Nomad Royalty (NSR.TO) is the newest addition to the Canadian royalty and streaming scene. The company just closed a transaction with Orion Mine Finance and Yamana Gold (YRI.TO, AUY) and started trading last Friday upon completing the reverse takeover of Guerrero Ventures. We sat down with CEO Vincent Metcalfe, whom we remember from his days at the Osisko Group and Falco Resources (FPC.V).

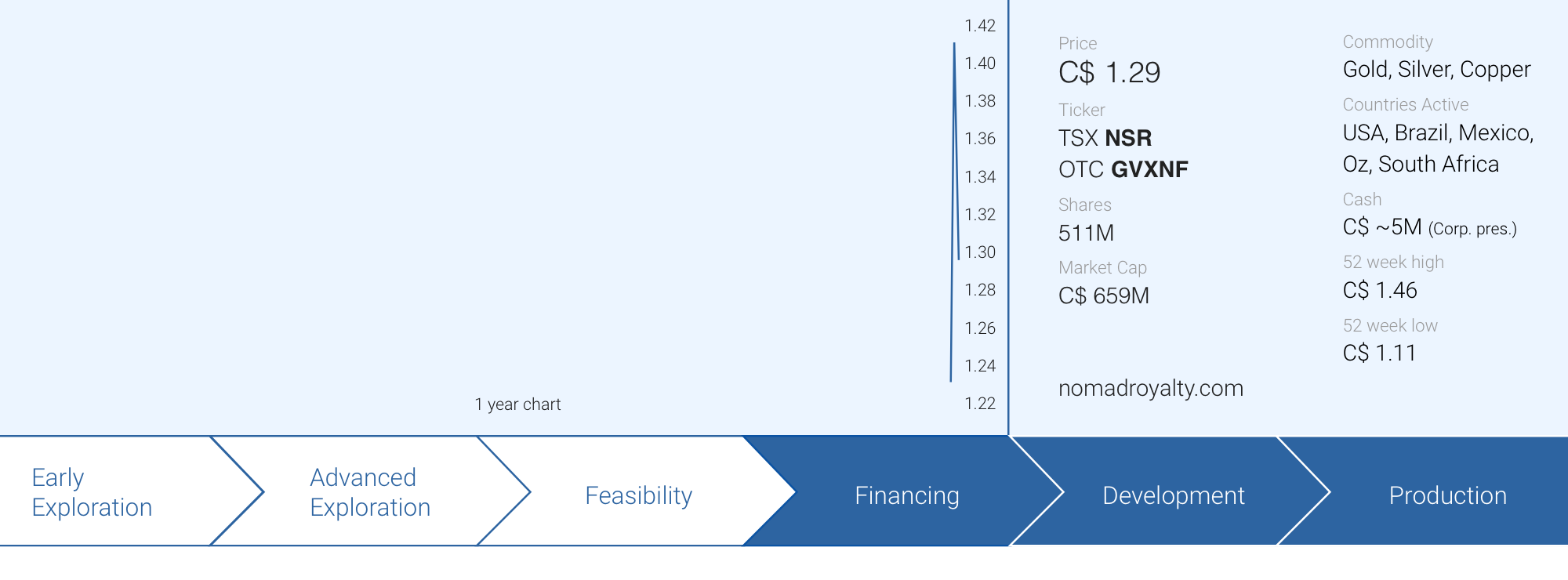

Nomad Royalty closed at C$1.29 giving the company a market capitalization of C$659M using the current share count of 511,015,979 shares.

Creating a new royalty company

Most people will remember you from your roles at Osisko Gold Royalties and Falco Resources. How did the idea grow to create a new royalty player with your Osisko group colleague Joseph de la Plante?

When I left the Osisko Group my plan was not to start another royalty company, but rather to focus on a development or near-production play. Joseph and I always knew we would start a Company at some point. We both have the entrepreneurial spirit, so it was really a matter of time. However, following Joseph officially partnering up in Guerrero (our shell), we started getting calls from several parties. We obviously knew Orion quite well, so when they asked us to sit down with them to discuss their portfolio of assets we jumped on the opportunity. As for Elif, when we saw that she was moving on we sat down and explained several concepts we were working on, a few weeks later she was coming on as the third founding partner. Her experience is unparalleled and she’s a great asset for Nomad.

Can you elaborate on how the evolution from concept to execution happened? Did Nomad approach Orion, or was the creation of a new royalty company a ‘mutual’ idea fostered over the past few years?

