Canterra Minerals (CTM.V) was previously known for its gold exploration in central Newfoundland, when a new opportunity presented itself. While the company had been assembling a land package of base metals projects (with an existing resources) in the same part of central Newfounland adjacent to its process effective gold claims, Canterra was able to acquire the zinc assets of unlisted Buchans Resources and is now a dominant player in the Newfoundland base metal market.

And Canterra’s land package isn’t just a few acres of moose pasture. The company’s total resources now stand at 25 million tonnes of rock (23.4 million tonnes in the indicated resource category and 3.2 million tonnes in the inferred resource category to be exact) which suddenly catapulted the company to the status of a rather important regional player.

The company’s main metal is now zinc. That’s not a coincidence, as zinc was named one of the most critical minerals in Canada. Although the zinc sector hasn’t been a great subset of the base metals space to be invested in in the past few years, plenty of (zinc) companies haven’t performed well. But after a few years of being in the doghouse, there appear to be signs the level of interest in zinc might be returning. And the sharply lower TC/RC charges applied by zinc smelters worldwide is a very interesting development.

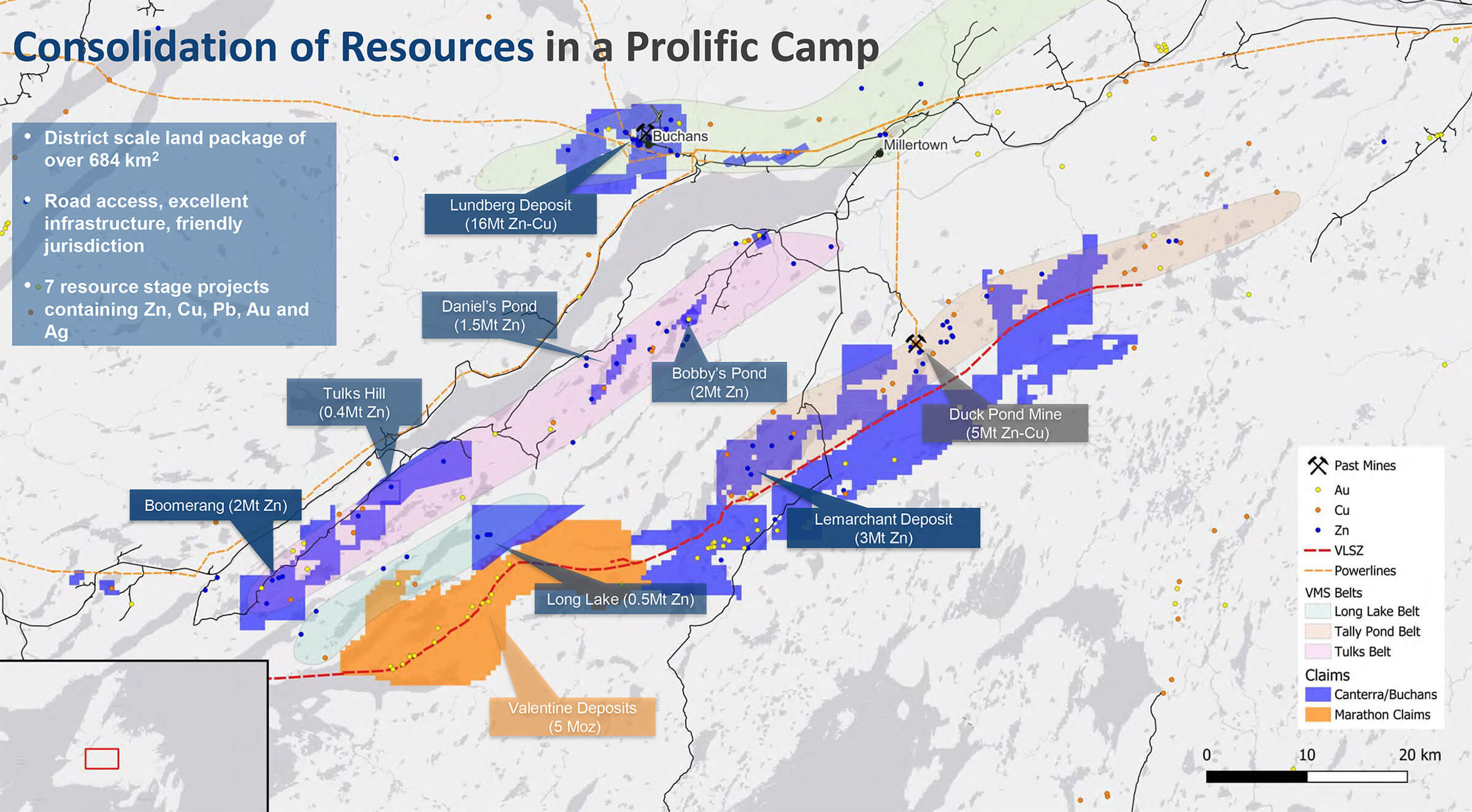

Consolidating an entire zinc district in Newfoundland

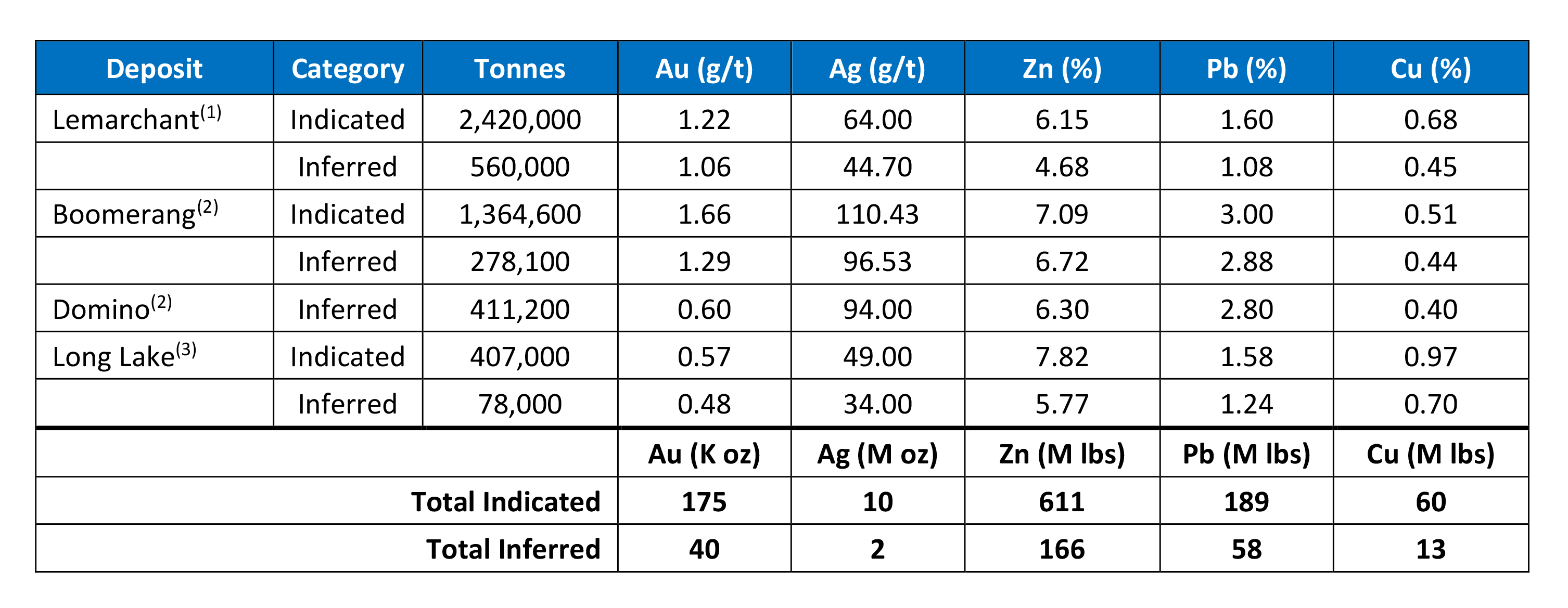

Although Canterra Minerals rebranded itself as a gold company after abandoning its focus on diamonds, the drill results on the Wilding Gold project didn’t yield the desired results and the company decided to re-focus on its base metals assets. This wasn’t a new idea as Canterra Minerals had previously acquired four properties from NorZinc with a total indicated resource of 611 million pounds of zinc and an additional 166 million pounds of zinc in the inferred resource categories. And as you can see below, the resource also contained 215,000 ounces of gold (175,000 ounces in the indicated category and 40,000 ounces in the inferred resource category) as well as lead, silver and copper as shown below.

The resources shown above clearly weren’t sufficient to have the required ‘critical mass’ to even consider thinking about refocusing on base metals, and zinc in particular. Although zinc made the list of critical minerals as issued by the federal government of Canada in 2021, there was very little appetite in the metal while Canterra’s asset base simply was too small to draw any interest.

