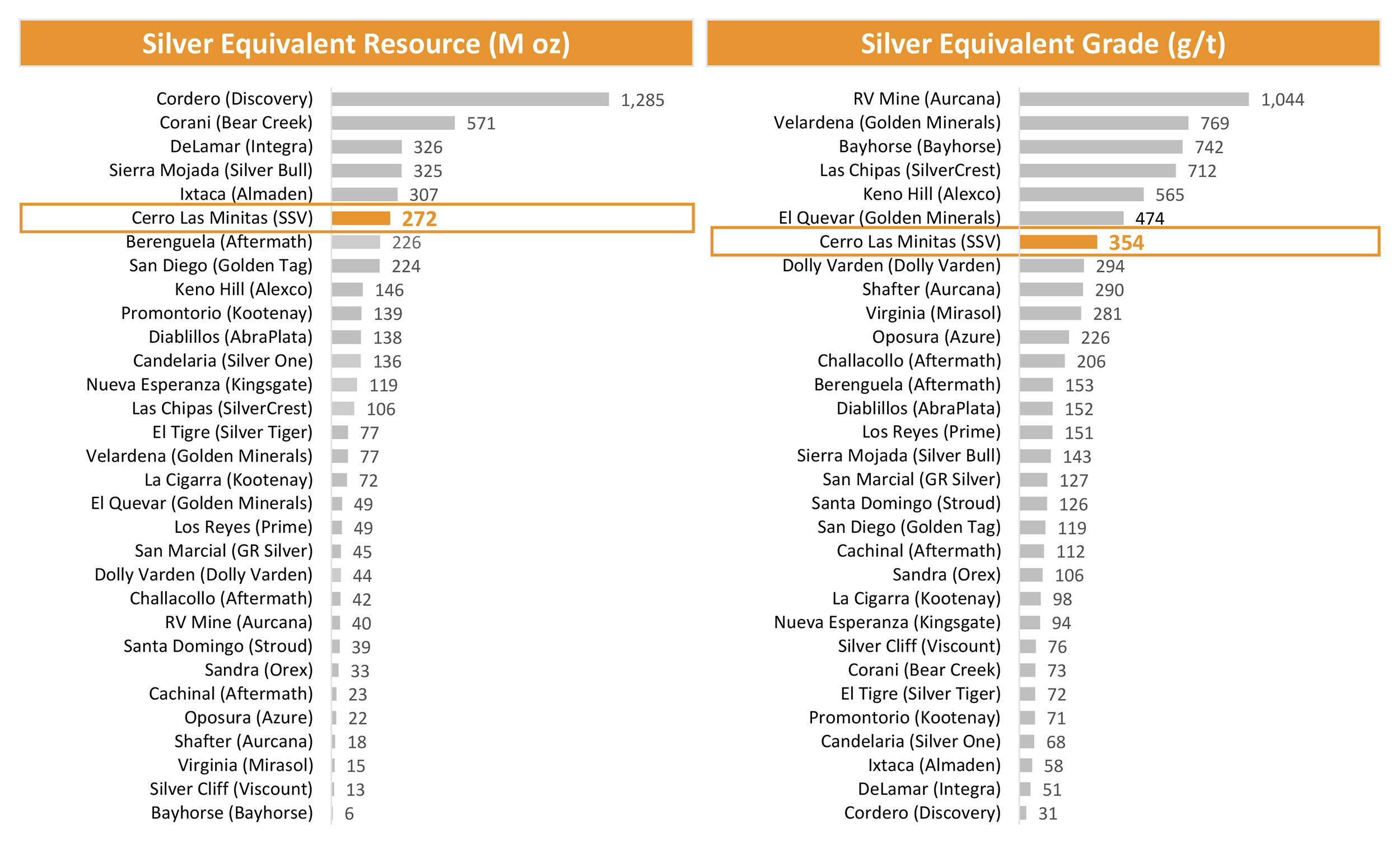

In the mining sector, an outlook or a situation may change fast, very fast. Just four months ago, Southern Silver Exploration Corp. (SSV.V) owned just 40% of Cerro Las Minitas and its share price was trading at just C$0.20 due to the low silver price and uninspiring zinc price. In June, Southern Silver announced it had reached an agreement with Electrum to purchase the 60% of Cerro Las Minitas owned by the latter.

