After several years of hibernation, the uranium market seems to be coming back to life. Uranium giants Cameco and Kazatomprom have announced they will scale back their uranium production rates to bring the supply in balance with the demand. On top of that, a new company, Yellowcake (listed on the London Stock Exchange) has struck a deal with Kazatomprom to purchase just over 8 million pounds of uranium at spot prices. 8 million pounds that will no longer be hitting the market.

After several years of hibernation, the uranium market seems to be coming back to life. Uranium giants Cameco and Kazatomprom have announced they will scale back their uranium production rates to bring the supply in balance with the demand. On top of that, a new company, Yellowcake (listed on the London Stock Exchange) has struck a deal with Kazatomprom to purchase just over 8 million pounds of uranium at spot prices. 8 million pounds that will no longer be hitting the market.

We do believe the uranium sector has reached a turning point as there are very few large-cap and mid-tier producers left (Paladin Energy (ASX:PDN) went bankrupt, and several other smaller producers had to team up and subsequently go into hibernation mode). This means uranium investors (both retail and institutional) will have to follow the food chain and have a look at exploration companies.

Skyharbour Resources (SYH.V) is one of those uranium exploration companies that could be particularly appealing, as it employs a dual strategy of focused exploration at its flagship Moore project as well prospect generation at its other projects to ensure they are advanced and the level of news flow remains high.

The company is also gearing up to publish its own maiden resource estimate at the Moore property in H1 2019. To complement its top-tier project base and experienced team, Skyharbour has two larger strategic partners in Denison Mines (DML.TO, DNN) as its largest shareholder and industry leader Orano out of France is earning a majority stake on one of Skyharbour’s properties. And the timing couldn’t be better: a go-to uranium exploration story by the time we expect the entire uranium sector to heat up.

The Athabasca Basin: the hot spot for serious uranium exploration companies

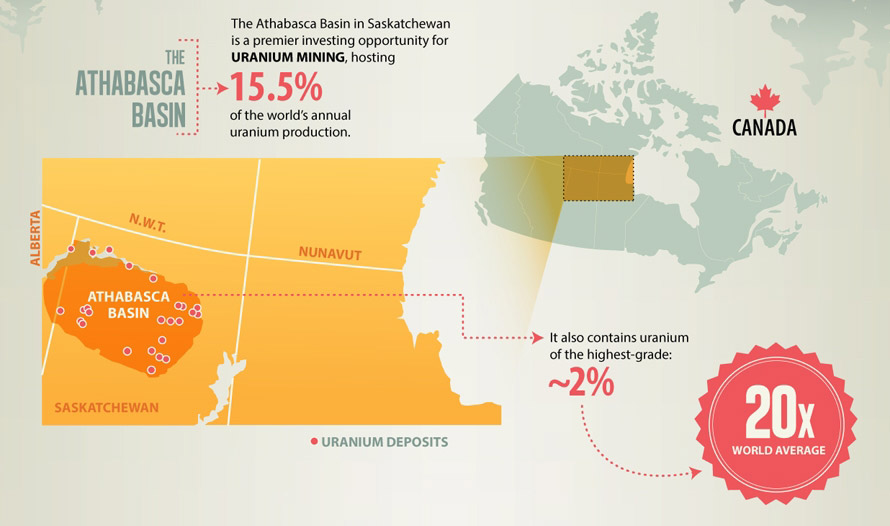

Anyone who’s serious about exploring for uranium in Canada will be focusing on the Athabasca Basin in Saskatchewan. Yes, there are other uranium projects in other provinces, but those continuously hit walls with exploration and development moratoria and low grades (for instance, Paladin’s Michelin project in Newfoundland hasn’t gone anywhere in the past few years).

The situation is different in the Athabasca Basin, which has been known for its (high grade) uranium occurrences since the 1940’s and where the local Saskatchewan government has developed a good (legal) framework and is backing the uranium industry. Since the Rabbit Lake uranium deposit was discovered in the late-60’s, an additional 100 uranium discoveries have been made in the Athabasca Basin, with resources totalling in excess of 2 billion pounds of uranium. According to a recent keynote submitted to and published on the PDAC website, just 1/3rd of the discoveries have been brought into production.

