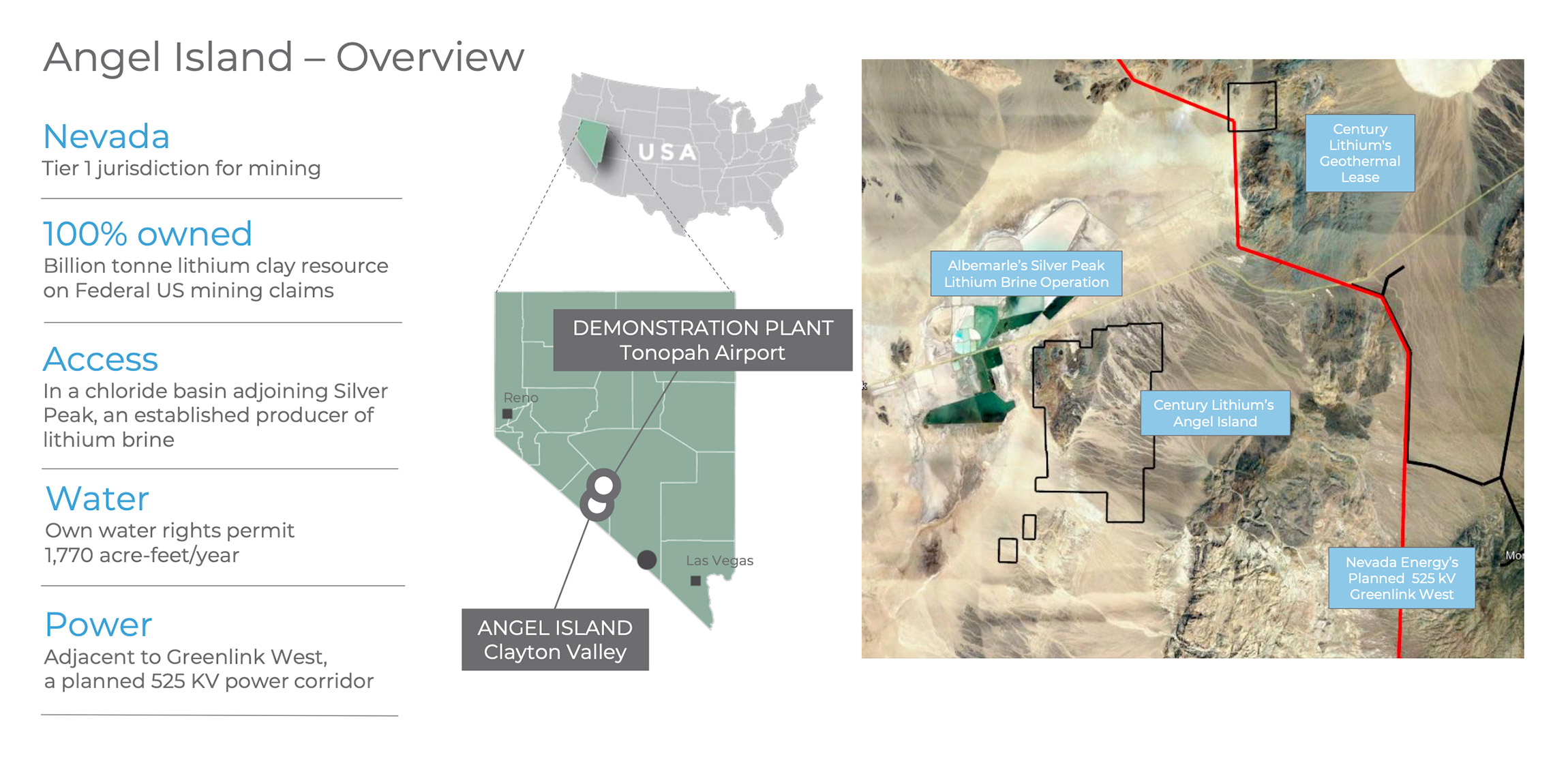

In the past few years, Century Lithium (LCE.V) has been working diligently on improving the 2024 feasibility study on its flagship Angel Island lithium project in Nevada. While that study yielded a positive NPV and IRR, it fell a bit short of the expectations and combined with a weakening lithium market, Century Lithium couldn’t get any traction.

Rather than remaining idle, Century’s management team had good ideas how it could improve the feasibility study and this culminated in the new study. While we are waiting for the full technical report to be filed, the initial breakdown provided by the company already provides plenty of data to dig into.

