Southern Silver (SSV.V) has kept its promises and provided an updated resource estimate on its flagship Cerro Las Minitas project in the second quarter of the year. We have combed through the technical report of the resource update and combined this with the previously reported results of the metallurgical test work on the different types of mineralization at CLM to build some sort of (very) preliminary economic model to check how the recent resource updates and more finetuned metallurgical test work has impacted the NPV of the project.

All our calculations are based on what we think are reasonable assumptions, but keep in mind they are for educational purposes only and should definitely not be interpreted as Southern Silver’s official guidance or expectations. The official Preliminary Economic Assessment, expected to be published in late 2020, is the document that will really matter.

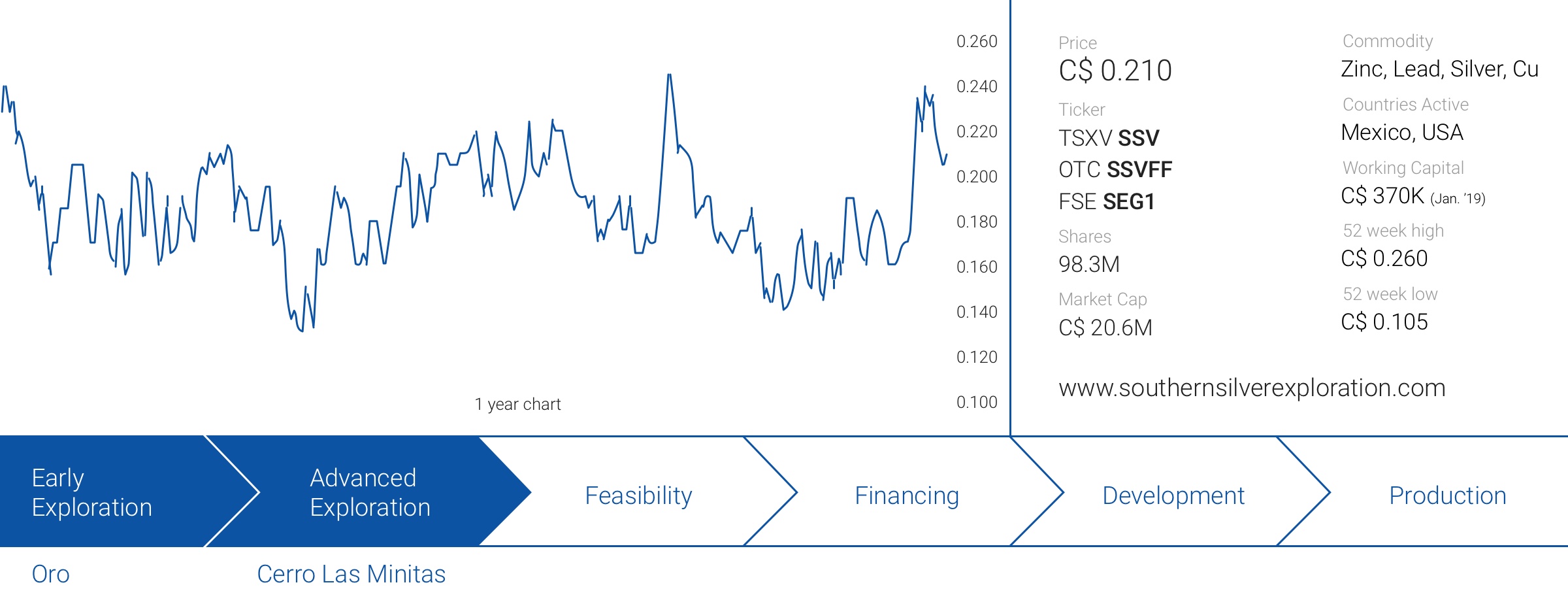

The share count and working capital position mentioned above do not include the impact of the current private placement and warrant exercises yet.

The background of Cerro Las Minitas

Cerro Las Minitas clearly is Southern Silver’s flagship as it continues to grow and expand the mineral resources from the earlier reported 2018 estimate of 209 million ounces silver-equivalent. Cerro Las Minitas (hereafter sometimes called ‘CLM’ for simplicity sake) is Southern Silver’s 34,500 hectare property located towards the northeast of the city of Durango, in Mexico’s Durango state which is just a short drive away.

Southern Silver started the earn-in procedure to acquire a 100% ownership in these claims in 2010, and in 2014 it completed the requirements of this earn-in agreement. Once it owned the entire project, SSV was able to attract the Electrum Group as a joint venture partner with Electrum earning up to a stake of 60% in the property through a US$5 million earn-in. The injection of cash was just what the project needed and resulted in 24,500m of additional core drilling, allowing Southern Silver to publish an initial mineral resource estimate in 2016.

