The uranium equities have been exceptionally strong lately and it looks like the market is already positioning itself for a renewed interest in the uranium space. The spot price and contract price aren’t really moving just yet, but seeing the speculative cash inflow in the uranium exploration and production companies could be a good first step.

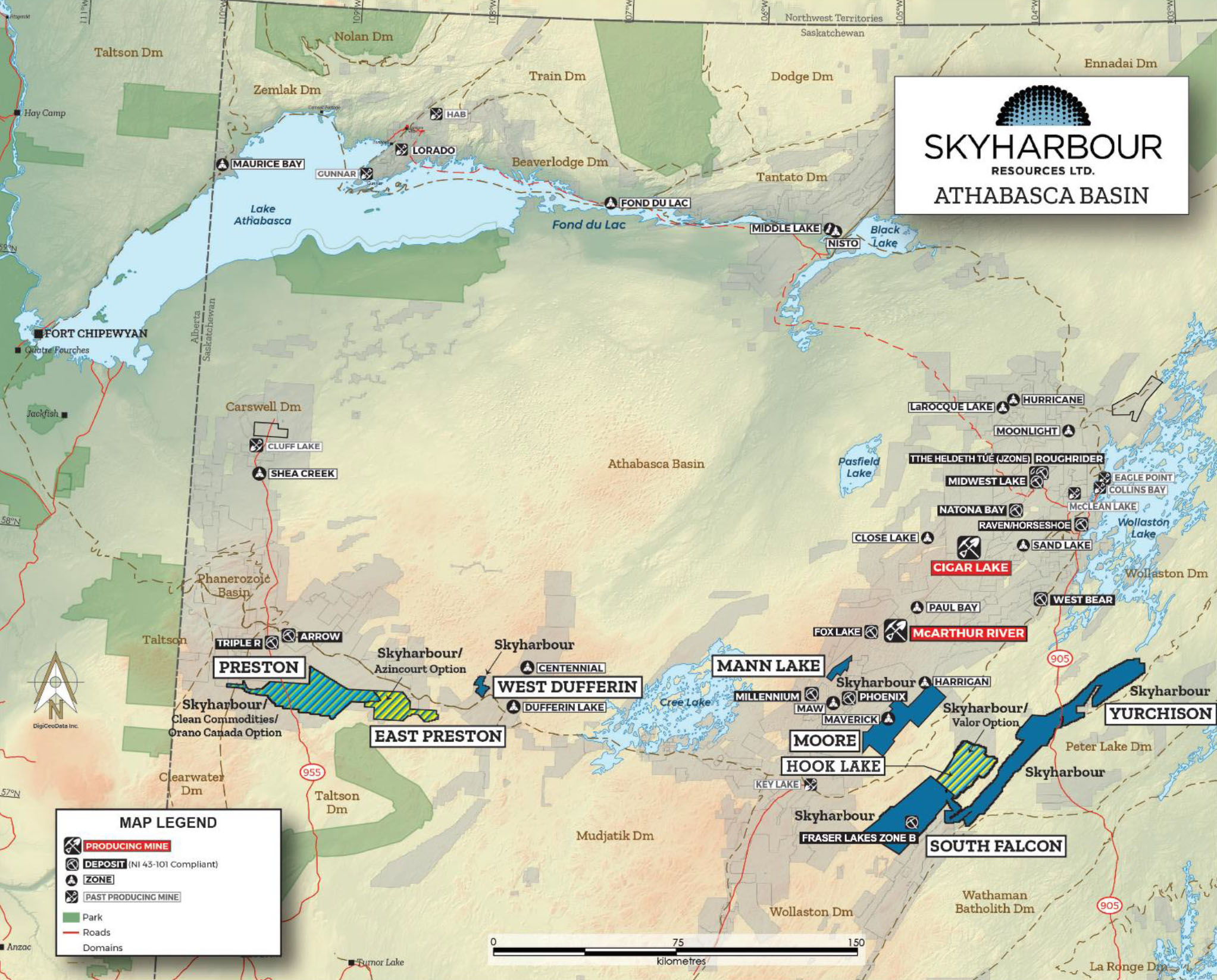

Skyharbour Resources (SYH.V) has a two-pronged approach. On the one hand it’s exploring its fully owned Moore uranium project where it hopes to have a resource calculation out by the end of this year or early next year, on the other hand its prospect and project generator model is bearing fruit as the company has several active joint ventures where other companies are spending their money to earn a majority stake in those projects.

We sat down with CEO Jordan Trimble, not just to discuss Skyharbour and its asset portfolio, but also the uranium market in general.

Sitting down with Jordan Trimble

The Projects

Your flagship project obviously still is the Moore project in Saskatchewan’s Athabasca Basin. You recently announced you were gearing up for a 3,500m drill program, do you have any update on the drill program? Your joint venture partner Azincourt Energy had to abort its East Preston drill program due to warm weather, will this be an issue for you too? When can we expect assays?