Not only do we strongly believe the company was able to boost its value by securing full ownership of the project (companies with a minority stake in a project tend to trade at a discount), the timing was also absolutely excellent as both the silver and zinc price – the two main metals at Cerro Las Minitas – started moving up with the silver price putting in an excellent performance. That has been a tremendous help for Southern Silver to raise the cash needed to make the initial payment to Electrum, and Southern Silver actually also already has the cash on hand to make all remaining payments. Excellent timing and excellent execution. Now that deal has concluded, we wanted to see how the potential economics of the Cerro Las Minitas project are evolving based on an updated price deck and the updated metallurgical test results announced by the company earlier this year.

Of course, you should only consider our calculations as a back of the envelope calculation where we use parameters we think are realistic and reasonable. The company hasn’t completed any economic studies on the project, our calculations are clearly not the holy grail and margin of error should be applied as our numbers serve for educational purposes only.

The updated metallurgical test work: a very important achievement to optimize the value

Although the purchase of Electrum’s 60% stake is a major achievement, the more important update in 2020 was the updated metallurgical test work, with fresh results announced in January. The success of every mining project in the world depends on how much of the metals can actually be recovered. It’s an integral part of deciding whether or not a mining project has even a chance of being built.

In January, Southern Silver announced the results of an additional met test program which was based on processing almost 211 kilograms of material from 17 drill holes, of which seven samples were put together for a master composite sample of 92 kilos with a representative grade of 111 g/t silver, 0.24% copper, 1.3% lead and 5.8% zinc. This resulted in the following recovery rates and concentrate types:

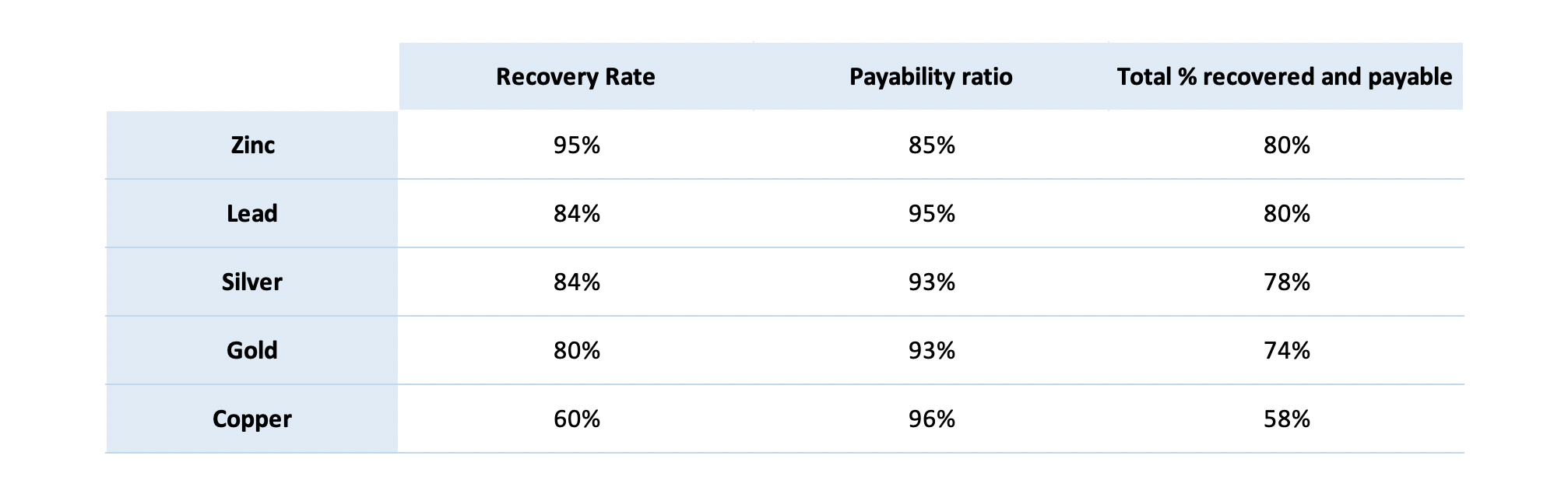

When you’re looking at the metallurgical test results of companies, the recovery rate is just one element you need to keep an eye on. Two other elements that are equally important are the quality of the concentrate (trying to get as few deleterious elements as possible to avoid penalties on the pricing. In Southern Silver’s case the sulfur percentage will be important) as well as the payability ratio. For instance, the silver that ends up in the zinc concentrate will only be payable after the first three ounces. Which means that not a single gram of the silver ending up in the zinc concentrate at Cerro Las Minitas will generate any revenue as the zinc concentrate has a silver content of 92 g/t silver. So it is important to make sure as much of the silver ends up in the copper and lead concentrates to maximize the payability percentage of the metal.

