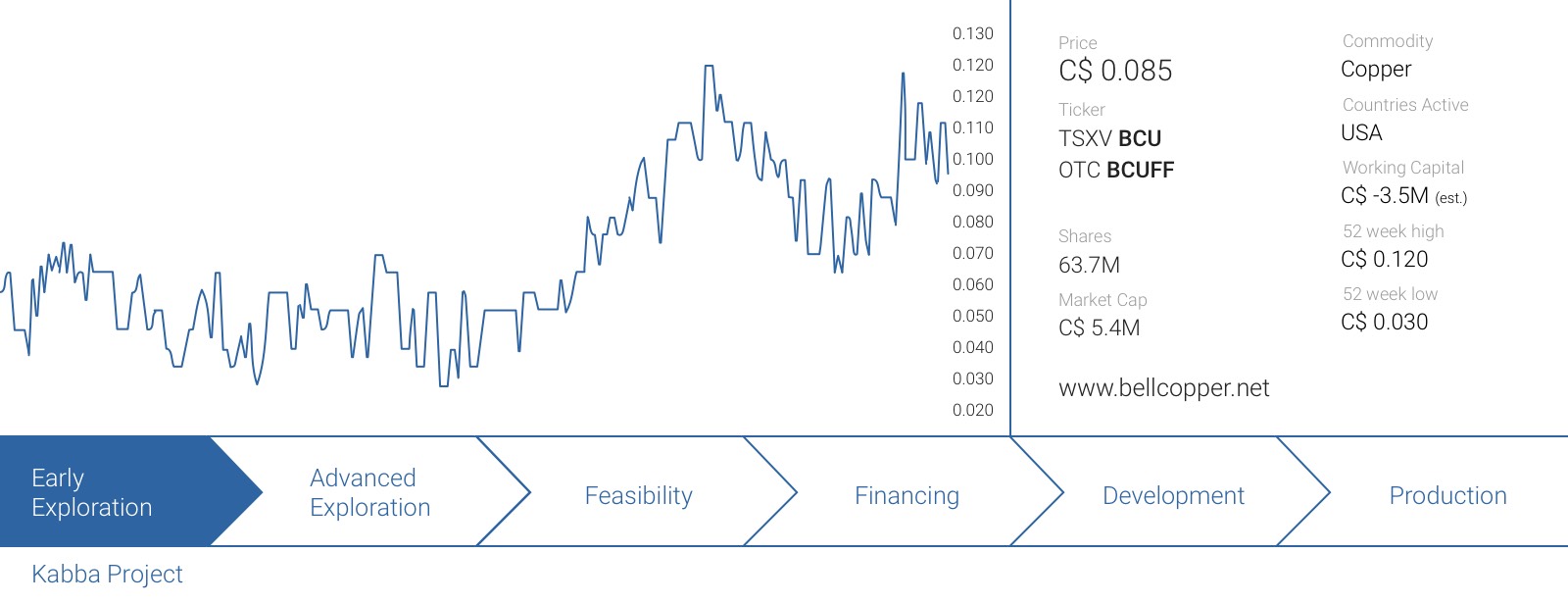

Bell Copper (BCU.V) has a decent shot at becoming one of the hottest exploration stories of the second half of this year, as its joint venture partner Rio Tinto (RIO) is gearing up to start a drill program on Bell Copper’s Kabba copper porphyry project in Arizona.

For now, Bell Copper and Rio Tinto are trying to confirm a theory from Bell’s CEO Timothy Marsh, but after a 2.5 hour chat with Marsh in Arizona last month, we now share the conviction Kabba hosts a very large copper porphyry system. Drill rigs are dispatched to Kabba as we speak, and the Rio Tinto / Bell Copper joint venture will focus on size and grade in the upcoming drill program.

Bell Copper cleaned up its legacy debt whilst retaining full ownership of Kabba

Back in 2012, Bell Copper was pretty much bankrupt as it owed Macquarie a bunch of money whilst the assets could be foreclosed at any day. It worked out a plan with Macquarie and was able to pay Macquarie with the proceeds of the sale of the company’s two other projects.