Everything happened rather quickly. We got a call from Orion, jumped on a plane to New York and following our meeting, we ended up proposing the possibility of creating a new royalty company with Orion as a main partner. The go-public angle is something that had been discussed within the sector, but the difficult part for a Vendor is finding a credible management team, and a suitable vehicle. Timing was good for us, we were able to offer Orion both.

And how did you bring Yamana Gold to the table to vend in 4 different assets?

Really impeccable timing, we also had heard Yamana was nearing the end of their process on the sale of its portfolio. Once we came to an agreement with Orion, we presented the concept to Yamana and their response was really good. Yamana also had the benefit of having done several spin-offs in the past. They realized great value with Brio that became Leagold, and now Equinox Gold (EQX.TO, EQX).

In your company presentation, Nomad claims it will save on costs by not having an offshore entity. One would think that having an offshore subsidiary (Barbados seems to be popular for streaming companies) would result in significant tax benefits. Can you elaborate on the expected fiscal structure of Nomad and the anticipated income taxes and depreciation expenses to reduce the taxable income?

Yes, having gone through building an offshore sub in the past, we were able to evaluate the pros and cons of it quite objectively. Savings are quite material given you don’t need another team offshore and from an auditing/legal/fees standpoint there are additional substantial savings. From a tax standpoint, we were able to minimize the tax leakage of bringing the assets onshore. We had the ability to gross up the tax pools, so we will see little effect on value. And really, given project financing will not be a core part of our strategy having an offshore sub will not really affect our competitiveness.

You tout the Nomad team to implement ‘a new vision for the sector’, can you elaborate on what you will do different with Nomad and how this will benefit shareholders?

A strong focus on alignment with shareholders is particularly important, that means minimizing G&A expenses while returning capital to shareholders through a strong dividend. We will also be implementing new ESG measures within our investment products.

Is Nomad operating fully independent from the Osisko group of companies, or are there still ‘open communication lines’ that could help you in sourcing new opportunities that may not be a good fit for the Osisko Gold Royalties portfolio?

We are 100% independent. We still have a good relationship with Osisko, we certainly learned a lot and gained a tremendous amount of experience during our years with the group. Joseph and Elif were an important part of the success of Canadian Malartic mine as well, so we are obviously all thankful and appreciative of our time spent with them. They’ve solidified themselves in Canada’s mining world, we sure hope Nomad will do the same in the future.

Yamana Gold will probably want to monetize its stake in Nomad further down the road. Although we would expect a senior producer to be smart enough to ensure this happens in an orderly fashion anyway, did you build in any safeguards and protection measures that would give you enough time to find buyers for any blocks Yamana would potentially like to sell?

Yes, we did. We do have mechanisms in place, there is a 6 month lock up to start, but also notices and orderly sale mechanisms in place, etc. Most importantly, it is why we wanted to get investors in this first round, to make sure they can participate in the current re-rating, but also have capacity if blocks become available. But Yamana really believes in the long-term re-rating story, they recently sold the Equinox block, which they held for over 4 years.

