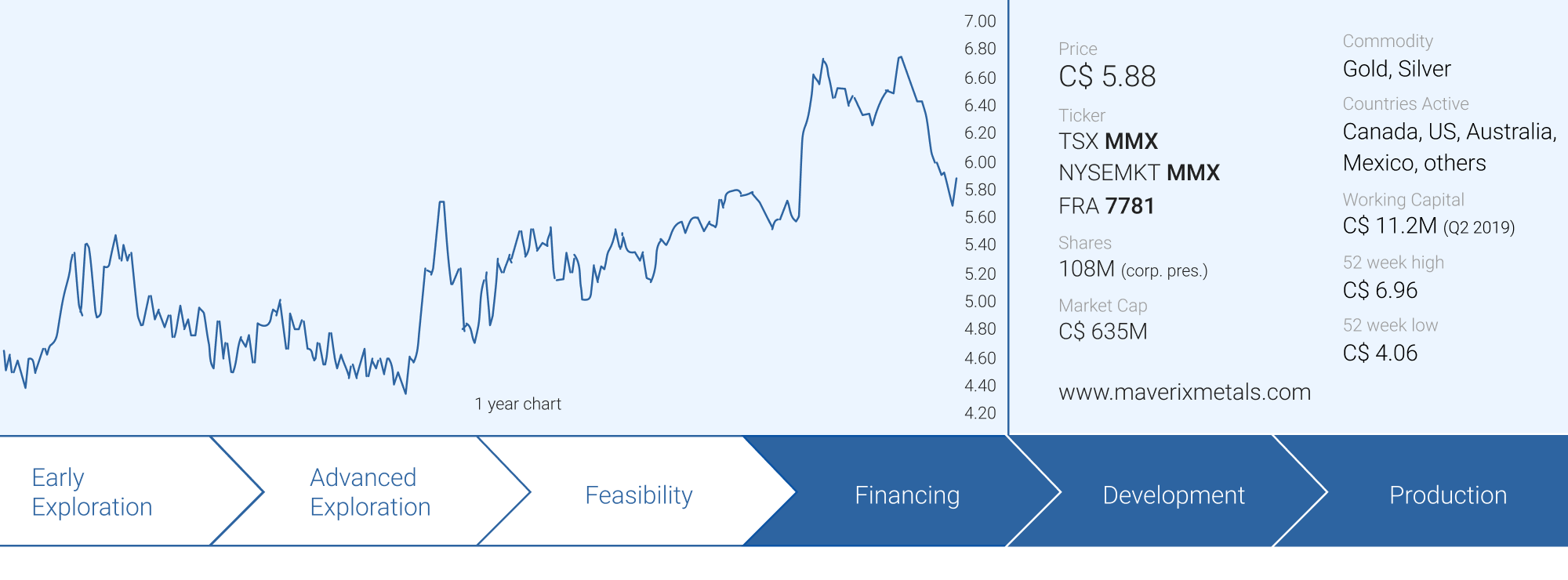

As Maverix Metals (MMX.TO, MMX) is a cash flowing company, it makes sense to keep our fingers on the pulse every quarter to check up on the company’s operating cash flows and its (financial) ability to close new deals.

The current gold (and silver) price will prove to be a blessing for royalty and streaming companies as the marginal increase in the precious metals prices will go directly to its operating cash flows. As the gold and silver prices only started to gain momentum towards the end of the second quarter, we will only begin to see the real impact from these higher metal prices in the future quarters as the gold price in Q2 averaged just over $1300/oz.

The royalty machine is gaining traction: a look at the Q2 results

For royalty and streaming companies, there’s only one thing that matters, and that’s the incoming cash flow. Being able to report a net income is great but let’s keep in mind this usually represents a ‘paper’ profit which includes the assumed depletion and depreciation charges on the royalties and streams.

Usually the cash flow performance is more interesting as it indicates how much cash flow a company is generating which provides a good overview of how much the company can spend on acquiring new royalties and streaming deals on assets to A) mitigate the impact of the depletion of the existing assets as mines obviously don’t have an infinite mine life and B) continue to grow the business by expanding the production profile.