A solid move as this allowed Bell Copper to be debt-free and fully focus on its Kabba exploration project and although it still is in an early stage, it has the potential to be a company-maker.

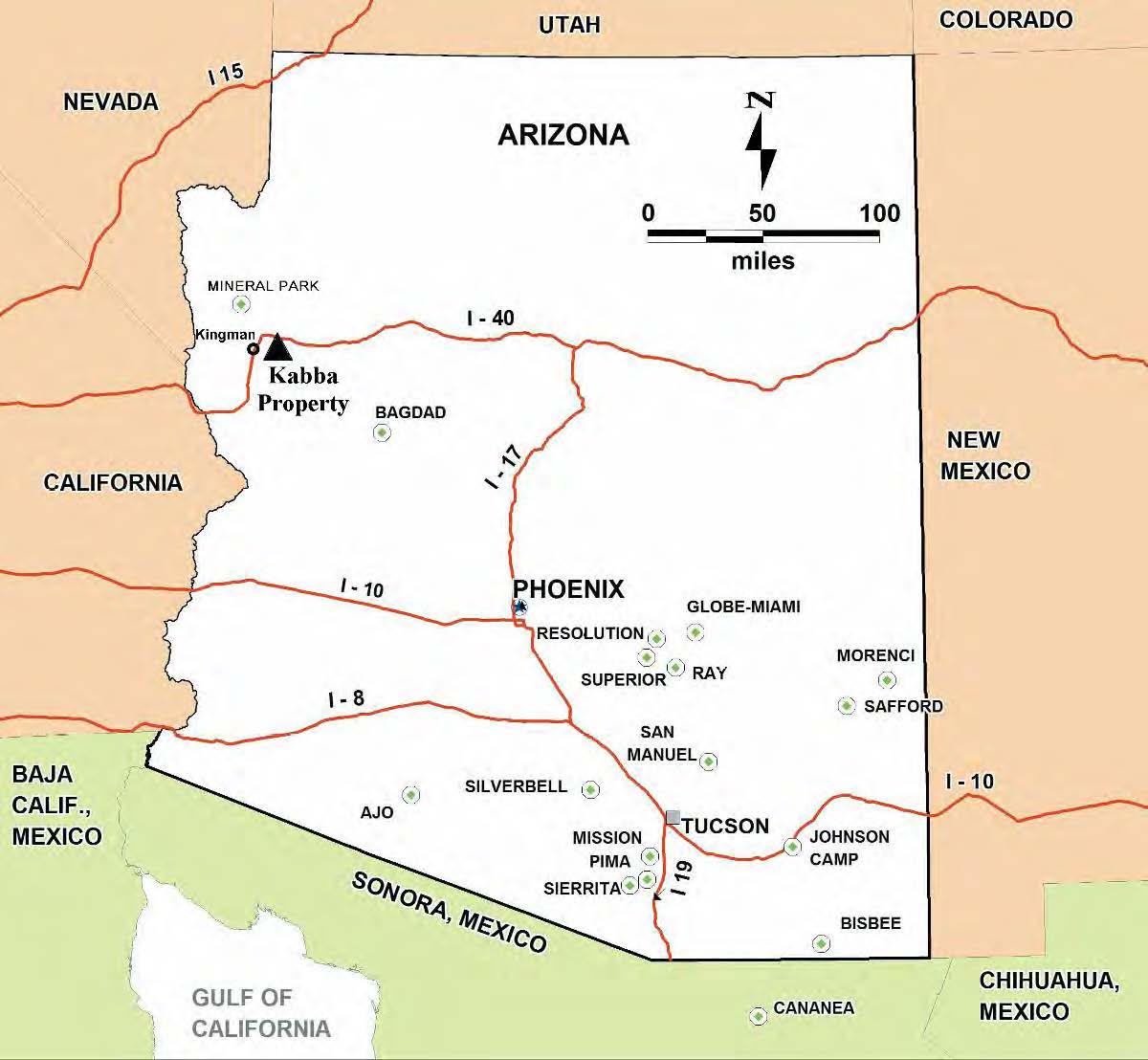

Kabba is located approximately 250 kilometers northwest of Phoenix and about 30 kilometers to the Southeast of Kingman, right in the middle of a historically very prolific copper trend with the Mineral Park mine (ex-Mercator Minerals) and the Bagdad copper mine (Freeport McMoRan) as best-known large copper producers, whilst Rio Tinto is getting ready to advance the underground Resolution mine towards production as well. Needless to say the Kabba land package is located right in the middle of one of the hottest copper districts in the USA (and the world).

There have been a lot of very intriguing copper discoveries (and project developments) in the past few years, but virtually none ticked all the boxes as they had to deal with either geopolitical unrest, being located in a remote area (which jacks up the development cost) or anti-mining lobby groups.

That’s not the case at Kabba. The State of Arizona has been and still is one of the most important copper mining areas in the world, and the locals really do ‘understand’ mining, and accept mining operations to be a part of their economy. So we wouldn’t expect any locals to protest against the mine, nor would we expect the USA and the State of Arizona to object against a potential new copper mine and the accompanying jobs.

Infrastructure was the final box that has been ticked. A high voltage power line is located just a few kilometers from the property (a simple substation would be sufficient), whilst Bell Copper encountered ground water during its previous drill programs and thinks there might be a substantial aquifer on the western side of the land package.

So, yes, Kabba ticks all the boxes you’d like to see ticked, but why is the company exploring right there, in the middle of nowhere?

