Millennial Lithium (ML.V) has now published the summary of its feasibility study on the Pastos Grandes lithium project in Argentina’s Salta province. The feasibility study shows the company’s PEA was very robust as there are very few changes: the initial capex is estimated at US$448M ($410M in the PEA) and the average production cost for the lithium is estimated at just below US$3,400 per tonne of lithium carbonate (compared to just over $3,200/t in the PEA).

As we mentioned in a previous report, we felt the 25 year mine life used in the PEA was very arbitrary as the resource (and reserve) estimate at Pastos Grandes could underpin a multi-decade mine life. As such, it wasn’t a big surprise to see the feasibility study is now taking a mine life of 40 years into account which is even longer than the 30 years we used in our October report.

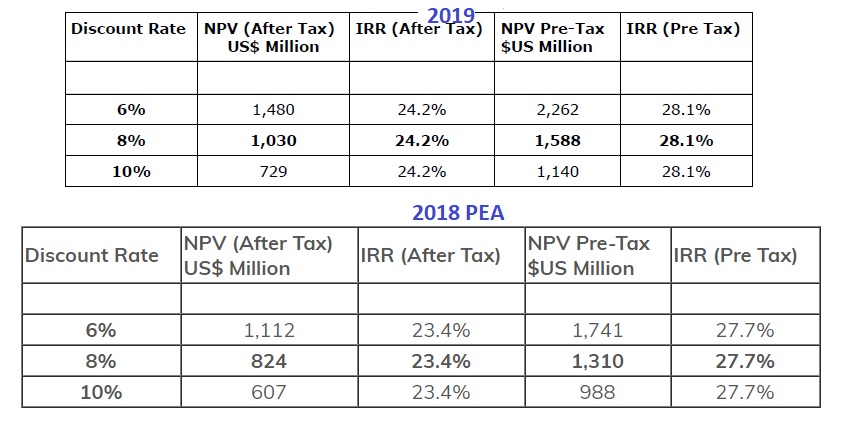

And although the discount factor will play a very important role towards the end of the mine life (in the 35th year for instance, the incoming cash flows are discounted by a factor of almost 15 using an 8% discount rate), Millennial’s Pastos Grandes project currently boasts an after-tax NPV8% of US$1.03B and an IRR of 24.2%. That’s higher than the US$824M NPV8% in the PEA.

Unfortunately the press release doesn’t contain a sensitivity analysis to check how the NPV and IRR evolves using a different lithium price. Although CEO Abasov mentioned during a recent presentation in Brussels the company would use a lower base case price, the currently used price of $13,199/t is only marginally lower than the $13,499/t used in the 2018 PEA, and is still approximately 10% higher than the current spot price of battery-grade lithium carbonate (but in line with longer-term contract values). This won’t be a deal-breaker as a lower lithium price would only be useful to ‘stress test’ the base case scenario); we already established in October 2018 Pastos Grandes remains world class at a lithium price of $9,000/t, and have no reason to assume this will be different as the much longer mine life will compensate for the slightly higher capex and opex. It’s a very robust PEA and even if you’d use a 10% discount rate, the after-tax NPV would still end up close to a billion Canadian Dollar.

Go to Millennial’s website

The author has a long position in Millennial Lithium. Millennial currently is not a sponsor of the website but has been a sponsor in the preceding twelve months. Please read the disclaimer