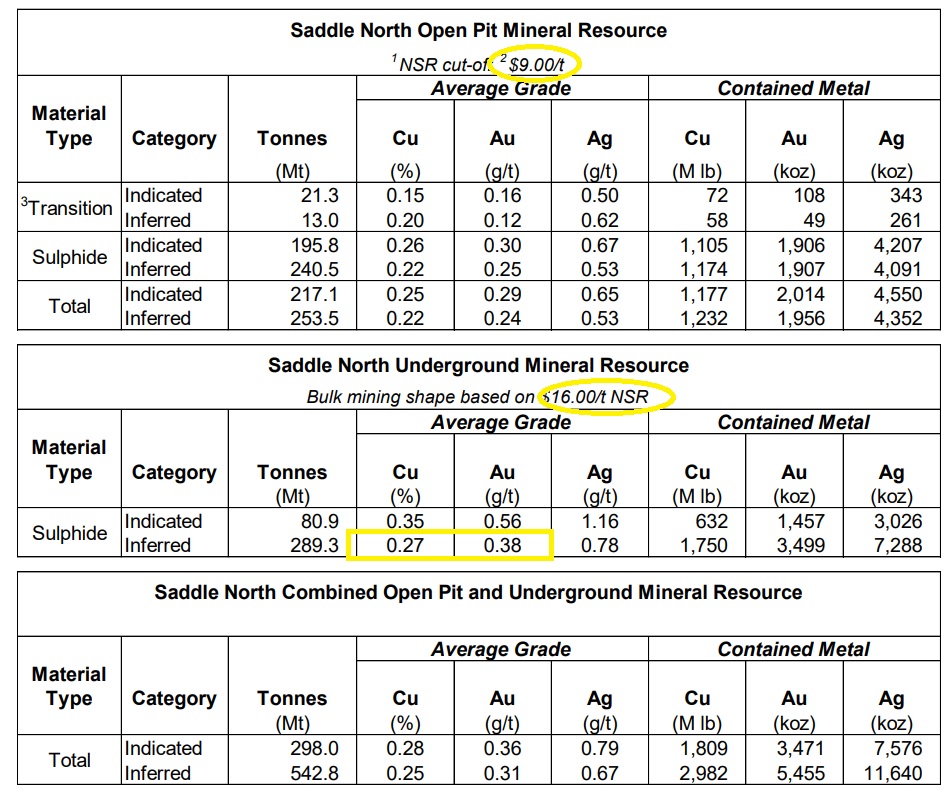

GT Gold’s (GTT.V) maiden resource estimate came in much higher than we expected (original expectations: 220 million tonnes in the open pit and around 90-100 million tonnes in the underground resource. The resource released after-hours contained 470 million tonnes in the open pit (217Mt indicated, 254Mt inferred) while the underground resource was an impressive 81Mt in the indicated category and an additional 289 million tonnes in the inferred category (for a combined 370 million tonnes, or almost 4 times higher than our expectations).

However, it looks like GT Gold has been focusing on size rather than profitability. Let’s leave the open pit out of the equation for now and have a look at the underground resource. The indicated underground resource hosts 81 million tonnes at 0.35% copper and 0.56 g/t gold (and just over 1 g/t silver) for a total of 632 million pounds of copper and 1.46 million ounces of gold. Applying the 88% recovery rate for copper and 67% for gold, the recoverable copper and gold content is 6.8 pounds of copper and 0.37 g/t gold per tonne of rock. At $2.75 copper and $1500 gold, this represents a recoverable rock value of $18.7 + $18 = $36.7/t. A block cave model will work on this 81 million tonnes.

The inferred underground resource however is less impressive. Having almost 290 million tonnes is huge but the grade of 0.27% copper and 0.38 g/t gold could be problematic: the recoverable rock value will be just $14.4 + $12.3 = $26.7/t. While this will cover the expenses of an efficient block cave mining model, this won’t be sufficient to justify building the infrastructure for this mine (unless of course copper goes to $3.50 and gold stays at $1750-1800/oz).

It looks like GT Gold wanted to flex its muscles and show its potential to the neighbors at Red Chris as it looks like the only way the majority of the inferred underground resource could be mined at a profit is if you wouldn’t have to build a mill.

The maiden resource at Tatogga is big, it’s huge and much larger than anticipated. But ‘big’ doesn’t mean profitable and we expect a substantial amount of the tonnes not making it into a mine plan based on a standalone scenario. After the recent run GT Gold had, this could very well become a ‘sell on the news’ story.

Disclosure: The author has a long position but will very likely take profit and sell tomorrow.

I sold with loss when I saw this analysis here. The next day the GTT stock recovered 50% of its previous day loss. If I have waited just one day I would have not lost so much money.

The share price opened on Tuesday Morning (12.5 hours after the publication of this article) at C$1.87 and closed the three subsequent days of the week lower (1.80, 1.83, 1.78). It sounds like you sold an additional 10-20% below the Tuesday opening price, that’s hardly something to blame anyone else for, isn’t it?