In our assumptions, we are being conservative: we are only using the silver that ends up in the lead and copper concentrate (assuming 0% of the silver in the zinc concentrate will be payable), and we are doing the same thing for the copper that doesn’t end up in the copper concentrate. This results in the following table which includes both the recovery rates and assumed payability percentage.

We see slightly lower recovered & payable percentages for the copper and lead concentrate (as our approach is more conservative last time) but we see a substantial boost in the zinc results (80% recovered and payable compared to 74% in our previous model) and the silver results (78% versus 76%).

An updated NPV calculation

Southern Silver hasn’t published a PEA on Cerro Las Minitas just yet, so we tried to build an economic model ourselves. Please make sure to interpret this section of the update report as a back of the envelope calculation based on our interpretations; these calculations don’t represent the company’s official guidance in any shape or form, so you should take them with as many grains of salt as you wish. We think these assumptions and calculations are very reasonable but of course, the official PEA will be the only study that really matters.

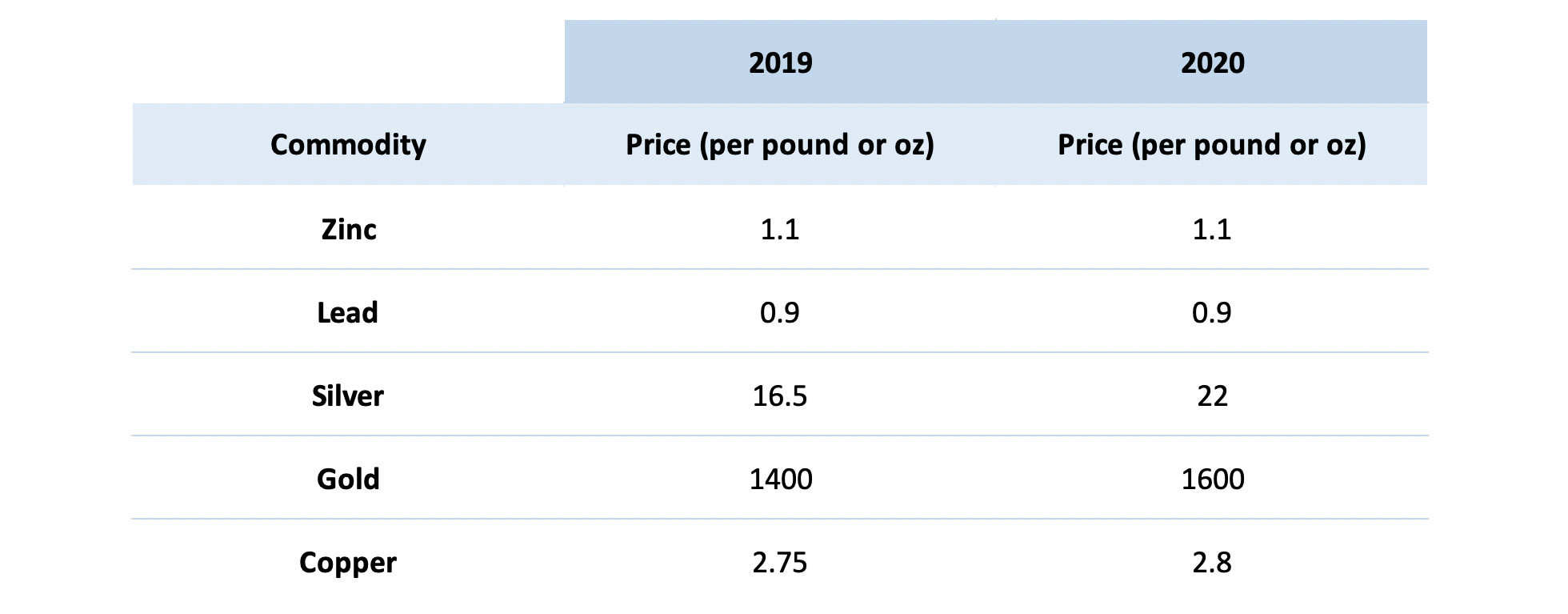

We will be using an updated price deck. Here below you can find the table with the 2019 price deck we used for the commodities as well as the new commodity prices we will be using in the current calculations.

We are indeed using slightly higher silver, gold and copper prices but given the current spot prices which are even higher, we think these are fair pricing assumptions to use given the current precious and base metals climate. When we get closer to the expected publication date of the PEA, we will revisit the calculations using different commodity prices.