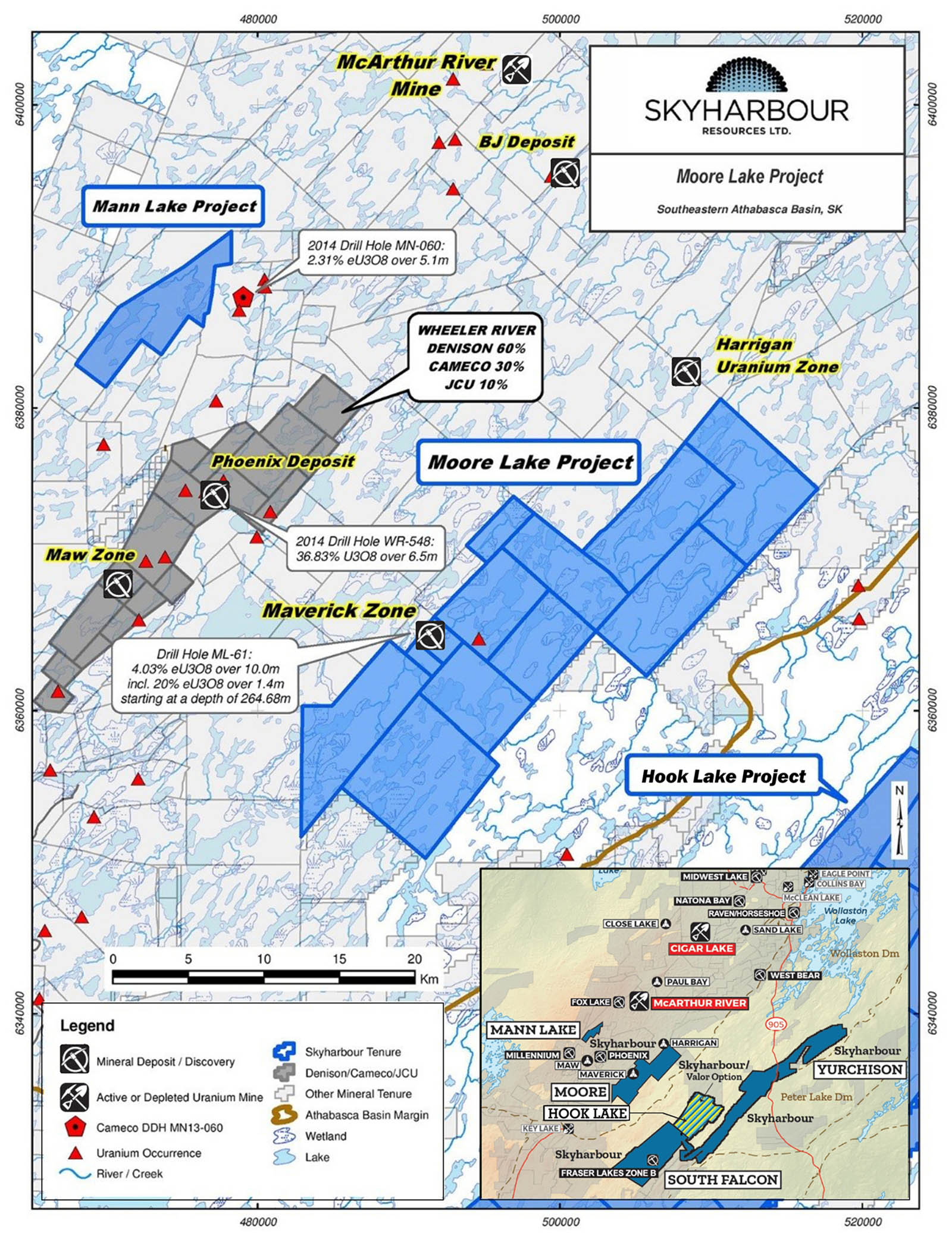

Yes, we recently announced mobilization for an upcoming drill program at our 35,705-hectare flagship Moore uranium project located approximately 15 kilometres east of Denison Mine’s (DNN.TO, DML) Wheeler River project and near regional infrastructure on the southeast side of the Athabasca Basin, Saskatchewan. Winter exploration programs in the Basin were cut short due to the weather but this will not be an issue for us with this program as we can drill right through the summer and early fall. This program will be commencing shortly, and assay results will likely start coming out in July. We are fully funded, with over C$9 million in cash and equity holdings, for an increased program as well. So if we like what we are seeing, we will likely expand the program providing news flow right into the fall.