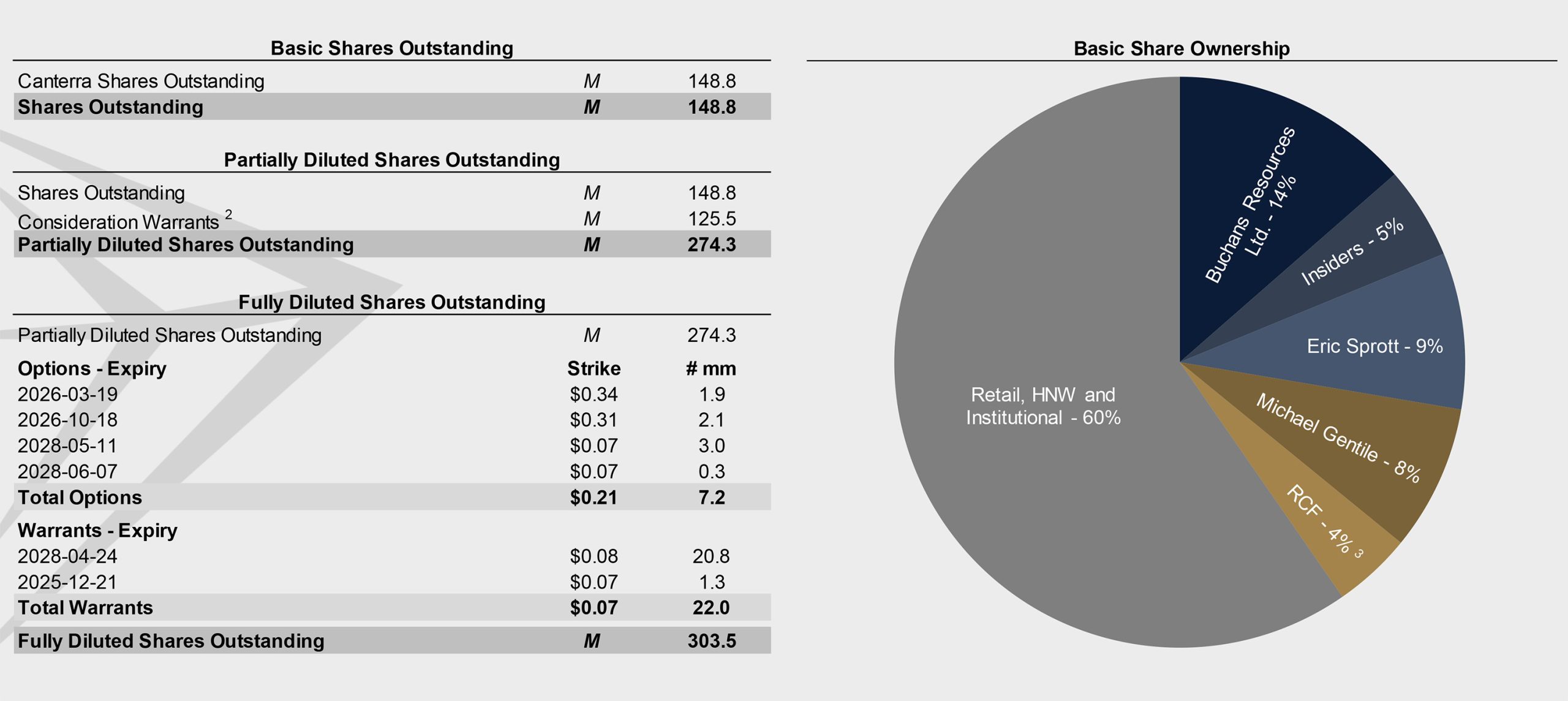

This changed when the company announced the acquisition of all assets of Buchans Resources in Newfoundland. That deal closed in December 2023 and required the company to issue 24.9 million shares, representing a 19.9% stake in Canterra’s capital stack. Additionally, Canterra issued 128.55 million warrants which are exchangeable into common shares of Canterra Minerals for no additional consideration after closing the acquisition and the TSX Venture approval, on the condition that no change of control will be triggered on the Canterra level.

This means that for all intents and purposes, we should consider those “consideration warrants” to be equal to common shares, resulting in a normalized share count of 274.3 million shares.

Concurrent with the acquisition, Canterra also issued 23.7 million flow-through shares at a price of C$0.065 per flow-through share for total proceeds of just over C$1.5M. Those 23.7 million flow-through shares are already included in the capitalization overview above and are part of the 148.8M shares issued and outstanding. Those flow-through shares were subject to the standard 4 month and 1 day hold