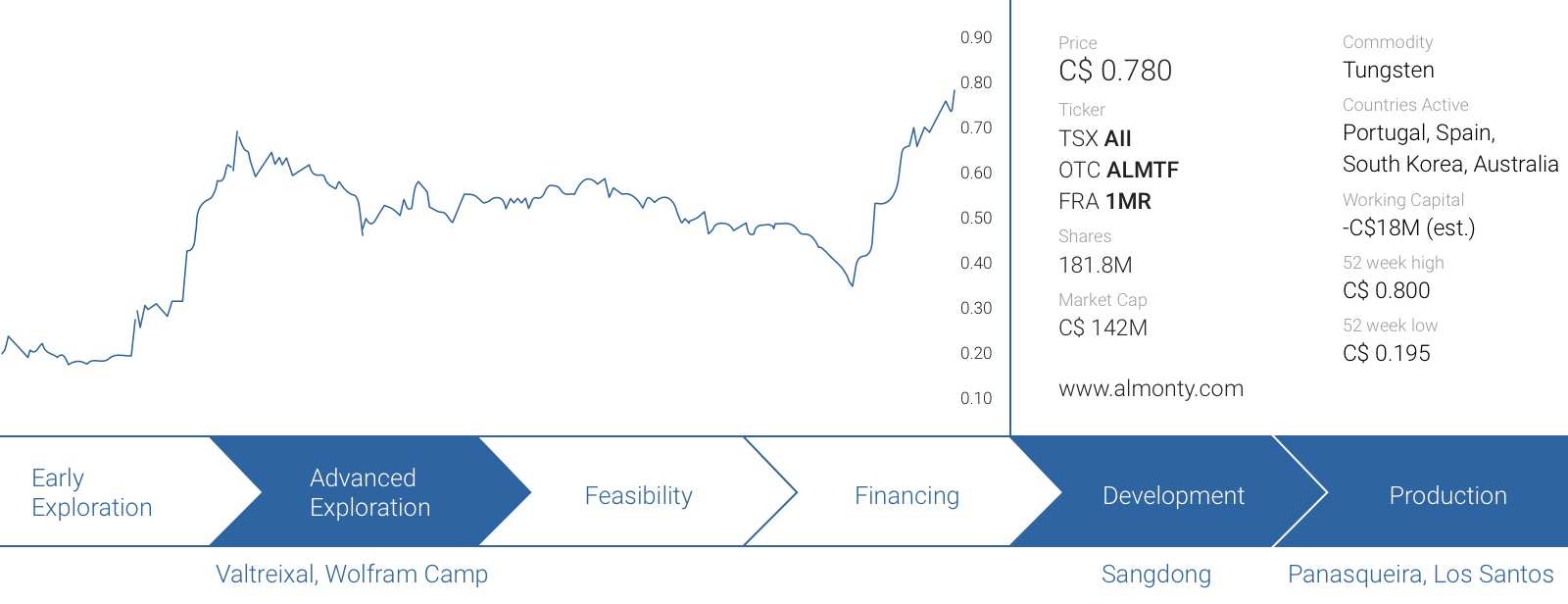

We have been keeping an eye on the developments on the tungsten market as several years ago, we were looking for potential producers with a short timeframe towards production. Unfortunately the tungsten price collapsed and several producers and explorers were caught in the downturn. There was no need to panic as the tungsten market was expected to rebound again. This has now happened, and Almonty Industries (AII.TO) seems to be in a position to take advantage of the current strength on the tungsten price market as the company owns a mix of producing and near-term production assets in the world.

We have been keeping an eye on the developments on the tungsten market as several years ago, we were looking for potential producers with a short timeframe towards production. Unfortunately the tungsten price collapsed and several producers and explorers were caught in the downturn. There was no need to panic as the tungsten market was expected to rebound again. This has now happened, and Almonty Industries (AII.TO) seems to be in a position to take advantage of the current strength on the tungsten price market as the company owns a mix of producing and near-term production assets in the world.