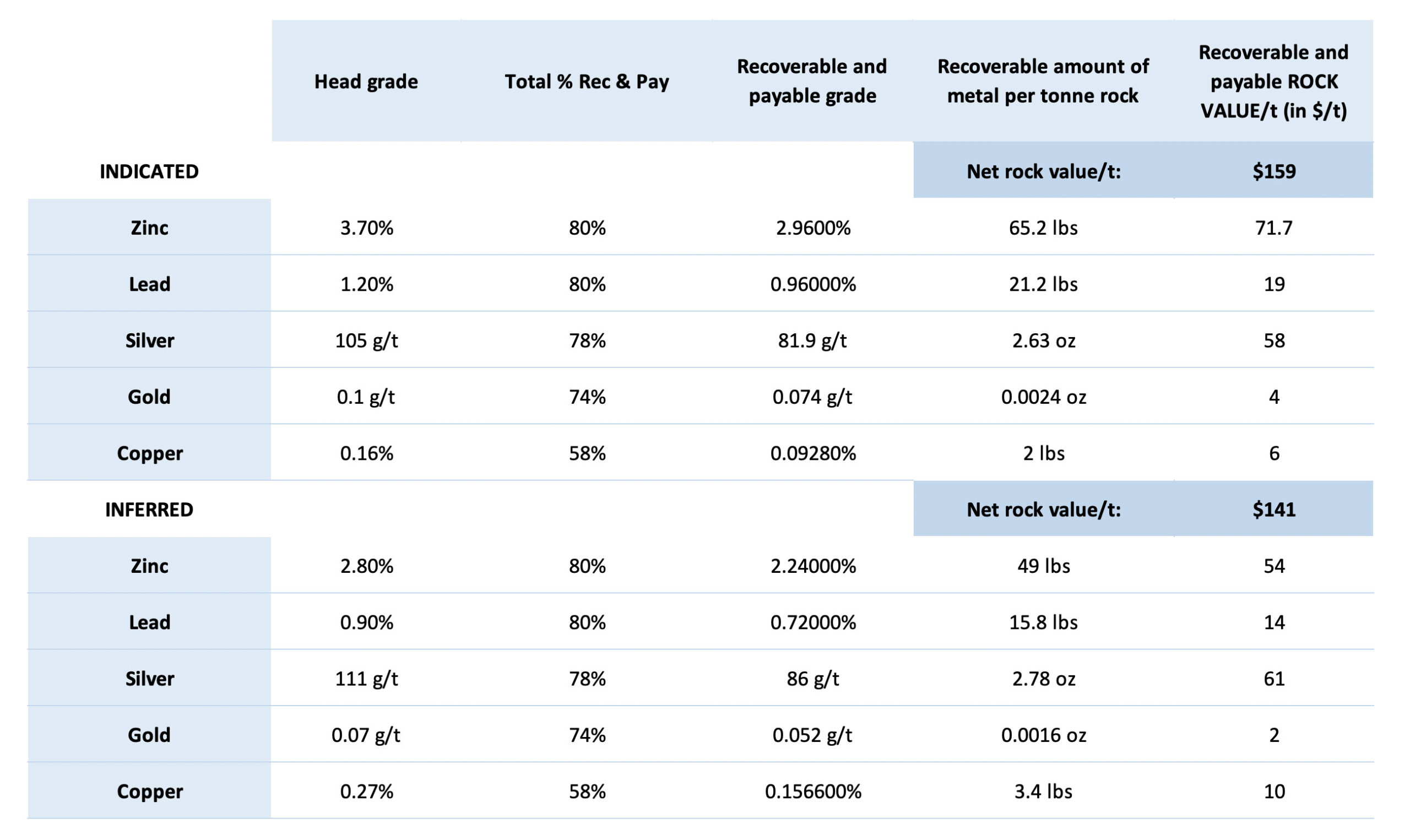

Inserting these prices in the model and applying the recovery and payability percentages results in the following table.

The average net smelter revenue per tonne in the indicated resource category is approximately $159/t while applying the same calculation to the inferred resource estimate results in a net recoverable value of US$141/t. These are nice increases from the $136/t and $121/t we ended up within last year’s calculation.