The Basin heated up in 2010 and 2011 which culminated in Rio Tinto (RIO) winning a bidding war to acquire Hathor Exploration for C$650 million. This was followed by the huge discoveries made by Nexgen Energy (NXE, NXE.TO) and Fission Uranium (FCU.TO), which reconfirmed the Athabasca Basin as ‘the place to be’ for high-grade uranium exploration.

Moore: gearing up for a summer drill program and maiden resource estimate

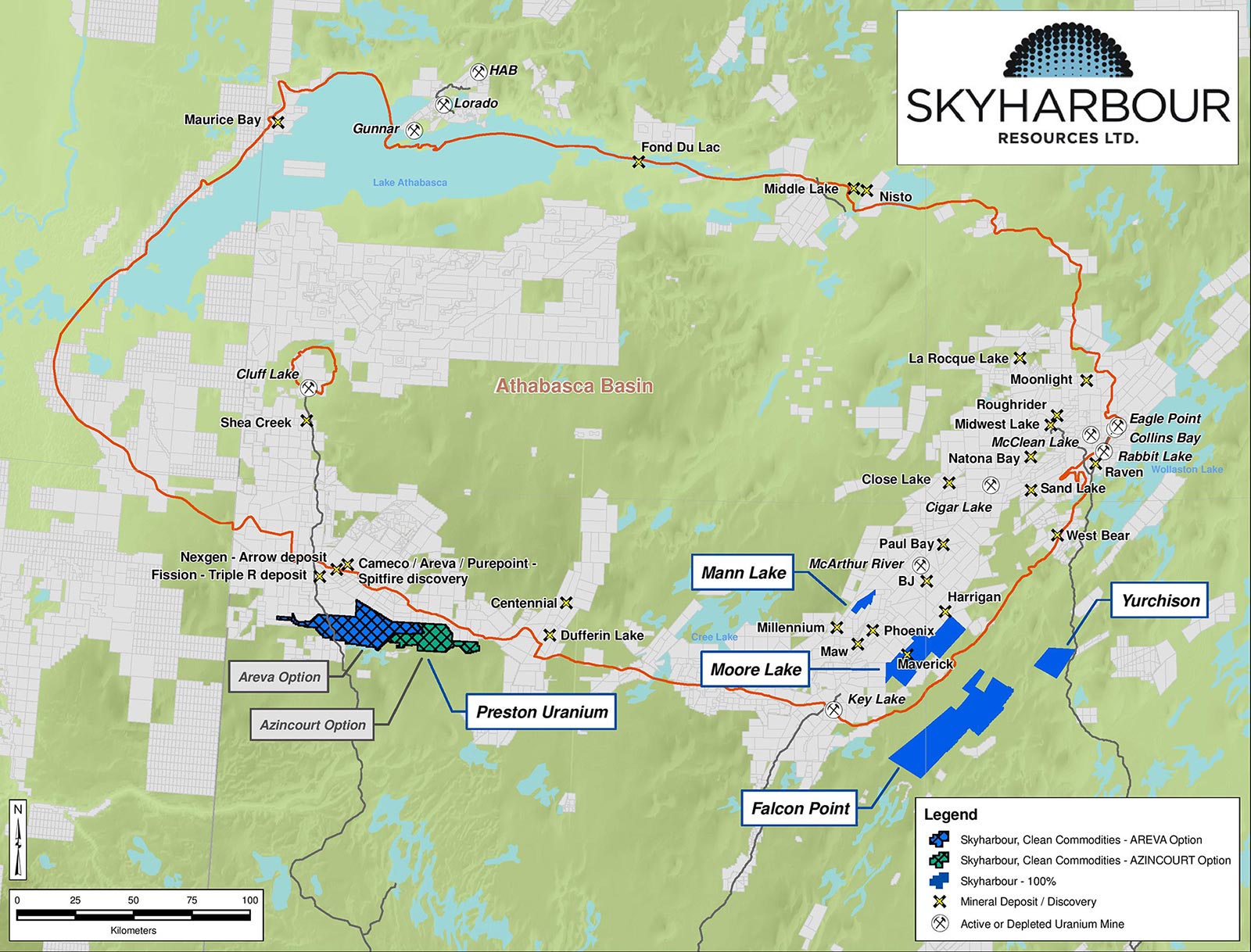

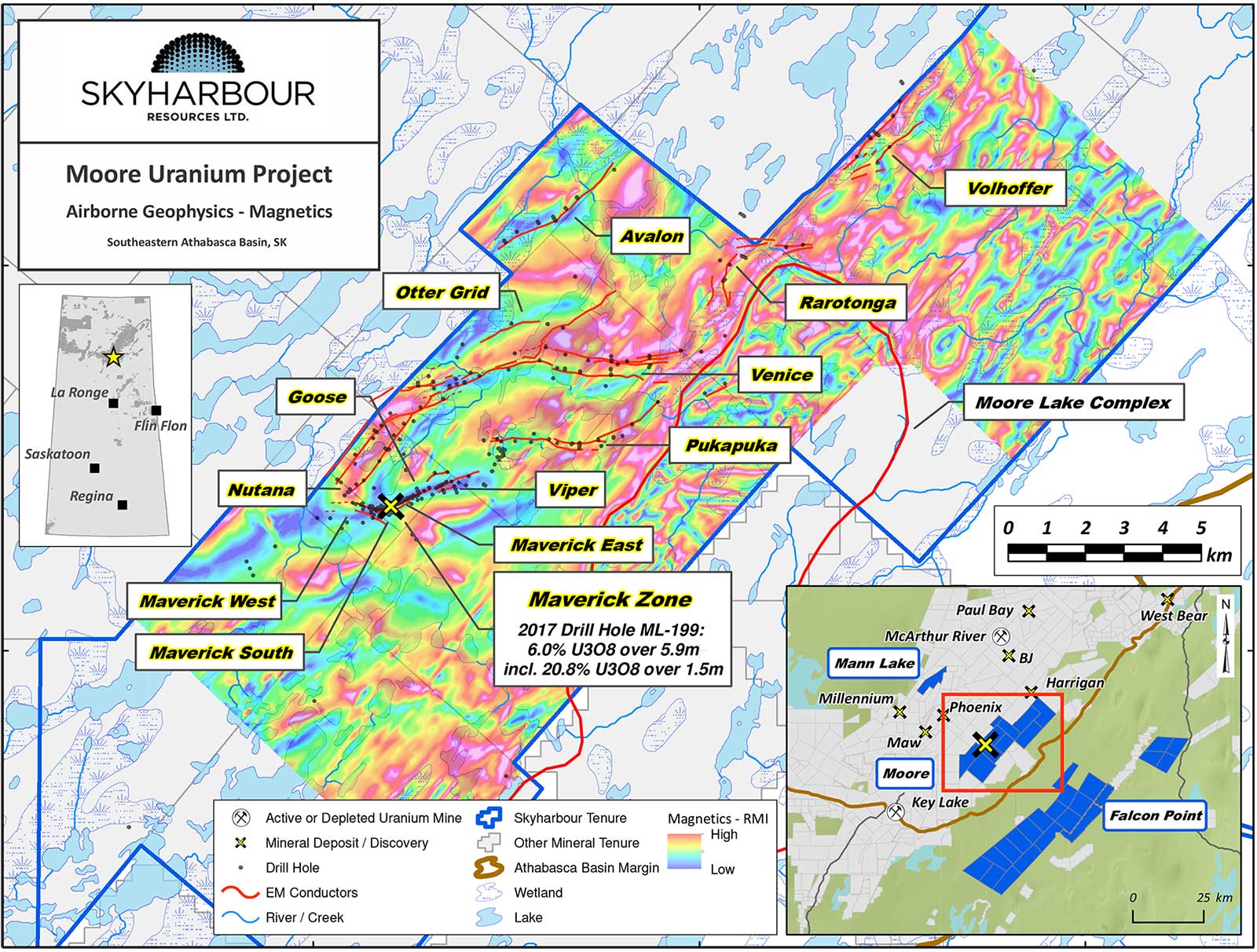

The high grade Moore Uranium Project is Skyharbour’s flagship asset as this 35,700-hectare property should be seen as an advanced stage exploration project. The project has had a fair bit of significant historical drilling and a high grade zone called the Maverick Zone was discovered in the early 2000’s. Skyharbour’s recent drill programs have expanded this high grade zone and have yielded additional discoveries along strike.

The project is located on the southeastern end of the Athabasca Basin, and is just 15 kilometers away from Highway 914. That’s an important feature as the nearly immediate access to a road is helping the company to keep the operating and exploration expenses down. More importantly, the property is located close to the power grid as well, so as far as exploration projects go, the access to existing and freely available infrastructure is a huge bonus.