The exploration theory…

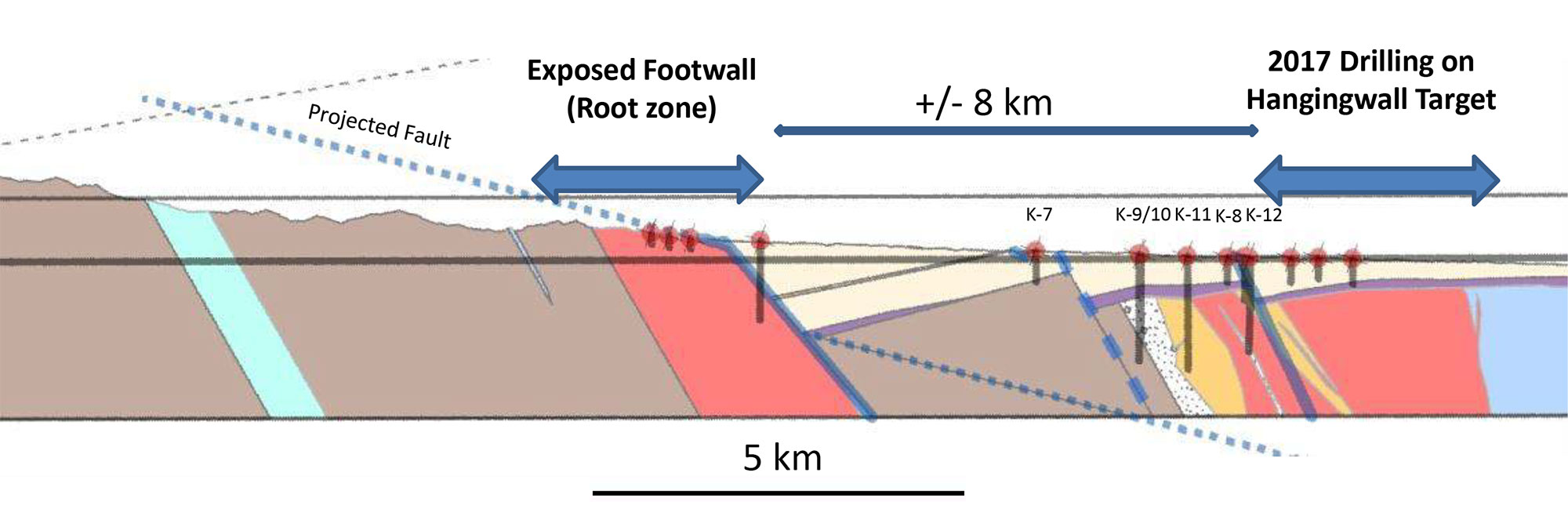

This specific porphyry system seems to consist of a footwall and a hanging wall, and the footwall generally consists of a large ‘blanket’ of molybdenum, with a copper-heavy system on top of that. To explain it with Tim Marsh’ own words: “The geometry before faulting is like a carrot, with a tall cylindrical stem (not a “blanket”) containing molybdenum and a “shell” or half-cantaloupe rich in copper on top of that. At Kabba, because it is faulted, the stem is in the footwall piece and the cantaloupe is in the hangingwall piece.”