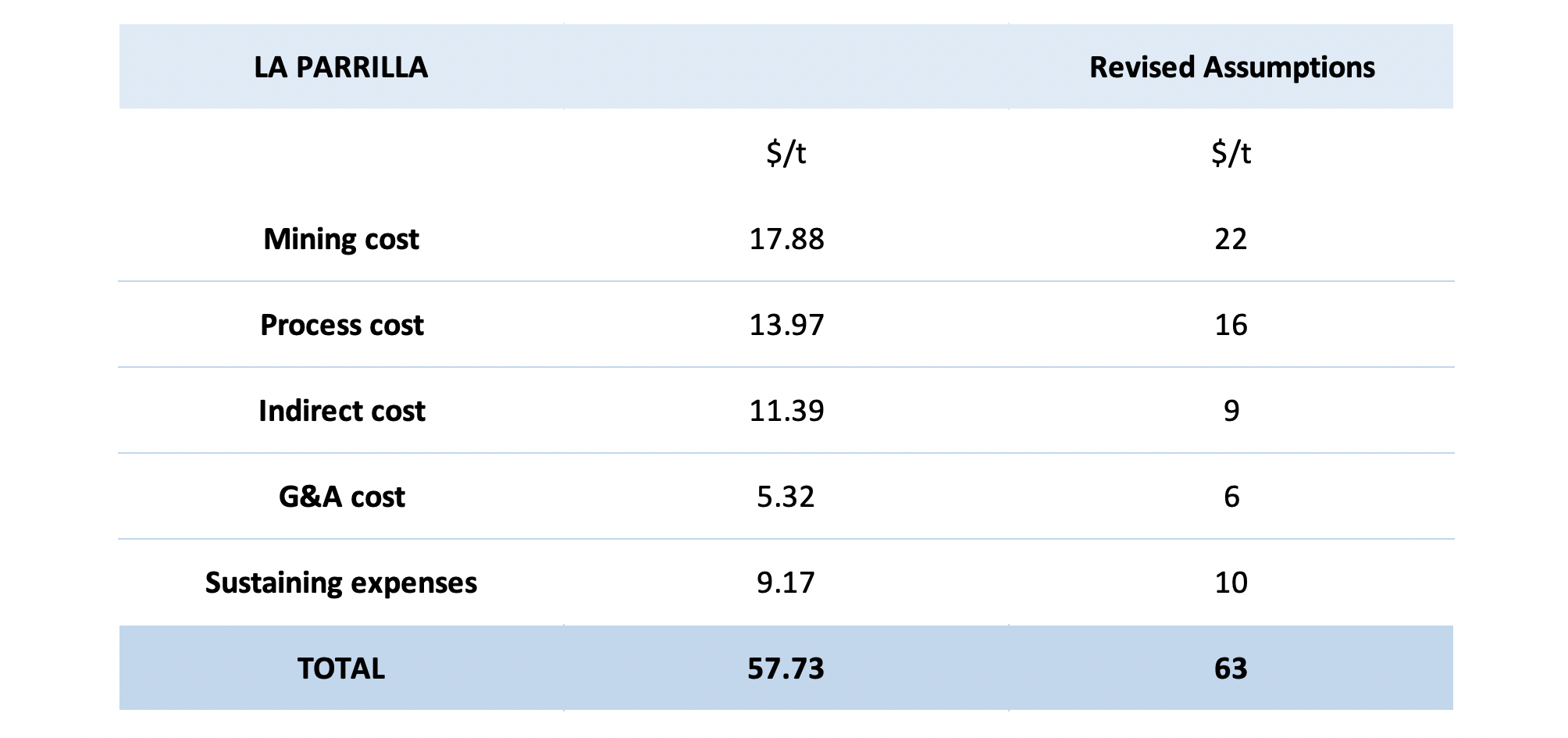

Now we have established the anticipated net smelter revenue per tonne (important: there are no royalties on the Cerro Las Minitas project, so ‘what you see is what you get’) and we will continue to use the data used by First Majestic Silver (FR.TO, AG) in its economic studies on the La Parrilla mine in Mexico. However, to err on the side of caution, we have also tweaked those estimates a bit and will be using a total production cost per tonne which is approximately 10% higher than the economic study released by First Majestic Silver. Perhaps a small sidenote to the table below. We apply a 15% mining dilution to the $17.88/t mining cost estimated by La Parrilla as well as a 2.5% annual inflation since the study was completed. Of course, these are still just assumptions, and we are looking forward to see what Southern Silver’s PEA consultants will come up with.