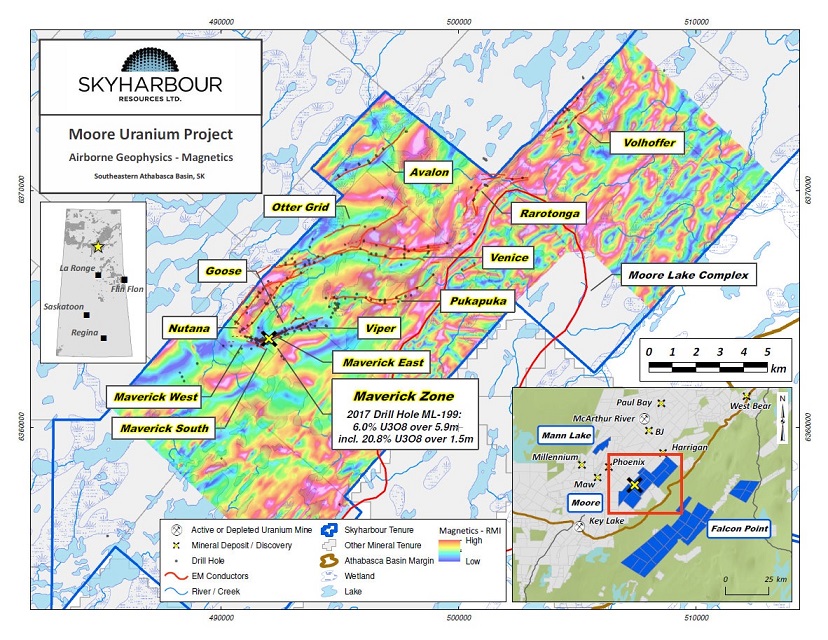

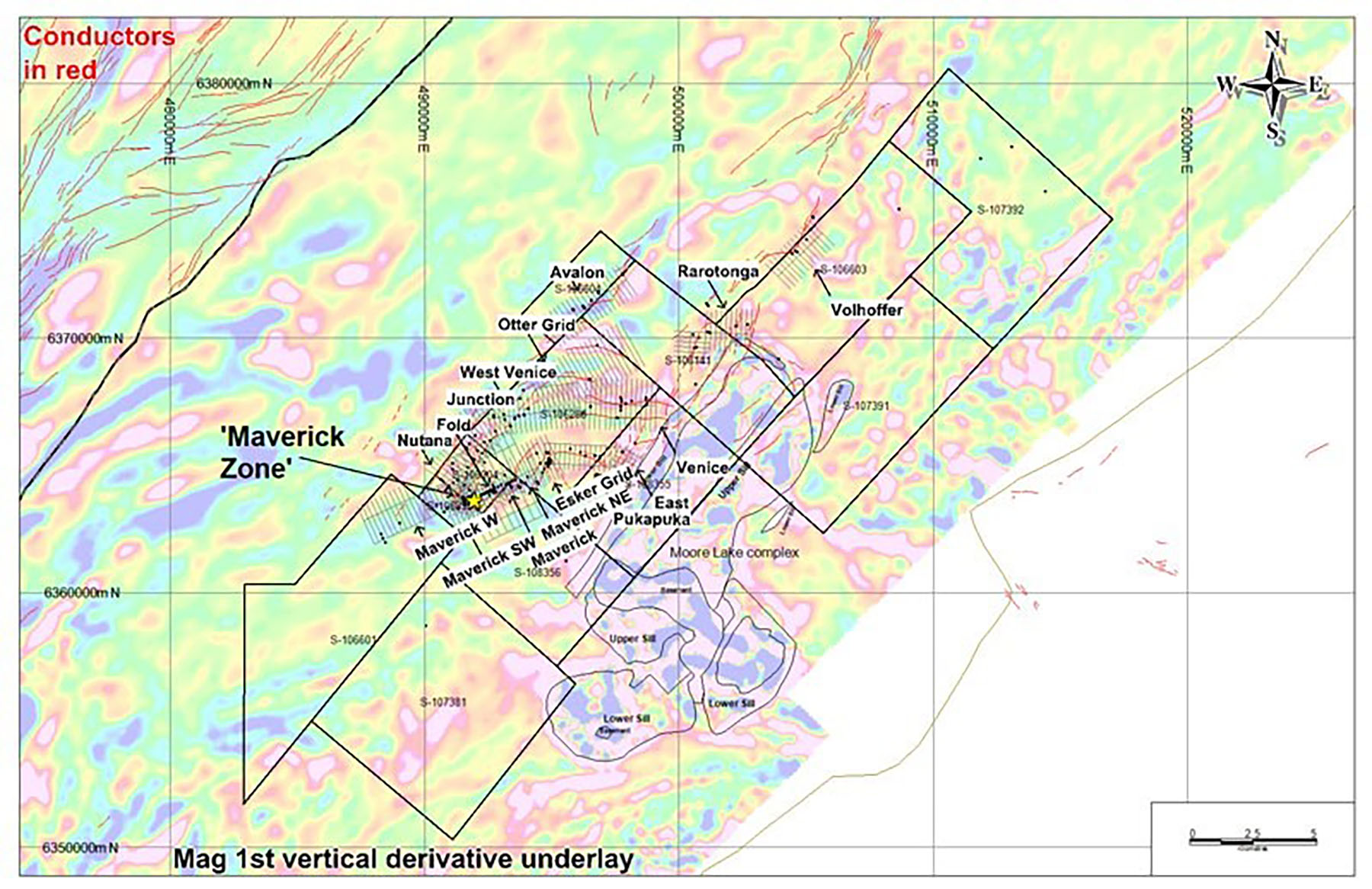

We have recently completed a 9 km Small Moving Loop EM (SML-EM) geophysical program to refine additional drill targets for this minimum 3,500 metre diamond drilling program consisting of at least 7-8 drill holes. They will focus on following-up on existing unconformity and basement-hosted targets along the high grade Maverick structural corridor as well as newly defined targets at the Grid Nineteen area.

At Moore, your drilling will be focusing on both the structural corridor as well as on the Grid Nineteen area. Regarding the structural corridor, is it fair to assume this will be the last drill program to drill-test for targets as it looks like the majority of your drilling will be concentrated on virgin ground and subsequent drill programs will be focusing on known occurrences?