Upon Electrum having completed its earn-in commitments to own a direct stake of 60% in the project and a 36% stake in Southern Silver (for a total direct and indirect interest of almost 75% in Cerro Las Minitas) the 60/40 joint venture was formed, and both partners continued to work on advancing Cerro Las Minitas. Needless to say, Electrum has a lot of influence on the (exploration) decision making process and a vested interest in seeing the project develop into a world-class deposit. Being a major investor, Electrum’s interest is strongly aligned with other investors.

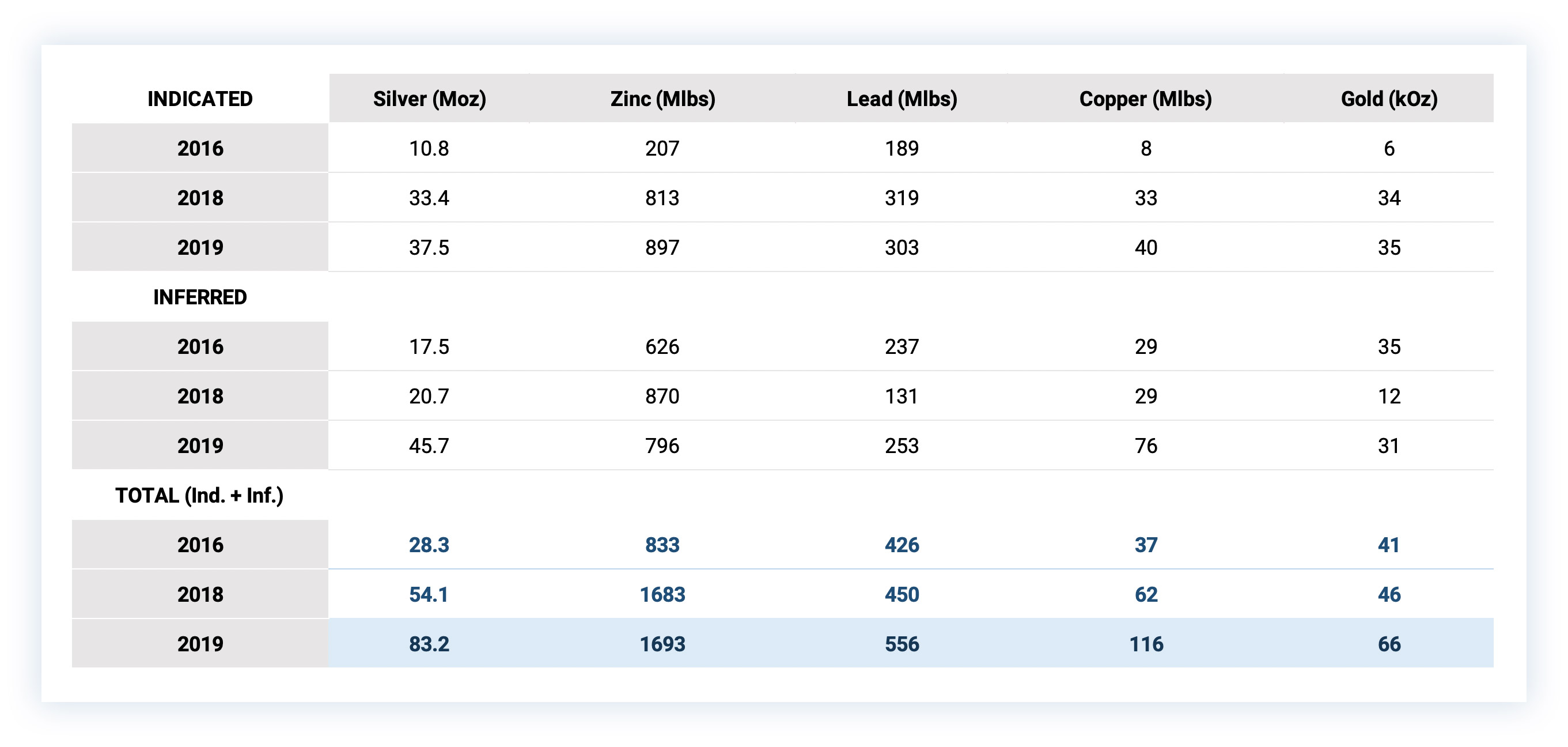

That’s why Electrum hasn’t been playing any ‘funny games’ in the past few years and has always prioritized the project over corporate games. A good approach as just last quarter, another resource update was published which once again expanded the resources at Cerro Las Minitas. In the next table, you can find the consecutive resource updates since 2016, showing the continuous increases.

The pre-summer resource update was excellent

Southern Silver Exploration (SSV.V) has been able to update its resource estimate at the Cerro Las Minitas project after completing an additional 10,157 meters of drilling. These additional meters added a lot of value as the indicated resource increased to almost 134Moz AgEq (consisting of 37.5Moz silver, 35,000 ounces gold, 303 million pounds of lead, a bit of copper and almost 900 million pounds of zinc).

There’s an additional 138 million ounces of silver-equivalent in the inferred category, and of the 138Moz, almost 46Moz are pure silver with the majority of the silver-equivalent consisting of zinc. These results are based on a cutoff grade of 175 g/t silver-equivalent (based on a $75/t operating, smelting and sustaining cost) but even at a higher cutoff grade of 250 g/t AgEq the project would still contain in excess of 200M oz AgEq.