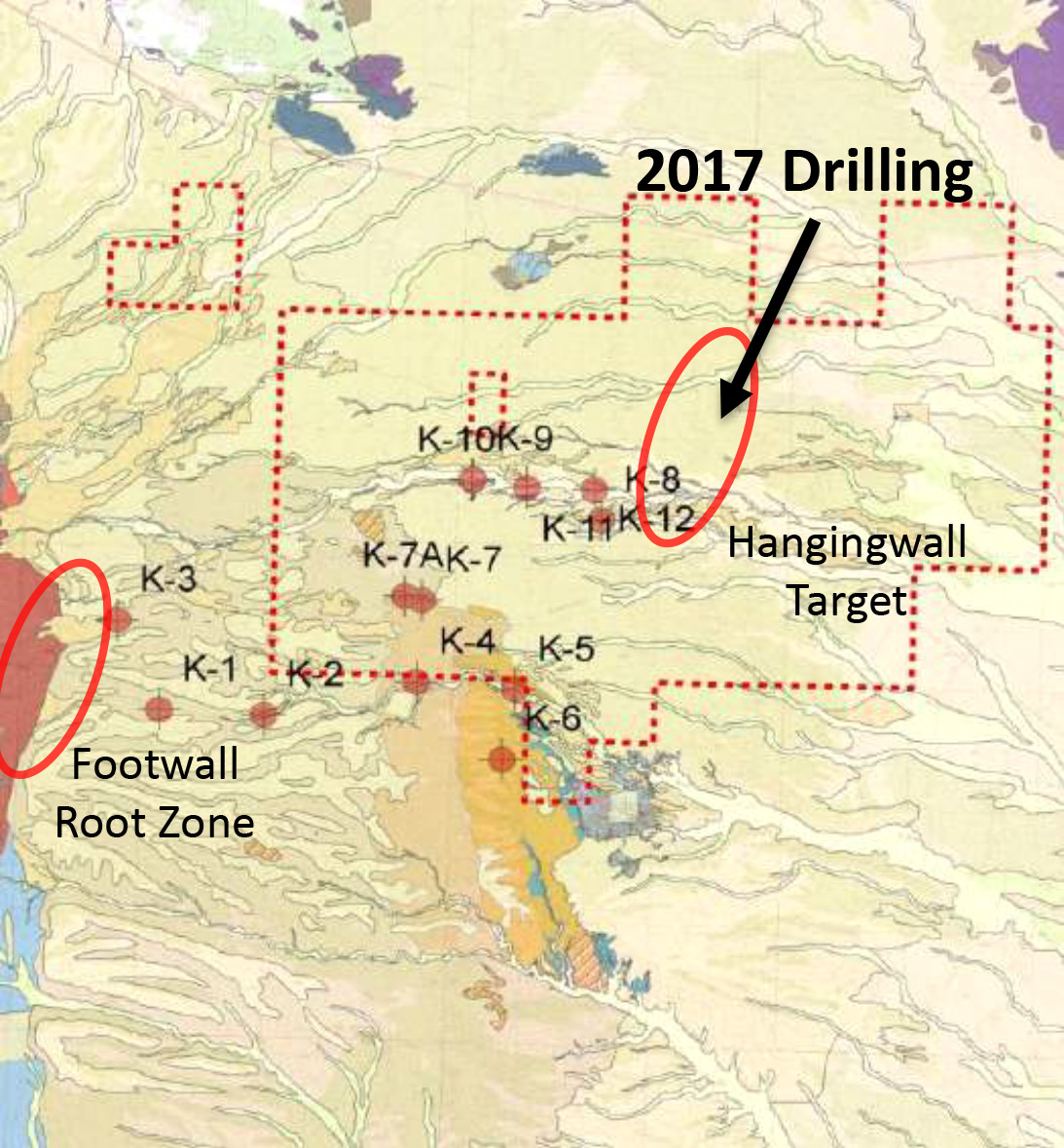

Several years ago, CEO Tim Marsh discovered a huge ‘sea’ of Molybdenum on the Kabba project area, and developed the theory the Moly-zone could have been the footwall part of a much larger porphyry zone. It took years of exploration and several drill holes, but Marsh has eventually been proven right as the company discovered the ‘missing’ hanging wall approximately 8 kilometers to the east of the footwall zone. Both zones have an identical type of mineralization, as you can see in the next image.

Finding the hanging wall zone wasn’t easy, but Bell Copper gained a lot of useful information along the way, as the company continued to move towards the east with its previous drill holes.

The further towards the east, the more the continuity and the strength of the alteration and copper mineralization was improving and Bell’s most recent drill hole, K-12, was the best one so far. At hole K-11, the geo’s working on the project detected a clear transition zone marking the transition from footwall to hanging wall zones, so it certainly does look like Bell is really zooming in on the ‘hot spot’ now.

Why should you care about all this?

1. Because Rio Tinto Cares

Tim Marsh’ exploration theory didn’t only convince us, but it was also sufficient to convince Rio Tinto’s exploration subsidiary, Kennecott Exploration, to throw some money at it.

