Mkango Resources (MKA.V, MKA.L) has released the results of an updated feasibility study on its Songwe Hill REE project in Malawi, in combination with the result of a pre-feasibility study completed on the Pulawy Rare Earths Separation plant in Poland.

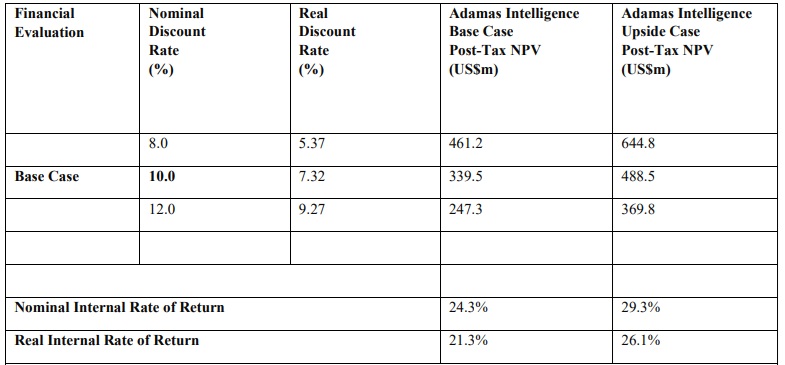

The feasibility study calls for an 18 year mine life, producing an average of just under 6,000 tonnes of TREO per year in the first five years. This includes almost 2,000 tonnes per year of neodymium and praseodymium oxides and 56 tonnes per year of dysprosium and terbium. The initial capex is estimated at US$326M, resulting in an after-tax NPV10% of US$339M and an IRR of 24%. The total incoming after-tax cash flow of the project is estimated at US$1.55B. Using the upside forecasts provided by Adamas Intelligence, the NPV10% increases to US$489M (and US$645M using a lower discount rate of 8%) with a net after-tax cash flow of in excess of US$2B.

Adding the impact of the Pulawy separation plant, the after-tax NPV increases to US$892M at a 10% discount rate (with a post-tax life of operations cash flow of in excess of US$5.5B). The capex for the Polawy plant is estimated at just US$212M which is very reasonable to get another EU rare earth separation plant (relying on the feedstock from Mkango’s Malawi project, but able to treat mineral concentrates from third party suppliers as well).

Mkango also recently completed a capital raise of 12.5M GBP / C$23M by issuing just under 38 million new shares at 33 pence (approximately C$0.606 on a CAD-equivalent basis). The company’s CFO participated in the offering for a total amount of approximately C$275,000.

Disclosure: The author has no position in Mkango Resources. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.