A quick introduction to the tungsten market

Tungsten isn’t exactly one of the best-known metals, so it’s perhaps a good idea to provide a brief overview of the applications for tungsten, the tungsten market, and why it’s an important element for western countries.

Tungsten rock gets processed into a variety of end-products, of which ferrotungsten, APT and tungsten concentrate are the best known variants. Both of the latter could then be used for alloys, carbides and metal, to improve the qualities of the metals they are being blended with. The most important use of all aforementioned applications would be the use of tungsten carbide which hardens a material to ensure it’s possible to drill or press steel. As it’s also used to protect military equipment, the range of applications is enormous. It’s not surprising to see 55% of all tungsten used in the United States is going to those carbide-based applications.

It’s an important metal for numerous industries. But there’s one big issue: supply chain risk. Looking at the 2017 production numbers assembled by the United States Geological Survey, the total mine production was 95,000 tonnes. China took care of the bulk of this number, as in excess of 83% (!) of the world’s tungsten supply is coming from China. Throw in an additional 3,100 tonnes (3.5%) from Russia, 1,100 tonnes (1.1%) from Bolivia and a few hundred tonnes from Rwanda, Mongolia and other second-tier countries, and you soon realize approximately 90% of the world supply on the tungsten market is coming from countries that don’t have to do the western world any favors.

Those western countries realized the potential risks to see a disruption on the tungsten supply side, and the European Union reacted by putting tungsten on the list of ‘critical raw elements’ with a substantial supply risk. As you can see in the next image, tungsten scores really high on the list of ‘economic importance and is a metal with a relatively high supply risk:

In fact, the European Union considers the potential supply risks for tungsten to be higher than the supply risk associated with cobalt and vanadium. Food for thought!

And just a quick line on the price setting mechanism for tungsten: although benchmark prices are expressed in mtu (one metric tonne unit is 10 kilograms), it’s important to realize these usually are the prices for APT (Ammonium Para-Tungsten), a ‘finished product’. What’s really interesting is that the concentrate producers (like Almonty) which are producing WO3 (tungsten concentrate at a benchmark grade of 79%), are paid based on the APT price, but at a 19-23% discount (Almonty applies a concentrate price which is 78% of the APT benchmark price). Just to explain this clearer: if the APT price is $300/mtu, concentrate producers will receive just $234 per mtu of concentrate.

Given the contraction on the tungsten markets, we don’t anticipate this discount to increase. In fact, it would make more sense to see that discount shrink as more buyers will be competing for the same supply of tungsten concentrate. According to Almonty’s official presentation, its floor price for the Sangdong project is $183/mtu, and this effectively would be the ‘net’ concentrate price, after applying the discount to the APT price. That being said, with APT prices trading comfortably over $300/mtu (indicating the current concentrate prices are approximately $260-275/mtu), we aren’t too worried about the specifics of the bottom price.