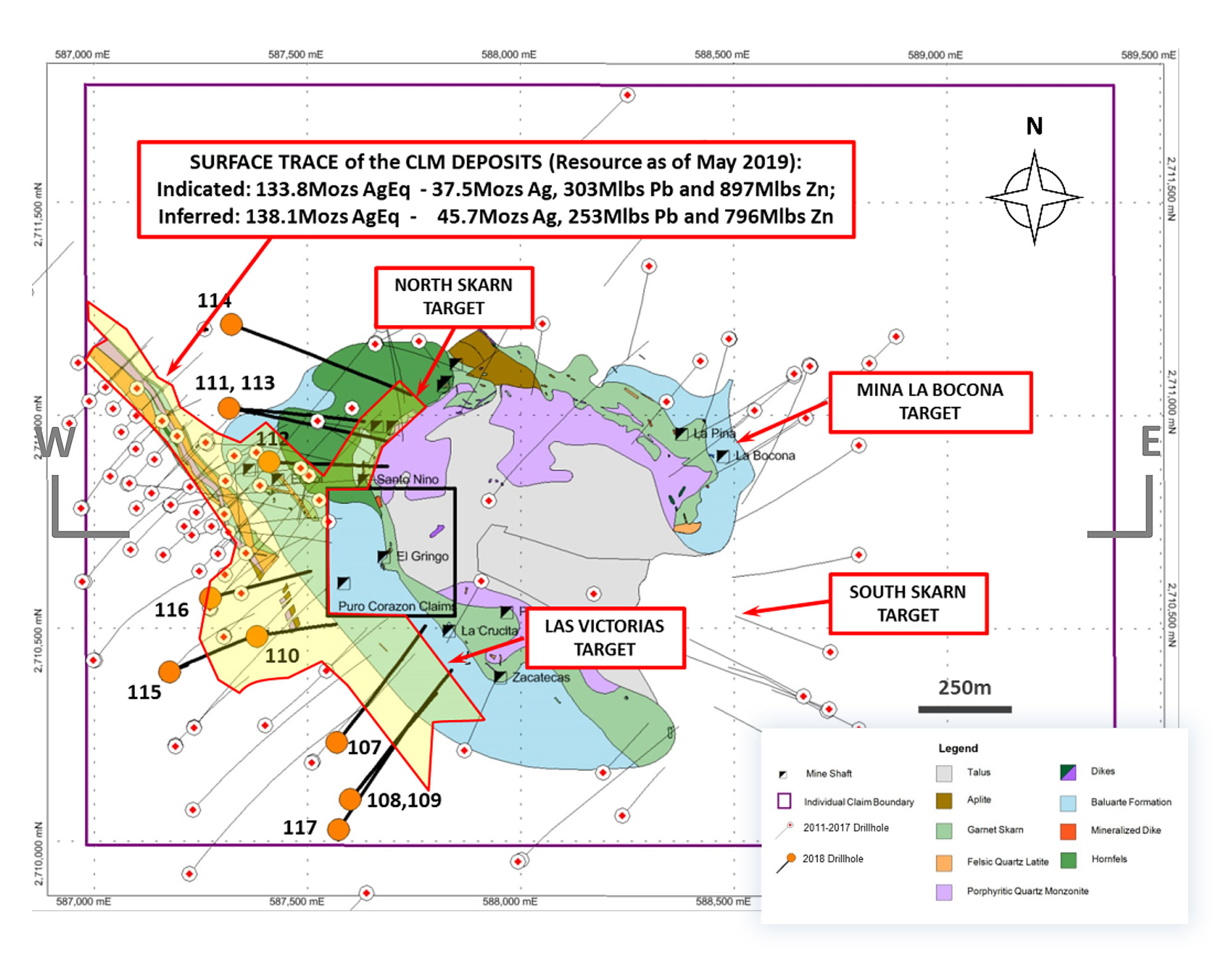

The resource estimate consists of four separate deposits and the newly discovered Skarn Front zone is the main contributor to the updated resource estimate as this zone added almost 5 million tonnes of rock to the overall resource. The relatively low US$2M that was spent in 2018 on additional exploration, resulted in adding 5.1 million tonnes to the combined indicated and inferred resources, and added 63 million ounces silver-equivalent. Definitely a good return on investment!

Based on this updated resource, we can now update our preliminary and very much back-of-the-envelope economic model which we published in 2018. Despite the additional data, our accuracy level will still be relatively low as both different types of the deposit have different recovery rates as the Blind, El Sol and Las Victorias deposits have (slightly) higher recovery rates for silver, gold and lead, but the Skarn Front boasts a higher zinc and copper recovery rate. Additionally, Southern Silver is still working on optimizing the flow sheet to make sure the metals end up in the most favorable concentrate (as explained before, you would want the silver to end up in the lead concentrate as the payability in the zinc concentrate is much lower).