period, which will expire on April 21st. It’s perhaps not a bad day to mark that date in the calendar as we may see some share price weakness around that date as some of the participants in the flow-through financing may choose to exit their positions.

At the current share price of C$0.07, the market capitalization of Canterra is approximately C$10M.

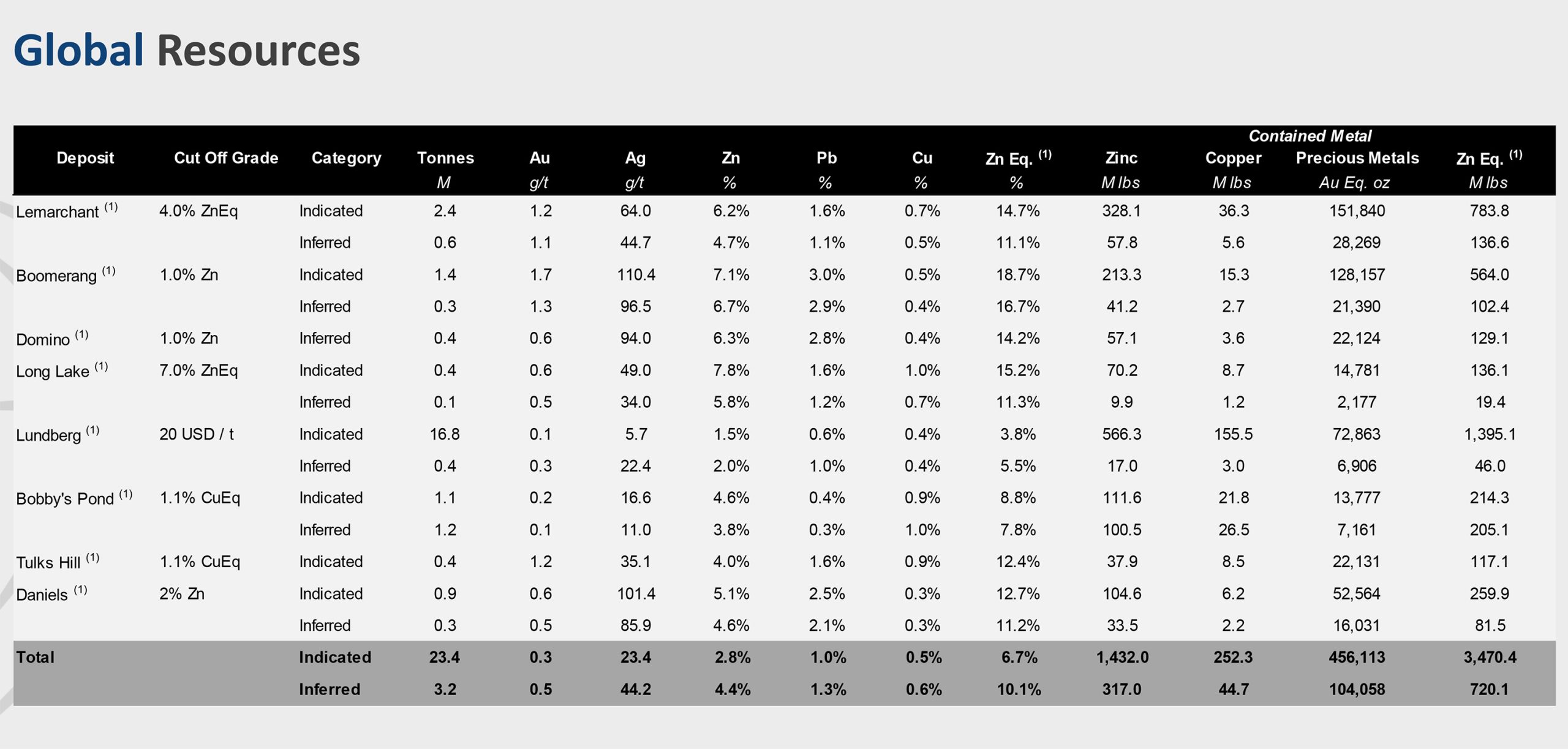

The acquisition immediately catapulted Canterra Minerals into a whole new league. As you can see below, the global resources currently stand at 23.4 million tonnes in the indicated resource category and 3.2 million tonnes in the inferred resources.

The indicated resources have an average grade of 2.8% zinc and 1% lead which is relatively low, but the 0.5% copper grade is quite interesting as well because at the current copper price, 1% copper equals more than 3% zinc on a zinc-equivalent basis (on an in situ basis, so before taking recoveries and payabilities into account) so a 0.5% copper grade would represent approximately 1.5% ZnEq. The average zinc-equivalent grade as reported by Canterra Minerals is 6.7% in the indicated resource category and 10.1% in the inferred resource category.