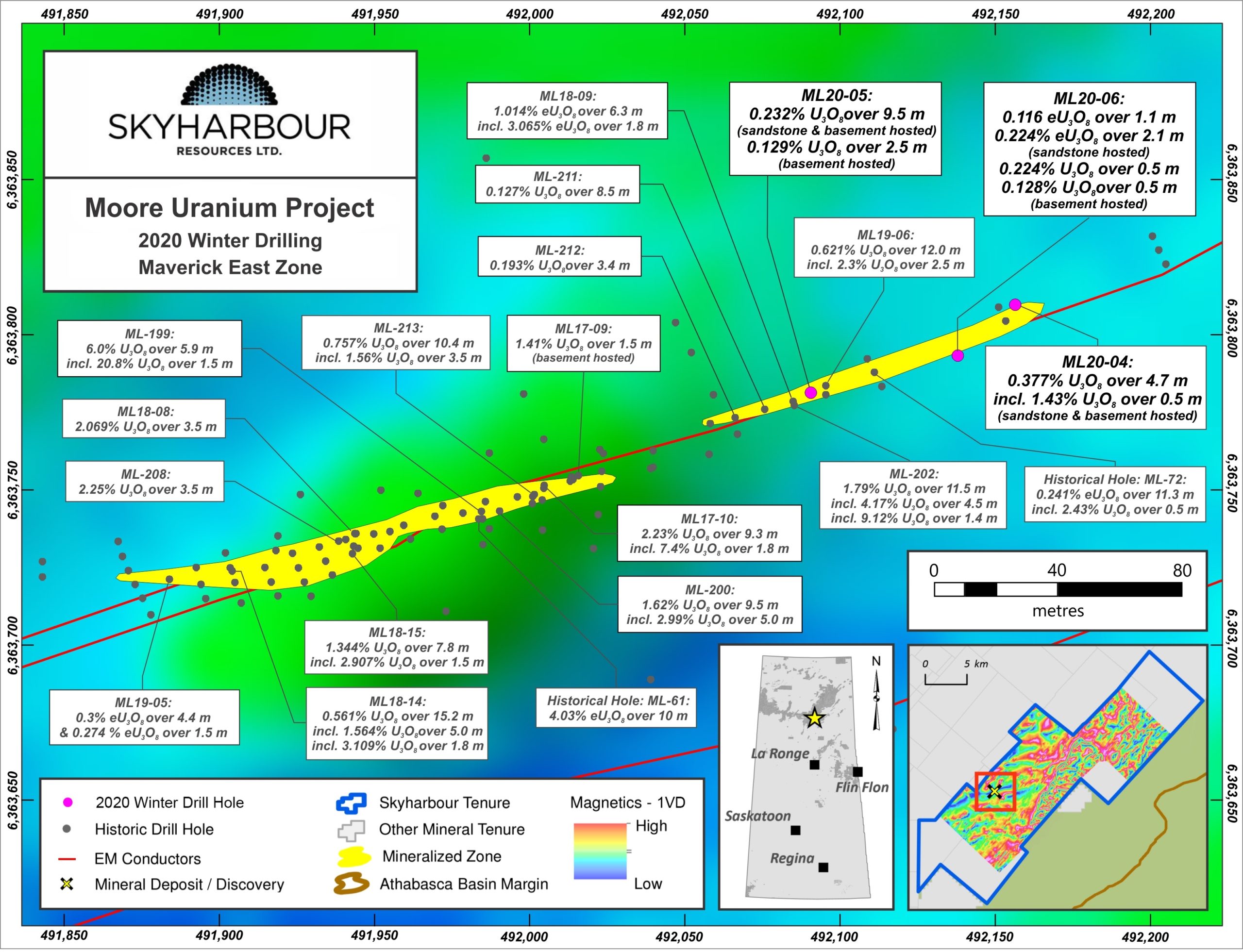

The drilling will focus on both unconformity and basement-hosted targets along the Maverick structural corridor and new targets identified elsewhere on the project including the Grid Nineteen area. We specifically plan to expand the high grade mineralization discovered recently at the Maverick East Zone, along strike, down-plunge and at depth with a focus on both unconformity- and basement-hosted mineralization. The high grade Maverick East Zone has been identified over a minimum of 170 metres strike length.

It is currently a minimum of 10 metres wide, open down dip and is up to 17.9 metres thick with grades of up to 9.12% U3O8 (with a minimum grade of 0.1% U3O8). The mineralization is accompanied by intense clay alteration and geochemical enrichment of pathfinder elements such as B, Ni and Cu, with the localized high grade uranium mineralization extending from the unconformity into the basement rocks. The mineralized zone appears to plunge moderately to the northeast, with minimal drill testing at depth along plunge.

In the eastern extent of the Maverick East Zone, copper values of up to 2.3% Cu along with up to 0.076% U3O8 were obtained from graphitic, clay-rich fractures within a broader zone of uranium-enriched and clay-altered granitic pegmatite and granite nearly 100 metres below the unconformity. This may be an important vector for additional basement-hosted mineralization.

Some of the most significant drill hole intersections in the Maverick East Zone include ML-202, which returned 1.79% U3O8 over 11.5 metres, including 4.17% U3O8 over 4.5 metres and 9.12% U3O8 over 1.4 metres, as well as recently announced hole ML20-09, which returned 0.72% U3O8 over 17.5 metres from 271.5 metres to 289.0 metres, including 1.00% U3O8 over a 10.0 metre interval in the basement portion of the interval (279.0 metres to 289.0 metres).

This 17.5 metre zone of mineralization is hosted in the basement rocks and represents the longest continuous width of uranium mineralization discovered at the project to date. The focus for future drilling in this area will be on the down-dip, along strike and down-plunge extensions of the Maverick East target.

Other targets along the 4.7 km long Maverick structural corridor will also be investigated, including the Esker Target, again with a focus on both unconformity- and basement-hosted mineralization. Only 2.5 km of the Maverick corridor has been systematically drilled and most of this drilling was only testing sandstone and unconformity targets leaving strong discovery potential on the remaining 2.2 km and at depth in the basement rocks.

We will continue to drill test the Maverick Corridor in future programs as significant portions of the trend have only been tested by a series of broadly spaced drill holes and fences with significant untested gaps. It is a very fertile corridor as most historical drill holes along this conductive corridor have exhibited extensive sandstone and basement alteration as well as geochemical enrichment similar to that found within the known high-grade Main Maverick and Maverick East zones where grades as high as 21% U3O8 have been discovered in drilling. Narrow intercepts of uranium mineralization have been identified in numerous locations along the relatively untested 2.2 km portion of the Maverick corridor. Many of these mineralized intercepts occur at the unconformity, but in a few key areas significant strongly altered basement structures within prospective graphitic and metasedimentary units are the host for this mineralization with only limited drilling of the basement rocks at depth that warrants further drilling.

There are a dozen other high-priority regional targets on the project that have uranium showings and mineralization in historical exploratory drill holes. In this program, we will be focusing about 2/3 of the metreage at the Maverick Corridor wit the other 1/3 allocated to test a new regional target known as Grid Nineteen.

Could you elaborate a bit on how Grid Nineteen was identified and what your initial plans are here?

A review of historical airborne EM identified several conductive features in an area located between the East Venice and Raratonga conductor systems that warranted follow-up groundwork. This target is about 11 km NE of the Main Maverick Zone. The airborne conductors lie in a structurally complex area that bridges a break in the east trending East Venice conductive system and the north trending Raratonga conductors. A total of 9 line km of survey was completed utilizing 200 metre loops in a moving array.

The preliminary results from the geophysical survey further refined the historical airborne conductors in the Grid Nineteen area and confirmed the extension of the Raratonga conductive system to the south. The survey further defined the abrupt change in the strike of the conductive systems at the southern end of the Grid Nineteen area, from an almost north-south orientation of the Raratonga conductors to the east-west orientation of the East Venice conductors. Weak basement-hosted mineralization was intersected in hole ML17-04 (1.0 m of 0.094% U3O8 at 235.0 metres depth) just to the west of this strike change, along with strong structural disruption and local pathfinder element enrichment in the sandstone of both ML17-04 and follow-up hole ML18-01. The intersection of these conductive systems forms one of several newly developed targets in the Grid Nineteen area.

The Grid Nineteen area has only seen limited historical drill testing consisting of two holes, one of which ended in sandstone and failed to test the main conductor target, thus there remains significant discovery potential in this area. Several drill targets have been developed based on the preliminary results of the ground geophysical survey, with plans to drill the most accessible targets during the upcoming drilling program.

At what point will you feel sufficiently confident to work towards a maiden resource estimate on Moore?

We are currently working towards a maiden resource estimate at Moore and expect to have one out later this year or early in 2022 after we complete several drill programs in 2021. It is an advanced stage uranium exploration property, and we believe there is potential for a much larger basement-hosted uranium deposit in the underlying feeder zones to the Maverick Corridor.

We also believe we can discover more high-grade lenses or pods at the unconformity and in the sandstone, much like what we see currently at the Main Maverick Zone. Finding more of these pods in a specific geological setting is intriguing given the potential use of ISR and SABRE to mine these types of deposits in the Basin. The property has been the subject of extensive historical exploration with over $45 million in expenditures, and over 150,000 metres of diamond drilling completed in over 390 drill holes throughout the property.

Can you provide an update on your partner funded programs and projects?