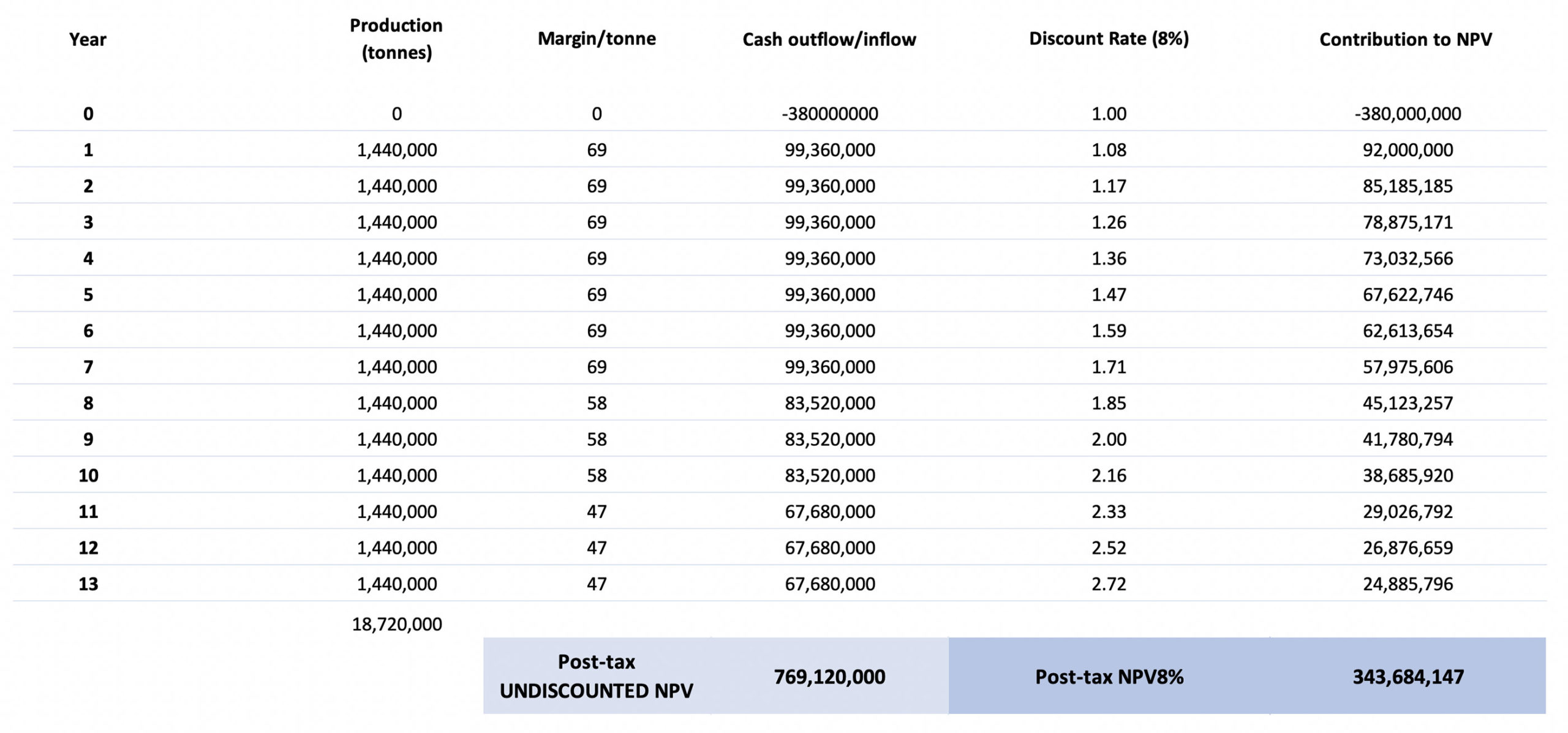

We originally estimated the capex to be US$370M for a 4,000 tonnes per day processing scenario, and to remain conservative and cautious, we will increase this capex estimate to US$380M. Note, the initial capex to develop a mine is the main uncertainty at this point. We could be off $100M in both directions and our 4,000 tonnes per day scenario is an arbitrary assumption. Southern Silver may very well decide to investigate a 3,000 tpd of 5,000 tpd scenario depending on its trade-off studies. We are also increasing the discount rate from 7% to 8% in this year’s economic model.

Given the net smelter revenue of $159/t for the indicated resources and $141/t for the inferred resources, the net margins could reasonably be respectively $96/t and $78/t (this is obviously still pre-tax and undiscounted).

Let’s now assume the higher-value indicated resources gets mined first for the first seven years, where after Southern Silver switches to the lower grade inferred resources for the subsequent 8 years (that’s obviously not a real-life scenario as the mine plan will be based on what’s the most opportune mining scenario rather than categorizing things as indicated and inferred). But as mentioned before, there’s no mine plan yet, so we will just have to work with assumptions here, again, this is just a back of the envelope calculation.