The main assets

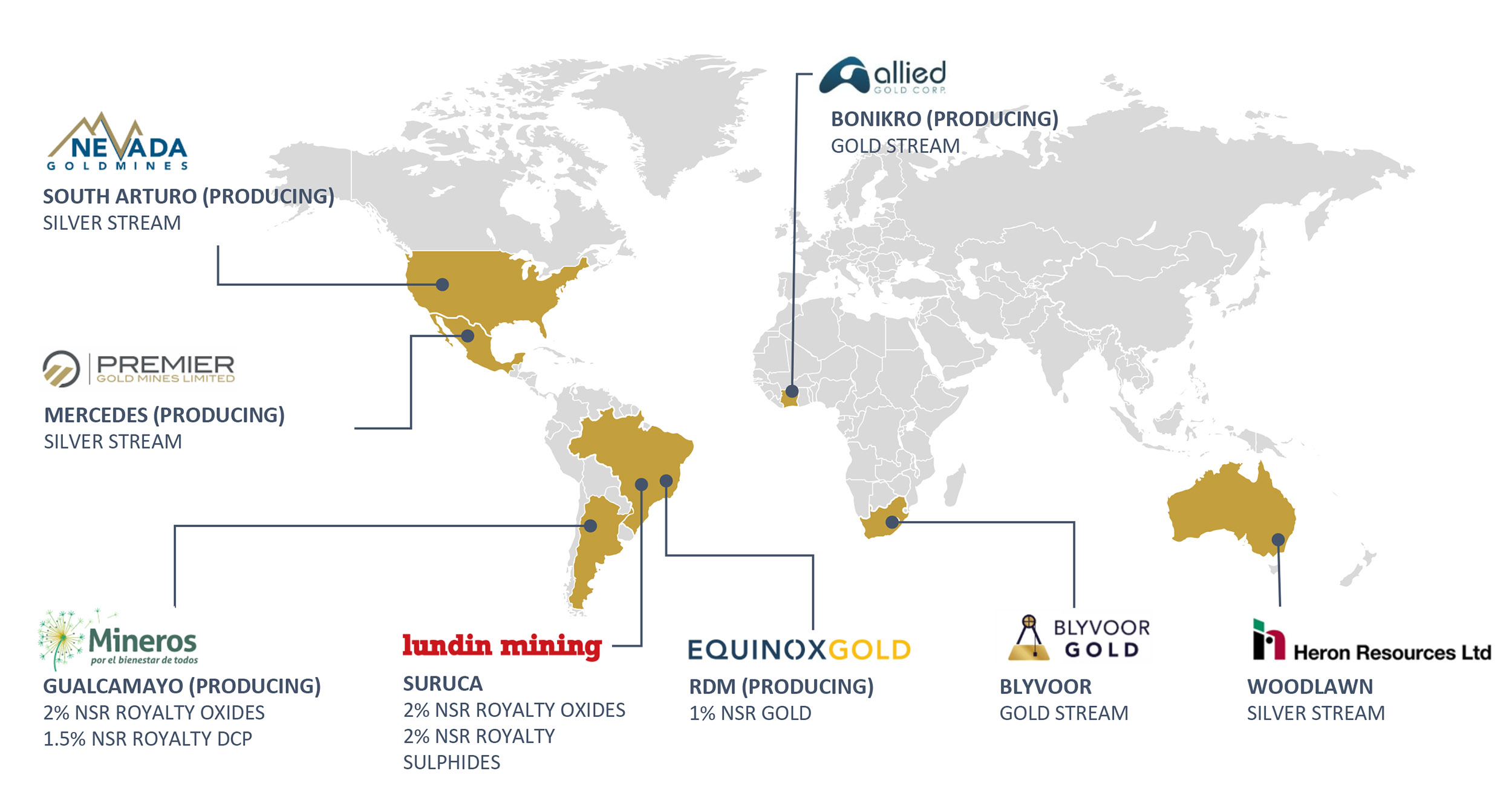

Your two main gold projects that will contribute the majority of the 2021 and 2022 cash flows are based in Africa. Can you elaborate on why you like the Bonikro (Ivory Coast) and Blyvoor (South Africa) mines?

For Bonikro, it’s a “known” commodity per say, it’s been operating steadily for 10 years, and will go on for another 10 years. Great exploration potential, but most importantly, a great team of operators in Allied Gold, who also recently took control of of Sadiola. As for Blyvoor, there is an incredible resource of over 26 million ounces, replacement CAPEX of probably $1.5-$2.0 billion with regards to the underground infrastructure, and a very capable management team. They have a very attractive vision to implement new mining methods to an old camp, and really perhaps act as a game changer.

If we are correct, the operators of both mines (Allied Gold and Blyvoor Gold respectively) are private companies. Do you find dealing with private companies easier than with publicly listed companies? Do both operators have more assets in their portfolios that you could have ‘dibs’ on if they are looking for additional capital to develop new projects?

Both teams have been great to deal with. We conducted site visits to both operations, and what we saw really reassured us. They do have more assets, we do not have ROFRs per say, but having a good working relationship always helps introducing new ideas.

How to grow Nomad Royalty

It sounds counter-intuitive but aren’t high metal prices also a negative factor for royalty and streaming companies. While the incoming cash flow will be relatively high, it makes it tougher to find new deals to replenish the attributable reserves as you will have to acquire new assets at a premium price compared to just six months ago? Additionally, for developers, the high commodity prices could mean there are funding options with a lower cost of capital available to them.

The great thing about the royalty sector is that you cater to both the precious metal and the base metal sectors. It almost acts as a hedge for a royalty company. We see a lot of opportunity at the moment. Interestingly, we are also seeing a lot of single royalties and small packages become available. Investors are increasingly deploying capital in our sector given the lower volatility vs the producers or explorers, this allows us to help and support the junior sector as a whole, the role of royalty companies is becoming vital for the mining sector.