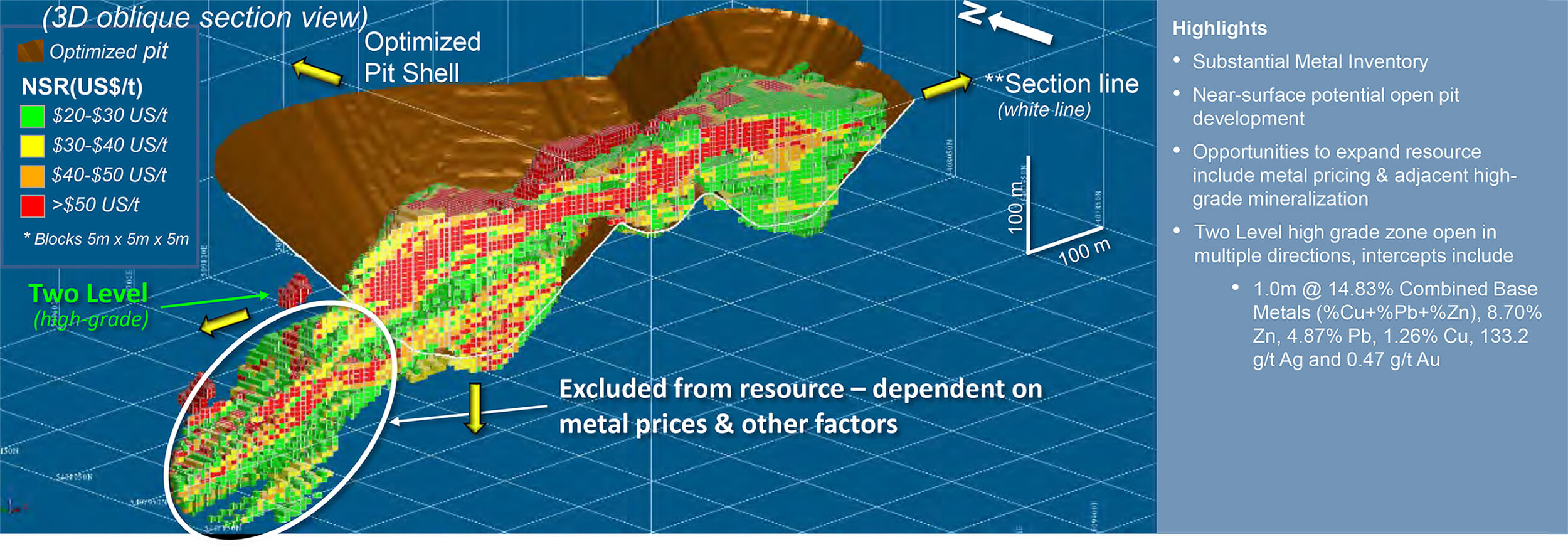

The recent acquisition immediately boosted the global resources to 1.43 billion pounds of zinc in the indicated category, with an additional 252 million pounds of copper and almost half a million ounces of gold-equivalent (consisting of gold and silver) for a total zinc-equivalent content of almost 3.5 billion pounds. This is being complemented by an additional 720 million pounds of zinc-equivalent in the inferred resource category. And despite an interesting amount of precious metals, this is a base metal district with a total zinc content of 1.75 billion pounds across both categories, with about 300 million pounds of copper, as shown in the table above. And it’s an additional bonus the majority of the tonnage and resources are in the indicated resource category; the inferred resource is just the icing on the cake.

Although the resources are scattered around, the Lundberg deposit could very well prove to have been the missing link for the company. While the average grade at Lunberg is pretty low (with a 3.8% zinc-equivalent grade for the almost 17 million tonnes in the indicated resource category), it’s noteworthy the deposit remains underexplored and Boliden walked away before it could really thoroughly investigate the asset. As will be discussed below, Boliden did nòt walk away because it didn’t believe in the merits of the project but because it couldn’t get to a definitive joint venture agreement with the optionor.