Another assumption is to use a 10-year depreciation schedule for the initial capex, and using a total tax pressure of 40% (corporate tax + the specific mining taxes). This means that the total average tax per processed tonne of rock in the first 7 years will be 0.40 X [(1.44Mt X $96/t) – $40M) = $39M, or $27 per processed tonne. Note; we are using a depreciation of $40M per year as we expect Southern Silver to be able to depreciate some sunk costs. There are no sunk costs right now (as exploration has been expensed rather than capitalized) but we expect the company to start capitalizing certain expenses after the first economic study.

For years 8-10, the numbers are: 0.40 X [1.44Mt X$78/t) – $40M]= $29M, or $20/t.

For years 11-13 there will be no depreciation allowance and the tax pressure will be 0.4 X 78/t = $31/t.

This results in the following after-tax cash margins per tonne of processed rock:

| Years 1-7 | Years 8-10 | Years 11-13 |

| $69/t | $58/t | $47/t |

Putting these elements in an NPV model results in the following calculation:

Based on our parameters, the after-tax NPV8% of Cerro Las Minitas comes in at approximately US$344M, or almost C$460M. Keep in mind this is based on a relatively high capex of US$380M and a mine life of just 13 years (which could be longer if this year’s drill program is successful) and using a discount rate of 8% which is standard for base metal projects. Should the contribution from silver revenues become more dominant, Southern Silver could get away with using a lower cutoff grade as precious metals projects tend to use a 5% or 6% discount rate. That’s why we also provided the undiscounted after-tax NPV of US$885M. And just to be complete, applying a 5% discount rate on these cash flows would be around US$500M.

Although the current resource estimate at Cerro Las Minitas contains almost 24 million tonnes of rock in both resource categories, our model assumes a conversion rate of about 78% of resources into the mine plan. This leaves plenty of upside: SSV may be able to convert more than 80% of the resources into a mine plan, while our calculation also excludes any exploration potential. Should SSV’s 2020 exploration program be successful in adding 3-4 million tonnes to the resource, we can reasonably expect an additional 2-3 million tonnes to end up in the mine plan. But for now, we are considering any resource expansion as icing on the cake.