What are the main characteristics you will be looking for while trying to expand your asset portfolio?

Cash flow and near-term cash flow will be important

How relevant are the locations of assets?

Cash flow and near-term cash flow will be our main focus points. The location isn’t extremely important to us, we are looking pretty much everywhere around the world. We see more geographical diversification as good thing and we expect to keep adding royalties in various jurisdictions.

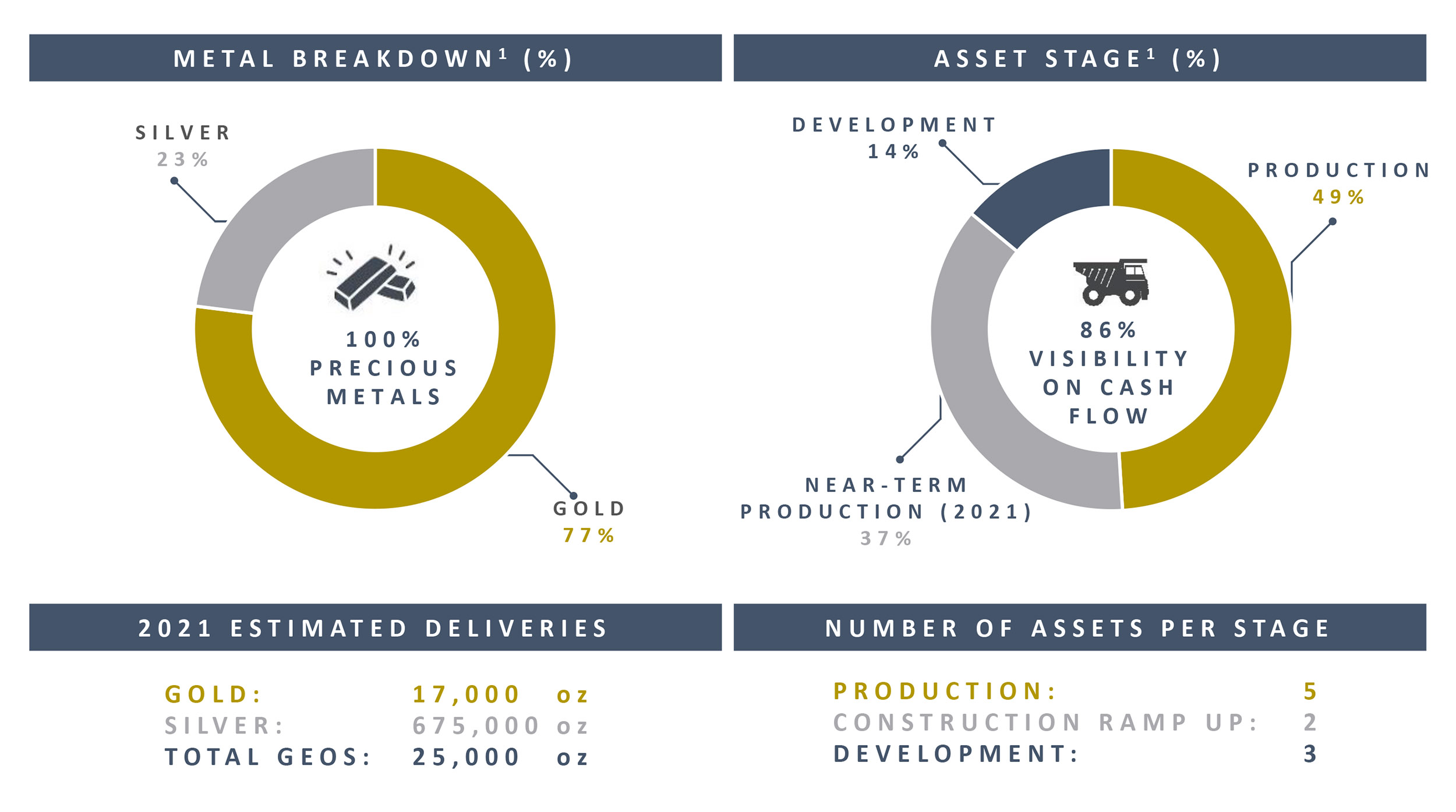

Right now your anticipated gold:silver ratio is roughly 77/23. Will you continue to favor gold over silver or do you see more potential to sign up deals for the latter?