For the upcoming drill program, Southern Silver will continue to focus on increasing the resource base but it will very likely also earmark some budget to pursue new epithermal vein based discoveries like the 3 meters containing 168 g/t silver that was discovered at Cerro Las Minitas West last year.

A caveat

Before we dive into some numbers, we would like to emphasize (once again) that there will be a lot of assumptions and projections in this article. All of these projections will be based on publicly available material, but please keep in mind these are our own calculations and conclusions and should not be seen as an official point of view from the company.

The calculations (and corresponding explanations on how we get to our numbers) are merely meant as a ‘back of the envelope’ calculation to have a first look at the project before Southern Silver publishes its PEA. This report should only be considered to be what it is – assumptions that we deem to be realistic, but not as refined as an official NI43-101 compliant mine plan which could use a different ore sequencing, have different initial capital expenditures and operating expenditures.

The importance of the metallurgical update

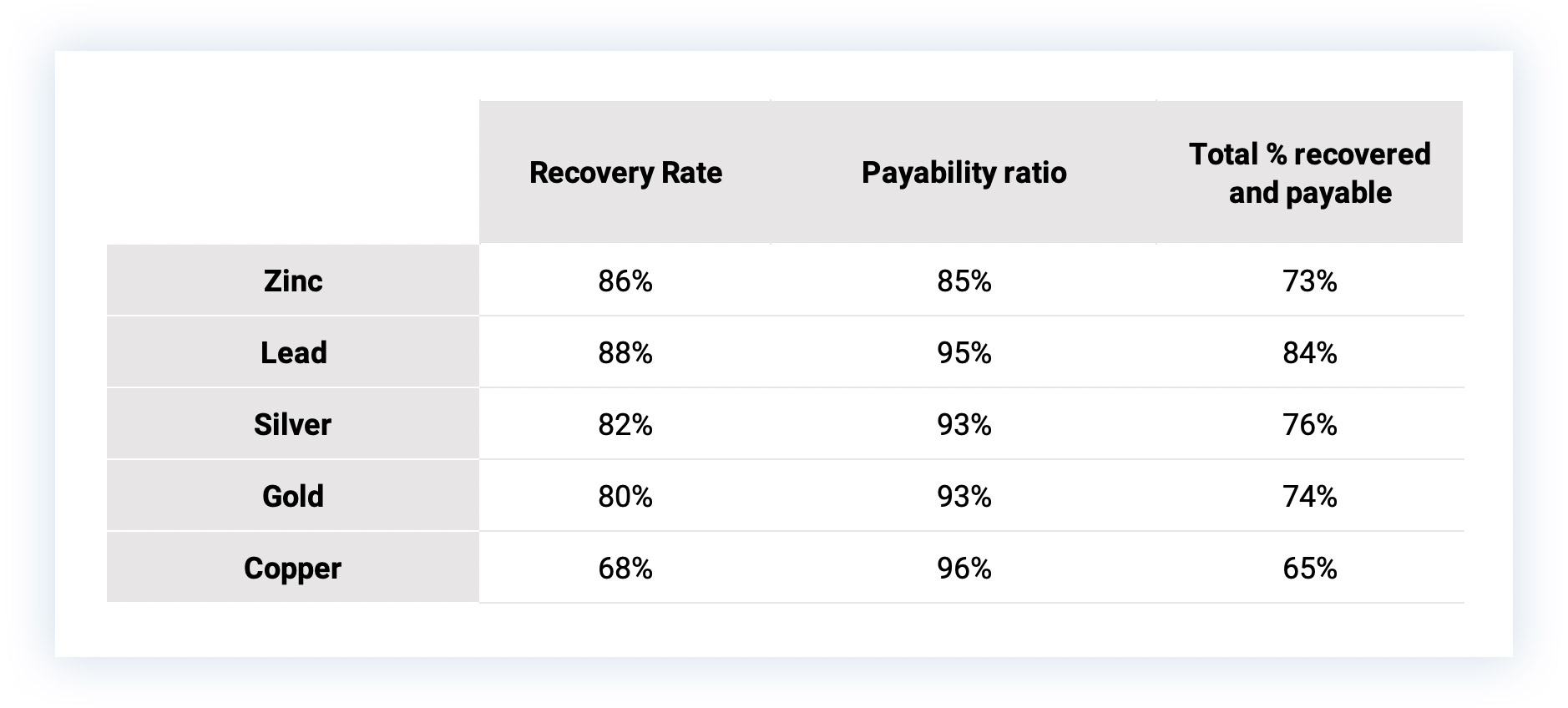

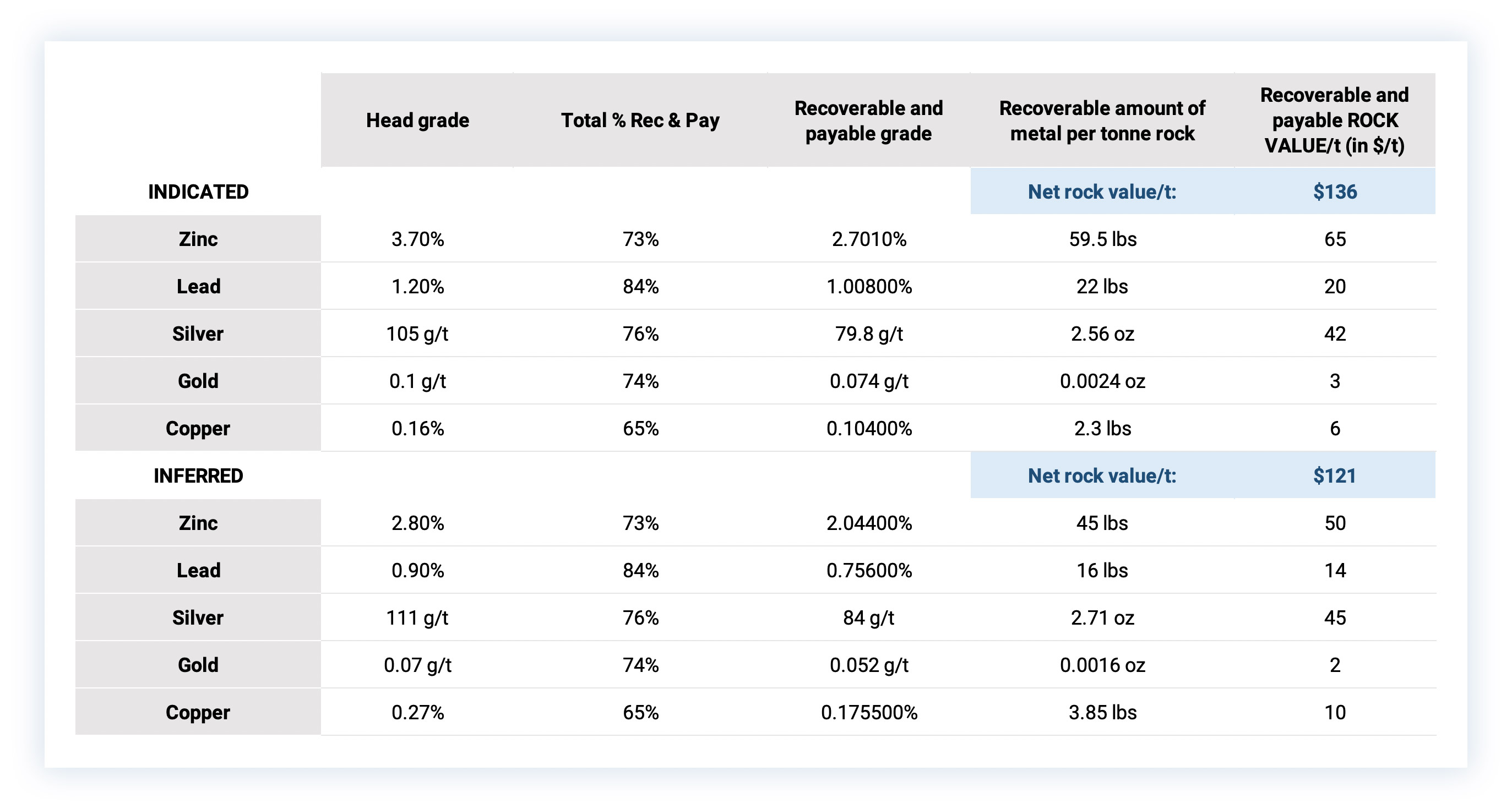

The updated metallurgical test results are actually very encouraging. There are no huge changes in the recovery rates of the lead, silver and gold, but two important elements deserve to be singled out here. First of all, the zinc recoveries have increased