The lithium price is firmly holding its ground above $20,000 per tonne, there has never been as much political support as there currently is for domestic lithium projects in the United states, yet Century Lithium (LCE.V) is trading at in excess of 20% below the price its most recent financing was conducted at.

While the market is still applying a ‘wait and see’ approach, the stars are starting to align for the company. Century Lithium also recently emphasized the increased reagent prices for sulfuric acid have no impact on the Angel Island project considering it uses a whole different approach as its proprietary metallurgy doesn’t use any sulfuric acid.

Century’s competitive advantage: using the chlor-alkali process

Just last week, Century Lithium provided an update to the market highlighting its proprietary production process without the use of sulphuric acid.

Century Lithium will now also move its demonstration plant from Amargosa Valley to Tonopah. A move that makes sense as it will be helpful to centralize the operations which will make it easier to showcase the Angel Island project and the use of the proprietary technology to interested partners. After all, Century Lithium’s next phase will be to work on permitting and funding for the project.

It’s perhaps also important to reiterate that the entire economic study on the Angel Island lithium project is based on Century Lithium’s patent pending chlor-alkali process. In that process, sodium chloride is used to produce hydrochloric acid and sodium hydroxide. The hydrochloric acid leaches the lithium from the claystone while the sodium hydroxide provides acidity level control throughout the entire production process. The excess sodium hydroxide could be sold, generating a by-product revenue which enhances the overall project economics.

Perhaps that still is an underrated part of the entire economic thesis but it plays an important role as this means the Angel Island project does not need any sulfuric acid.

And that is important because the global sulfur markets have been hit pretty hard by the war in the Middle East (as approximately half of the globally traded sulfur volumes pass through the Strait of Hormuz, as per recent reports). Prices have skyrocketed (outside of the lithium sector, this also makes uranium producers nervous as sulfuric acid is an important component in the recovery of uranium too) and for instance the Tampa contract sulfur prices (which are a well-used benchmark for the domestic sulfur price) have seven-folded in the last few years. This had an immediate knock-on effect on the price of sulfuric acid which almost doubled in the same time frame.

While sulfuric acid is a well-known component used to leach lithium, it’s important to realize that Century Lithium’s process does not need a single gram of sulfuric acid. And that is of course a major competitive advantage right now.

The lithium price remains strong

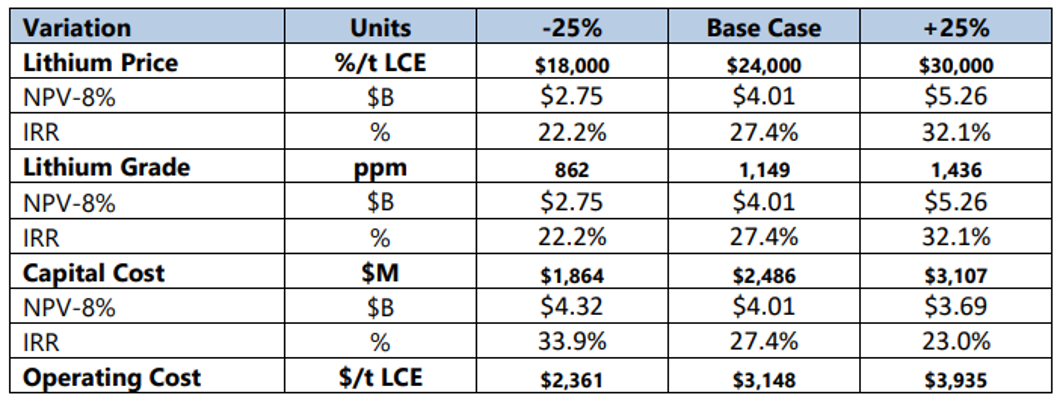

Based on the share price of Century Lithium, you would expect a weak lithium market in general, but that couldn’t be further from the truth. As of the time of writing this update, the price for lithium carbonate in China exceeds $25,000/t. And that’s even higher than the $24,000/t that was used in the base case scenario in the feasibility study. The table below shows us everything we need.

