Integra Resources (ITR.V) kept its promise and was effectively able to publish the results of the Preliminary Economic Assessment in the first full week of September, right in time for the important Beaver Creek and Denver Gold Forum conferences this week.

As expected, the PEA was predominantly focusing on bringing as much of the heap leachable tonnage into the PEA as this would allow Integra to keep the initial capex low which would in turn A) increase the Internal Rate of Return, B) reduce the payback period and C) boost the life-of-mine cash flows.

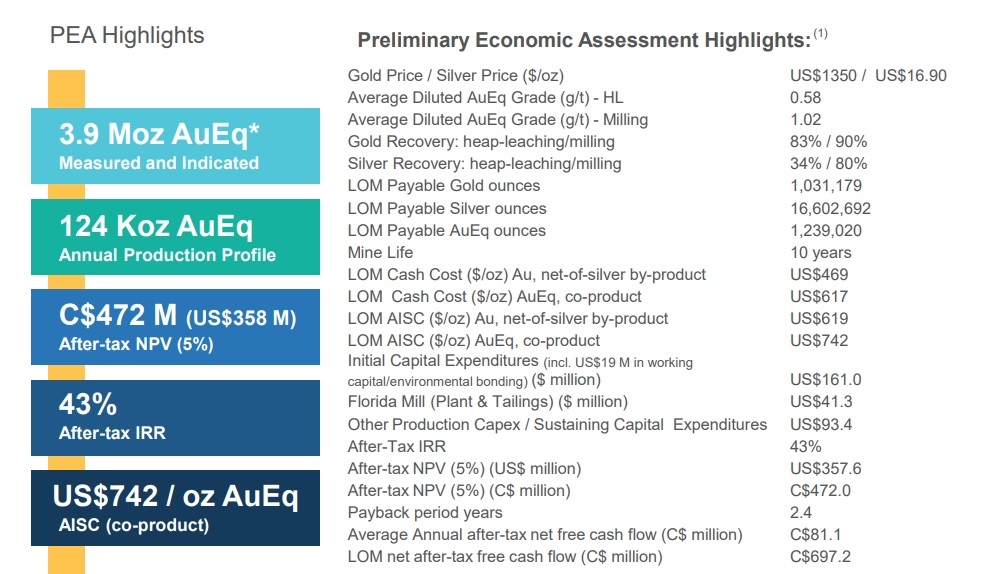

And it looks like Integra succeeded as the initial results indicates a total of 1.03 million ounces and 16.6 million ounces of silver will be recovered from processing almost 94 million tonnes in a combined heap leach and milling scenario. The summarized results speak for themselves:

The main takeaway is the after-tax NPV5% of C$472M (C$5.14/share) at $1350 gold and $16.90 silver which increases to C$623M (C$6.79/share). Keep in mind the NPV/share is based on the current share count of 91.8M shares and the share count will obviously increase should Integra decide to put the project into production themselves. But even if you’d use a share count of 175M shares (the additional 83M shares would allow Integra to raise roughly C$100M at the current share price), it’s clear the value per share is higher than the current C$1.30. The conclusion is quite simple: it’s a good and robust PEA, and the value is mainly generated through the low-cost heap leach phase which will auto-fund the construction of the mill in the second year of the operations.