by quite a bit: Approximately 89% of the zinc mineralization in the Skarn zone is being recovered into a zinc concentrate while the sulphide zones at Blind – El Sol showed an 78% recovery of the zinc in a zinc concentrate. The weighted average of both recovery rates thus increases to 86% (note, we realize a weighted average isn’t 100% reliable, but it does show you the positive developments on the metallurgical front).

Looking at the zinc concentrate, it looks like there will now be a very small silver credit payable. The average grade of the silver in the zinc concentrate produced from the skarn zone is 111 g/t. For the first 3 ounces of silver per tonne of concentrate, a company doesn’t get paid anything, while the payability ratio is around 70% for the metal above this cutoff grade. This means that per tonne of zinc concentrate, Southern Silver should be able to be paid on 0.7 X 18 g = 12.6 grams of silver. That’s around 0.4 ounces per tonne and just $6/t zinc con at this point. Considering the total indicated and inferred resource, a mine plan would result in the production of approximately 1.2 million tonnes of zinc concentrate. The $6/t will contribute just $7M over the entire mine life, so that’s negligible (also because we just cannot assume 100% of the indicated resources and 100% of the inferred resources will make it to the mine plan, that’s just not realistic at this stage, but exploration if obviously still ongoing). Needless to say, we will not account for this small by-product credit in our assumptions.