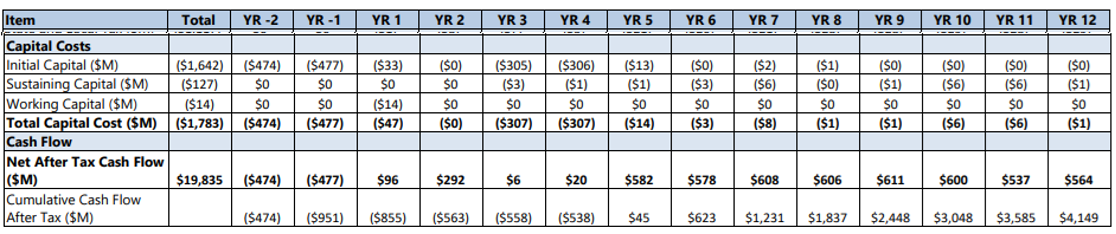

As you are aware, the project sports a US$4B after-tax NPV8% using a base case lithium price of US$24,000/t. This comes with a 27.4% after-tax IRR despite spending north of US$2B in capital expenditures within the first six years (including two years of pre-production capex and the continuous investment to increase the output that will be incurred in the first four years of the mine life).

From Y5 on, it will be smooth sailing with almost US$600M in net after-tax free cash flow (not our numbers, but the numbers in the official feasibility study, shown above). Which means this is exactly the type of project (with a manageable capex, low opex and multi-decade mine life) that larger companies and offtake partners are looking for, to secure a reliable flow of lithium for decades to come.

Note; these economics include the impact of selling sodium hydroxide as a by-product credit at a price of $750/dmt on a FOB basis. As per the effective date of the feasibility study, this represented a 20% discount to the market price at that moment. In full production, the NaOH by-product revenue represents just over 20% of the pre-tax cash flow. A nice addition to boost the economics, but the Angel Island project does not rely on selling sodium hydroxide to make it work. And keep in mind the company has a non-binding MOU in place with Orica which is interested in purchasing membrane-grade sodium hydroxide from Angel Island.