The updated feasibility study: a lower capex is key

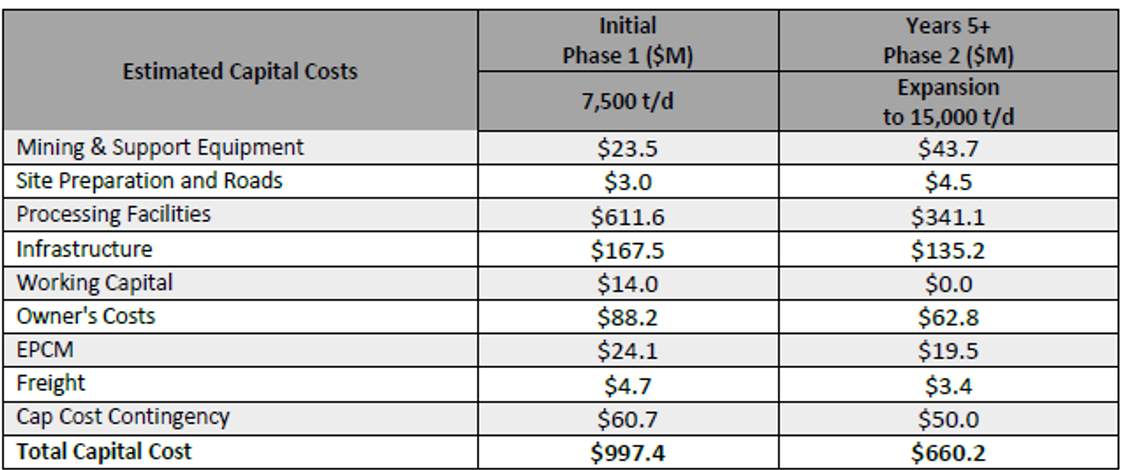

Some of the key elements we wanted to see an improvement on were the initial capex and the operating expenses. Bigger isn’t always better, and in the updated feasibility study, the Phase 3 expansion has been removed. The first two stages remain unchanged with an initial throughput of 7,500 tonnes per day, increasing to 15,000 tonnes per day upon completing the Phase 2 expansion.

This initial capex is now expected to come in just below $1B (at $997M), including a 6.5% contingency estimate. And as you can see below, the capital intensity is much lower to double the throughput to 15,000 tonnes per day in the phase 2 expansion: the additional capex requirement is just $660M bringing the total capex to $1.66B for a mining scenario that envisages an average output of 26,500 tonnes per year of battery-grade lithium carbonate.

And while the third phase expansion was removed from the current feasibility scenario, it goes without saying that scenario could be on the table again after successfully completing the Phase 2 expansion. But that’s a bridge that would only be crossed in a decade or so. In any case, the optionality exists, underpinned by a 60 year mine life based on the current reserves at a 15,000 tonnes per day throughput.

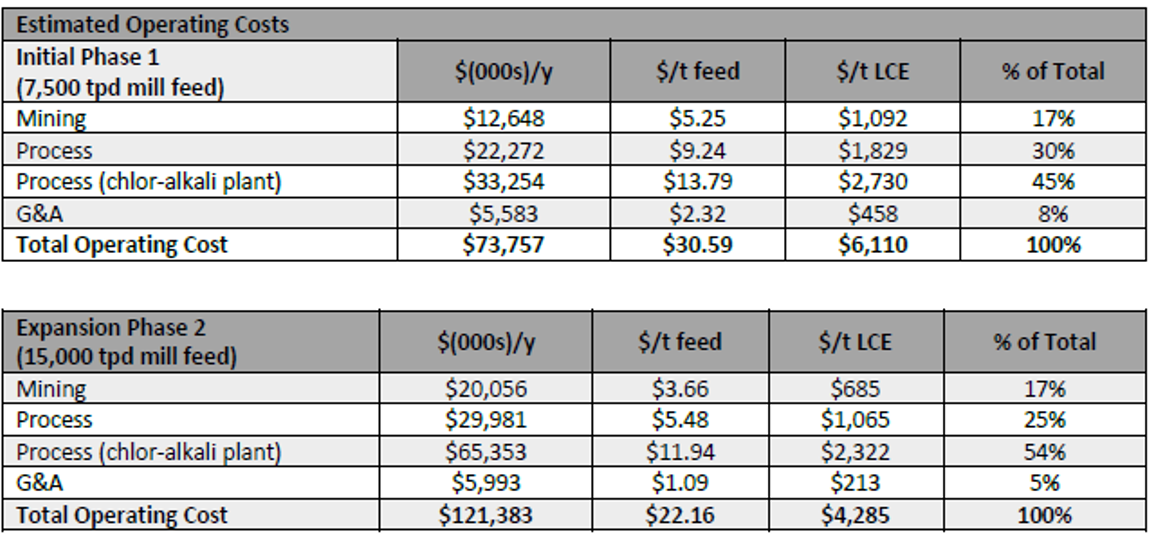

The substantial capex reduction is a very important element that helped to boost the economics. But the continuous focus on improving the flow sheet and refining the mining sequence has also benefited the operating expenses.