Secondly, in the metallurgical test work that was announced, Southern Silver was now also successful in producing a copper concentrate. In our previous back of the envelope model, we didn’t take the copper into account but according to last year’s test work, almost 68% of the copper was recovered in a concentrate with a marketable grade of 27.9% copper. Additionally, approximately 15% of the silver reported to the copper concentrate and that’s important as the minimum deduction for silver in the copper con is just 1 ounce, while the payability of the remainder is 90%. It’s very clear that producing a separate copper concentrate with a high silver content is much more valuable than seeing the silver end up in the zinc concentrate.

And sure, while Cerro Las Minitas doesn’t contain a lot of copper and the 68% recovery rate isn’t that great, it does have the potential to move the needle. The skarn zone contains 103 million pounds of copper in the indicated and inferred resource and after applying the 68% recovery rate and 96% payability, the total amount of recoverable and payable pounds of copper would be 67 million. Assuming a copper price of $2.75, that’s an additional US$185M in net smelter revenue. Sure, the operating costs will also increase a bit by adding the copper flotation circuit and it’s very unlikely every pound of copper will be mined, but more than the increase in the zinc recovery rate, being able to produce a separate copper concentrate could move the needle. Not just on the NPV and cash flow front, but it would also allow Southern Silver to negotiate different offtake agreements with different parties for the copper, lead and zinc concentrates at Cerro Las Minitas.

Putting everything together in a NSR model

Now we have established the percentages of the metals that could be recovered and the percentages of the gross value of the concentrate that will effectively be paid by smelters, we can now work towards establishing a Net Smelter Return model based on the average grades of the indicated and inferred resource categories. We are using the following commodity prices:

Again, these are just averages and in some years the net value of the rock will be higher than in other years. This results in the following net smelter revenue per tonne of rock based on the current resource estimate:

A few interesting observations here. Despite using lower commodity prices compared to our previous model from last year (see below), the higher recovery rates and the addition of a copper concentrate to the product mix (last year, we excluded any potential by-product revenue from the copper), we see a slightly higher NSR in the indicated resource ($136/t versus $132/t last year) and a virtually unchanged value of the inferred resource where the higher silver grade is mitigating the impact of the lower zinc grade.

Just for fun, we also applied last year’s prices on the updated resource estimate, and that would have resulted in a NSR of $144/t for the indicated resource and $127/t for the inferred resource. So a marginal increase of the commodity prices does have a meaningful impact on the NSR.

