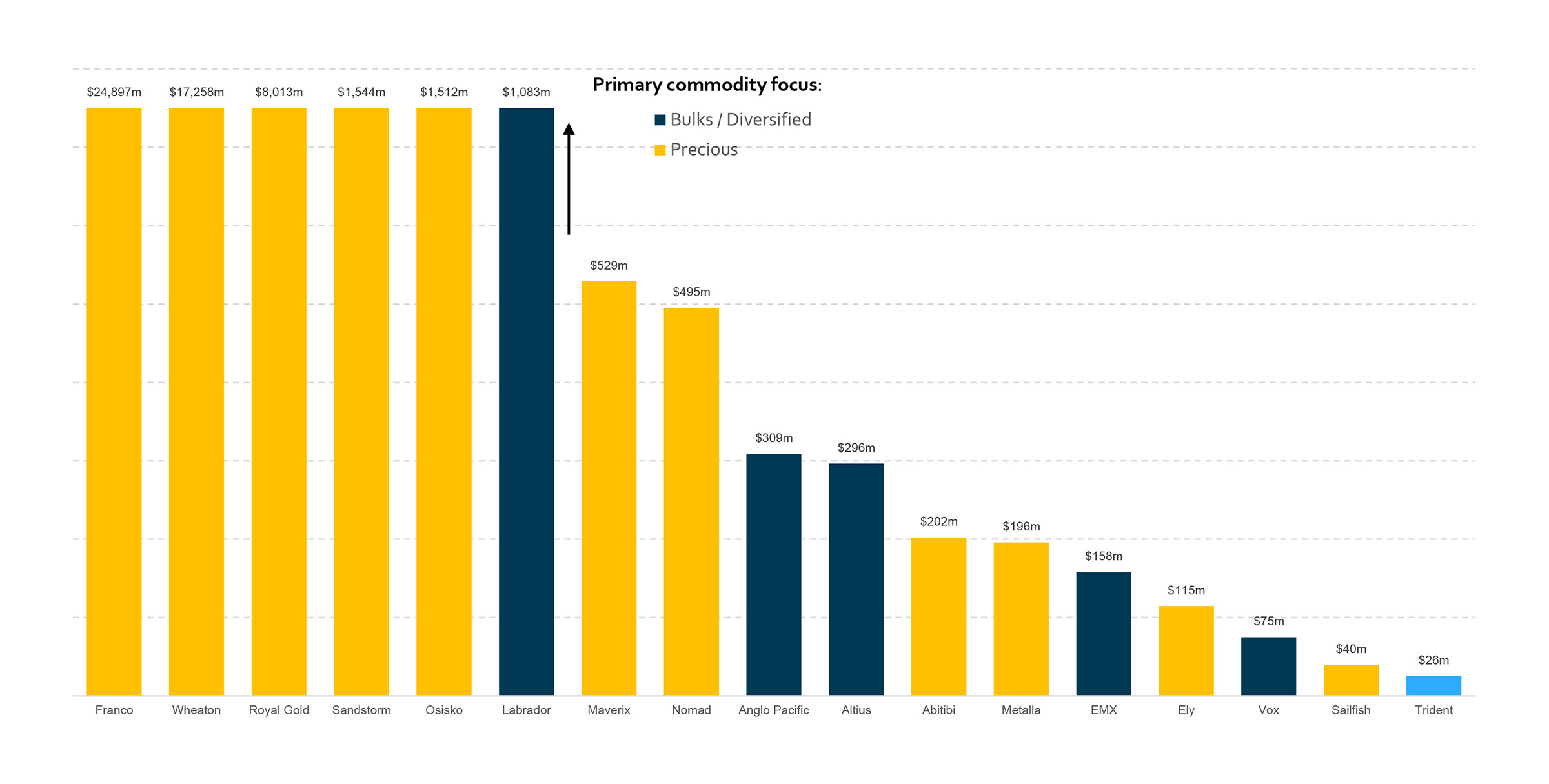

Royalty companies seem to be popping up everywhere these days and as most North American royalties seem to have two things in common (a high multiple to NAV and a specific focus on precious metals), it’s always interesting to look abroad for potential new royalty companies.