Almonty’s main producing projects

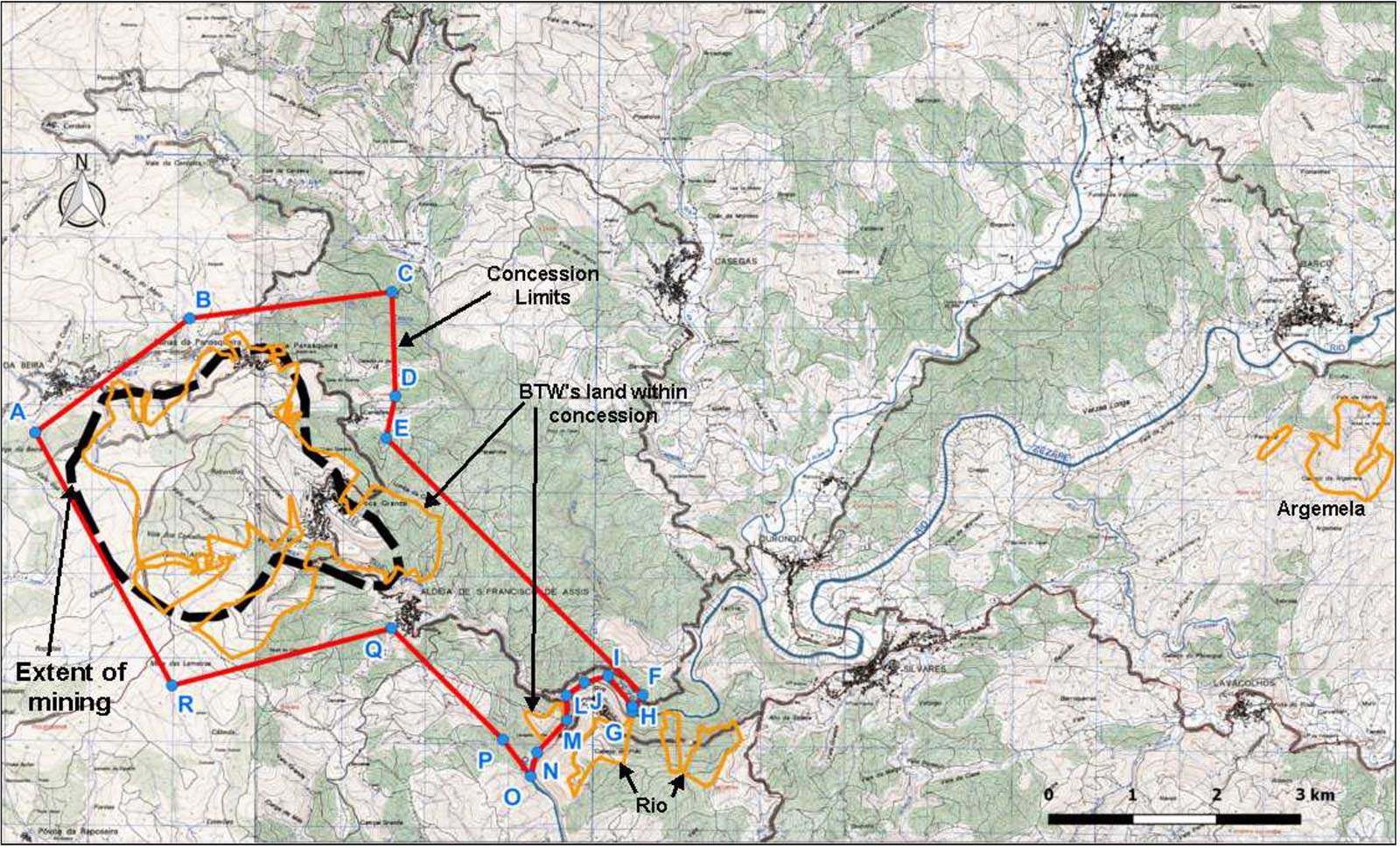

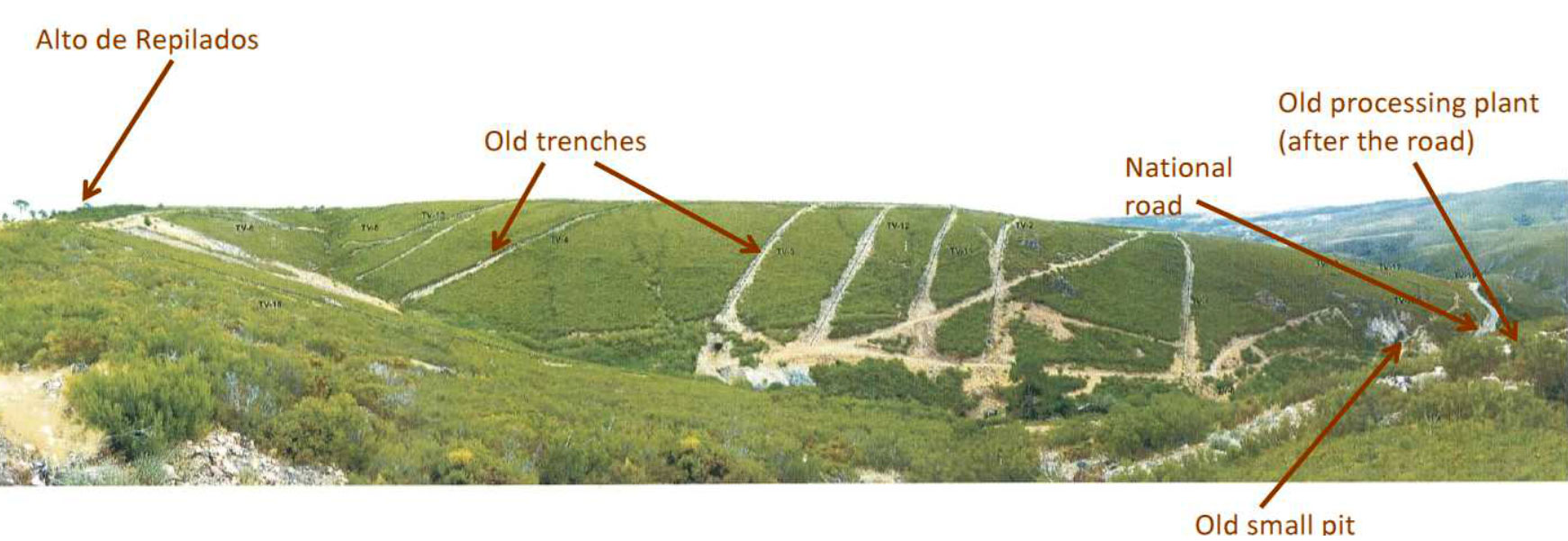

Panasqueira, Portugal

Panasqueira isn’t just a tungsten mine in Portugal, as it’s the main project that made Primary Metals big (Primary Metals was a tungsten-focused company that several members of Almonty’s team helped to build up). That company listed on the TSX Venture Exchange at C$0.15 but was sold to Sojitz for C$3.65 after drilling out the Panasqueira project, and making it appealing enough for a suitor. Primary Metals wasn’t the first company to detect tungsten at this location, as the district has been known for its tungsten occurrences (and production) since 1896.