La Colorada Mine, Pan American Silver

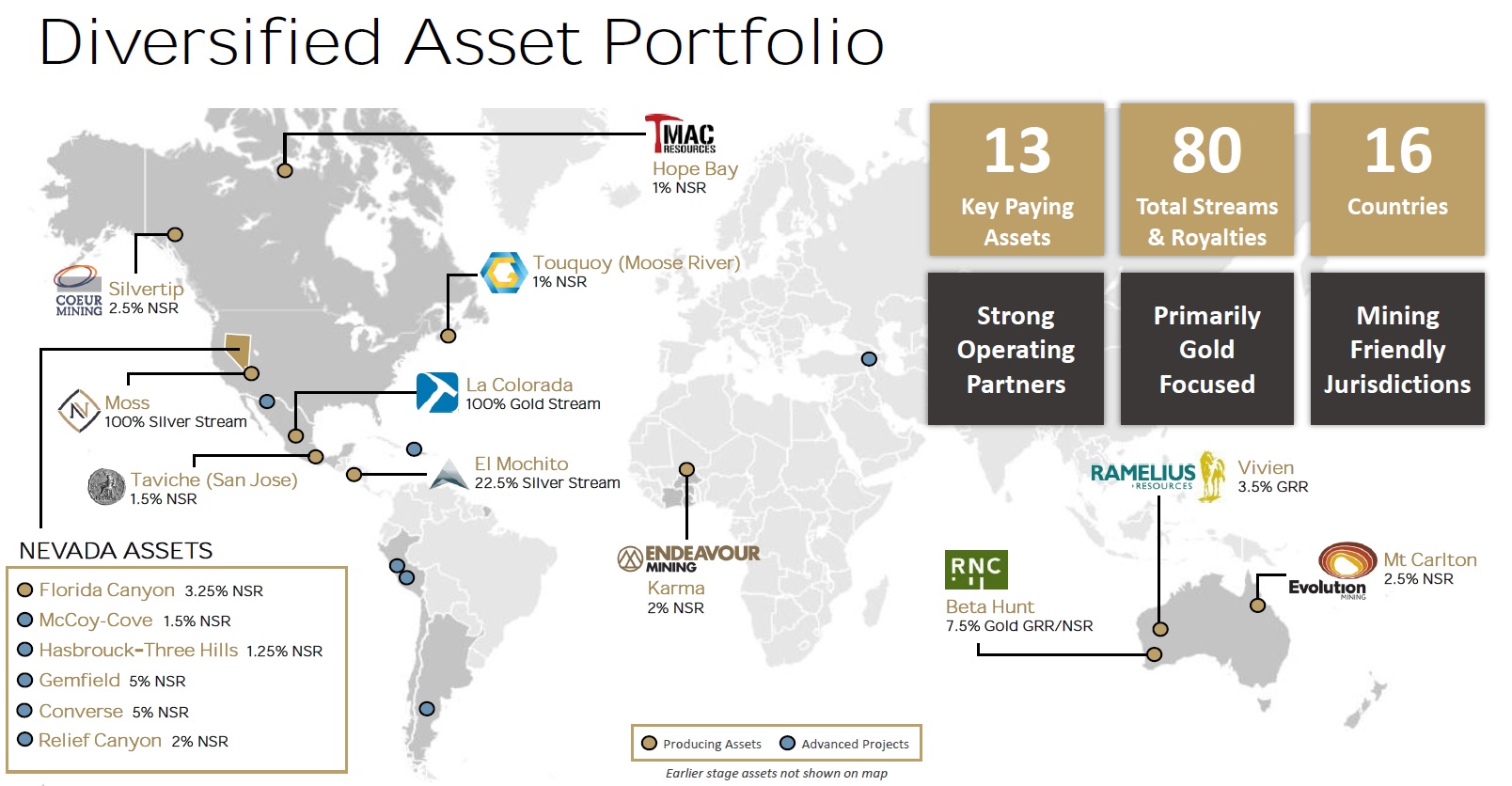

In an ideal world, a royalty and streaming company’s business model and assumptions should allow it to pursue both A and B at the same time. That effect of compounding is what made peers like Franco Nevada (FNV) and Wheaton Precious Metals (WPM, WPM.TO) so significant. We argued before that Maverix Metals is still in its relative infancy so it should be relatively easy to pursue additional growth. The recent purchase of an additional royalty on the Hope Bay gold mine owned and operated by TMAC Resources (TMR.TO) will contribute towards future growth (see later).

But first, let’s check up on Maverix Metals’ financial performance in the second quarter and the first semester.

As expected, the attributable gold production increased in the second quarter thanks to a higher contribution from RNC Minerals’ (RNX.TO) Beta Hunt mine in Australia and the very strong result at the La Colorada mine owned and operated by Pan American Silver (PAAS, PAAS.TO). La Colorada contributed an attributable production of 1,090 ounces gold-equivalent in the second quarter (compared to just 848 gold-equivalent ounces in the first quarter). Maverix’s total attributable gold production was just over 6,400 ounces in the second quarter (on a gold-equivalent basis) and this pushed the total gold-equivalent output to just short of 11,700 ounces in the first semester.