As a part of our prospect generator business, we now have three partner companies in Orano, Azincourt Energy (AAZ.V) and Valor Resources (VAL.AX) actively exploring our Preston, East Preston, and Hook Lake projects, respectively. Orano recently completed the requirements to earn a 51% stake in the Preston Uranium project after having spent approx. $5 million in exploration and cash payments. Orano is a strategic partner and industry leader in the uranium mining and nuclear industry so officially having them as a JV partner is a positive development for the company.

At the East Preston Project, Azincourt has recently completed their 70% earn in of the project while we retain a minority interest in the property going forward. They completed the earn in through $3.5 million in project consideration ($2.5 million in exploration and $1 million in cash), as well as issuing shares to us. As noted earlier, their winter drill program was truncated due to warm weather conditions, but they were able to complete 1,195m in 5 holes with assays still pending. They are well funded to complete additional programs at the project through the remainder of the year.

Lastly, we have signed a Definitive Agreement with ASX-listed Valor Resources on the Hook Lake (previously North Falcon Point) Uranium Project whereby Valor can earn-in 80% of the project through $3,500,000 in total exploration expenditures, $475,000 in total cash payments over three years and an initial share issuance of 233,333,333 shares of Valor. They are now carrying out a low-level airborne magnetic and VLF-EM survey to cover the entire Hook Lake claim area, using a fixed-wing aircraft, at 75m line-spacing totaling 5,100 line-km. Based on the results of the Phase I airborne survey and a review of the historical data, Valor expects to implement a Phase II groundwork program in June/July 2021. Details of this work will be the subject of forthcoming announcements but is likely to include further ground geophysics as well as geochemical surveys, geological mapping and surface prospecting designed to delineate drill targets for a Phase III program later this year.

Corporate

You recently closed a C$3.06M flow-through financing, priced at C$0.38 per unit (with each unit consisting of a share and ½ warrant at C$0.50 exercisable for a period of three years). This has boosted your cash and cash equivalent position to in excess of C$9M which was almost as much as your entire market capitalization just over a year ago. How things have changed. How much of your current cash position consists of flow-through money and how much will you have to spend by the end of this year and by the end of 2022?

After closing this recent non-brokered private placement, which was made up entirely of strategic institutional investors, the company now has over C$6M in cash, half of which is flow through that needs to be spent in the next 12 months. C$3 million should get us over 10,000 metres of drilling, the bulk of which will be at our Moore Project with a small amount likely to be allocated to our South Falcon Point Project host to the Fraser Lakes uranium and thorium deposit. We have another over C$3 million in equity positions of partner companies as well which have been appreciating recently.

Do you notice a difference in participants in your recent placements compared, say, two years ago? Is it still mainly a core group of Uranium aficionados or have you seen a more widespread interest in uranium assets from different types of investors?

We have noticed significantly more interest in the uranium sector from both institutional and retail investors over the last two years. Having said that, our financings continue to be made up of mostly of strategic institutional investors and family offices. Skyharbour is currently fortunate to include Denison Mines Corp., North Shore Global Uranium Mining ETF, MMCap, OTP Fund Management Ltd., Extract Capital, Sachem Cove Partners, KCR, and L2 Capital Partners as shareholders. More recently, we have seen quite a bit of retail and ESG focused investor interest in the open market as uranium equities have been moving higher.

You have some options (1.8M at C$0.30) and warrants (9 million warrants at C$0.27) expiring within the next few months (August 10th for the warrants). While you are probably excited to get the cash in, do you feel like this could keep a temporary lid on your stock?

We have been seeing these warrants steadily exercised over the last 6 months, yet we have still managed to see a rising price. Most of the remaining warrants, and all of the options, are now held by insiders, consultants, and close business associates so I do not expect there to be much in the way of selling pressure. The funds from the warrant exercise are being put to work advancing the projects, which is ultimately beneficial to the shareholders.

Have you seen any inbound interest to partner on other projects in your portfolio?

Yes, we are in discussions with several groups to option our Mann Lake, Yurchison and South Falcon Point Projects which we own 100% of each. We have seen much more capital flow into the uranium space in the last 6 months, including risk capital into exploration companies which should help facilitate new property transactions and partnerships.

We have built out our prospect generator model with over 240,000 hectares of properties to accommodate these groups and companies looking to earn-into or acquire outright prospective projects in the Basin. Skyharbour continues to execute on its business model by adding value to its project base in the Athabasca Basin through focused mineral exploration at its flagship Moore Uranium Project as well as utilizing the prospect generator model to advance its other projects with strategic partners.

Future cash payments and share issuances from partner companies allow us to monetize our asset base to keep equity dilution in check while benefiting from rising equity valuations as a shareholder of these partner companies.