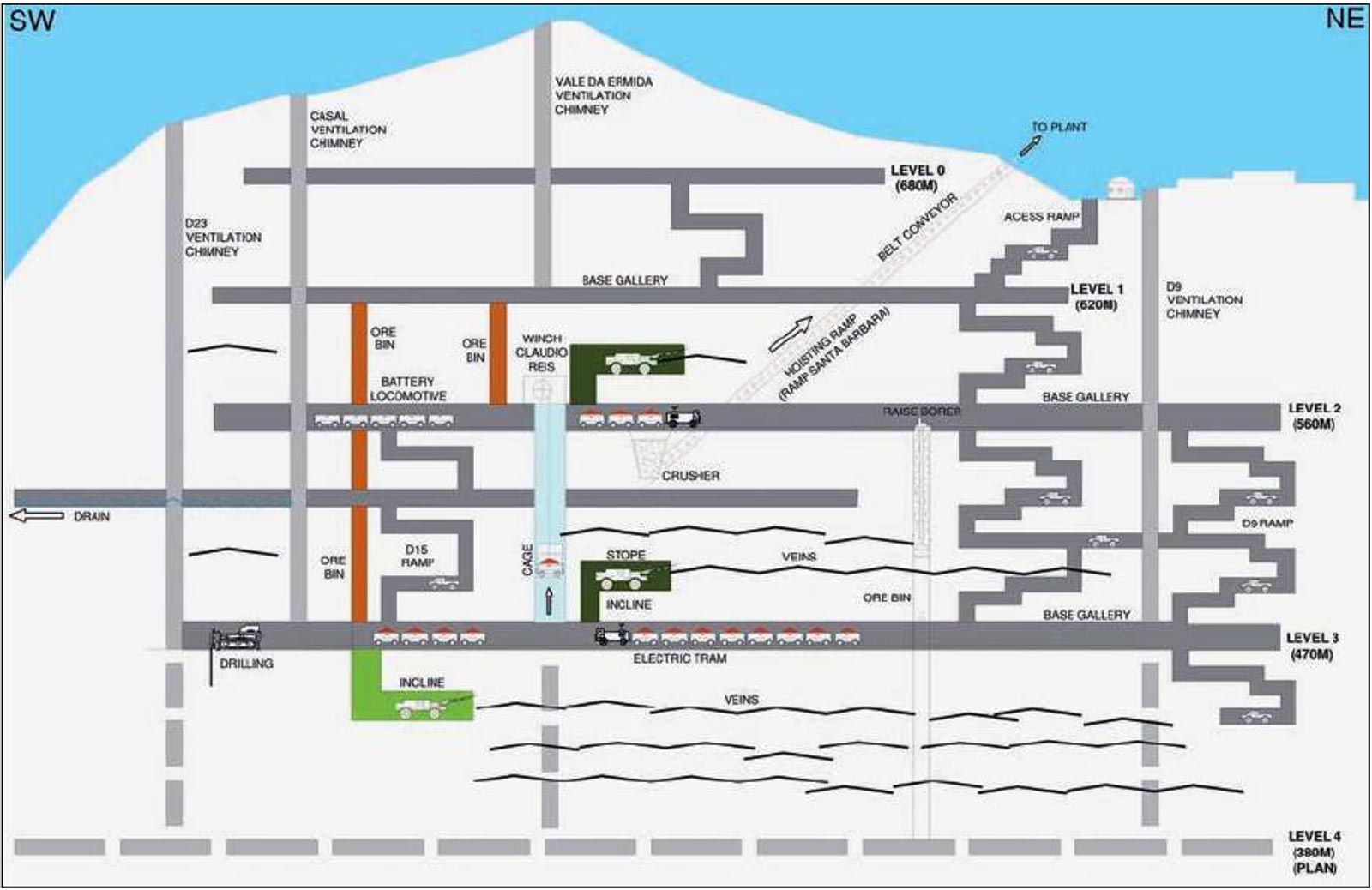

The project has been switched hands several times, and is now owned again by Almonty Industries, which owns 100% of the property. Panasqueira is located pretty much right in between major cities Porto and Lisbon in the Serra da Estrela mountain range. The total size of the concession is almost 2,000 hectares, and could easily be reached by the excellent road infrastructure. A nicely paved highway takes you to approximately 40 kilometers from the property where after normal secondary (but paved) roads pretty much take you all the way up to the mine gate. The Panasqueira mine is currently hooked up to the electrical power network, and Almonty is paying just 0.05EUR/kWh for its energy needs.

Not only is the power price relatively low (for European standards), the Panasqueira mine doesn’t need as much power as comparable projects: there’s no need to grind the ore whilst there also is a high level of ‘natural’ ventilation in the underground mine.

Contrary to what you might think, it’s not necessary to have a very high tungsten grade to be a successful underground mine. The average grade of the resources (and reserves) at Panasqueira is just 0.23%, and Almonty Industries has been able to make that work as the quartz veins are a ‘pleasure’ to work on: there’s very little ‘support’ needed to ensure the safety of the stopes.

The mine is operating on a 2-shift structure, and just 5 days per week, resulting in a production rate of 54,000 tonnes of rock per month. That’s a pretty good performance considering one shift consists of just 6 hours where the employees effectively work (approximately 2 hours are lost on transportation from surface to the stoping areas, as well as the lunch/dinner break). After the final shift (around 11 PM), the mine gets ventilated. It all sounds really old-school, but appears to be very effective.

The tungsten concentrate from Panasqueira is highly sought after, as even the official technical report calls it ‘a very high grade concentrate, almost pure wolframite’. The process is pretty straightforward: crushing, screening and sand tables are pretty much the only elements needed to get from ‘run of mine’ ore to a high grade concentrate. What’s interesting is the fact Panasqueira also contains (very small) copper and tin circuits. Approximately 100 tonnes of copper (in concentrate) and 70 tonnes of tin concentrate are produced on an annual basis. This doesn’t move the needle, but it’s an interesting ‘fait-divers’.