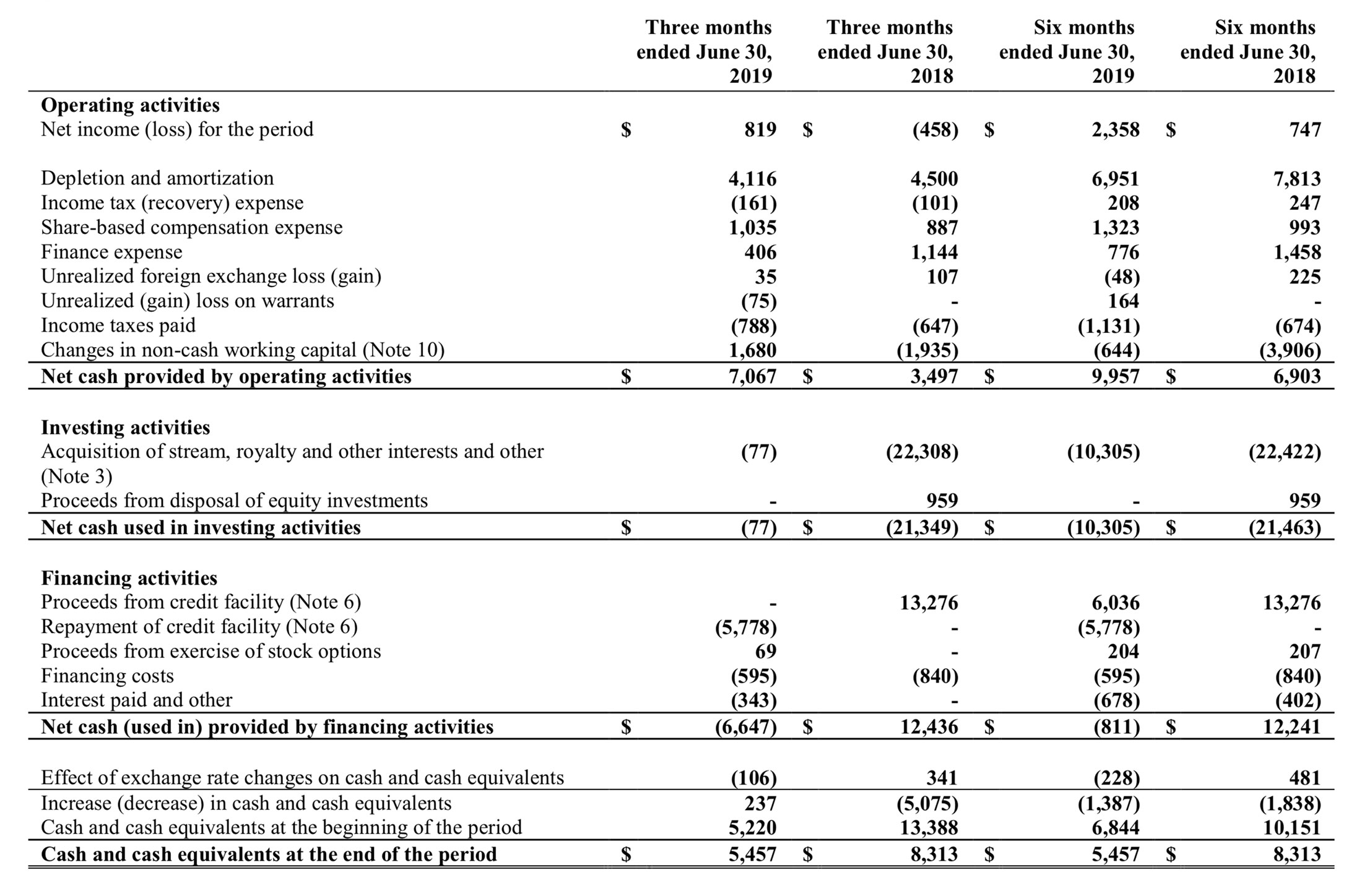

Despite the excellent results and strong gold price (in CAD), the total revenue generated through the sales of the attributable gold production came in at just C$9.35M in the second quarter of the year. That’s on the lower end of the expectations, and this appears to be due to a discrepancy between ounces produced and ounces sold as just 5,359 gold-equivalent ounces were sold as compared to the 6,425 gold equivalent ounces that were produced. Despite not selling the entire attributable production, Maverix’s income statement still shows an operating income of C$1.15M (despite a C$1M share-based compensation expense which should be much lower over the next few quarters).