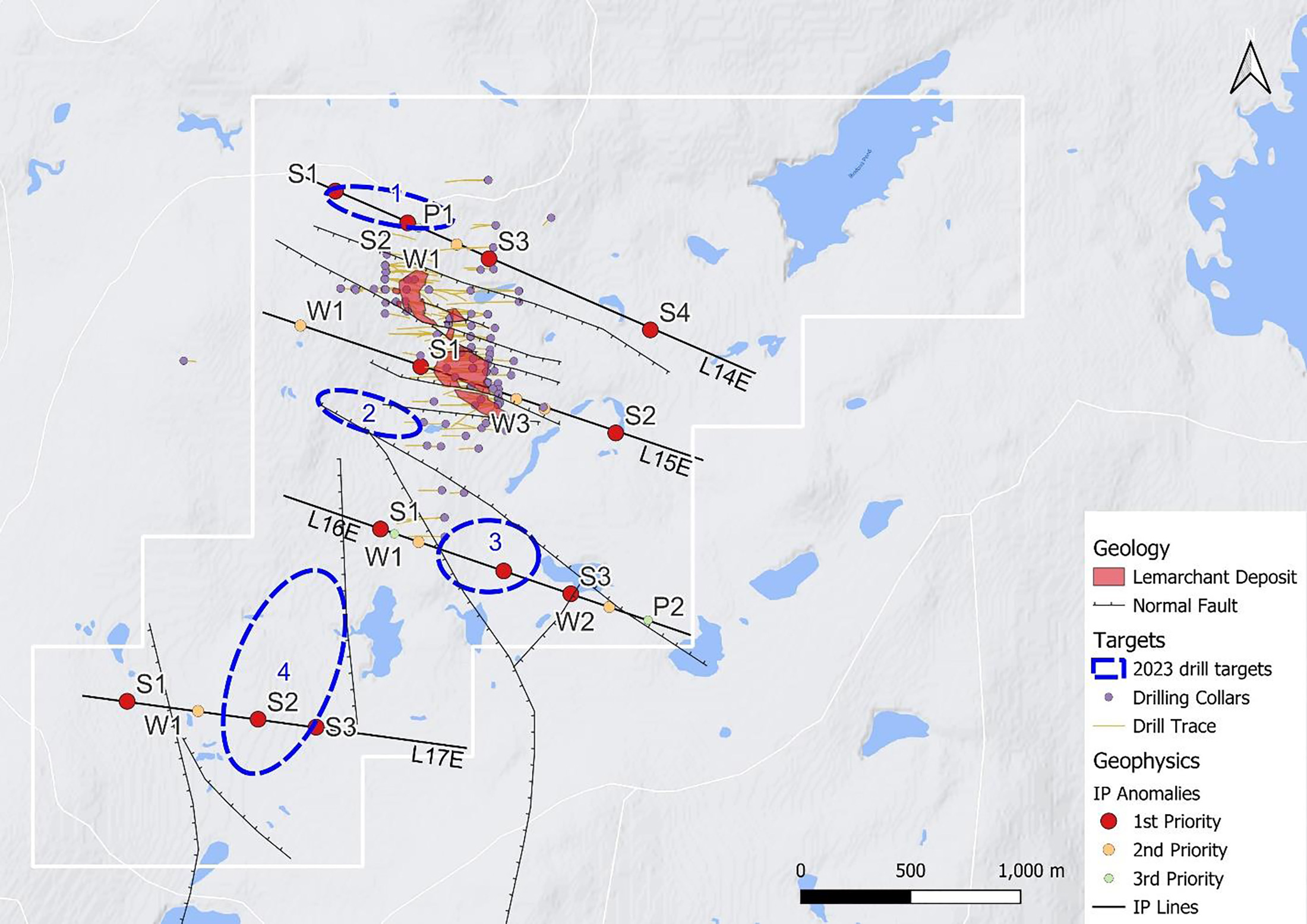

Despite the addition of the Lundberg deposit, the company has decided to spend the recently raised flow-through funds on the Lemarchant deposit, where previous operators completed in excess of 50,000 meters of drilling in 165 holes. The company already reviewed all historical data at Lemarchant before acquiring the Buchans Resources assets, and came up with new exploration targets last summer. And those targets have now been drilled as Canterra went straight back into the field after raising the money and it completed 2,000 meters of drilling in seven holes. The company targeted five specific targets, which it nicely elaborated on in its drilling announcement.

- Shallow IP chargeability anomalies of similar magnitude to the established deposit, located in favourable geology northwest of known Lemarchant mineralization, with no previous drilling

- Shallow target anomalies that follow the fault displaced continuation of Lemarchant Deposit, coinciding with the IP anomaly trend

- Strong chargeability IP anomaly with potential deep extension of Lemarchant mineralization in down thrusted graben structure

- IP/magnetic anomaly and EM Conductor in prospective geological horizon, with no previous drilling

- Drilling within the deposit’s eastern portion near the transition of Indicated and Inferred category resources. Drilling is designed to determine if the core of the deposit may be expanded on its eastern margins in an area hosting some of the deposit’s largest thicknesses and highest grades

We expect assay results to be released later in April as the turnaround times are very reasonable these days. And although it was a small drill program, hopefully some of the holes hit some nice mineralized intervals (which would certainly help to counter the impact of the end of the lock-up period of the flow-through shares no April 21st). In a worst-case scenario, Canterra will learn a lot from the first-ever drill program it completes at Lemarchant.

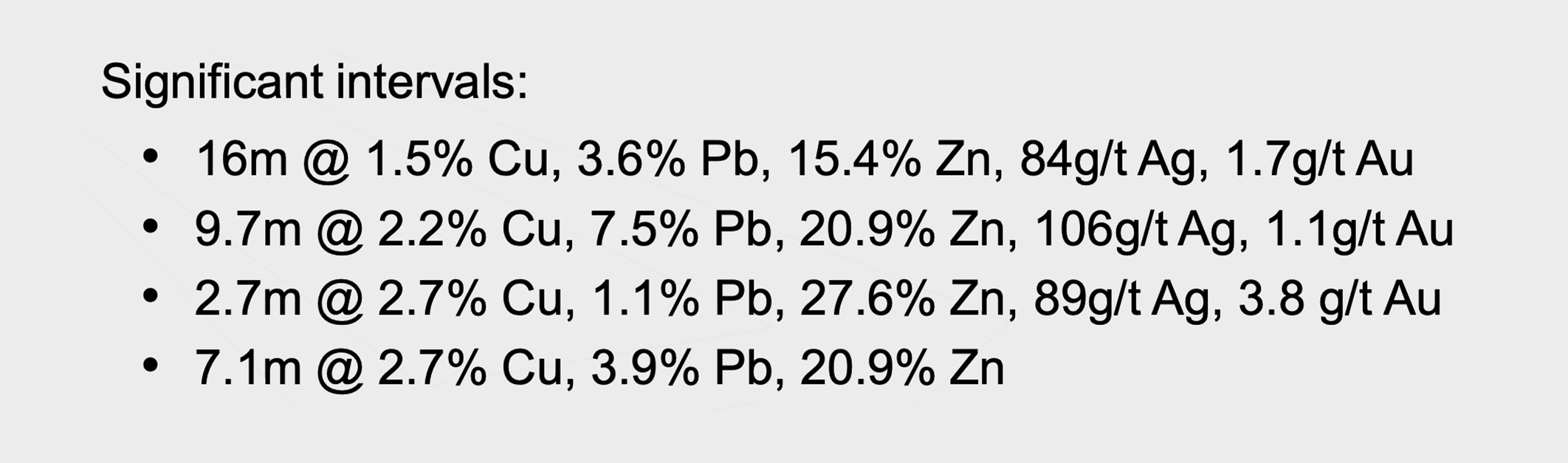

Let’s also not forget the previous drilling at Lemarchant. Some of the historical drilling encountered high-grade results, with 16 meters containing 1.5% copper, 19% ZnPb, 84 g/t silver, and 1.7 g/t gold, while other holes also contained high-grade mineralization, as you can see below.