The next steps

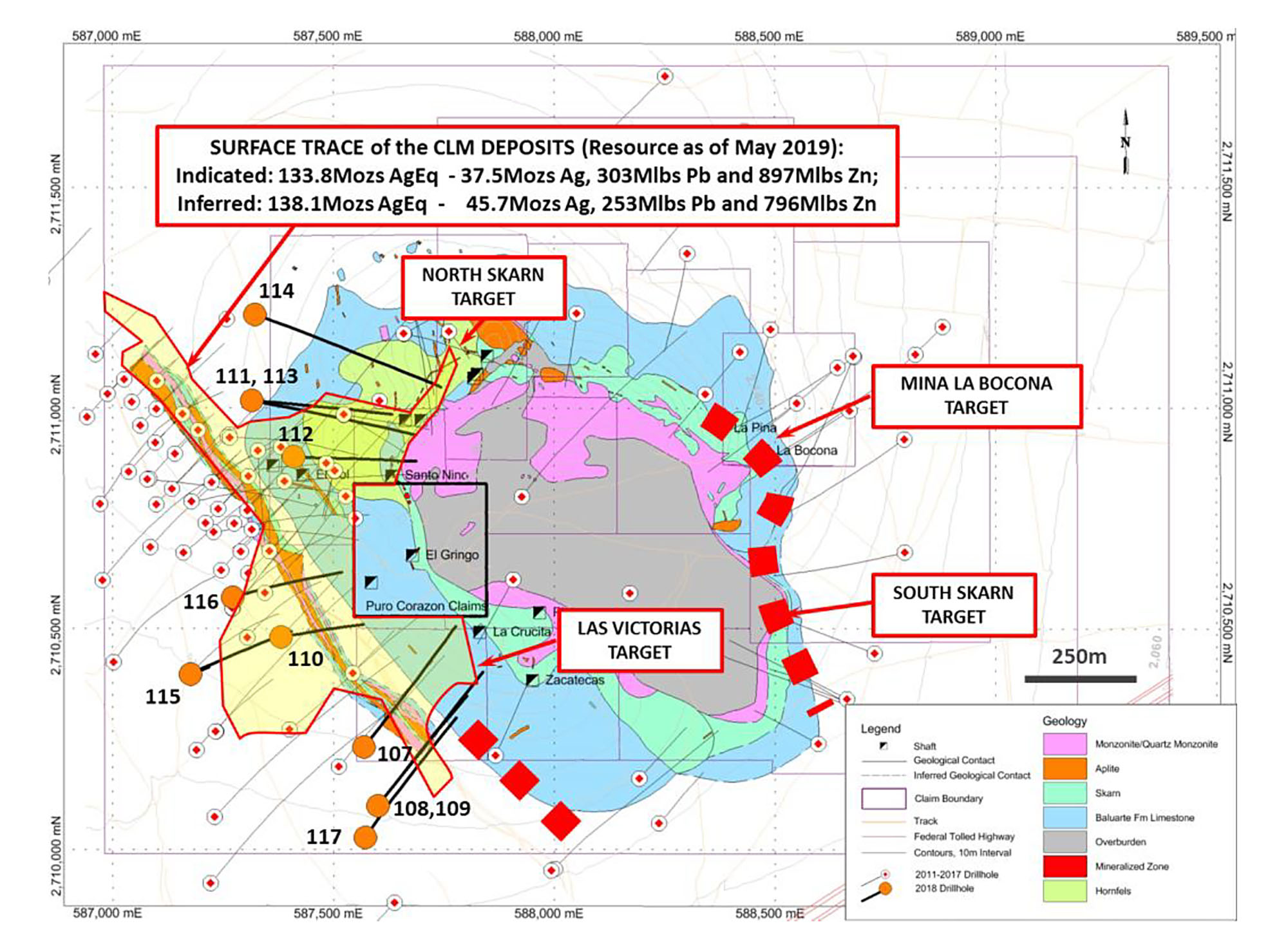

We also caught up with Robert MacDonald, VP Exploration of Southern Silver to discuss the next steps for Cerro Las Minitas. A first drill rig has now arrived on site and will start a 10,000-meter drill program in 20-25 holes in the very near future. This drill program should be completed in the fourth quarter and will be included in the next resource update at Cerro Las Minitas which should be ready by the end of Q4, or early Q1 next year.

This exploration program will drill-test a strike length of 800 meters of the skarn front as well as Bocona zone towards the east of the currently know mineralization. Based on our conversations with the management and the confirmation in the press release ‘new drill targeting […] aims to increase the current mineral resource estimate on the property by approximately 30%’. This means the technical team of Southern Silver appears to be quite confident we will see a total resource of 350 million silver-equivalent ounces across all resource categories. Upon our question whether this resource increase would solely be based on drilling or if the company is planning to update the cutoff grades of the mineralization, MacDonald told us ‘that wasn’t even a consideration’. In that case, growing the resource to about 350 million silver-equivalent ounces would be an excellent achievement with just a relatively small amount of drilling.

The updated resource estimate may not yet be used to complete a Preliminary Economic Assessment which should be ready in the first quarter of 2021, and we are looking forward to compare the official PEA with our own back of the envelope calculations. If Southern Silver indeed reaches that 350M oz AgEq target, our anticipated mine life may be conservative, but let’s see what the drill bit delivers in this 2020 drill program!

Conclusion

The decision to acquire full ownership of Cerro Las Minitas was an excellent decision and on top of that, the timing was excellent as the two main metals of the project, zinc and silver, saw their prices increase as well. Based on a zinc price of $1.10/pound and a silver price of $22/oz, zinc remains the primary metal in the indicated resource category but passes the baton to silver in the inferred category as the zinc grade in the inferred resource is lower.

We ran our numbers using parameters we think are realistic and reasonable and at $1.10 zinc and $22 silver, Cerro Las Minitas will have an operating margin of close to 60% of its revenue, making it one of the more interesting silver-lead-zinc companies out there and we can’t wait for Southern Silver to publish a Preliminary Economic Analysis to see how our numbers stack up against the technical review by the independent consultants.

With C$10.5M in cash on the bank, a bunch of warrants that are in the money and only a relatively small drill program planned for the next few months, we expect Southern Silver to end the year with a very comfortable cash position of around C$6M if no additional warrants are being exercised. Considering there are a few dozen million warrants that are currently in the money, it would be reasonable to expect a bunch of those warrants to be exercised in the next few months.

We will be keeping an eye on the zinc and silver prices as those are the two main metals at Cerro Las Minitas, and will try to finetune our calculations once we get closer to the anticipated publication date of the PEA.

Disclosure: The author has a long position in Southern Silver Exploration. Southern Silver Exploration is a sponsor of the website.