Whereas the operating cost comes in at $6,110/t LCE in the 7,500 tpd scenario, this drops dramatically to less than $4,300/t LCE in the expanded scenario.

That is a substantial cost saving versus the $10,390/t and $7,970/t respectively in the 2024 feasibility study and a very clear improvement.

But there is more. The processing phase will unlock the production of sodium hydroxide as a by-product. The 2026 study assumes a sodium hydroxide price of $750/dmt, compared to $600/dmt in the 2024 study (both numbers are on a FOB basis). Sodium hydroxide sales are projected to generate just under $5,400 in by-product revenue per tonne of of lithium carbonate, enough to more than cover direct operating costs in the 15,000 tpd production plan.

We are looking forward to seeing the detailed technical report to gain more insight in the sodium hydroxide market, its size, pricing and what percentage of the demand Century Lithium could provide with its 190,000 tpa production (based on the 15,000 tpd processing scenario).

The feasibility study offers a base case scenario using an LCE price of $24,000/t, resulting in an after-tax NPV8% of US$4.01B (approximately C$5.5B at the current exchange rate) and an after-tax IRR of 27.4%. Good results, and especially the ‘profitability index’ (NPV versus capex) of 4 is an exceptionally robust result.

The sensitivity analysis above also clearly shows the project remains economic at lower lithium prices. Using $18,000 per tonne of LCE, the after-tax NPV8% would still be $2.7B and in the positive scenario using $30,000/t LCE, the after-tax IRR jumps to 32%.

The relatively minor fluctuations despite applying pretty severe 25% swings in the lithium price are mainly thanks to the very low production cost due to the sodium hydroxide by-product credit. In fact, using the company’s pricing and volume assumptions, even if the LCE price would drop down to $10,000/t again like in the second half of last year, the project would still generate $265M per year in operating cash flow on the mine level. And although Century Lithium would still have to cover sustaining capex, interest payments and taxes, the company would still be free cash flow positive in that scenario. The sodium hydroxide production is an important element that very clearly enhances the project’s economics.

What’s next?

This is a good study, and even better than we had anticipated after the initial results in 2024. The reduced capex is important, but the reduced opex and substantial sodium hydroxide by-product credit are really moving the needle here and we cannot emphasize the importance of a very low (or negative) production cost per tonne of LCE.

With the second feasibility study now confirming the economic viability of the project, the focus should now shift towards permitting. That’s also the recommendation of the independent consultants that completed the feasibility study. Century Lithium should complete and file a Plan of Operations with the Bureau of Land Management to kick off the National Environmental Policy Act process. Concurrently with this federal trajectory, the company should start the local state-level permitting process as well. And let’s not forget the project was awarded the FAST-41 status, which is intended to improve transparency and streamline the permitting process.

Meanwhile, additional technical work should be completed on the project to for instance support the tailings storage facility design. Additionally, it is recommended to start working with NV Energy to work on connecting the project to the electrical grid and to drill a few water wells (on the land where the company has already established its water rights) to complete pumping tests to determine flow rates and requirements for the Phase 1 and 2 development of the Angel Island lithium project.

A recent appointment

Earlier this quarter, Century Lithium appointed Cormac O’Laoire as Strategic Advisor to the company. O’Laoire, a Ph.D. based in Hong Kong, is an expert in the lithium-ion battery ecosystem with about two decades of experience in the mining, refining and technology subsectors in said ecosystem. He currently is the managing director of Electrios Energy, where he advises on lithium supply chains with a specific focus on the challenges to refine lithium into battery-grade and high-purity lithium products.

Century’s financial situation

Century Lithium engaged BMO Capital Markets to assist the company in securing a potential partner and to work on development funding. The company’s most recent financing was in July 2025, when Century Lithium raised C$4.74M in gross proceeds (approximately C$4.4M in net proceeds) in a financing priced at C$0.30 per unit. Each unit consisted of one common share and a full warrant with each warrant allowing the warrant holder to acquire an additional share at C$0.45 during a five year period.