Using the Net Smelter Returns to complete a back-of-the-envelope NPV calculation

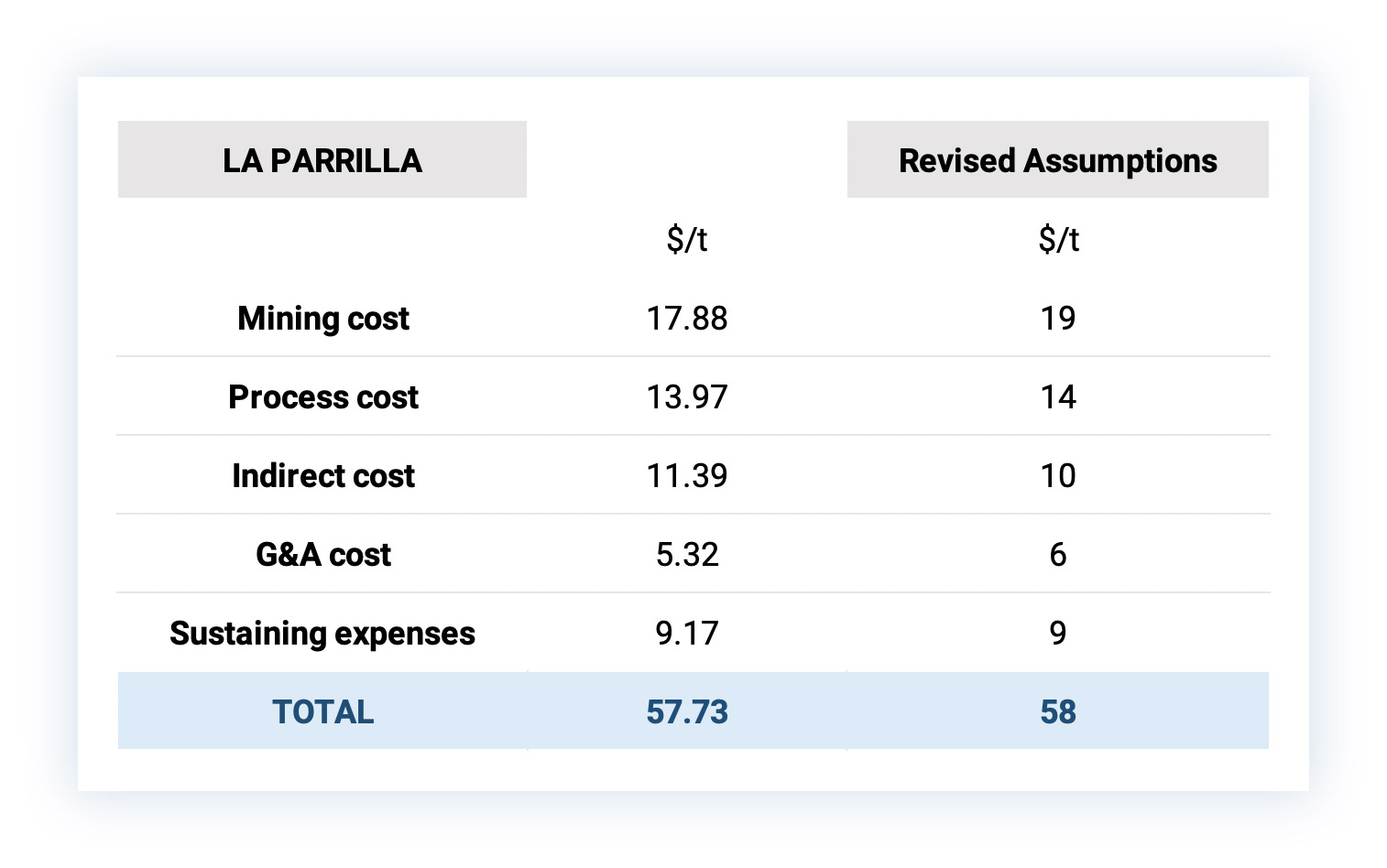

As mentioned last year, the La Parrilla mine owned by First Majestic Silver (FR.TO, AG) could provide a good basis to build an economic model. We are using the results from the 2017 technical report on the La Parrilla mine and have tweaked it a little bit (for instance, the $11/t in indirect costs indicated by First Majestic contain some headquarter-related expenses) so we have reduced this to $10/t, but hiked the G&A expenses to $6/t).

Note these costs are based on a throughput of up to 2,000 tonnes per day. As we will assume a 4,000 tpd throughput in the Cerro Las Minitas Model (due to the higher tonnage in the resource estimate), it would be realistic to assume some economies of scale will take place as well, and the real operating cost could be a few dollar per ton lower. But for now, let’s use $58/t.

