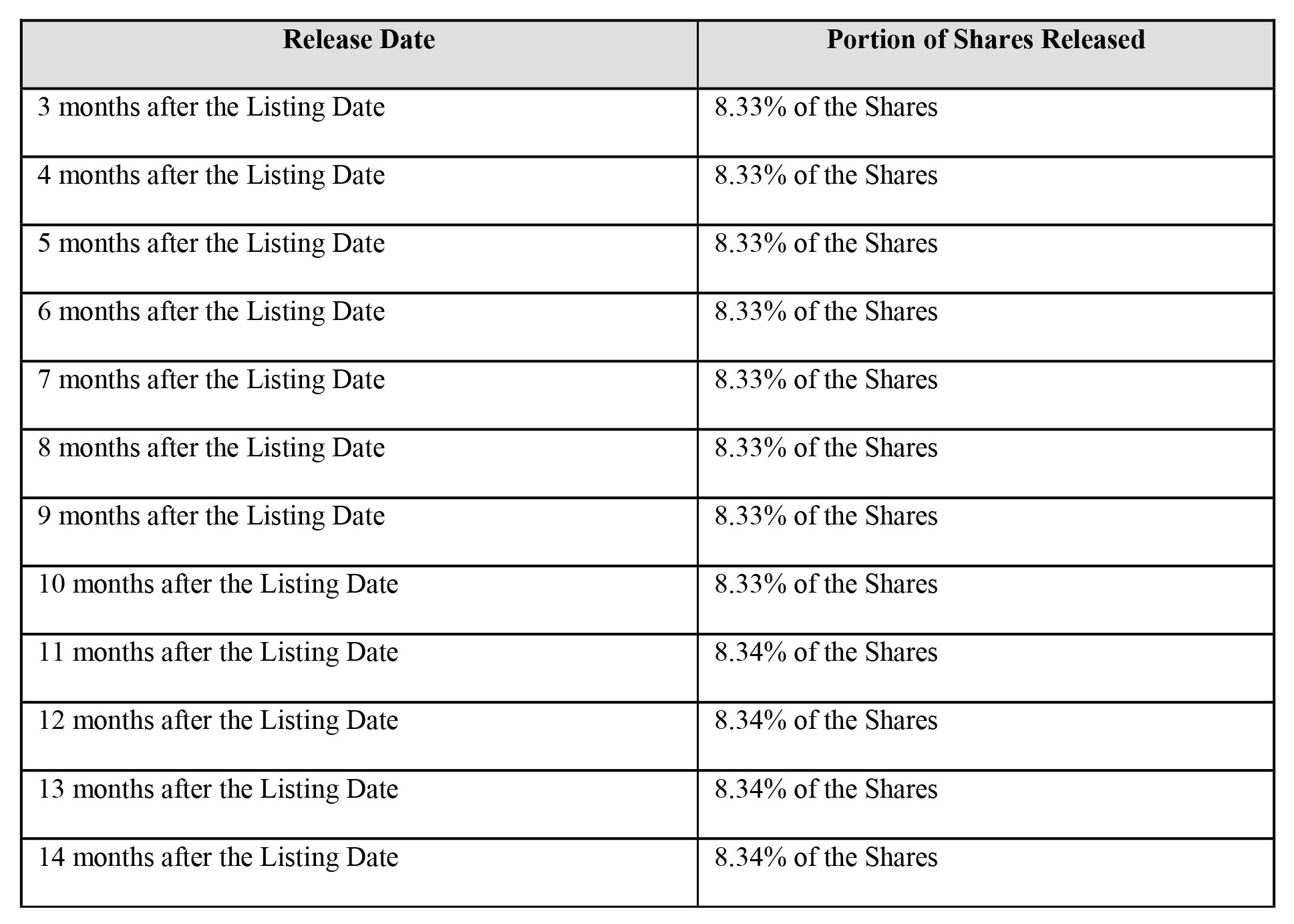

This means that about half of the shares outstanding have an average cost basis of C$0.50 and Sierra Madre did the right thing: investors who paid the most for their shares can trade them first. Right now, only the C$0.50 IPO financing is free tradeable (as well as a handful of shares that were part of the shell that was used for Sierra Madre). The C$0.15 round will only become tradeable in twelve tranches starting three months after the initial listing date.

That’s an excellent solution as this means there will be no cheap shares flooding the market. The first batch of C$0.15 stock will only come out of escrow on July 19th and there should be less than 1 million shares coming out of lock-up on a monthly basis so the market should be able to absorb most of the selling that could occur. Management and founders participated for approximately 50% of this financing and currently hold just over 40% of the total issued and outstanding shares.