Of course, there is no guarantee the few holes drilled at Lemarchant will contain high-grade mineralization, but it goes to show Canterra isn’t just drilling moose pasture here, and some of the targets could hopefully add value to the project.

Groan, yawn – not another zinc story?!

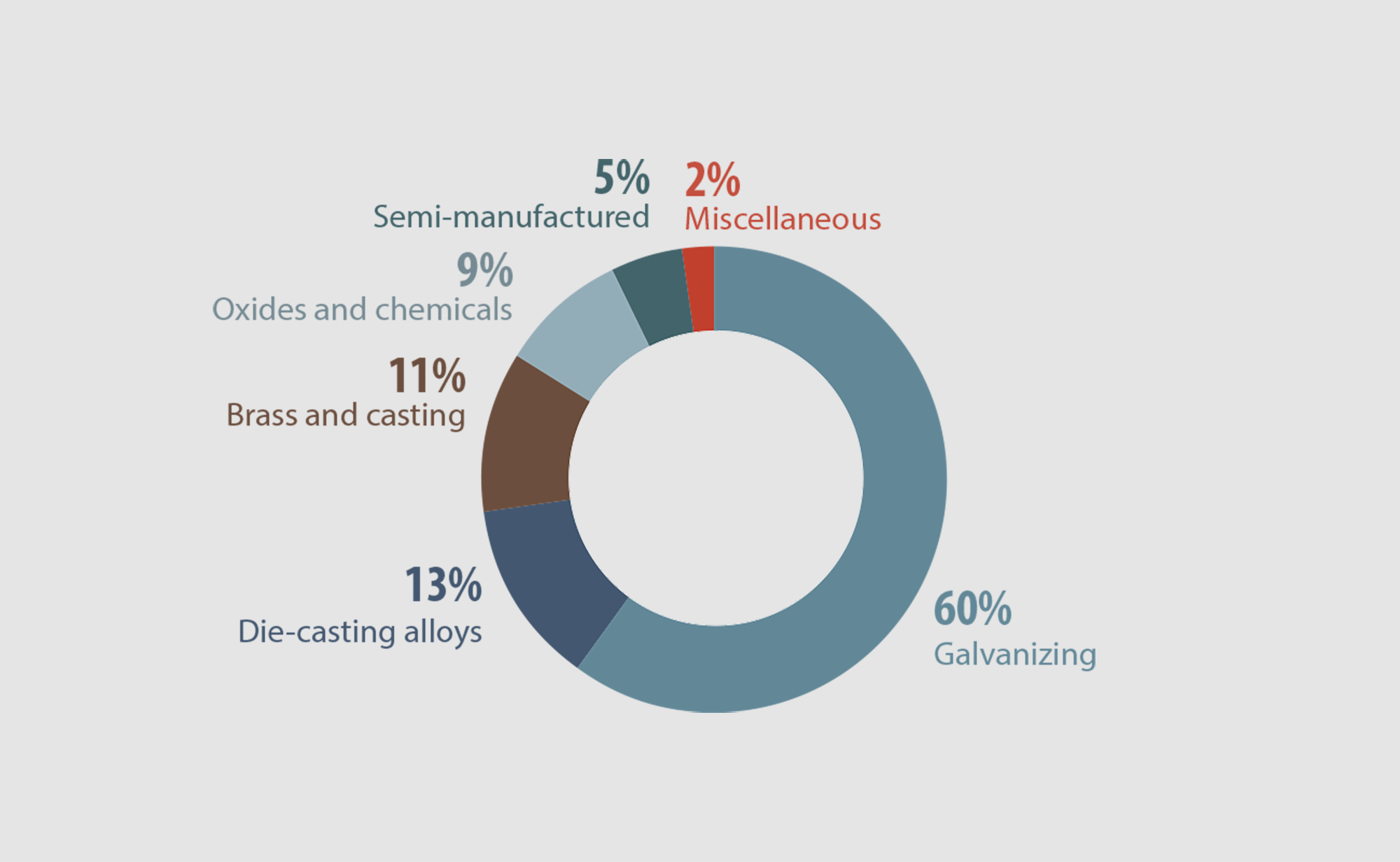

Perhaps it would be useful to provide a quick primer on the zinc market and the applications for zinc. Approximately 60% of the zinc is used for galvanizing steel, while other applications represent just a minority of the demand.

