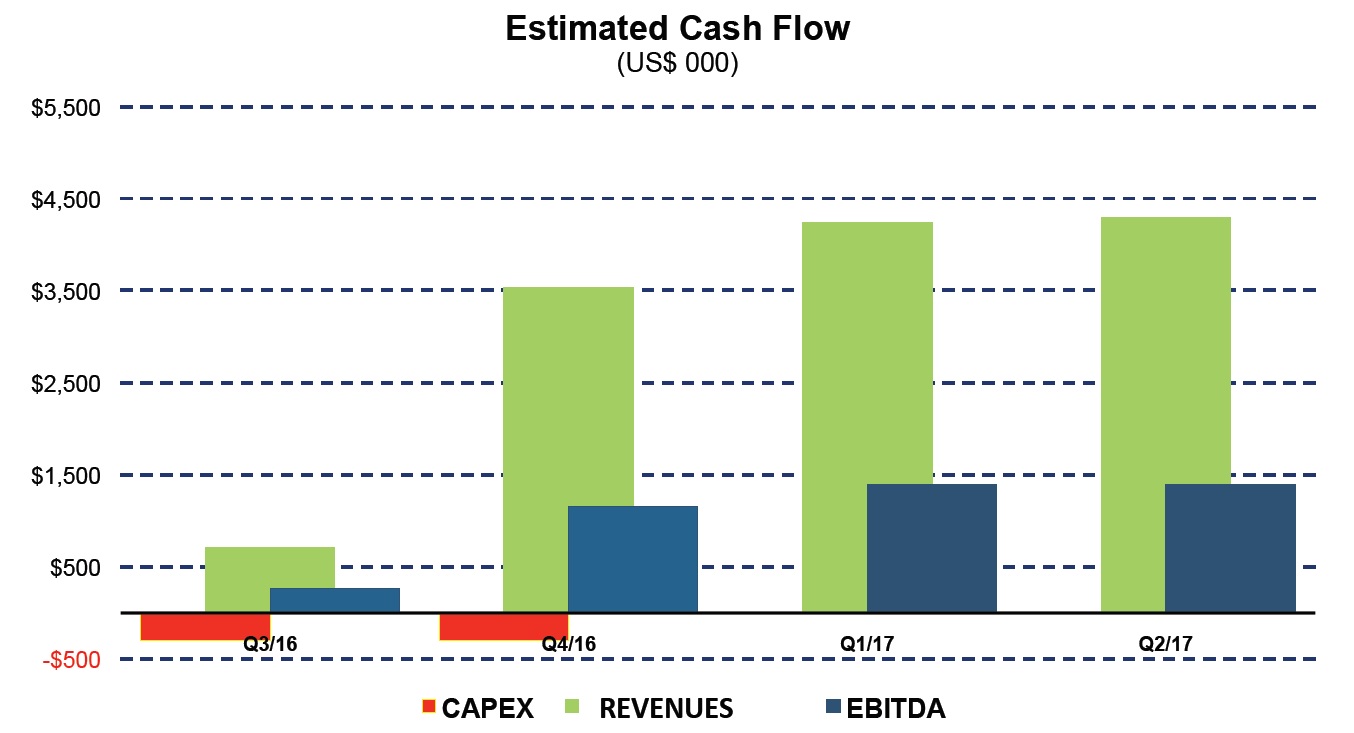

Duran Ventures (DRV.V) has now completed its restructuring and after raising an additional C$1M, this is the newest company in Peru’s milling space. What’s interesting about Duran is the fact the company is completely debt-free and will complete the commissioning of its Aguila Norte processing plant before the end of this year, putting the company on track to generate a substantial amount of revenue and EBITDA.

In fact, Duran is expecting to generate a substantial amount of EBITDA (approximately C$1.5M per quarter on an 80% basis), and this C$6M annualized EBITDA would mean the company is currently trading at less than 1 time its expected EBITDA as it now has just 41.4M shares outstanding (a final tranche of a C$0.09 placement will be closed soon, increasing the share count to somewhere in between 45 and 50 million shares).

Whereas Inca One will continue to focus on the ‘essence’ of toll milling by purchasing ore from artisanal miners and processing that ore at its Chala facility, Duran Ventures’ plan consists of moving to a steady supply of its ‘own’ ore as fast as possible, and the company wants to source 100% of its ore from properties it either owns or will own the mineral rights on.

Duran will own an 80% ownership interest in the Aguila Norte processing plant after having spent C$1.5M on capital expenditures to get the plant up and running with an expected nameplate capacity of 100 tonnes per day. This will just be a first step, as the company has already initiated ground preparations to add more ‘modules’ to the existing plant, to take the capacity up to 350 tonnes per day in the not-so-distant future. At that time, the tailings facility will very likely also have to be upgraded, as the initial size of the tailings will support a ‘processing life’ of approximately 3.5 years.

What’s a key feature is the fact the Aguila Norte plant won’t be just another gold toll mill, as the plant will be able to recover base metals as well (and we would expect the company to focus on the several silver-lead-zinc occurrences in the wider region). Another key feature is the fact the company doesn’t want to rely and depend on artisanal miners, and secure its ore feed by locking up the mineral rights of mining properties.

A first important step has been completed when the company entered into a mineral assignment agreement in May of this year, which basically gives it the right to mine, extract and process the ore from the Chucara property which is located in the La Libertad gold mining district. As of right now, small artisanal miners are already mining on the property and this will supply the Aguila Norte plant with mill feed. The company expects to receive 1,000 tonnes per month from Chucara before the end of this year, increasing to 1,500 tonnes per month from early next year on. This means 50% of the total capacity will already be provided by the company’s ‘own’ mining projects.

And Chucara isn’t just ‘a project’. Duran Ventures took 23 samples and the average grade of these samples was almost half an ounce of gold per tonne, 13 ounces of silver per tonne and in excess of 11% Zinc-Lead, and we wouldn’t be surprised if the by-product credits of this type of ore would cover the entire mining and processing cost, which could lead to outsized margins on the gold production.

This short article is by no means a comprehensive review of this company, but we would like to draw your attention to Duran Ventures as the company is getting ready for an action-packed final quarter of the year. We will follow up on this blog post with an in-depth review in one of our next reports.

Fully-funded and debt-free Duran Ventures will, together with Inca One Gold (IO.V), be one of the last company’s standing in Peru’s toll milling sector. As the company is debt free, an EV/EBITDA target ratio of 5 would indicate a fair value of C$30M for the company, rather than the C$4.5M it’s currently trading at, but we realize that after Standard Tolling (TON.V) went belly-up and Anthem United (AFY.V) decided to pursue other interests (even though the company emphasized the milling space makes economic and strategic sense), it will take some time to convince the market.

Duran is ready to hit the ground running and we would expect to see numerous operational updates in the final quarter of this year, as the company is building a platform to reach its annualized C$6M EBITDA as fast as possible.

Go to Duran Ventures’ website

The author is participating in Duran’s current financing. Duran isn’t a sponsor of the website yet, but will be one in the near future. Please read the disclaimer