In April last year, both companies signed a joint venture agreement whereby Rio Tinto can earn a 75% stake in the property. It has already earned an initial 5% stake upon signing the deal, and the commodity major will now have to spend US$3M on exploration to increase its stake by 51% to 56%.

US$3M isn’t a lot of money when you’re chasing a large copper porphyry system (but it would have been ‘mission impossible’ for Bell Copper to have raised the cash at the 1 cent level it was trading at when the option agreement was announced), and we would expect Rio Tinto to complete its earn-in to 56% by the end of this summer. The completion of this milestone will trigger another possibility for Rio Tinto to increase its stake in Kabba, and it could acquire an additional 19% (to earn a total of 75%) by completing US$10M on exploration expenditures.

We realize some investors won’t be too impressed with this deal, thinking ‘if the odds are really this good, why did Bell Copper sell a 75% stake for just US$13M in exploration expenditures?’.

First of all, it’s better to have 25% of something potentially viable rather than remaining in semi-hibernation, and it’s pretty much guaranteed Bell Copper would have been unable to raise the initial US$3M (C$4M) at one or even two cents. Raising an additional US$10M would also have been an extremely difficult task, so we feel Bell’s management team has made the right decision. At least the project is now moving forward, and having a credible partner like Rio Tinto validates Marsh’ exploration theory