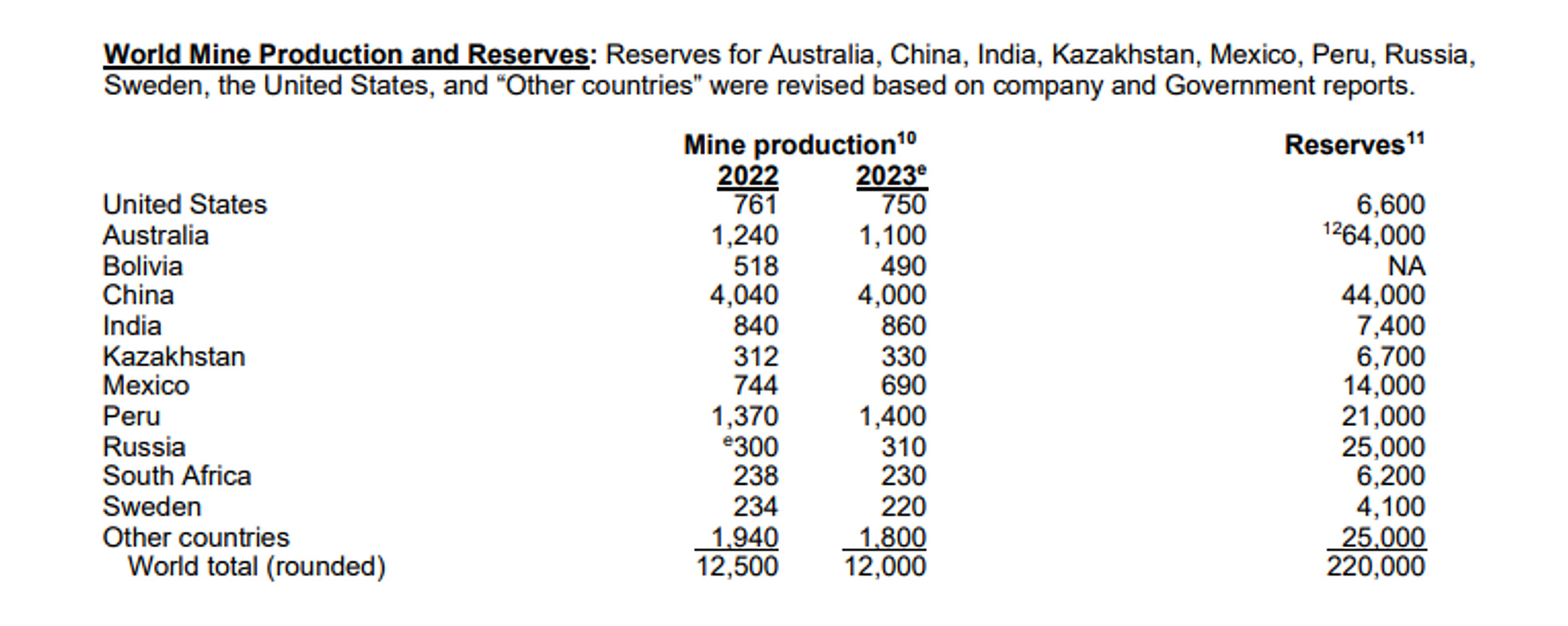

The total zinc production has been declining for quite a while, and according to the most recent report published by the US Geological Survey, the total output was approximately 12 million tonnes of zinc, which represents just under 27 billion pounds. That’s a 4% decrease compared to the preceding year, as there were noticeable production decreases in Australia and Mexico, partially offset by higher production in Kazakhstan and Peru.

The total refined zinc production was approximately 12.4 million tonnes (this includes zinc sourced from secondary supplies) and according to the International Lead and Zinc Study Group, the total output will increase by approximately half a million tonnes this year as a large mine in Russia is currently ramping up production. That ties in nicely to the anticipated supply/demand balance.

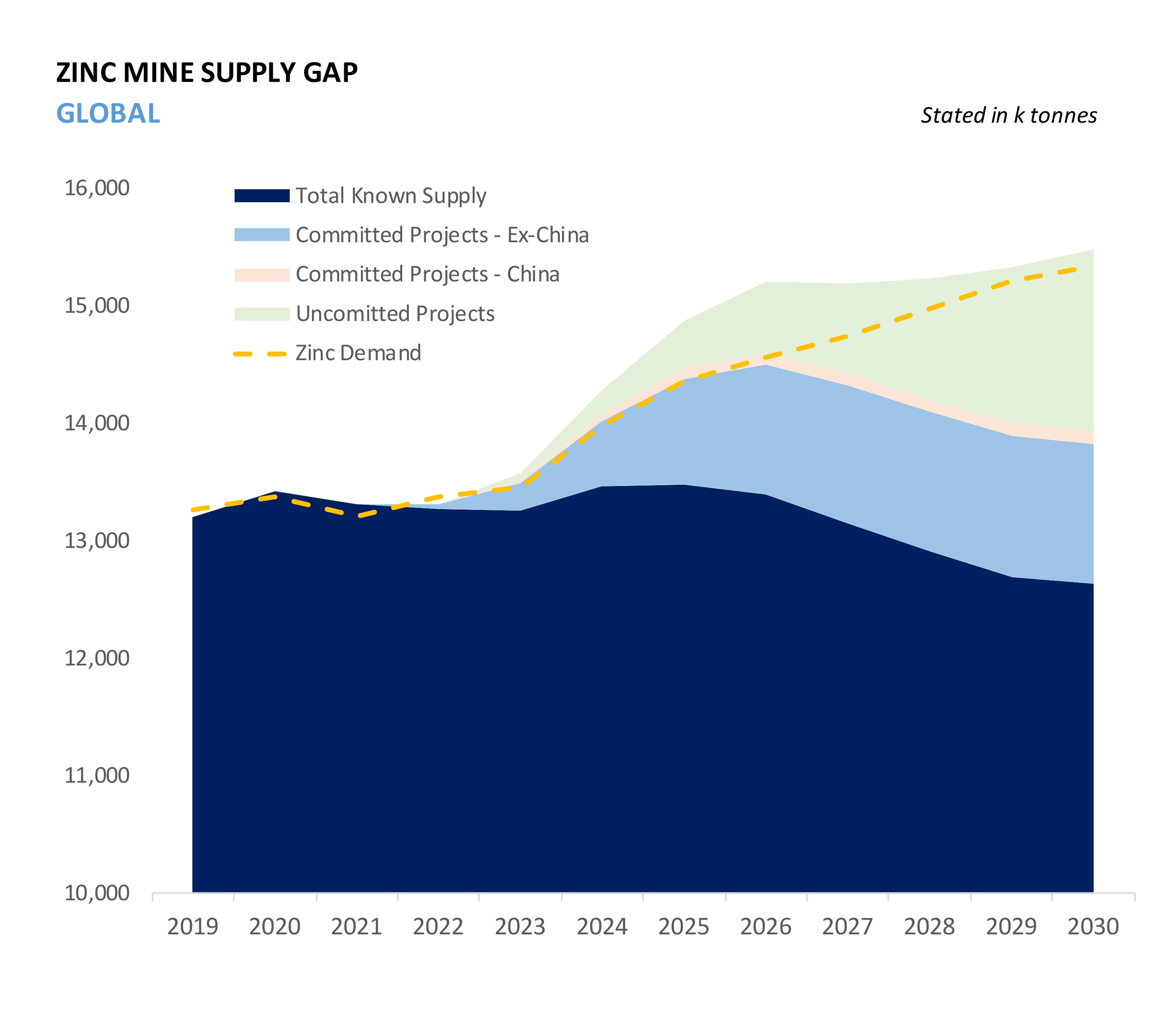

Last year, metals trader Trafigura posted an interesting chart that explains how it expects a supply gap from 2026 onwards. As you can see below, the zinc demand will gradually increase. Still, so will the zinc production as the committed projects outside of China (this includes the large new Ozerny zinc mine in Russia – assuming there are no technical hiccups due to the Western sanctions) are expected to follow the anticipated demand increase basically.