The Uranium Sector

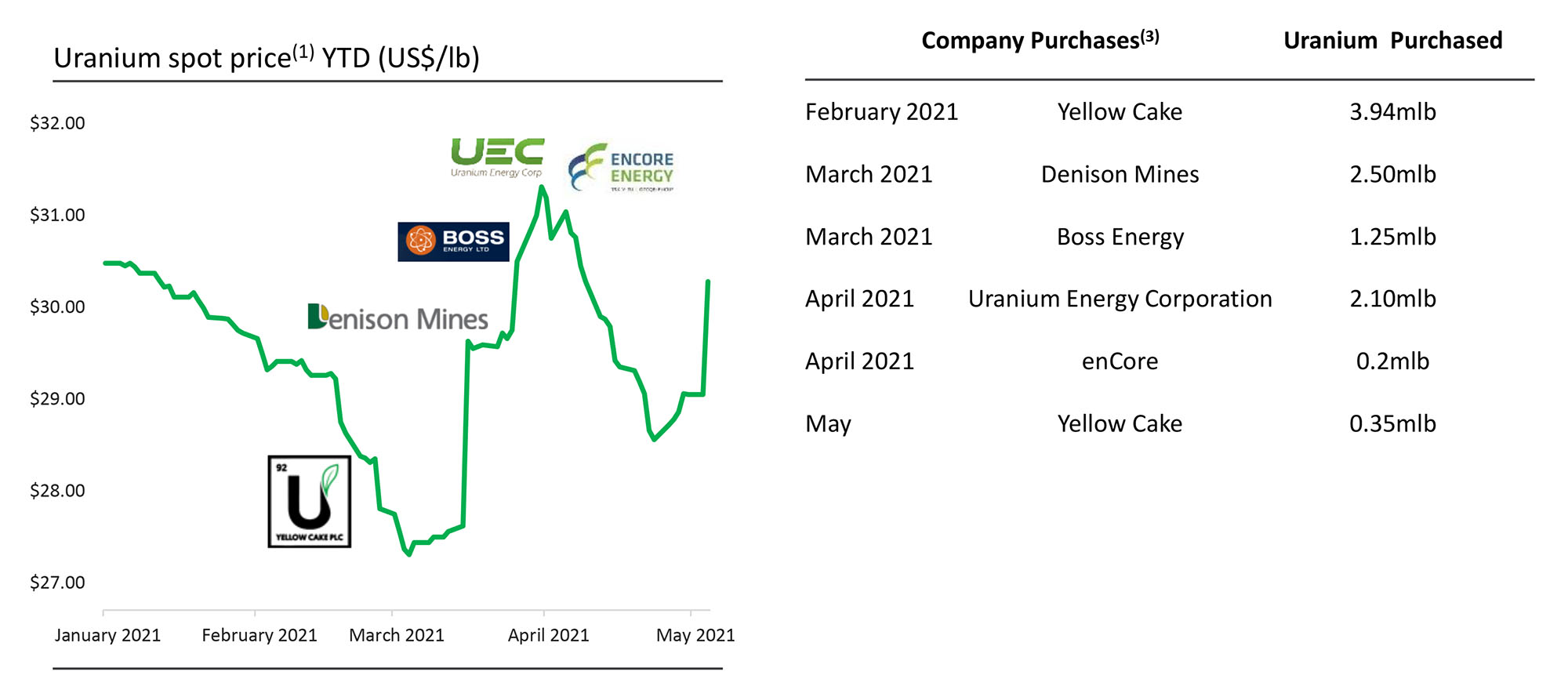

The uranium sector has been left behind for dead since Fukushima but is now showing signs of life again. A few years ago we saw the interest in uranium equities come back, only to fade away again. Meanwhile, we are now several years later which would mean tens of millions of pounds of uranium that were ‘readily available’ on the spot market should have been absorbed by now. Especially as we also saw new funds (Yellow Cake in London) buy more uranium on the spot markets while certain uranium miners did the same thing. How do you see the demand and supply evolving from here?

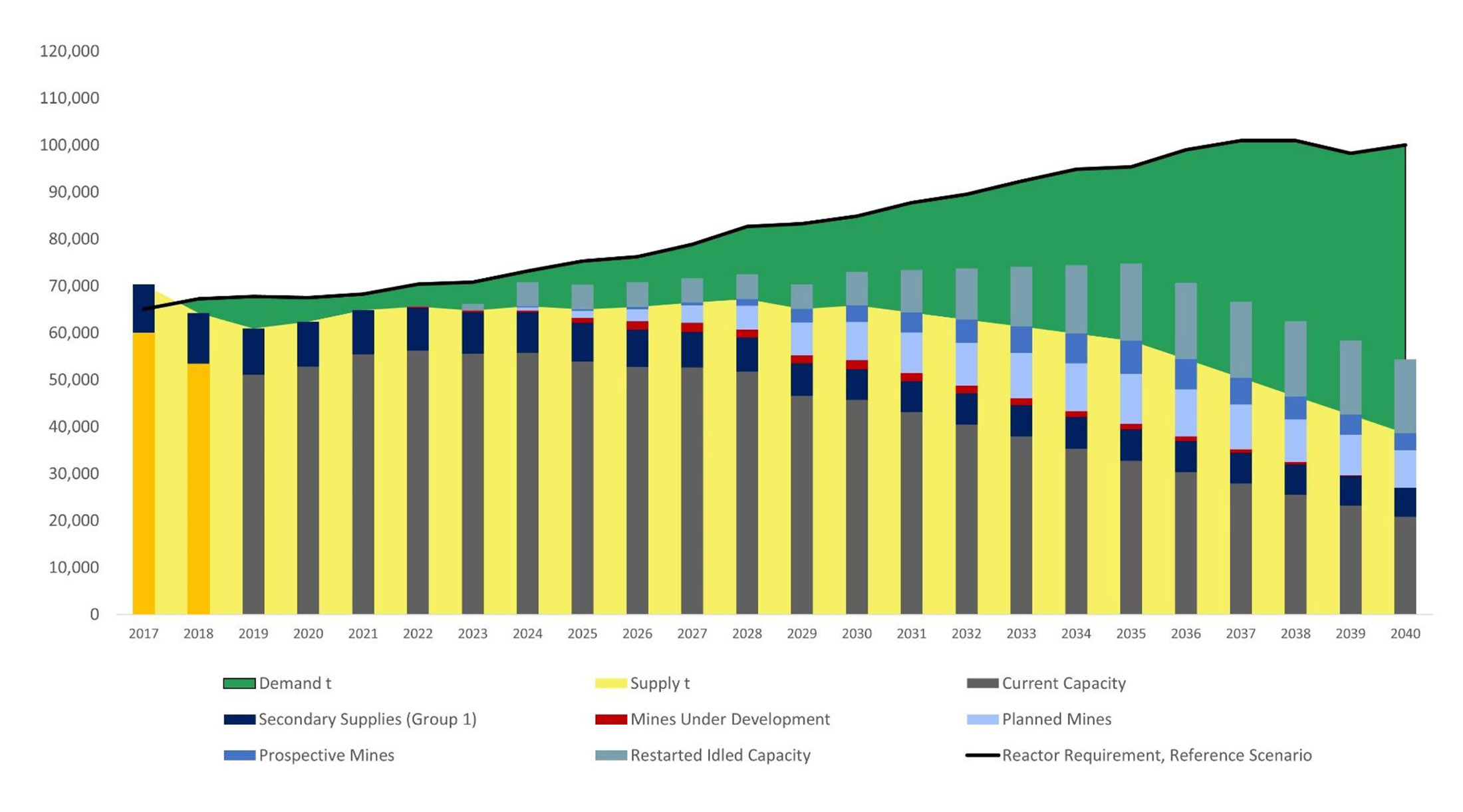

It is clear to me that we are now in the early stages of the next uranium bull market with rising equity valuations and a rising uranium price. Looking at the supply-demand fundamentals, there is a large primary mine supply deficit looming with only 120 million lbs produced in 2020 in the backdrop of over 180 million lbs of demand. Supply will likely increase back up to 140-150 million lbs assuming there are no more disruptions from Covid but that still amounts to a 30-40 million lb shortfall that must be made up from secondary supplies which have been dwindling over the last several years.