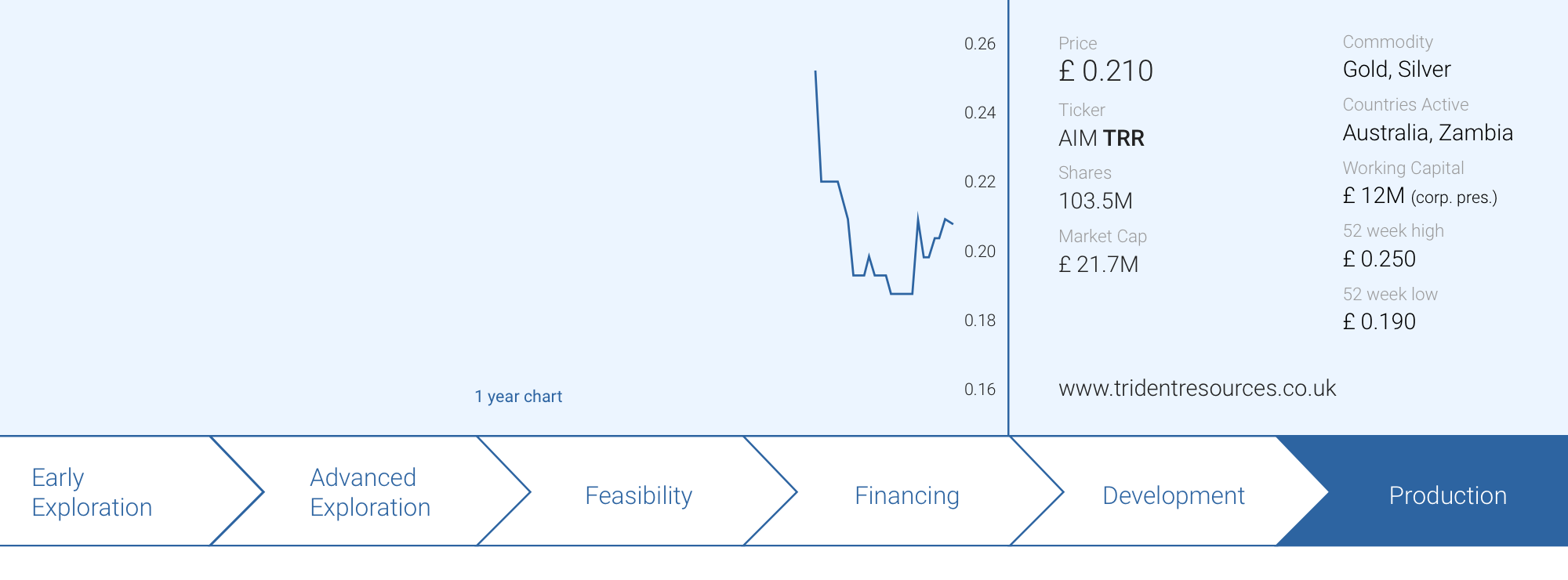

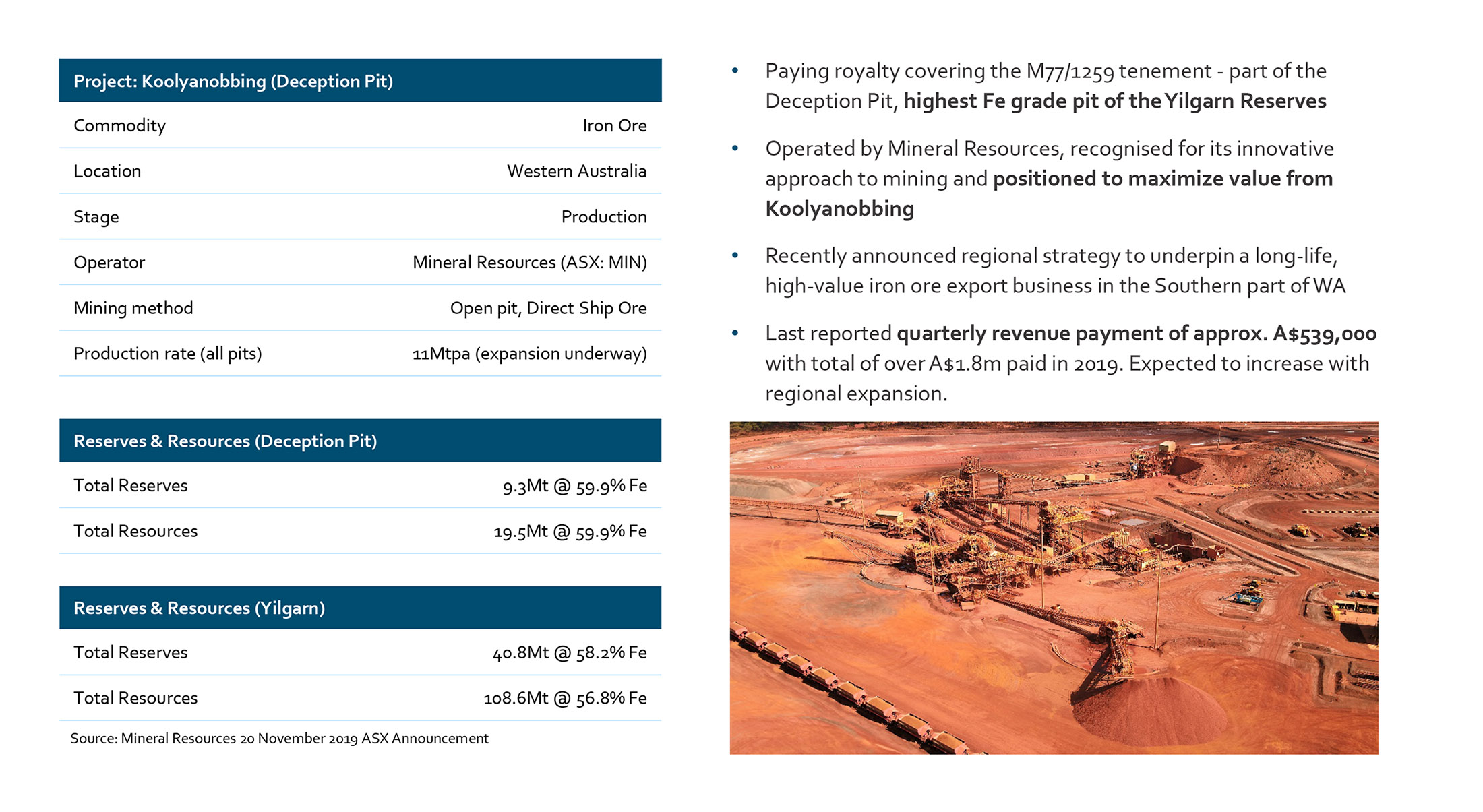

In the first week of June, Trident Royalties (TRR.L) listed on the London Stock Exchange, raising $20M in cash in the process. The placement was conducted at 20 pence and surprisingly Trident’s share price dropped below the going-public price right out of the gate despite having a strong cash backing and one cash flowing royalty on an Australian iron ore asset (a 1.5% FOB royalty on the Deception pit, mined by well-respected Australian company Mineral Resources (MIN.AX)).

We caught up with CEO Adam Davidson to gain more insight on Trident’s business plan.