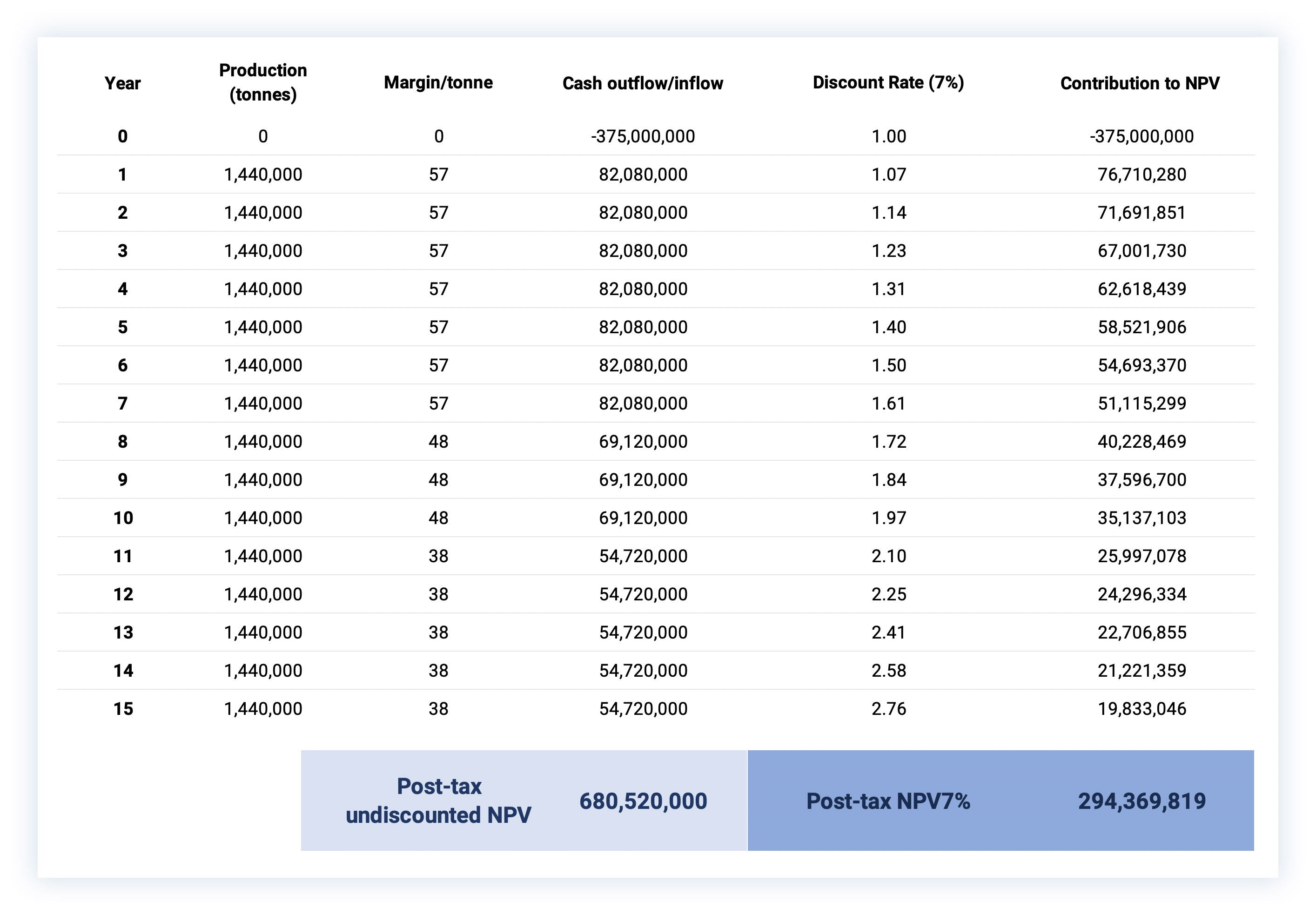

Given the net smelter revenue of $136/t for the indicated resources and $121/t for the inferred resources, the net margins could reasonably be respectively $78/t and $63/t (this is obviously still pre-tax and undiscounted).

In 2018, we used an initial capex of US$280M for a 2,500 tpd mine and processing plant. Considering the recent resource update to 24 million tonnes (in the indicated and inferred resource categories), this may be a bit too low for an optimized mining and processing scenario. As such, a 4,000 tpd mining and milling scenario may be justified (of course this will depend on the mine plan as there are no guarantees the mine could yield 4,000 tonnes of pay dirt per day), and we will assume the initial capex to be US$370M.

Next up: determining a discount rate. Although the company’s name is Southern ‘Silver’, the Silver is just a by-product as 67% of the recoverable and payable rock value in the indicated categories is generated by base metals. Therefore, we will use a weighted average between a discount rate of 5% that seems to be the standard for precious metals projects these days (but too low if you ask us) and the 8% that appears to be common for base metals projects. So, let’s use 7%.

Let’s now assume the higher-value indicated resources gets mined first for the first seven years, where after Southern Silver switches to the lower grade inferred resources for the subsequent 8 years (that’s obviously not a real-life scenario as the mine plan will be based on what’s the most opportune mining scenario rather than categorizing things as indicated and inferred. But as mentioned before, there’s no mine plan yet, so we will just have to work with assumptions here).

Another assumption is to use a 10-year depreciation schedule for the initial capex, and using a total tax pressure of 40% (corporate tax + the specific mining taxes). This means that the total average tax per processed tonne of rock in the first 7 years will be 0.40 X [(1.44Mt X 78/t) – $37.5M) = $30M, or $21 per processed tonne.

For years 8-10, the numbers are: 0.40 X [1.44Mt X$63/t) – $37.5M]= $22M, or $15/t.

For years 11-15 there will be no depreciation allowance and the tax pressure will be 0.4 X $63/t = $25/t.

This results in the following after-tax cash margins per tonne of processed rock:

Years 1-7: $57/t

Years 8-10: $48/t

Years 11-15: $38/t

Using these numbers in a back of the envelope calculation based on an annual throughput of 1.44 million tonnes results in this:

So according to our ‘thinking exercise’, the after-tax NPV7% based on the assumptions and inputs we mentioned before would be US$294M. Southern Silver owns 40% of the project so its attributable NPV7% would be US$118M or C$154M.

Raising C$3.8M to further advance Cerro Las Minitas

Last week, Southern Silver announced its plans to issue 10 million units priced at C$0.20 per unit to raise C$2M to be spent on advancing Cerro Las Minitas to the next stage. The financing is ‘priced to sell’ as it contained a full warrant exercisable for a 5 year period at C$0.25, making it a very appealing ‘kicker’ for people with a long-term vision that are bullish on either the zinc price and/or the silver price.

The financing appeared to be a huge success as the financing was oversubscribed on the very same day and subsequently increased to C$3M.

Additionally, Electrum and another warrant holder have indicated their desire to exercise just over 10M warrants with an exercise price of C$0.08 to add an additional C$835,000 in proceeds to the treasury.

Conclusion

Southern Silver’s exploration programs continue to add value to the Cerro Las Minitas project and the increased resources should make it easier to put a longer term mine plan together. In our calculations, we ended up with an after-tax NPV7% of US$294M for the entire project, and the after-tax NPV7% attributable to Southern Silver came in at just over C$150M.

Of course, there still are a lot of other variables that could change (mine life, capex, throughput,…) so our calculations are and should be seen as a ‘thinking exercise’ in anticipation of the publication of the ‘official’ PEA which is slated for late 2020.

The author has a long position in Southern Silver Exploration. The company is a sponsor of the website. Please read the disclaimer