The property has been around for about 40 years, and the first traces of uranium mineralization were discovered in 2000 when a joint venture between Kennecott Exploration (Rio Tinto) and JNR Resources encountered almost 10 meters at 0.44% U3O8. This Maverick zone was subject to very extensive exploration campaigns in the subsequent few years. JNR continued to work on the property (in joint venture with Denison Mines, when Kennecott dropped out), and was able to quickly advance the property. A total of 120,000 meters was drilled, which allowed JNR and Denison to delineate the high grade Maverick pod contained in the 4 km long Maverick corridor.

This first pod of high grade uranium is approximately 220 meters in length and sits at the unconformity at about 265 meters depth. Skyharbour recently discovered another pod approximately 100 meters along strike from the known high grade pod and is looking to make additional discoveries with only half of the 4 km Maverick corridor having been systemically drilled.

The recent drill programs carried out by Skyharbour have revealed some very interesting results including 20.8% U3O8 over 1.5m within 5.9m of 6.0% U3O8, 9.12% U3O8 over 1.4m, and 5.29% U3O8 over 2.5m. The upcoming summer drill program will be interesting as Skyharbour plans to drill test the potential feeder zones of this high grade uranium in the underlying basement rocks. Recent basement hosted discoveries include well know discovery successes like Nexgen Energy (NXE.TO, NXE) and Fission Uranium (FCU.TO).

And don’t think the Maverick zone is the only thing the Moore property has to offer. We talked to the company’s CEO, and Jordan Trimble is convinced there’s a very good chance to discover more high grade mineralized zones. His expectations and claims don’t come out of the blue, as JNR and Denison have already found over 10 other high priority targets on the property many of which have had uranium in previous drill core.

Although it’s easy to be side-tracked to pursue other high-value targets, Skyharbour kept its eye on the main prize and realized it needs to complete a resource estimate on the Maverick zone to avoid being perceived as an ‘eternal exploration company’: exploring without being able to release tangible results. We firmly agree with this approach, and with a maiden resource estimate on the important Maverick zone, Skyharbour will have a platform to build upon, and have something tangible to show the market.

The earn-in terms

Skyharbour can acquire 100% of the property by paying C$500,000 in cash ($200,000 of which has been paid) and spending C$3.5M on exploration within a 5-year time frame (which has now been spent). Although Skyharbour has the option to earn a 100% stake in Moore Lake, Denison Mines has the right to re-acquire a 51% stake on two different occasions.

Denison has the right to exercise a first buyback option to repurchase a 51% interest in the property by making a payment of C$200,000 and spending C$6.75M in exploration expenditures on the property in the subsequent three years, where after both companies would form a 51/49 joint venture. If Denison doesn’t exercise the first buyback option, Skyharbour would retain full ownership in the property but would need to incur an additional C$3M in exploration expenditures in a five-year period to force Denison’s hand on the buyback option. If Skyharbour does not spend this additional $3M in five years, Denison retains a perpetual buyback option on the property for 2.5x whatever Skyharbour spends.

At this point (after completing the additional C$3M in exploration expenditures), Denison may elect to exercise a second buyback option to repurchase the same 51% stake by making a cash payment of C$500,000 to Skyharbour and by spending C$16.5M on exploration in the next four years.

We would expect Denison to pass on the buyback right after the first stage, but should Skyharbour prove up the value of the property by discovering more uranium-bearing mineralized zones, it’s not unlikely Denison would exercise the C$16.5M back-in right. So either Skyharbour will end up with 100% of the property, or 49% whilst being carried for the subsequent C$16.5M in exploration expenditures.

Both potential outcomes are fine with us, considering Skyharbour’s current market capitalization is just CAD $25M, which also includes the other irons in the proverbial Athabasca Basin fire with the other projects.

The prospect generator model

As Skyharbour is prioritizing its (human and capital) resources on the Moore project, it didn’t want to spread itself too thin. It decided to option out its other projects and has some sort of hybrid model: focusing on one own property, while using the prospect generator model to keep the news flow going, and advance other properties using other companies’ money.