With a tungsten price of $340/mtu, the price received by concentrate producers is approximately $265/mtu. That sounds great, but it also means the head grade of this underground mine (0.23%) represents a gross rock value of just US$61M. Applying the 84% recovery rate reduces this to just $51/t.

If you would be operating an underground gold mine in Ontario or Québec, this project would be dead from the start. But thanks to the low production expenses (with an operating cost of just $22/t ore), the total operating cost is relatively low as well. According to the technical report, the break-even cut-off rates range between 0.11% and 0.14% WO3. With an average production rate of 70,000 mtu per year (66,000 mtu in FY 2016, 80,800 mtu in FY 2017), Panasqueira isn’t a huge mine, but it pays the bills. It’s also interesting to see how the total WO3 production already reached 45,000 mtu in the first half of the financial year, so we think Almonty has a good shot at producing more tungsten than last year.

Los Santos, Spain

Almonty’s second producing mine is the Los Santos tungsten mine in Spain’s Salamanca province. The mine has been in production for approximately 10 years now, and is recovering the tungsten from a relatively large open pit operation. The total resource estimate (measured + indicated + inferred) contains 4.1 million tonnes of rock at an average grade of approximately 0.27% WO3. The measured and indicated resources contain 2.2 million tonnes at an average grade of 0.29% WO3, for a total of 6,316 tonnes of tungsten (approximately 630,000 mtu). Note these resources were calculated in the summer of 2015, so we would have to take 3 years of depletion into account.

At a production rate of approximately 500,000 tonnes per year, we expect the Los Santos mine to have a remaining mine life of 2 years based on the ‘old’ measured and indicated resource, and 4 years if we would a 50% conversion rate of inferred resources to the measured and indicated category.

The average recovery rate is expected to be 60-65%, and applying a 62% recovery rate and an average grade of 0.29% WO3, the 520,000 tpa processing rate should result in an annual production of 85-95,000 mtu of tungsten.

Once the open pit has been mined out, Almonty could investigate going underground, and preliminary calculations seem to indicate the applicable cutoff grade for an underground operation at Los Santos would be approximately 0.24% WO3 using a tungsten price of $370/mtu (APT-basis). Additionally, the 2.1 million tonnes of tailings contain an average grade of 0.15% WO3 and could be reprocessed as well.

The icing on the cake? The Sangdong Development project in South Korea

Whilst Almonty Industries is able to immediately capture the benefits of the higher tungsten price by selling the concentrate from its two producing mines, it has another important iron in the fire. Some readers might remember we discussed the Sangdong tungsten project several years ago, when it was still owned by a company called Woulfe Mining. Almonty has now gained total control over the asset, and it’s the company’s development asset with the highest priority.

At the end of last year, Almonty has already secured an EPC agreement with POSCO for the development activities at the Sangdong mine. POSCO E&C indeed is a subsidiary of the well-known POSCO conglomerate, headquartered in South Korea. This could ensure a very smooth construction period (considering the corporate culture of the EPC contractor and the local labor force will be streamlined), and POSCO has already started the demolition activities on the old Sangdong mine site.

As the project is fully permitted, the final piece of the puzzle consists of getting the financing package in place. Given the current strength on the tungsten market and the high-margin nature of the Sangdong project (see later), the US$85M shouldn’t be too hard to find. Once funding has been secured, the 18-month construction period will start, followed by a 6-month commissioning process.

With APT prices trading at $340/mtu (resulting in an expected concentrate price of $265/mtu WO3), the Sangdong project could very well be one of the highest-margin projects in the world as the feasibility study expects the cash cost per mtu to come in at less than $125, resulting in an operating margin of $140-150/mtu. In the first few years of the mine life, the throughput will be fixed at 640,000 tonnes per year, but it’s Almonty’s intention to increase this to 1.2 million tonnes per year. The feasibility study also shows an average concentrate production of 5.500 tonnes per year, and applying the expected grade of 65% tungsten in the concentrate, the total annual production would be just over 350,000 contained mtu/year.