Given the success of Skyharbour’s drilling at the Moore Project over the last several years, the Company will be commencing a 2,500 metre Summer/Fall diamond drilling program consisting of 7-9 drill holes. Drill targets will include both unconformity and basement-hosted mineralization targets along the Maverick Structural Corridor and of particular interest are potential underlying basement feeder zones to the unconformity-hosted high-grade uranium present along the Maverick corridor (previous drill results include grades as high as 21% U3O8 over 1.5m).

The Company specifically plans to expand the high-grade mineralization recently discovered at the Maverick East Zone and to test the Viper target area along strike as well as new targets in the West Maverick area.

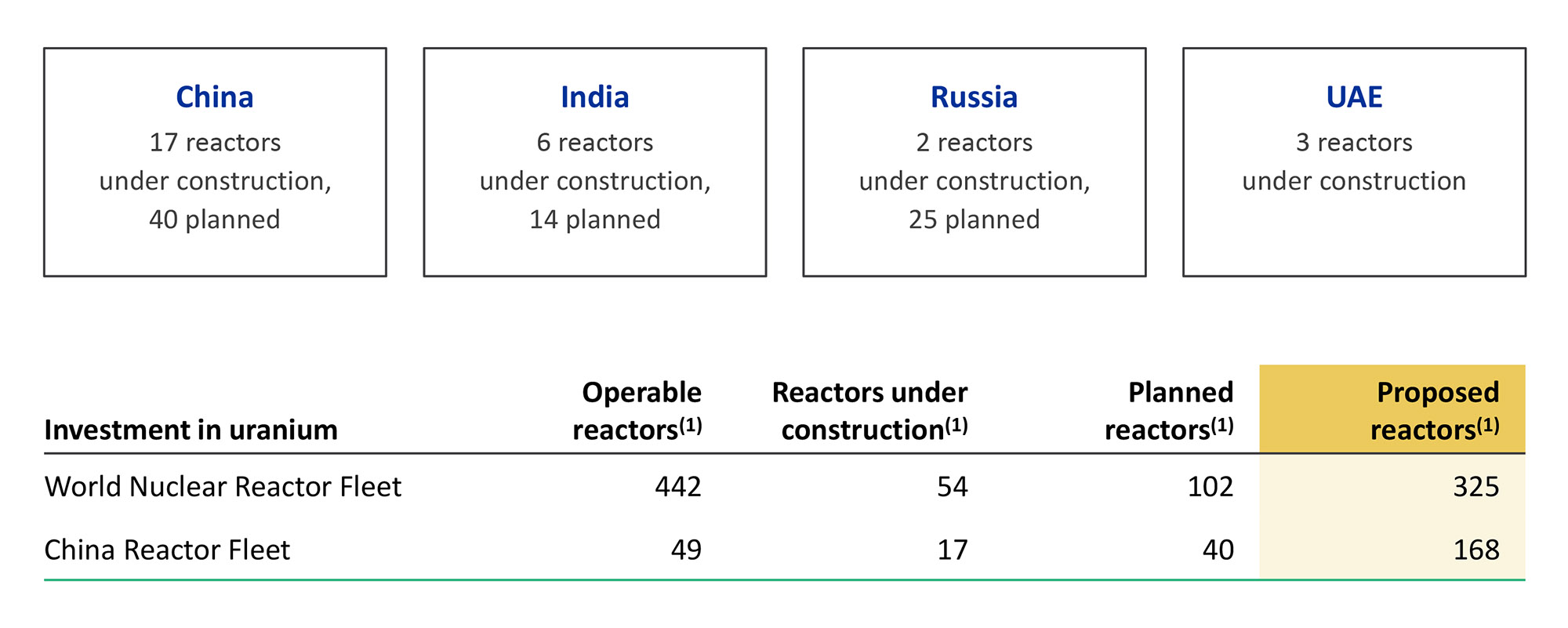

The demand side of the equation is looking stronger than ever with renewed interest in nuclear as countries race towards carbon neutrality with a massive energy transition underway from carbon-emitting sources of electricity to clean sources. Government policy support has improved dramatically and growth from non-OECD nations has been and continues to be the focal point for growth in demand over the last few decades. This has strengthened following the release of China’s 14th Five-Year Plan, which incudes a 40% increase in its nuclear fleet to 70GWe by 2025 as well as an additional 50GWe under construction. However, sentiment and growth potential in North America has been improving in the wake of bipartisan support for nuclear energy in the US for the first time in almost 50 years, the US rejoining the Paris Climate Agreement, and clear support for nuclear energy in the “American Jobs Plan”. The same appears to be happening in Europe as well with the European Commission recently announcing that it will potentially include nuclear energy in the European Union’s sustainable financing taxonomy.

Acknowledgement of nuclear power’s critical role in providing reliable, cost-effective, emissions-free, baseload power is gaining momentum. This has reduced the risk of accelerated plant closures in most nations and continues to drive growth in developing nations. The advent of SMR’s and new advanced nuclear technologies is also a potential new source of uranium demand that could have a dramatic impact on the market down the road.