We mainly focus on precious metals right now. Whether that’s predominantly gold or silver doesn’t really matter right now. We do like silver a lot at the current valuation.

Would you consider venturing out into the base metal space? As most existing royalty companies are focusing on precious metals projects, the base metal space doesn’t enjoy the main attention. While we understand this would have a negative impact on how you would be perceived by the market as a pure precious metals play, there may be more opportunities and higher potential returns by also kicking the tires of non-precious metal projects. Your Woodlawn stream already contains exposure to zinc, do you see more opportunities in this area?

There needs to be a precious metal angle, we want to make sure that remains a focus. But a royalty on a Copper-Gold deposit for example would definitely fit well. We are looking for long life assets.

Right now, everything is equity-funded, but we expect you will be able to announce a credit facility soon, backed by the existing and producing royalties. Have you found the banks to be receptive to a new royalty company?

We were very advanced prior to COVID-19 happening, we were provided terms that were very attractive. Given the current credit situation, we will likely wait for the credit markets to come back prior to moving, but we anticipate having a facility in place in the near-term which will help us increase financial capacity. In the interim, we have approached alternative capital providers.

A few years ago we saw Sandstorm taking over Mariana Resources for its minority stake in a high-grade project. Meanwhile, Osisko Gold Royalties has been investing in an ‘incubator model’ to help companies moving their projects forward which allows them to both benefit from royalty revenue if a mine does get built as well as from the share price appreciation. Is this (taking stakes in companies/projects beyond a royalty/stream) an approach you would consider doing with Nomad?

No it is not something we will be focused on, we want to stay as pure play as possible, we may take small bets on early stage projects to get rights on future upside, and also add to long term optionality, but we do not forecast buying or participating in a project that would require us to be a “on the hook” for an unspecified amount.

We noticed there are virtually no royalty players in Australia. Is this an area you anticipate to target?

Yes, all of Australasia will also be a focus, there are several opportunities that recently came to us on very interesting projects.