Based on the most recent financial statements from Q3 2025 (the company hasn’t filed its full-year financials yet), Century Lithium ended September with a positive working capital position of C$6.4M and almost C$6.7M in cash.

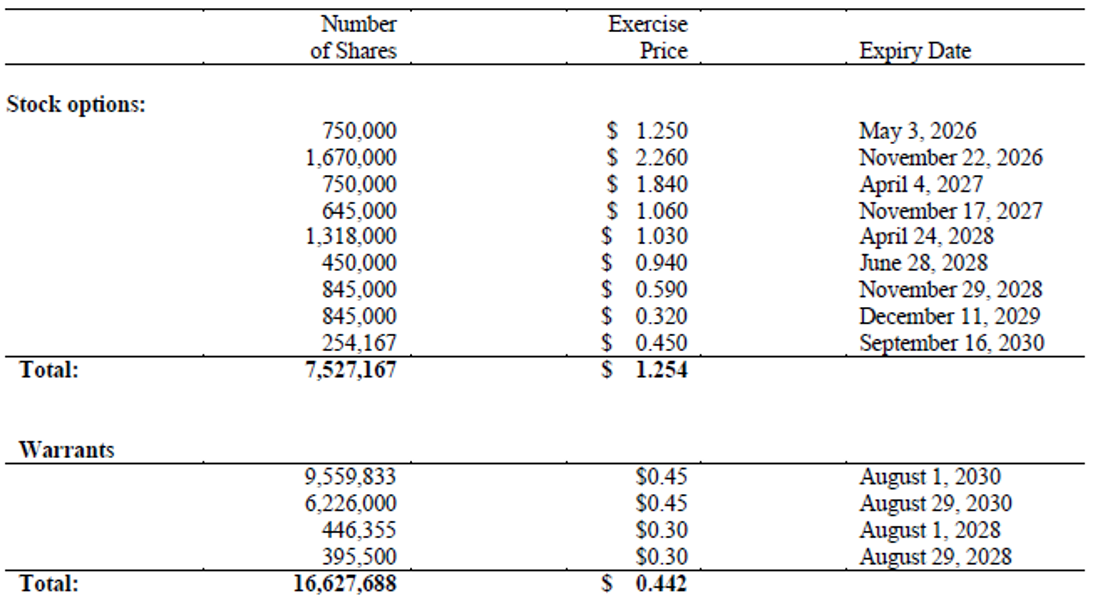

Let’s also not forget all the warrants that are currently outstanding are in the money right now. We are looking forward to seeing an update when the company files its updated financials, but at the end of September, there were 16.63M warrants outstanding with a weighted average exercise price of C$0.442. Should all these warrants be exercised, Century Lithium will receive approximately C$7.35M in proceeds. But as the first expiry date is still more than 2 years out with the majority of the warrants expiring in 4.5 years, we shouldn’t bank on that cash hitting the company’s treasury anytime soon (although we do expect some warrants to be exercised allowing for some cash to trickle into the treasury on a quarterly basis).

Most options are currently out of the money, and we don’t dare to expect to see a share price north of C$2.26 this year (it would be a nice surprise though, and a reward for the company’s substantially improved feasibility study), so we anticipate the 2.42M options that are expiring this year to roll off unexercised, reducing the fully diluted share count. Management option grants, in fact, were restrained relative to share price levels in 2025.

Century Lithium will need to raise money at some point to continue to advance the Angel Island lithium project, but that task should be easier now with the robust feasibility study in hand.

Conclusion

We think the key takeaway from the updated feasibility study is that the project is now ‘financeable’. Spending $1B + $660M to reach 26,500 tonnes in annual lithium carbonate production definitely sounds more feasible than the $1.54B + $0.65B in the previous study. And with the operating expenses dropping to zero (or even into the negative territory in the Phase 2 production scenario), the project should be able to withstand even large fluctuations in the lithium price.

Combine this with the recently granted FAST-41 status which should make the permitting process relatively smooth, and all stars are aligning for Century Lithium. That’s likely why the company engaged BMO Capital Markets to help secure strategic interests and development funding for the Angel Island lithium project.

The updated feasibility study is an important stepping stone to continue to advance Angel Island. And with the lithium carbonate price trading at almost $24,000/t, up 12% in the past two days and having doubled in the past few months, the timing appears to be right.

Disclosure: The author has no long position in Century Lithium but owns warrants from a previous financing. Century Lithium is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.