And that’s the big prize. Should the Sangdong mine indeed reach full production, early next decade, the operating cash flow from the mine would be in excess of US$50M per year (and get pretty close to C$65M using an USD/CAD exchange rate of 1.25). Almonty has published a feasibility study but the US$70M after-tax NPV8% is definitely outdated as this study was published in 2016 and uses a different mine plan with a lower production rate.

The reserves are supporting a mine life of approximately 6-8 years, but once the project starts generating cash flow, we would expect Almonty Industries to spend several millions per year on exploration and upgrade drilling. The inferred resource is almost 10 times as large as the reserves, so it shouldn’t be too difficult to convert a part of the inferred resources to reserves which will result in an updated mine plan. Even converting just 20% of the inferred resource would increase the mine life by approximately 10 years. It’s a no-brainer to spend some money on exploration.

The development pipeline remains filled with Valtreixal and Wolfcamp

Although the Valtreixal and Wolfcamp projects aren’t really moving the needle for Almonty, we would like to briefly highlight these assets as they confirm Almonty’s development pipeline contains more than just Sangdong.

Valtreixal

The Valtreixal project is a tungsten/tin project in Spain, literally within walking distance from the Portuguese border. Tungsten/tin projects are pretty common in that (wider) region as for instance the Bejanca project in Blackheath Resources’ (BHR.V) project portfolio appears to be similar.

The resources at Valtreixal are pretty small: the previously filed technical report discussed a 2.55 million tonne reserve. The average grade isn’t particularly high (0.25% WO3 and 0.12% tin), but what’s really interesting is the existence of a large inferred resource (15 Mt at a lower WO3 grade, but a stable tin-grade) and the fact that this deposit could be amenable to a simple gravity method (as long as the rock gets crushed to a size smaller than 1 millimeter). According to the study (which was completed on a PFS-level), the recovery of the tungsten is expected to be 55% whilst 65% of the tin will be recovered.

Those percentages appear to be low, but keep in mind that’s fine, as mining a deposit like this will always be a trade-off based on capital efficiency: higher recovery rates are possible, but these improvements will result in a higher capex and opex and could actually result in a lower IRR and NPV.

Just like all other projects in Almonty’s portfolio, Valtreixal isn’t a ‘new’ project, and although legend has it the Romans were mining there, the first clear evidence of mining goes back to 1883 (open pit) and 1920 (underground).

The potential start-up date of the Valtreixal project coincides with the potential end of the open pit mine life at Los Santos. It’s not unlikely Almonty will be able to move equipment and plant (and some parts of its labor force) to Valtreixal, which would drastically reduce the initial capex.

Wolfram Camp

The Wolfram Camp project is located in Queensland, Australia, and used to be an open pit producer of tungsten before the mine was shut down in 2016 due to the low tungsten price, and the company has been working on a new plan ever since. During the shut-down, Almonty has been working on the tailings facility as well as installing new equipment at the mill, which should improve the economics of processing the tungsten-bearing rock.

According to the company’s most recent MD&A report, Almonty seems to be hinting at a production restart by the end of this year (only if the tungsten price continues to cooperate). According to the 2017 technical report, the Wolfram Camp project contains 0.5 million tonnes (at 0.23% WO3) in the indicated resource and an additional 1.9 million tonnes at 0.31% WO3 in the inferred resource. The total amount of tungsten on an in-situ basis is just over 700,000 mtu. So once the Wolfram Camp project gets going again, Almonty should be able to add a third producing asset to its portfolio (timing based, Sangdong will be the 4th producing project).

We expect to see an update from Almonty on its plans to re-open the Wolfram Camp mine sometime this summer.

Share structure and management

The current share count of Almonty is approximately 181.8M shares, giving it a market capitalization of C$142M. It’s interesting to see Almonty Industries has implemented a Normal Course Issuer Bid, and actually repurchased 313,000 shares (for cancellation) as part of this NCIB. As Almonty’s situation continues to improve, it’s not unlikely to see Almonty stepping up the pace of its buyback program.