The recent purchase of the Zambian copper royalty

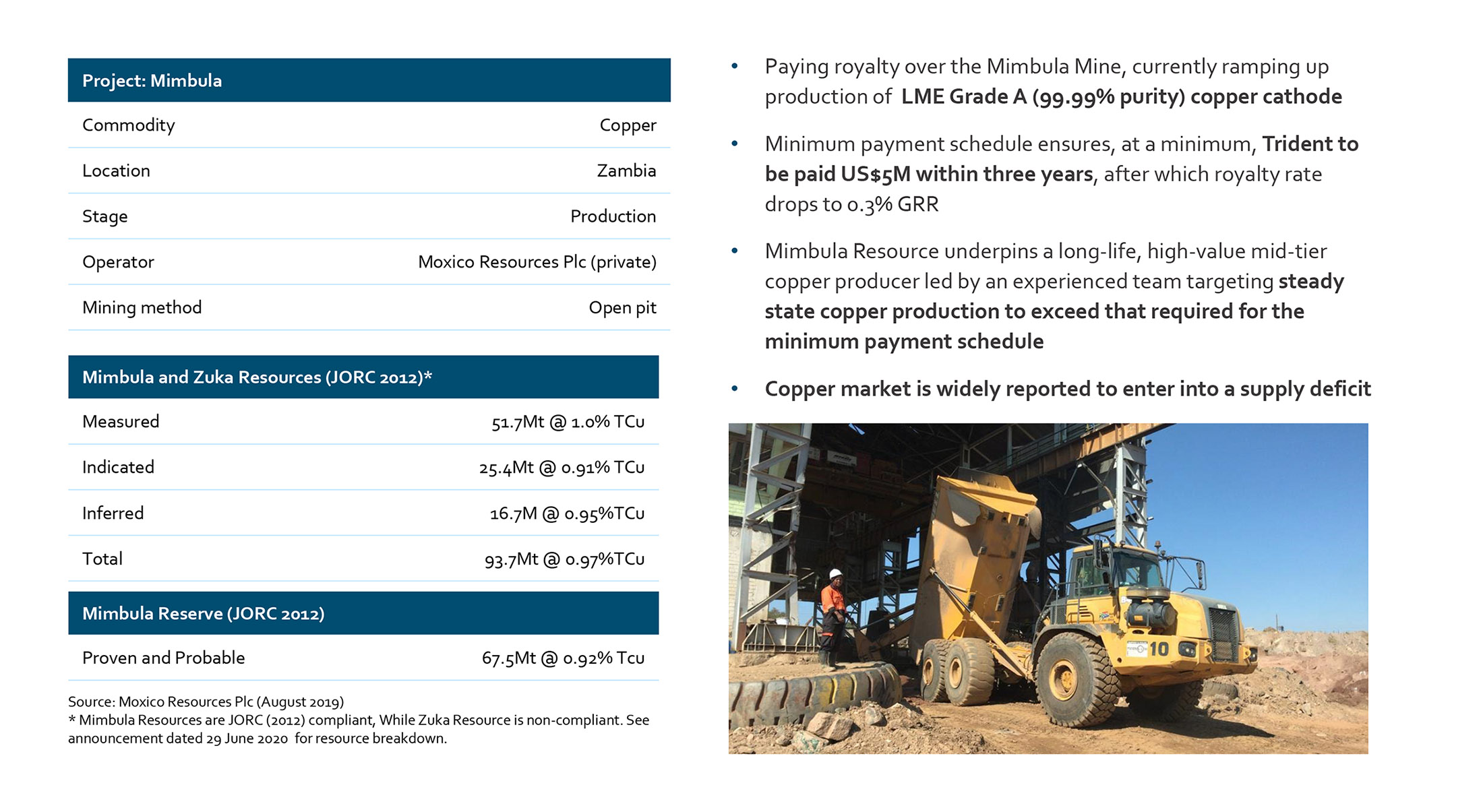

Just last week, Trident Royalties announced the purchase of a second royalty and once again, the royalty appears to be focusing on base metals. Trident purchased a 1.25% Gross Revenue Royalty on the Mimbula copper mine in Zambia for US$5M in cash. Once the initial US$5M investment has been recouped by Trident, the GRR drops to 0.3% until the mine has produced 575,000 tonnes of copper (1.27 billion pounds), where after Trident will still retain a 0.2% GRR. With a total reserve of almost 68 million tonnes at 0.92% copper, the asset has a respectable 1.3 billion pounds of copper to start with, so Trident’s first purchase as a publicly trading company definitely isn’t a ‘mom & pop’ asset but a real mine with real potential.

Although the specific details of this transaction are confidential, a news article published last year provides more insight on the Mimbula mine and if the 2019 numbers are correct, Trident’s royalty should have a very short payback period while the royalty company retains exposure to the mine through the 0.3% and 0.2% GRR.

According to the aforementioned article, the Mimbula mine will produce 30-40,000 tonnes of copper per year. Assuming a normalized production profile of 75 million pounds of copper per year (which is slightly less than the midpoint of the guidance used in the news article) and a copper price of $2.60 per pound, the 1.25% GRR will result in an annual cash flow of $2.35M to Trident Royalties (give or take a few hundred thousand dollars per year as Moxico, the owner of the mine, hasn’t published a detailed production profile). This means Trident can recoup its investment within 2-2.5 years (depending on the effective production rate and copper price), where after it will fall back on a 0.3% GRR.

If we would assume a long-term copper price of $2.80 per pound and a production profile of 75 Million pounds of copper per year, even the 0.3% GRR will bring in just over $600,000 per year for the next 10 odd years. And that makes this royalty acquisition an interesting one as the structure is very different from what we’re used to seeing in North America where payback periods are often over a decade. In Mimbula’s case, the payback period will be very short (which reduces the risk for Trident Royalties) where after the royalty rate will fall off a cliff (-75%). This will allow Trident to recycle its capital and redeploy it elsewhere quite fast while the company retains exposure to potential exploration upside at Mimbula.

A Q&A with CEO Adam Davidson

The Creation of Trident

Trident Royalties, is a new royalty company that recently started trading on the AIM division of the London Stock Exchange. Can you elaborate at how the team came together and how the idea to create a royalty company was born?