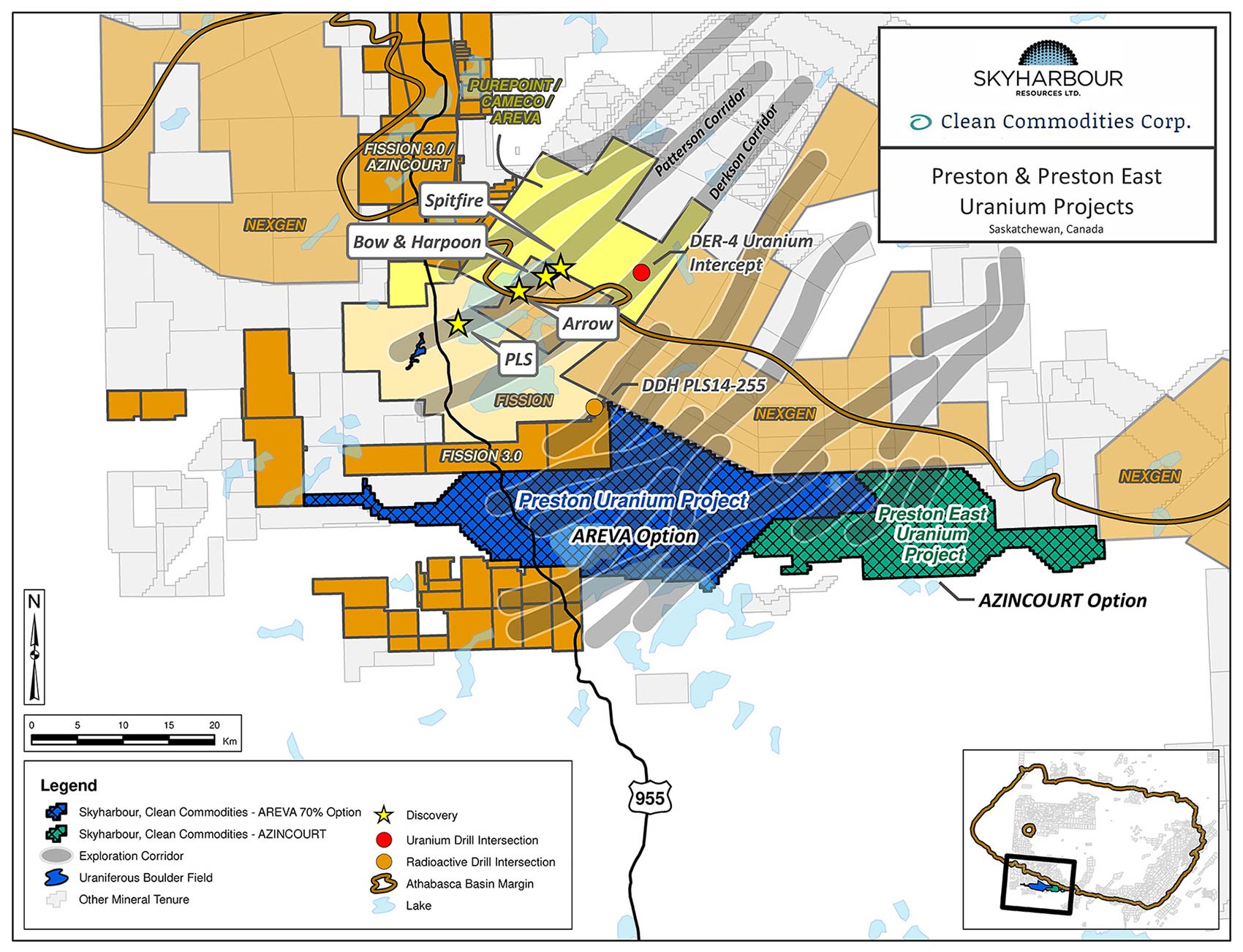

Back in 2017, Skyharbour was able to attract AREVA (now: Orano), the large French nuclear power and uranium mining conglomerate as a joint venture partner on the Preston uranium project on the western end of the Athabasca Basin. Perhaps a surprising deal as AREVA had not done many deals with junior companies in recent history. But the fact it wanted to up its game in the Athabasca Basin and its mindset on the cusp of a restructuring was ‘yes, we really need this project’ says a lot about the Preston project. Fortunately the French government stepped in and recapitalized the company to the tune a of few billion euros which allowed Orano to continue with its day-to-day operations.