2. The total size could be absolutely massive

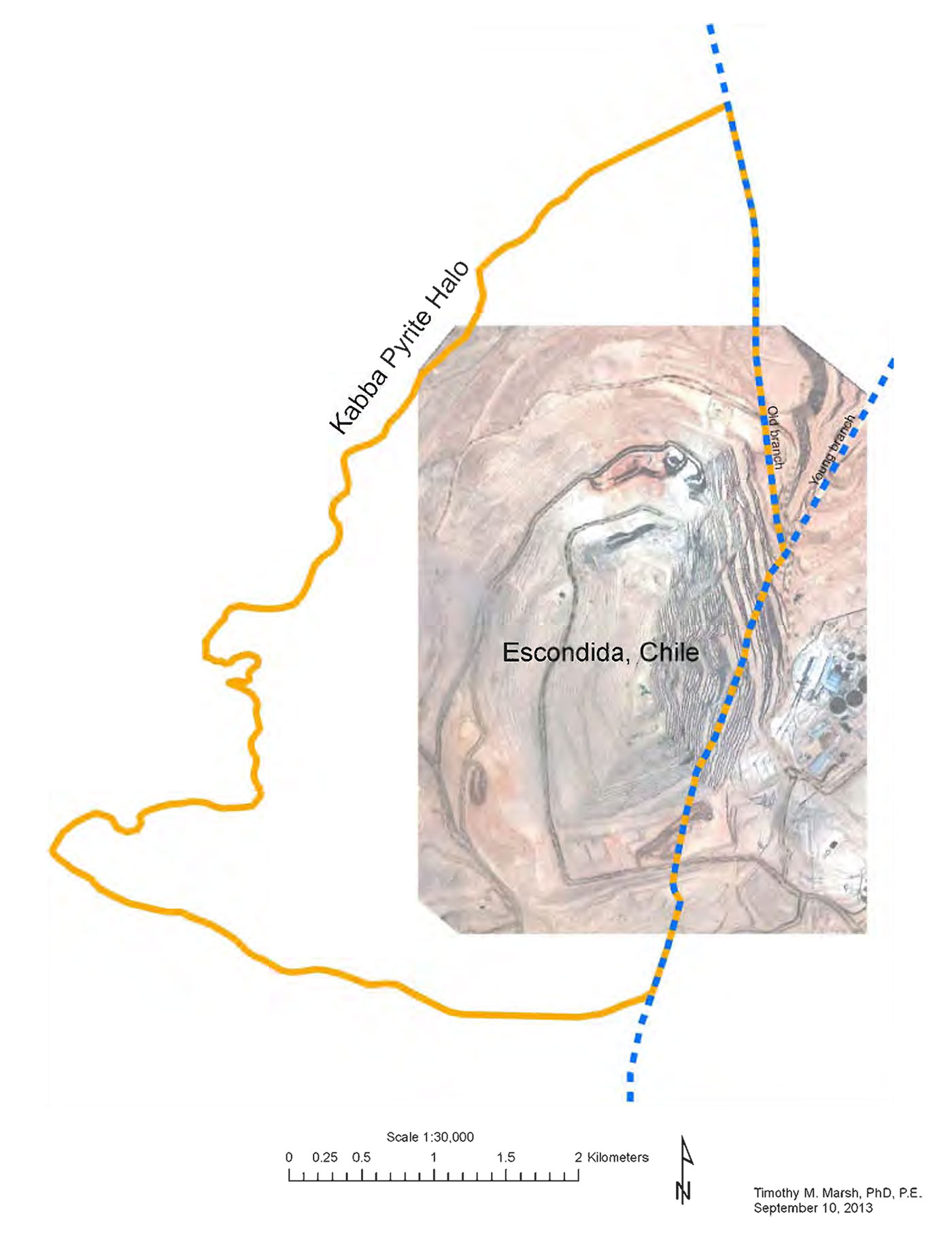

Looking at the size of the footwall zone, the hanging wall which is now being chased could be massive. The company has provided a nice image of the size of its pyrite halo compared to the total size of the Escondida copper mine in Chile, and as you can clearly see, the geological footprint of Kabba is larger than Escondida was.

With a total surface area of 3 kilometers by 5 kilometers (supported by the size of the molybdenum footprint), the system is absolutely huge and could probably best be compared with Bingham Canyon (3.2 billion tonnes) and Cananea (5.1 billion tonnes).

The proof will be in the pudding, that’s for sure, but based on the size of the pyrite shell, we aren’t talking about discovering a few billion pounds of copper, but about tens of billions of pounds. Just to give you an idea, 1 billion tonnes of rock at an average grade of 0.5% copper equals 11 billion pounds of copper on an in-situ basis.

What’s next?