Royalties and streams are a space in which my colleague, Tyron Rees, and I have been interested for some time and have had experience given our background in mining-focused private equity. We saw a clear market opportunity for a growth-focused, diversified mining royalty company in a space which is currently dominated by precious metals-focused royalty companies.

With regards to how the team came together, we had experience with the three advisory groups which originally set up the Trident vehicle on the LSE in 2018 – Tamesis Partners, Azure Capital & Ashanti Capital. The advisers shared a similar view of the market opportunity in the royalty space and, through various discussions, asked if we would like to be involved.

Was there a specific reason to list the company in London, considering the team is spread out all over the world?

We are intentionally located in several of the key global mining centers: Perth, Denver, and London. We anticipate that this will provide us with a more diverse pipeline of opportunities, further differentiating us from our peers which are almost exclusively listed on the TSX and are located in North America.

The listing in London is born, in part, by the fact that Trident was originally listed on the LSE before making the recent move to AIM. Perhaps more importantly, we believe there is appetite on AIM for this offering. In addition, AIM is a part of the London Stock Exchange, so is easily tradable in most countries.

What is your anticipated annual G&A cost for Trident in the foreseeable future?

Per our recent AIM Admission Document, our anticipated G&A (prior to deal-related expenses) is circa US$1 million per year, which is very low relative to our peers.

The two assets: iron ore and copper exposure

You listed with a 1.5% Free on Board royalty on the Koolyanobbing iron ore project owned and operated by Mineral Resources (MIN.AX). It’s our understanding your royalty comprises roughly 75% of the Deception pit which has just over 9 million tonnes in reserves and almost 20 million tonnes in resources which is a nice start. You announced your royalty revenue in Q1 (A$0.54M). In your presentation, you mention the royalty revenue could increase due to the regional expansion. How will this regional expansion have an impact on the Deception pit?

As the broader Koolyanobbing operation further increases its annual throughput from a run-rate of 11Mtpa to 15Mtpa, we would anticipate that this is reflected in the level of production being sourced from the Deception Pit – particularly as it is the highest grade pit of the Koolyanobbing operation.

Is there still additional exploration potential at the Deception pit (and more specifically, the tenements you have the royalty on), or will the current resource base be ‘it’?

It is always difficult to predict as, in this case, we aren’t privy to ongoing detailed drill results, etc. However, there is some historic data available from when Cleveland-Cliffs owned the property, which alludes to this potential. In addition, in our value analysis we only include a small portion of the Resource (over and above the Reserve), so there is always the potential for additional Resource-to-Reserve conversion.

Going back to the purchase of the Mimbula copper royalty, we noticed the agreement with Moxico Resources (unlisted) includes minimum payments as your contract also includes mandatory minimum repayments to ensure you can recoup your capital as fast as possible. The total minimum repayments are US$1.5M in 2021, US$2M in 2022 and US$1.5M in H1 2023. Is this a structure you’d like to use in future royalty acquisitions as well? It is an interesting strategy as it basically means the operating company won’t be eternally suffocated by a royalty while Trident recoups its cash within a few years and subsequently benefits from the tail-off of the asset. And if Moxico adds an additional 500 million pounds of recoverable copper to the mine life, you stand to make an additional US$2.8M (using a copper price of $2.75/pound and a 0.2% GRR).

These days, it’s very frequent to include a full or partial buy-back right on a royalty. However, it would be counterproductive for Trident to include buy-back rights as we are in the process of building a portfolio with the intent of providing long-term exposure to our investors. With that context, I think it’s fair to say that both parties found the structure to be suitable – it provides Trident with exposure to the asset in perpetuity, but isn’t overly burdensome to Moxico. That said, it isn’t necessarily a structure that we will always intend to implement, but was appropriate in this particular situation.

Expanding the asset base

Koolyanobbing obviously is just a listing asset and the incoming cash flow will allow you to cover all G&A expenses and your due diligence costs looking for additional royalties to acquire. In a way, it’s very interesting to see your first royalty being an iron ore asset. There already are plenty of precious metals focused royalty companies which are driving up the prices of precious metals royalties as they are all chasing the same type of assets. How will Trident set itself apart from other royalty companies?

You have really touched on a key aspect of the differentiation strategy. It won’t come as a shock that a dollar from an iron ore royalty is the same as a dollar from a gold royalty. However, given the competition in the space, an iron ore royalty can be acquired on much more attractive terms.