The earn-in agreement is relatively straightforward. Orano can earn up to 70% after spending C$8M in cash payments and in exploration expenditures on the property. A first 51% will be acquired by spending C$2.8M on the property and making a C$200,000 cash payment to Skyharbour Resources and Clean Commodities (CCE.V).

This indeed means that upon completing the earn-in phase of the joint venture deal, a threeway joint venture agreement will be in effect whereby Orano will own 70% of the almost 50,000 hectare land package whilst Skyharbour and Clean Commodities will each own 15% of the project. One could say that this won’t move the needle for Skyharbour, but there are three reasons why we think this is a good deal. First of all, Orano will have to spend C$8M to earn the 70% stake. This includes C$7.3M in high-risk exploration money (on top of the C$0.7M cash payments) Skyharbour doesn’t have to spend themselves. Secondly, it’s better to end up with 15% of a discovery instead of just sitting on the claims and risking the claims lapsing.

A second, separate agreement allowed Skyharbour to option the eastern end of Preston, conveniently called Preston East, to Azincourt Energy (AAZ.V). Azincourt will be able to acquire a 70% stake by making C$1M in cash payments and spending at least C$2.5M on exploration within a three-year period (we are now almost halfway that period). Additionally, Azincourt issued 4.5M of its stock to both Skyharbour and Clean Commodities in a 50/50 ratio (so Skyharbour ended up with 2.25M shares, currently valued at just over C$200,000).

But why is the Preston property so interesting?

The initial field work completed by Orano was focusing on completing the geophysical survey to define good drill targets and now the geophysical exploration program has been completed, Orano is gearing up for its first few drill programs. An initial program was recently completed with assays pending.

Azincourt is one step behind, as it just completed geophysical exploration programs in order to find the prospective drill targets.

This first round of Azincourt’s exploration program was successful as the HLEM and ground gravity surveys confirmed the existence of basement conductors which could host the unconformity-related uranium projects. Drilling is planned for this winter.

We have now discussed the company’s main two projects, but keep in mind it still has the 100% owned Falcon Point, Yurchison and Mann Lake projects in the portfolio. During a recent call with Skyharbour’s CEO, it sounds like these properties could also be optioned out (we would expect a similar earn-in model as on the Preston project to be deployed), but it could make more sense to wait for the uranium market to really turn around before actively pursuing a joint venture deal.

The financial situation, share structure and management

As of at August 3rd, the company had a total share count of 61M shares with over C $3.2M in the treasury having just raised $2.6M in a private placement consisting of common shares at $0.40 and flow through shares at $0.45.

Should the uranium market indeed get going again and Skyharbour’s upcoming exploration program be successful, the C$0.60 warrants in this financing could be seen as a ‘secondary financing’ bringing in an additional C$3.7M.

Jordan Trimble – Director, President and CEO

Jordan Trimble is the President and Chief Executive Officer of Skyharbour Resources. Mr. Trimble holds a Bachelor of Science Degree with a Minor in Commerce from UBC and he is a CFA® charterholder and serves as a director of the CFA Society Vancouver. He has worked in the resource industry in various roles with numerous TSX Venture listed companies specializing in corporate finance and strategy, shareholder communications, marketing, deal structuring and capital raising. Previous to Skyharbour, he managed the Corporate Development for Bayfield Ventures, a gold company with projects in Ontario which was acquired by New Gold (TSX: NGD). Mr. Trimble has an extensive network of institutional and retail investors as well as resource industry professionals bringing valuable relationships to the Company. He has appeared on BNN several times and has given presentations at numerous resource conferences across North America. Mr. Trimble has completed the Canadian Securities Course and Technical Analysis Course offered through CSI as well as several geology, exploration and mining courses.

Richard Kusmirski – Director, Head Technical Advisor, and Qualified Person

Rick Kusmirski, P.Geo, M.Sc., Head of Advisory Board, has over 40 years of exploration experience in North America and overseas, and has actively participated in the discovery of a number of uranium, gold and base metal deposits. For several years, in his capacity as Exploration Manager, he directed Cameco Corporation’s (TSX: CCO) uranium exploration projects in the Athabasca Basin. In 1999, Rick joined JNR Resources becoming Vice President of Exploration in 2000. Subsequently, he directed the exploration program that led to the discovery of the Maverick Zone on the Moore Lake uranium joint venture in the Athabasca Basin in Saskatchewan with partner Kennecott Canada. Rick became JNR’s President and CEO in January of 2001. In February of 2013, Denison Mines Corp. (TSX: DML) successfully acquired all of the outstanding shares of JNR by way of a friendly all-share take-over bid.