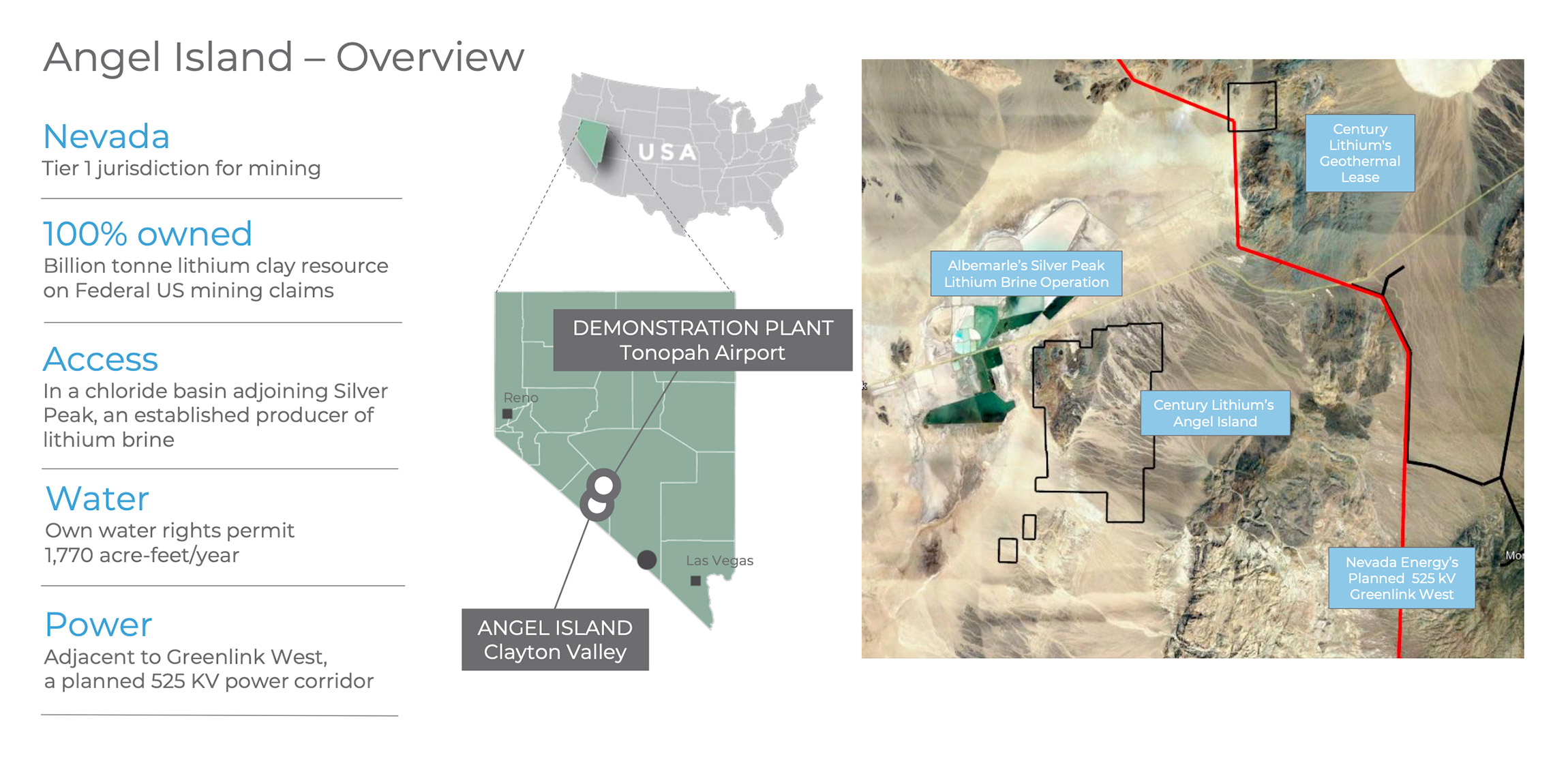

Airport (Source: GRE, 2022)

Adding a Chief Technical Officer to strengthen the team

Earlier this month, the company also announced it appointed Todd Fayram as its Chief Technical Officer. Fayram has been involved with Century Lithium since 2023 when he took on the role of SVP Metallurgy, a key role that cannot be underestimated considering it’s an incredibly important aspect to recover the lithium from the mineralized clay.

As Fayram has been instrumental in helping to design and improve the proprietary process allowing Century Lithium to produce battery grade lithium, a promotion to CTO was a logical next step.

The company cashed up after its C$7M raise

At the end of March, the company closed its C$7M brokered financing (after it was upsized from an initially planned C$5M) for net proceeds of C$6.5M. Century Lithium issued almost 15 million units at C$0.47 per unit, with each unit consisting of one common share and a full warrant. Each full warrant allows a warrant holder to acquire an additional share for C$0.65 during a five year period. The proceeds of the financing will be used for general working capital purposes as well as advancing the Angel Island lithium project through additional technical and permitting work.

Additionally, the company continues to top up its treasury with the proceeds of warrants that were issued in previous placements. In the first two months of 2026 this results in an additional cash inflow of approximately C$143,000. And while this is a negligible amount in the greater scheme of things, these proceeds are useful to help fund the day-to-day overhead expenses. As the majority of the warrants currently have an exercise price of C$0.45, we don’t anticipate any substantial warrant proceeds as long as the share price trades below that level (and hopefully the share price will find its way up again as a gradual exercise of the C$0.45 warrants likely is the best case scenario for Century Lithium).

We estimate the company currently has approximately C$12M in working capital on the balance sheet.

Conclusion

The pieces of the puzzle are finally falling into place for Century Lithium and the recent capital raise will allow the company to continue its efforts at the Angel Island project without slowing down its pace. With a definitive feasibility study in hand and with a lithium carbonate price that continues to trade above $20,000 per tonne (and trading above $25,000/t as recent as last week), Angel Island is one of the most advanced lithium projects in North America.

The project is also already on the radars of the decision makers as it was granted the FAST-41 designation, which should streamline the permitting process.

Despite all these positive elements, the share price continued to slide since the C$7M capital raise, and anyone buying the stock right now can do so at a 20-25% discount compared to what participants in the placement paid for their stock. At the current share price, the company is trading at just over 1% of the official after-tax NPV8% of the flagship Angel Island project.

Disclosure: The author has a long position in Century Lithium. Century Lithium is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.