Valuing Nomad

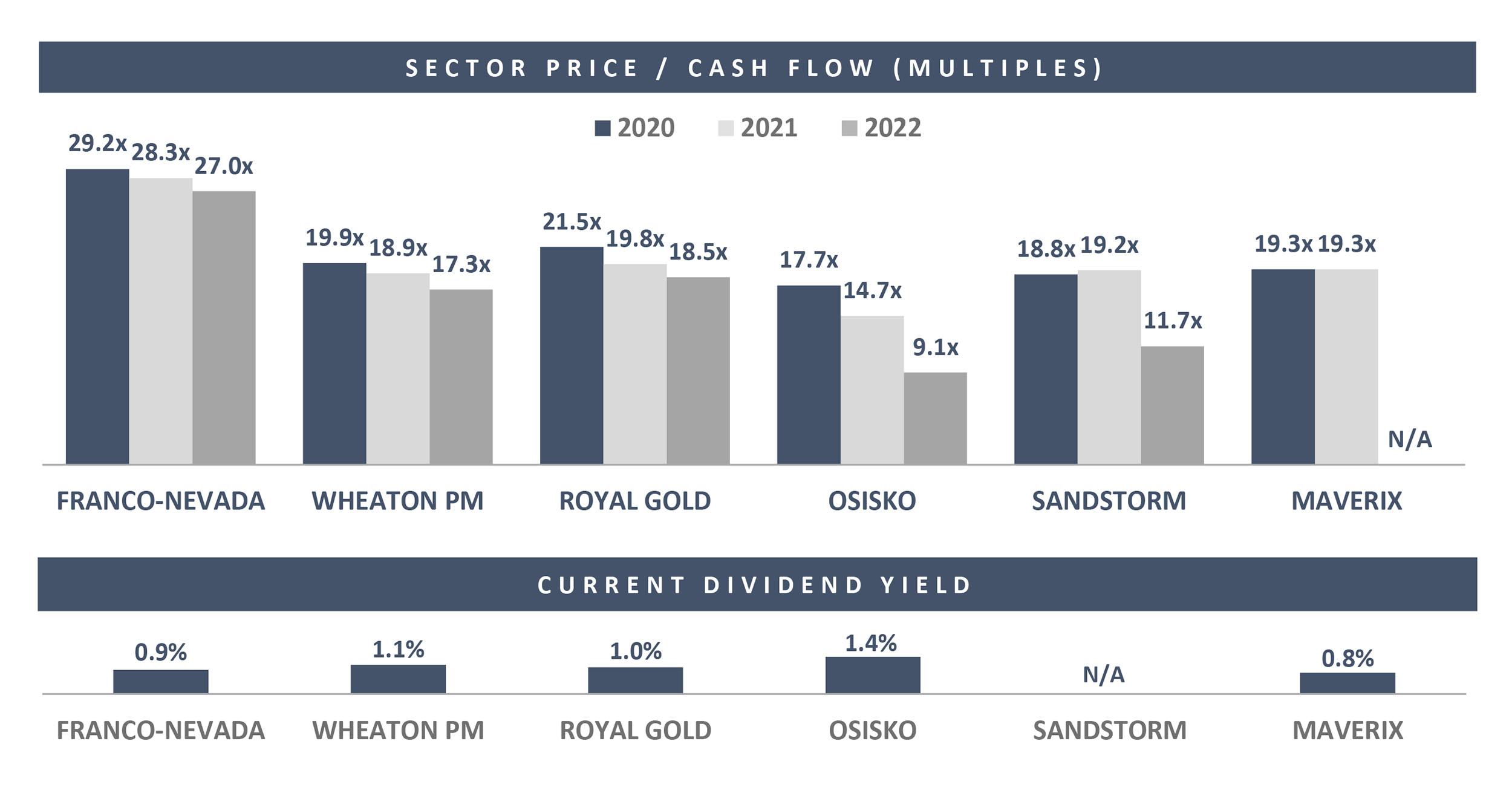

Large streaming companies like a Franco Nevada and Wheaton Precious Metals remain some of the most important proxies for generalist investors to gain exposure to the precious metals space. However, this also creates valuation issues as Franco is trading at almost 3X its NAV while the Wheatons and Royal Golds of the world aren’t doing much better. How would you value a streaming company?

Wheaton caught up quite nicely recently. Franco runs an incredible business and will likely always lead the pack given they are one of the most liquid and diversified names, but for us we see a lot opportunity to grow fast quickly. Teaming up and syndicating deals with peers or alternative groups will enable us to compete with the larger players. As the market understands our asset base and becomes familiar with it, we will continue to increase liquidity in the market and add to the portfolio. As we execute on those fronts, the valuation should strengthen and catch up to the rest of the peers. Plus, if gold continues to perform it could be a great timing for investors of Nomad.

In your presentation you announce Nomad’s intention to pay a ‘meaningful’ dividend. How should we interpret that?

We would like to lead with that, meaning we would have a 2%+ yield. We think that should be the norm in the sector.

Are you predominantly targeting income investors?

After marketing a royalty company for 5 years, it’s a comment that always came back from investors. Most royalty and streaming investors love dividends, we want to make sure we cater to them.

Let’s take a minute to discuss your dividend plans. While it’s noble to aim for a 2% dividend yield, the yield is obviously dependent on the share price and if the Nomad share price increases to a multiple of the NAV in line with other players, paying a 2% could reduce the cash available for additional royalty or stream acquisitions. So if the share price starts to move in line with peers towards a valuation of 2-3X NAV, you won’t be able to maintain your 2% dividend yield. May we interpret your targeted 2% yield as a somewhat ‘loose’ target which will not be obtained if your share price moves to a multiple of more than 2X NAV?

Yes it will be difficult to maintain a 2% at all times, I would say that maintaining a leading dividend is part of our vision. It is not crazy to think that we would pay out 50% of operating cash flow. We want to make sure our investors benefit from immediate returns of capital on top of share price appreciation. The best way to have access to the broadest set of investors possible.

With regards to capacity, that is why we are already very advanced on the credit facility. Using a credit facility to buy, and then refinance in the market through the equity market will be our “go to” scenario. It gives an opportunity for the market to understand our path forward.

Any parting thoughts?

Nomad is a pretty easy story to tell. A young but very experienced management team and board that was part of building a royalty company, so we are here to replicate that again. We are focused on cash flowing opportunities first, and gold & silver exposure. It does not happen often to have the opportunity to get in a story at the ground floor and participate in the creation of a new company.

Conclusion

Nomad Royalty Company is the newest addition to the landscape of royalty companies. Coming out of the gate with a portfolio of Orion and Yamana assets, Nomad seems to offer exposure to a different batch of assets in South America and Africa. We have known Vincent Metcalfe for the better part of the past decade and he seems to be hungry to hit the ground running here.

Disclosure: The author has no position in Nomad Royalty Company. Nomad Royalty is not a sponsor of the website.