James G. Pettit – Director, Chairman of the Board

Jim Pettit is the Chairman of the Board of Skyharbour Resources Ltd. Mr. Pettit is currently serving as a Director on the Boards of several public resource companies and offers over 30 years experience within the industry specializing in finance, corporate governance, management, and compliance. He specializes in the early stage development of private, as well as public companies. His background over the past 30 years has been focused primarily within the resource sector and he was previously Chairman and CEO of Bayfield Ventures Corp. which was sold to New Gold in 2014.

David Cates – Director

David Cates, CPA, MAcc, is a Director of Skyharbour. He is the President and CEO of Denison Mines (TSX: DML) and Uranium Participation Corp (TSX: U). Prior to being appointed the President and CEO position Mr. Cates served as Denison’s Vice President Finance, Tax and Chief Financial Officer. As Chief Financial Officer, Mr. Cates played a key role in the Company’s mergers and acquisitions activities – leading the acquisition of Rockgate Capital Corp. and International Enexco Ltd. Mr. Cates joined Denison in 2008 and held the position of Director, Taxation prior to his appointment as Chief Financial Officer. Prior to joining the Company, Mr. Cates held positions at Kinross Gold Corp. and PwC LLP with a focus on the resource industry.

Paul Matysek – Advisory Board

Paul Matysek is a Strategic Advisor for Skyharbour and is a mining entrepreneur, professional geochemist and geologist with over 35 years of experience in the mining industry. He was the Founder, President and CEO of Energy Metals Corporation (“EMC”), a premier uranium company that traded on the New York and Toronto Stock Exchanges. Mr. Matysek led EMC as one of the fastest growing Canadian companies in recent years, increasing its market capitalization from $10 million in 2004 to approximately $1.8 billion when it was acquired by a larger uranium producer, Uranium One Inc., in 2007. Mr. Matysek was recently the President and CEO of Goldrock Mines Corp. which on June 7th, 2016 announced it had entered into a definitive agreement to be acquired by Fortuna Silver Mines (NYSE:FSM) (TSX:FVI) for $129 million on a fully-diluted in-the-money basis. Previously, Mr. Matysek was the President and CEO of Lithium One Inc., which developed a high quality lithium project in northern Argentina. In July 2012, Lithium One and Galaxy Resources merged with a $112 million plan to create a fully integrated lithium company. Prior to Lithium One, Mr. Matysek was the President and CEO of Potash One Inc. where he was the architect of the $434 million friendly takeover of Potash One by K+S Ag, which closed in early 2011.

Uranium: a story for 2019

The past few years haven’t been great for any uranium investor. The Fukushima disaster killed all hopes for a swift move in the uranium price, but we feel the situation is now slowly turning around.

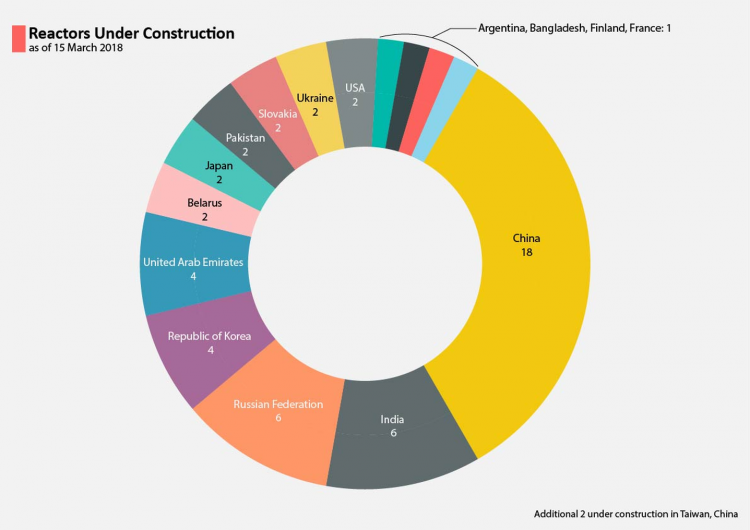

Contrary to what the uranium price action has been showing in the past few years, the total demand for uranium continues to increase. Germany and Belgium have been slow to “phase out” their nuclear power plants and for every plant that’s being shut down in Western Europe, India and China and other parts of the developing world are opening a few dozen of them. Right now, a total of 56 nuclear reactors are under construction worldwide, of which 24 are based in China and India, with Russia being responsible for an additional 9 reactors.