Lewis Black – Director, President and CEO

Mr. Black is currently a Partner of Almonty Partners LLC and has extensive experience in the tungsten mining industry. From June 2005 to December 2007, he was Chairman and Chief Executive Officer of Primary Metals Inc., an Exchange listed tungsten mining company, and he was formerly head of sales and marketing for SC Mining Tungsten Thailand. Mr. Black is a Member of the Executive Committee of the International Tungsten Industry Association.

Mark Gelmon – Director & CFO

Mr. Gelmon obtained his Bachelor of Arts degree at the University of British Columbia and subsequently attained his Chartered Accountant designation in 1995 and is a member of the Chartered Professional Accountants of B.C. Mr. Gelmon has provided his expertise to several TSX Venture Exchange listed companies in the capacity of director, chief financial officer and consultant. His background as a CPA, CA, provides the Company with the necessary skills required for financial management, reporting operating results to the Board of Directors, liaison with financial institutions, and compliance with today’s complex regulatory reporting requirements.

Daniel D’Amato – Director

Mr. D’Amato is currently a Partner of Almonty Partners LLC and has extensive experience in the finance industry specializing in portfolio management and private equity. He began his career on Wall Street with Bear Stearns where over nearly a decade he became Managing Director. In 2005, with business partner Lewis Black, Mr. D’Amato co-founded Almonty. From June 2005 to June 2007, he served on the board of directors of Primary Metals Inc., an TSX Venture Exchange listed tungsten mining company, of which Almonty was the majority owner.

Ore Extraction & Panasqueira Mine

The financial results: Almonty generated a positive free cash flow in the most recent quarter

Thanks to new offtake contracts with its customers at Panasqueira, we’ll see a substantially higher revenue per produced metric tonne unit of tungsten in 2018. Whereas the company entered into fixed price contracts to sell its tungsten concentrate at $210/mtu in FY 2017, the average price for the current calendar year have been set at $280/mtu. So based on a production rate of 80,000 mtu of tungsten at Panasqueira, the revenues are expected to increase by US$5.6M.

This was immediately noticeable in the company’s financial results. The EBITDA increased to C$5.8M in the first quarter of the current calendar year, which is a great improvement compared to the C$2.8M generated in the final quarter of 2017. On top of that, Almonty Industries was now free cash flow positive in the first quarter of the calendar year:

The operating cash flow excluding changes in working capital increased to C$5.6M, and Almonty needed just C$2M to cover its capital expenditures, leaving C$3.6M or C$0.02 per share on the table (the reason why Almonty repaid just a few hundred thousand dollars of its net debt could be found in those working capital changes, as some of the cash was tied up in the increased inventory levels.

But at an annualized free cash flow result of C$14M per year, Almonty should be in a position to quickly repair its balance sheet (which showed a working capital deficit of C$18M). AII is already on the right track, as the working capital deficit has decreased from almost C$32M as of at the end of September of last year, as the company was able to convert short-term debt into long-term debt.

As Almonty has locked in the higher tungsten price for an entire year at Panasqueira (and we expect the company to do the same with the Los Santos tungsten production), the C$50M in net debt has now become very manageable again. And let’s face it; the debt is pretty cheap as the average interest rates range from 2.06% to 3.81%.

The majority of the debt (C$34.7M) will have to be refinanced in 2019, and if the tungsten price remains this strong, the refinancing should be a non-event. Especially when the high-margin production from the Sangdong mine will come online from 2020 on.

Conclusion

The tungsten price remained depressed over the past few years, but appears to be taking up its place in the sun again. The APT-price has increased to in excess of $300/mtu again, and seems to be trading very resilient in a $325-350/mtu price range. This means the concentrate producers will receive $255-275 per mtu of tungsten contained in the concentrate.

Almonty is in the final straight line to put its financing package together for the Sangdong mine in South Korea, and that will be a game-changer for the company. Based on the expected production costs and looking at the current tungsten price, the operating cash flow could very well exceed US$50M per year (based on the 1.2Mtpa scenario).

Tungsten is still flying under the radar, but we expect end-users scrambling to secure reliable tungsten supplies within the next 24 months.

Disclosure: Almonty Industries is not a sponsor of this website, but we were compensated by a third party. We have no position. Please read the disclaimer