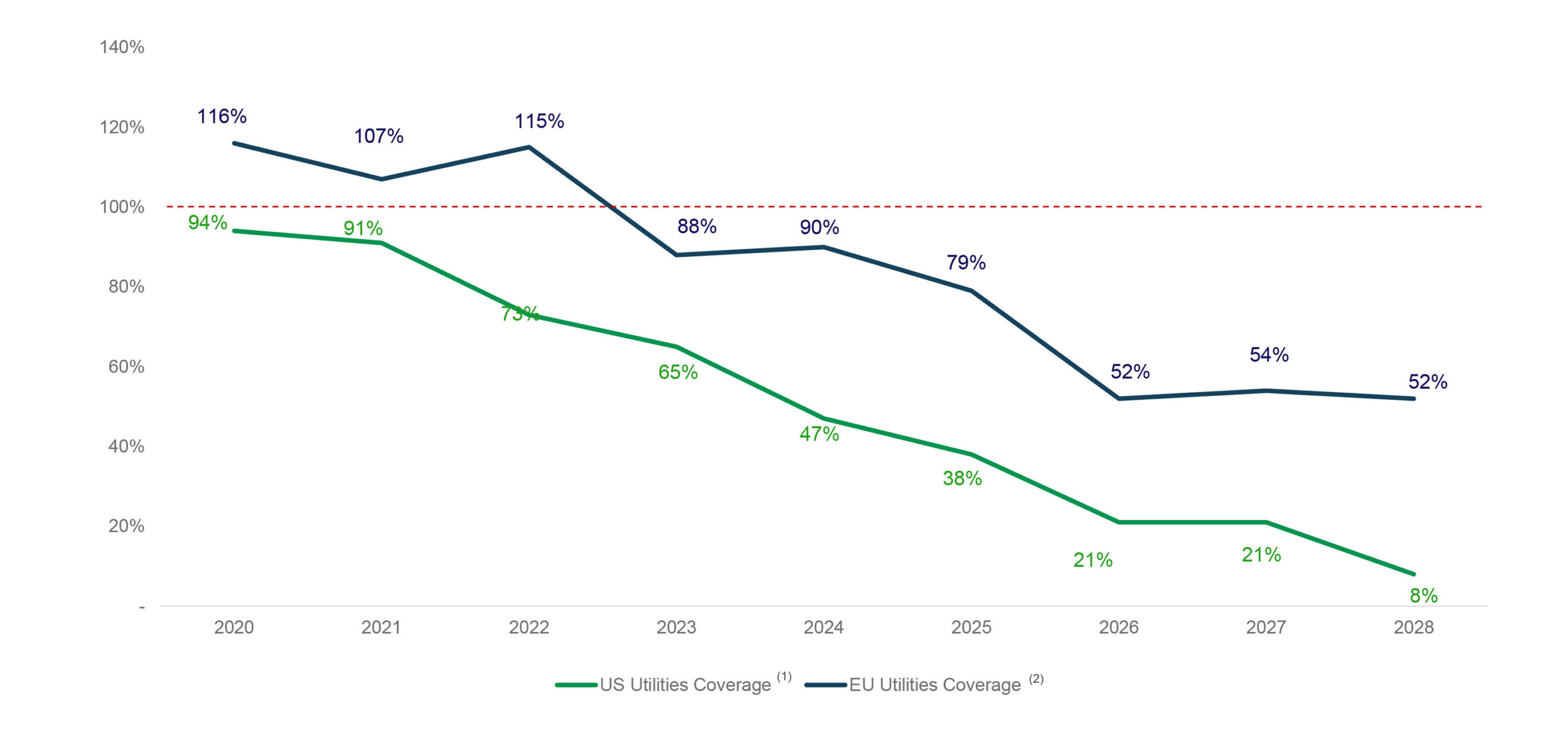

On the supply side, mine closures and unscheduled curtailments have caused a supply crunch. Primary supply remains under pressure, a situation which has only been compounded by the recent shutdowns of Ranger and Cominak which were collectively producing approx. 8.5 million lbs annually. The pandemic has created a slew of supply disruptions and has shown that the risks to the supply side far outweigh the risks to the demand side. Also, it is worth noting that conversion prices are now >US$20/kg U (up from US$8 a year ago) and SWU is US$53 (up from US$36 a year ago). These higher prices of the intermediate products in the nuclear fuel cycle reduce the drivers for secondary supply which is bullish for the uranium price

Uranium pricing at just over $30/lb in the spot market, is still not sufficient to facilitate restarts, let alone new mine developments. We have seen producers like Cameco and Kazatomprom continue to purchase material in the market to make up for curtailed production. Additionally, there has been a wave of announced physical purchases from uranium developers and holding companies (approx. 12.5 million lbs including purchases by Denison, UEC and Yellowcake) which is driving a further tightening of the market. With uncovered utility demand increasing globally (in the US it is estimated to rise to 50% in the next three years), this increasing spot market activity should force utilities back to the market earlier than planned.

Finally, a major recent development is Sprott Asset Management taking over the management of Uranium Participation Corp., a physical uranium holding vehicle. Sprott will reorganize UPC from a corporation into a trust and plans to list on the New York Stock Exchange. Sprott should benefit from its well-established brand name in the money management business and aims to leverage its 200,000 investors to improve trading liquidity. The very simple implication is this is going to drastically enhance access to the everyday investor who wants to be able to force purchases of physical uranium.

Cameco recently announced it will be restarting the Cigar Lake mine, does this have an impact on your anticipated timeline to see a higher uranium price? Or do you think Cameco is simply starting the restart process now as it will need a certain lead time to get back up to full production?

It does not have much of an impact on my anticipated timeline and it will take some time before the mine is producing at full capacity (likely 6-12 months). We saw a temporary pullback of ~$2/lb in the uranium spot price after Cameco announced they were restarting Cigar Lake, but the price bounced back quickly, and Cameco is still forecasting a uranium deficit of more than 33 million pounds in 2021. Tim Gitzel, the CEO of Cameco, recently stated: “There are significant costs associated with having the mine in temporary care and maintenance, and we have a home in our contract portfolio for these low-cost pounds. We will also continue to purchase material, as needed, to meet our committed deliveries.” It is worth noting that even with Cigar producing at full capacity, there is still a major primary supply deficit. We will also need to see several similar Cigar-sized mines developed and producing in the next decade to meet the shortfall and satisfy growing demand.

Conclusion

Syharbour Resources is definitely nicely surfing on the waves of the renewed interest in the uranium sector. Not only has the share price been moving up, Skyharbour also tapped the markets to fill its treasury. Additionally, we can expect the company’s cash balance to remain stable as the exploration expenses will be covered by the cash inflow from the warrant exercises with almost 2 million options and 9 million warrants currently in the money.

There have been a few ‘false alarms’ in the uranium space in the past decade, but markets and investors sound more upbeat now as the inventory levels of physical uranium are dwindling fast.

Disclosure: The author has a long position in Skyharbour Resources. Skyharbour Resources is not a sponsor of the website but has been a sponsor in the previous twelve months. Please read our disclaimer.