Those three countries are thus building 33 new nuclear reactors, and this doesn’t take the total of 252 new reactors that are being proposed and planned into consideration. Conclusion: We shouldn’t be too worried about the demand side for uranium. China and India are net importers of uranium, and as Russia currently is a net exporter, its total amount of exported uranium will very likely decrease as its domestic consumption will increase.

But there’s more than just this. Although the uranium consumption levels and total uranium demand have been increasing over the past few years as well, this was hidden by the higher amount of spot sales from the owners of nuclear power plants in Japan which were reducing their stockpiles. But that’s about to end.

Not only is the overhang of the stockpiles pretty much cleared by now, there will also be some changes on the supply side. Rather than just making hollow comments about the uranium price, Kazatomprom and Cameco aren’t just talking the talk, but are also walking the walk as both companies have announced severe production cuts to the tune of 25% of the total market. On top of that, Paladin Energy came out of a bankruptcy procedure after the majority of its debt was converted in new equity, which basically wiped out the existing shareholders.

But exactly because the debt was almost completely removed from the balance sheet, Paladin had no incentive to keep the Langer Heinrich mine up and running, as it has traditionally been selling uranium from the low-cost long mine life Langer Heinrich project on the spot market. The impact? An immediate 2.5 million pounds per year was removed from the spot market (based on the recent quarterly production results). However, as Langer Heinrich was predominantly working through stockpiled rock as it halted its mining activities in 2016, the total impact based on a normalized production rate is 5 million pounds per year.

On top of that, a new London-listed outfit called Yellowcake (what’s in a name) has completed its IPO in July. The business model of the company is pretty simple: it will purchase physical uranium from Kazatomprom and just sit on it, waiting for the prices to improve. It has entered into an agreement with Kazatomprom to purchase approximately 8 million pounds of uranium at spot prices and can purchase $100 million worth of uranium per year for the next 9 years.

We honestly believe the uranium sector is gearing up for a perfect storm. The major producers have announced production cuts whilst other mines and projects have been placed on care and maintenance. It’s not easy to bring projects back online from a care and maintenance status, and it will take several years to reach the full production capacity.

Meanwhile, Cameco obviously still has to honor the existing offtake contracts with its clients, and has confirmed its intentions to purchase 10 million pounds of uranium on the spot market next year and could step up its buying pace from 2020 on. That’s important as it means Cameco isn’t only taking uranium off the supply side, it will become a net buyer on the demand side as well in an attempt to corner the spot market.

This means the utility companies which have been printing money by purchasing cheap uranium on the spot market will be pushed into a corner as that very same spot market is now facing a severe drought. Keep in mind that most of the uranium prices are set based on long-term offtake agreements and the spot prices are relatively irrelevant for producers and utilities. But once the spot market starts to move up, it will be reflected in a higher long term contract price as well. And THAT is why the uranium spot market matters.

Conclusion

Uranium appears to have reached a turning point as the demand continues to increase and the main uranium suppliers have announced major production cuts as well as buying material to prop up prices in the spot market. We face lower output from the smaller independent players (Paladin Energy, UR-Energy, Energy Fuels and Uranium Energy Corporation). And there is a forecasted supply deficit in 2018 for the first time in many years.

As several major utility providers are also slated to renew their uranium purchase contracts in 2019-2021, the uranium price could finally break out, and this will have a positive impact on every part of the uranium supply chain: producers, developers and exploration stage companies should enjoy renewed attention and interest, and we expect more money to flow to the sector, enabling smaller exploration outfits to continue to develop their properties and grow at a rapid pace.

Skyharbour’s hybrid strategy of exploration and prospect generation appeals to us as Azincourt Energy and Orano are spending millions of dollars (and creating news flow) on one of the properties, which allows Skyharbour to fully focus on its flagship Moore property in anticipation of a maiden resource estimate in the first half of next year.

Disclosure: Skyharbour Resources is a sponsoring company. We have a long position. Please read the disclaimer