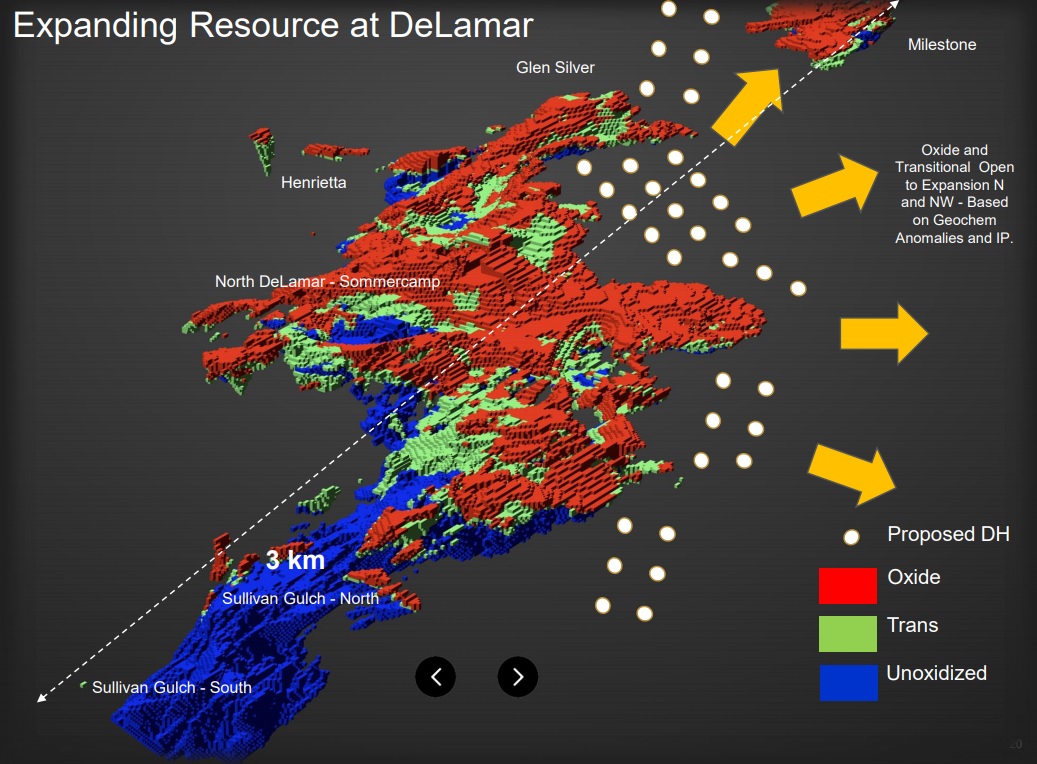

There still is plenty of upside from here as the PEA is just a first pass. Notice how the mine plan only includes 1.82 million gold-equivalent ounces to be processed (for a net recoverable production of 1.24 million gold-equivalent ounces). As that’s just 40% of the total resource at DeLamar and Florida Mountain and less than 50% of the 200.5 million tonnes in the combined measured, indicated and inferred resource categories), we wouldn’t be surprised if Integra would be able to further boost the NPV by extending the mine life by adding more tonnes to the milling scenario which could also unlock additional economies of scale as the current sulphide milling scenario is based on just 2,000 tonnes per day.

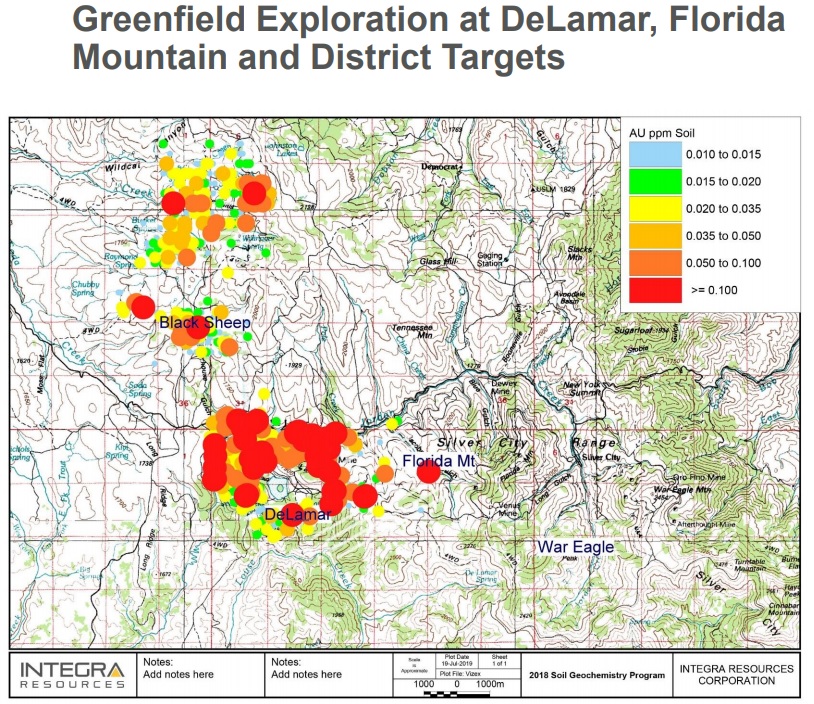

Additionally, Integra has just kicked off a regional exploration program as it will zoom in on the Black Sheep trend which hosts numerous exploration targets, some of which could contain some low-hanging fruit that could easily be included in the mine plan. After having completed its special warrant offering, Integra now has C$16M in cash on the bank (of which C$4.5M will be needed to make the final Kinross payment), so we should see some fresh exploration results from next month on.

Once Integra files the full NI43-compliant report on SEDAR, we will provide a more in-depth review of the PEA.

Disclosure: The author has a long position in Integra Resources. Integra is a sponsor of the website.