We anticipate to see the drill rigs starting to turn soon, but it will take quite a few weeks before seeing the first assay results. Once those are published, all odds are off. Should drilling already confirm the size of the zone and an economical copper grade, Rio Tinto will very likely accelerate its earn-in deal and won’t need the entire 8 years to get to a 75% stake.

We obviously can’t predict the future and only time will tell.

Management team

Tim Marsh – CEO, Director

- PhD Stanford University – Ore Deposits & Exploration BS Colorado School of Mines — Geological Engineering

- 27 year career in mine geology and exploration, focus on porphyry copper deposits

- Over 8 years as Qualified Person for Bell Copper Corporation

- Built value through exploration (Granduc, La Balsa, Sombrero, Van Dyke)

- Former Chief Geologist for Resolution Copper Company, a Rio Tinto/BHP JV company

- Former Cortez Joint Venture Geologist for Kennecott Minerals Co., Nevada

- Former Manager of Exploration at AMT International’s Copper Creek property, Arizona

- Pit and exploration geologist for 6000 t/d Cactus Gold Mine

Geoffrey Snow – Director

- Former Director, Bell Copper Corporation

- PhD University of Utah – Geology

- Partner – Barranca Resources

- Adjunct Professor of Geology – Colorado School of Mines

- Leads Exploration Management Courses at CSM, CU, and PDAC

- Nearly 50 year career in mining business

- Former President of Noranda Exploration

- Former Resident Geologist, Climax Mine, Colorado

Glen Zinn – Director

- Former Chairman, CEO, and President of Bell Copper Corporation

- +45 years of mining industry experience and senior executive positions

- Former VP Corporate Development, Hecla Mining Company

- Former Chief Geophysicist for Union Oil/Molycorp

- Member of the National Strategic Materials and Minerals Program Advisory Committee under Ronald Reagan

- Anaconda Company Geophysicist

- Postgraduate certificates from MIT, Stanford, and Northwestern University

- BS Michigan College of Mining & Technology — Geol. Eng. + Geophysics

Annie Storey – CFO, Corporate Secretary, Director

- Chartered Accountant

- BBA Simon Fraser University — Bachelor of Business Administration (Finance and International Business)

- Over 25 year career in accounting, auditing, financial reporting and corporate services for Canadian and US public and private companies operating around the world in mining, oil and gas, technology, entertainment, manufacturing, real estate and biotechnology.

- Proficiency in IFRS, US GAAP, and ASPE accounting standards

- Experienced with Canadian and US tax regimes.

- Committee member — ICABC Practice Review & Licensing Committee

- Board member — CICA Practitioners’ Technical Advisory Board

- Former Audit Partner — MNP and Auditor/Accountant – KPMG

- Former teaching and controllership positions

- Board member on various non-profit organizations

Conclusion

When keeping an eye on Bell Copper, we will be focusing on two things. A) is the porphyry system large enough? And B) is the average grade economical?

A will be relatively easy to answer. Based on the size of the footwall zone, there’s no doubt a huge porphyry system has shifted towards the east. The total size of the pyrite shell is approximately 3000 by 5000 by 500 meters, resulting in a total tonnage of 20 billion tonnes. Approximately 5-15% of this shell will contain the porphyry target, which means we would expect a size of 1-3 Billion tonnes.

The main question will be grade-related. Will the grade be high enough to warrant the start of economic studies? Looking at other underground porphyry mines, it looks like we would need to see an average copper grade of 0.65-0.7% and that’s the percentage you’ll need to keep in the back of your mind when the assay results start rolling in. And as explained above, 1 billion tonnes of rock at an average grade of 0.7% copper contains approximately 15 billion pounds of copper.

Bell Copper could be an absolute high risk/high reward play. We firmly believe there’s ‘something’ there, but we don’t know if the porphyry zone will be viable. Should the viability be confirmed, Bell Copper’s remaining 25% could be very valuable.

Disclosure: Bell Copper currently isn’t a sponsor of the website but that might change soon, we have a long position. Please read the disclaimer