An additional 11.5 million shares are part of a 42-month escrow schedule with the first batch of 10% (1.15M shares) coming out of lockup in October followed by six equal batches of 15% of the shares (approximately 1.72 million shares per batch) every six months thereafter. So the escrow conditions are quite well-organized: those who paid most for their stock can trade right away while participants in the C$0.15 round will have to be patient. And management has to be in for the long haul given the 3.5-year escrow release schedule for their shares.

Thanks to a well-timed raise fully capturing the renewed interest in the silver space, Sierra Madre Gold and Silver is in excellent financial shape. As of the end of Q1, the company had a working capital position of approximately C$14.6M which should be more than sufficient to complete this year’s drill program as well as making the final payments to acquire full ownership of the Tepic project.

The team: a few well-known names

Some of the members of the management team (and board) will sound quite familiar as they were recently involved with Millennial Lithium (ML.V), Prime Mining (PRYM.V), Reyna Silver (RSLV.V) while Greg Smith as VP of Exploration has been a member of the Calibre Mining (CXB.TO) team for as long as we can remember.

Greg Liller – Executive Chairman & COO

Mr. Liller has more than 40 years experience in exploration and mine development. Bachelor of Geology from Western State College in 1977. He has served as an officer or director of public companies listed on TSX Venture Exchange, the TSX main board, and the American Stock Exchange including Prime Mining (TSXV), Genco Resources (TSX), Gammon Gold (TSX, AMEX), Mexgold Resources (TSXV) and, Oracle Mining (TSX). Over the course of his career he has played a key role in the discovery and development of more than 11Moz Au and 600M oz Ag combined reserves and resources and securing over $300 million dollars in equity financings and $100 million dollars in debt financing.

Alex Langer – CEO, President & Director

Mr. Langer is a successful public markets specialist with over 15 years of experience. He started his career as an Investment Advisor with Canaccord Genuity, where he helped fund over 100 private and publicly listed companies including the IPOs for Endeavour Silver, Fortuna Silver, and Great Panther. Most recently he was Co-Founder and Vice President of Prime Mining (TSXV) and Millennial Lithium (TSXV) where he handled Capital Markets for both companies. He is a founding Director of Reyna Silver Corp. (TSXV)

Greg Smith – Director & Vice President of Exploration

Mr. Smith is an exploration geologist with more than 30 years of experience. He has worked as a consultant and for both junior and senior mining companies in various parts of the world including; North, Central and South America, Europe, and Africa. He brings a broad range of experience from the evaluation of grass roots properties to supervision of advanced programs including resource and reserve estimation, oversight of geological and technical activities for active underground and open pit mining operations including grade control, QA/QC programs and NI43-101 compliance. Mr. Smith was CEO, then VP Exploration of Calibre Mining helping guide the company through the acquisition of El Limon and La Libertad gold mines in Nicaragua.

Jorge Ramiro Monroy – Lead Director

Founder and Managing Director of Emerging Markets, a mining focused investment company based in Hong Kong and which has participated in the financing of numerous TSX Junior and Mid-tier exploration and mining companies. He is Founder and CEO of Reyna Silver Corp. (TSXV) and a former director of Prime Mining Corp. (TSXV) Mr. Ramiro holds a Bachelor’s degree from the State University of New York, an MBA in Finance from the Hong Kong University of Science and Technology.

Conclusion

Sierra Madre Gold and Silver has all the ingredients to be an exciting exploration story this year. It has a historical resource which provides an excellent starting point and the 67 permitted drill holes should be sufficient to confirm and increase that historical resource estimate. While that historical estimate of just 10.6 million ounces silver-equivalent seems to be pretty uninspiring, Sierra Madre has an excellent chance of rapidly expanding the historical resource as it’s using a new interpretation of the mineralized system as a blueprint for its exploration program while the more efficient RC drill program could provide a small grade boost.

The proof of the pudding is in the eating and in Sierra Madre’s case, we’ll know where we stand in less than a year as the updated resource estimate is expected by the end of this year (but could be pushed to Q1 depending on how fast drilling goes). We are charmed by the fact the company has mine builders in its team and if a viable resource could be established, we expect this team to actually try to develop and build a mining operation rather than sitting on their hands and hoping someone else will come along and buy the company.

Sierra Madre Gold and Silver is trading 80% above its C$0.50 IPO price but even at the current market capitalization of less than C$60M there could be plenty of upside potential if the resource can be expanded and if a realistic development scenario can be developed. Meanwhile, the company is trying to implement a ‘hub and spoke’ model and we expect Sierra Madre to try to acquire similar projects that could be satellite deposits and provide mill feed to one centralized processing facility.

With C$14.6M in cash in the bank, Sierra Madre has enough firepower to rapidly drill Tepic in an attempt to establish a viable silver-gold resource.

Disclosure: The author has a long position in Sierra Madre Gold & Silver. Sierra Madre will become a sponsor of the website. Please read our disclaimer.