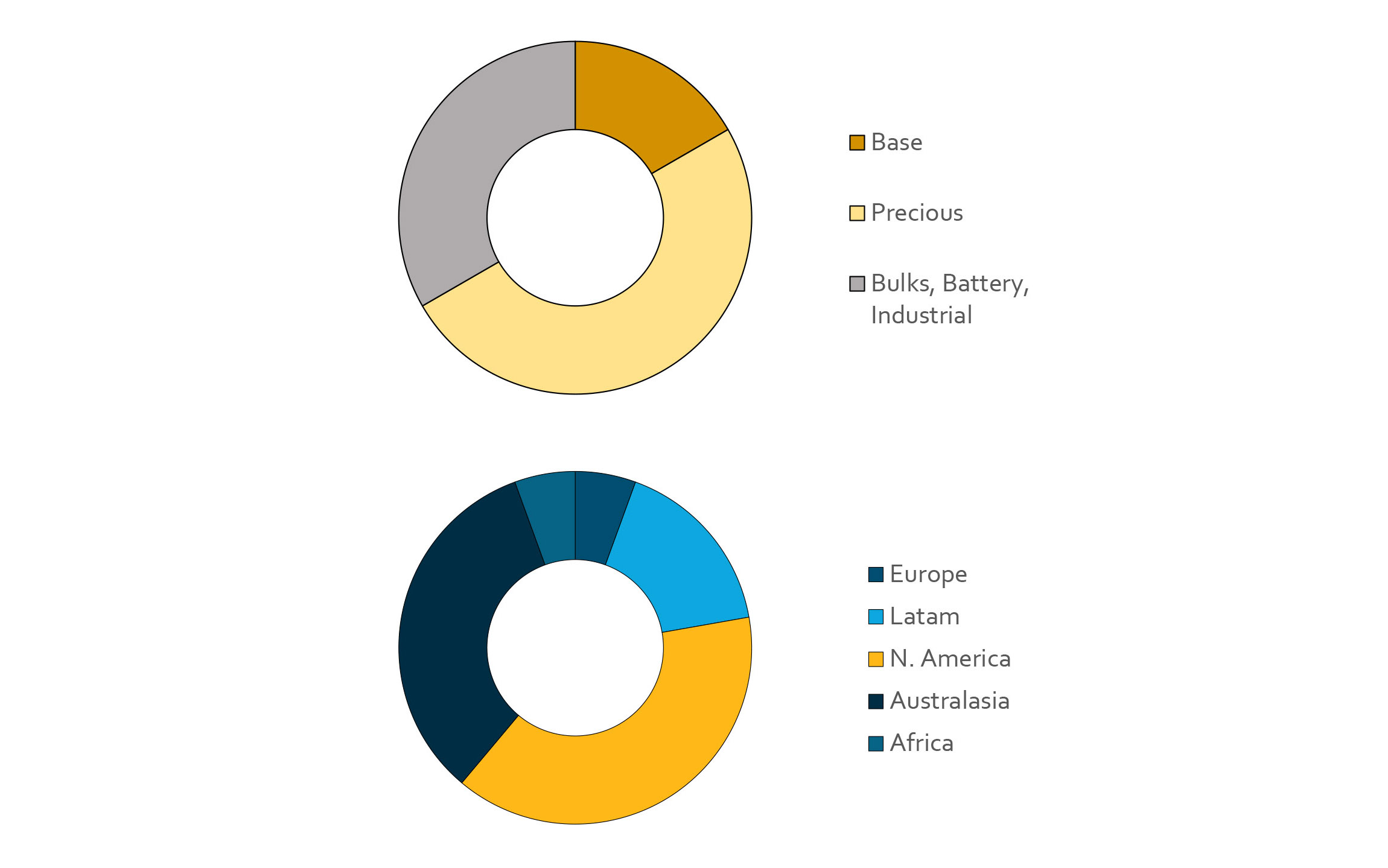

That said, we want a market representative portion of Trident’s portfolio to be in precious metals, as we intend to build a portfolio that is broadly reflective of the mining sector by commodity exposure. However, we will need to be smart in how we acquire them – either focusing on different geographies, assets progressing toward development rather than in production, and/or precious exposure as a biproduct.

Your presentation mentions Trident will be targeting ‘underserviced/unconsolidated jurisdictions and commodities’, which could be your unique selling point. Will you still be selective when it comes to jurisdictions, or are there no ‘no go’ zones?