The net income in the second quarter was C$819,000 (thanks to a C$161,000 tax contribution) while the total net income in the first semester was C$2.36M. An excellent Q2 performance considering the C$4.4M in overhead expenses and depletion charges. The G&A expenses were quite high in the second quarter (C$1.96M), but these included the bonus payments for FY 2018 as well as the due diligence and other expenses related to Maverix’s listing on the NYSEMKT in the United States and the upgrade to the TSX in Canada.

Considering a large portion of the expenses are non-cash expenses (depletion, share-based compensation,…), Maverix’s cash flow generation is obviously much higher than the net income as there’s virtually no sustaining CAPEX: once a royalty or stream has been purchased, there are no further commitments required to keep it in good standing.

Maverix Metals reported an operating cash flow of C$7.1M. This includes a C$1.7M cash contribution from changes in the working capital but also includes a C$788,000 tax payment. Those taxes weren’t all due over the Q2 performance and Maverix has been paying a ‘historic’ tax liability. Considering the tax payment should not be entirely attributed to the Q2 results, it makes sense to adjust the reported cash flow accordingly. After also deducting the C$1M in interest and financing expenses, the Q2 operating cash flow was approximately C$5.25M.

Keep in mind this still excludes the 1,066 gold-equivalent ounces that were produced in Q2 but weren’t sold in the same time frame. Given the strong gold price in July it’s not unrealistic to assume those ounces were sold for at least C$1800/oz and that would have pushed the adjusted operating cash flow to over C$7M. Undoubtedly these ounces will now have been sold and will contribute to Q3’s cash flow.

Karma, Endeavour Mining

Maverix purchases an additional royalty on the Hope Bay mine

Maverix used the incoming cash flow in the second quarter to reduce the total amount that has been drawn down from its credit facility but has now withdrawn more cash from the facility to fund a new royalty purchase.

Maverix agreed with TMAC Resources (TMR.TO) to acquire an additional 1.5% NSR on its producing Hope Bay gold project in Canada’s Nunavut territory. Maverix Metals made a US$40M payment to TMAC to acquire the additional 1.5% Net Smelter Royalty and considering TMAC expects Hope Bay to produce over 160,000 ounces of gold this year, the attributable gold production of the 1.5% royalty will be 2,400 ounces for a value of approximately US$3.6M annually, however the 1.5% NSR which was just acquired will only be payable from August 1st for this year so we can expect a contribution of around US$1.5M/C$2M for the current financial year.

Any time after June 30, 2021, TMAC has the right to buy back 0.5% of the additional 1.5% royalty and after a total of three million ounces is produced from August 1st 2019 on, the 1.5% royalty will decrease to 0.75%, regardless of whether the partial buyback is exercised, meaning even if the buyback is exercised once 3 million ounces has been produced Maverix will still retain a 1.75% total royalty on Hope Bay (a 1% NSR which Maverix previously owned and 0.75% from the newly acquired royalty).

Hope Bay, TMAC Resources

Another interesting feature of the royalty deal is the clause allowing TMAC Resources to repurchase the entire 1.5% NSR for US$50M in the event of a change of control before June 30th, 2021. As well, TMAC retains the right to pay the additional 1.5% NSR in TMAC stock rather than cash until the same date, and only from July 1st 2021 on, a cash settlement will be mandatory.

With the purchase of the additional NSR, Maverix Metals now owns a total 2.5% NSR on Hope Bay as well as a bonus 0.25% royalty which Maverix will be entitled to until the point at which the additional royalty is registered against the property. This makes Hope Bay one of Maverix’s most important assets with TMAC expecting production of over 160,000 ounces of gold in 2019. Moreover, with an initial 20-year mine life and almost 5 million ounces of gold in the measured and indicated resource categories and 3.6 million ounces of gold in the reserves, Maverix just secured exposure to an asset with tremendous exploration and expansion potential that will very likely operate for decades.

The only caveat is that TMAC has the option to settle its royalty payments in stock, but that doesn’t have to be a deal-breaker as TMAC’s share price also has upside potential if the company continues to execute its turnaround plan.

Beta Hunt, RNC Minerals

Conclusion

Maverix’s second quarter was good, and it’s fair to assume the current quarter will be the best in the history of the company with the combination of higher metal prices and a higher attributable production (the additional TMAC royalty has an effective date of August 1st and will contribute for two months to the Q3 result). Maverix has already publicly stated that they believe that attributable gold production will increase significantly in the 2nd semester of 2019.

As of the end of Q2, Maverix used approximately US$12M of its US$75M credit facility so it still had plenty of financial flexibility to close the Hope Bay royalty purchase and continue to pursue additional acquisitions. Additionally, Maverix just recently announced that it has upsized its credit facility (with CIBC and National Bank) to US$120M.

Disclosure: The author holds a long position in Maverix Metals Inc. Maverix Metals Inc. is a sponsor of the website.