We’re very open with regards to geography, though we obviously need to price jurisdictional risk into any transaction. And, of course, the legal framework of the jurisdiction must be suitable for a royalty.

A prime example of an “underserviced / unconsolidated jurisdiction” is Australia. Obviously, it is a massive mining jurisdiction but is without a single publicly-listed mining royalty company – despite the fact that there are many royalties in existence which can be acquired (on top of new royalties that can be written). We see a huge amount of opportunity in pursuing geographies which can offer more attractive, accretive royalties for our portfolio.

Do you feel like a focus on base metals could be a unique way to position Trident Royalty? Base metal companies will traditionally trade at lower valuations than precious metals royalty companies but it will be cheaper to acquire the royalties (and Koolyanobbing is a perfect example)?

It is fair to say that building a broadly diversified mining royalty company is unlikely to receive the same valuation as a precious-only company. However, as you point out, non-precious royalties can be acquired on much better terms. The reality is, once the portfolio has critical mass, Trident’s cash flow will speak to its value – so I’m not overly concerned about capturing the same valuation uplift as the precious Royalty Co’s enjoy. As we have demonstrated with Koolyanobbing and Mimbula, there are (largely uncompetitive) opportunities available to us with which to deliver value to our shareholders.

Financing the expansion

You went public with a US$20M raise (16M GBP at 20 pence per share). You made the initial A$3.46M payment for the Koolyanobbing royalty which means you are still sitting on approximately US$17M in cash. Is that a correct assumption?

There was approximately US$4 million in cash in the original Trident vehicle, so after the Koolyanobbing tranche 1 payment, we still had approximately $20 million available to us. After making the subsequent US$5M payment to acquire the Mimbula royalty, we will still have a touch under US$15M in cash on the balance sheet.

The existing cash position could allow you to immediately pursue some smaller royalty acquisitions, but you also have signed a mandate with Tribeca Global Resources for a US$10M debt facility. The debt facility was described as ‘up to’ US$10M in debt, may we assume this will be a target to work towards as you expand your asset base and your initial drawdown allowance will be lower as your only asset is the Koolyanobbing iron ore royalty?

The intent is to utilize the cash-on-hand to build the portfolio such that it will have value from both a security and cash flow perspective to lenders. Once this has been achieved, it will become imminently more achievable to apply leverage to the portfolio, further accelerating equity returns.

In an update released after Trident went public, Tribeca announced that as part of the Paringa Resources failure, it will reduce the credit assets as part of its portfolio to just 20% of the listed company. Does this decision have any impact on Trident and the credit commitment issued by Tribeca’s Credit Fund?

There has been no immediate impact to Trident. Our first step is to deploy the capital that was recently raised, with the debt process to be informed by the royalties and streams that we acquire.

Parting thoughts

At this point, we are charmed by your current market capitalization of just over 21M GBP based on the recent closing price of 21 pence. Considering you have approximately 13.5 pence per share in net cash, early bird investors are basically buying Trident at or slightly below NAV (depending on the Koolyanobbing cash flows). Do you have any parting thoughts to share?

I would encourage potential investors to review some of the recent precious-focus success stories in the royalty space. While we’re focusing on a different mix of commodities – with Trident intending to build a portfolio reflective of the commodity exposure of the global mining sector – I think that the precious guys have laid much of the groundwork with regards to the business model and style of returns which can be achieved for those who invest in the growth stage.

At a certain point, the share price acceleration of these companies flattens as the model shifts from a growth story, to a dividend story. With Trident positioned with two attractive royalties in the portfolio and US$15 million with which to execute on subsequent transactions, we’re at the start of our journey along this growth trajectory – so now is the most exciting time to be a Trident shareholder.

Conclusion

Trident Royalties is a new royalty company, and the company’s management team (consisting of ex-RCF and BMO people) will very likely want to set some precedents with the next few royalty purchases. It’s strange to see the company is still trading at its IPO level and this could likely be explained by the lack of interest in base metals as well as the company having a limited market cap and limited liquidity on the AIM segment of the London stock exchange.

As the company continues to grow, it should outgrow these issues, and with US$15M in cash on the balance sheet and royalty payments coming in Trident’s current two cash flowing royalties are a nice stepping stone to achieve greater things.

Disclosure: The author has a long position in Trident Royalties. Trident Royalties is not a sponsor of the website.