The situation gets interesting from 2027 on. As you can see, the current known supply will plateau and level off from 2026 on and unless some of the ‘uncommitted projects’ come online, the zinc sector may encounter an ‘oopsie’ moment in the second half of this decade.

And perhaps the turning point will come sooner rather than later. Throughout 2023, multiple mines were closed or mothballed. Boliden, the large Swedish zinc miner and smelter, placed the Tara mine in Ireland on care and maintenance. And that certainly is not because the mine was depleted, as the annual report for 2022 indicated the reserves underpinned an additional 6-year mine life with an additional 40 million tonnes (for a theoretical 20-year mine life) in the resources(subject to successfully dealing with the water inflow). Yet just six months after that updated reserve calculation, the mine was mothballed, thereby removing in excess of 100,000 tonnes of annual supply off the market.

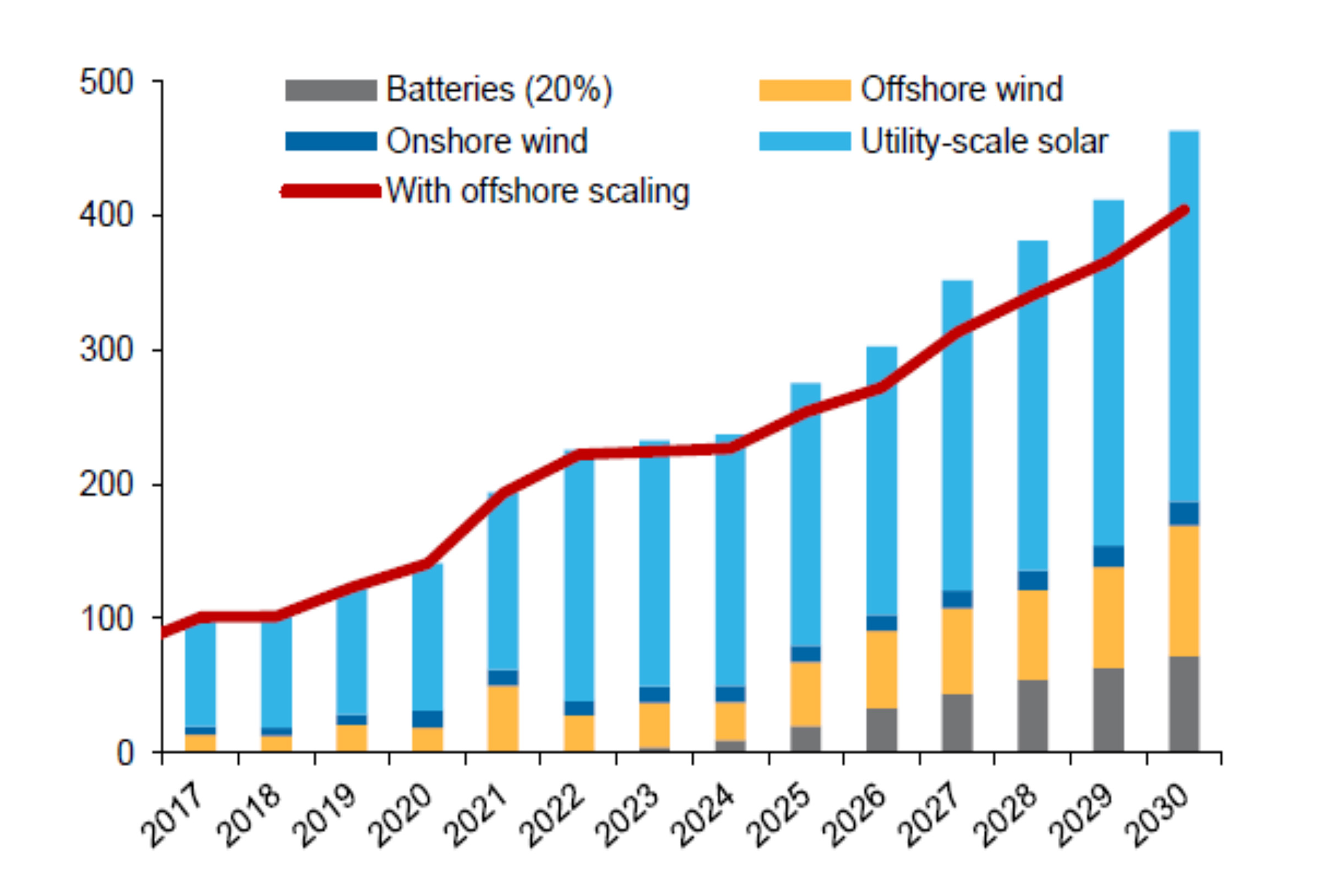

Aeris Resources in Australia put its Jaguar mine on care and maintenance as it couldn’t make the high-grade deposit work due to ‘seismic events’ and other operational challenges. That mine produced just over 22,000 tonnes of zinc per year, and that output has also dropped to zero. Meanwhile, the demand for zinc continues to increase. In the past 10 years, we have seen CAGR of 2-3% in the demand for zinc, and that growth rate is likely intact. The big ‘unknown’ is the demand for zinc from the wind, solar, and battery industries. Although we couldn’t find any recent expectations and assumptions, a report issued by Macquarie in Q4 2022 indicated it expected the demand for zinc from the ‘clean energy’ sector to increase by 200,000 tonnes per year by the end of this year.

This appears to be a very nuanced report and assumption and although all the EV aficionados would want to make you believe the demand for zinc from the clean energy transition will skyrocket, the Macquarie estimate appears to be reasonable in the greater scheme of things: a 200,000 tpa demand increase represents just over 1.5% of the current global demand, or less than 0.3% per year.

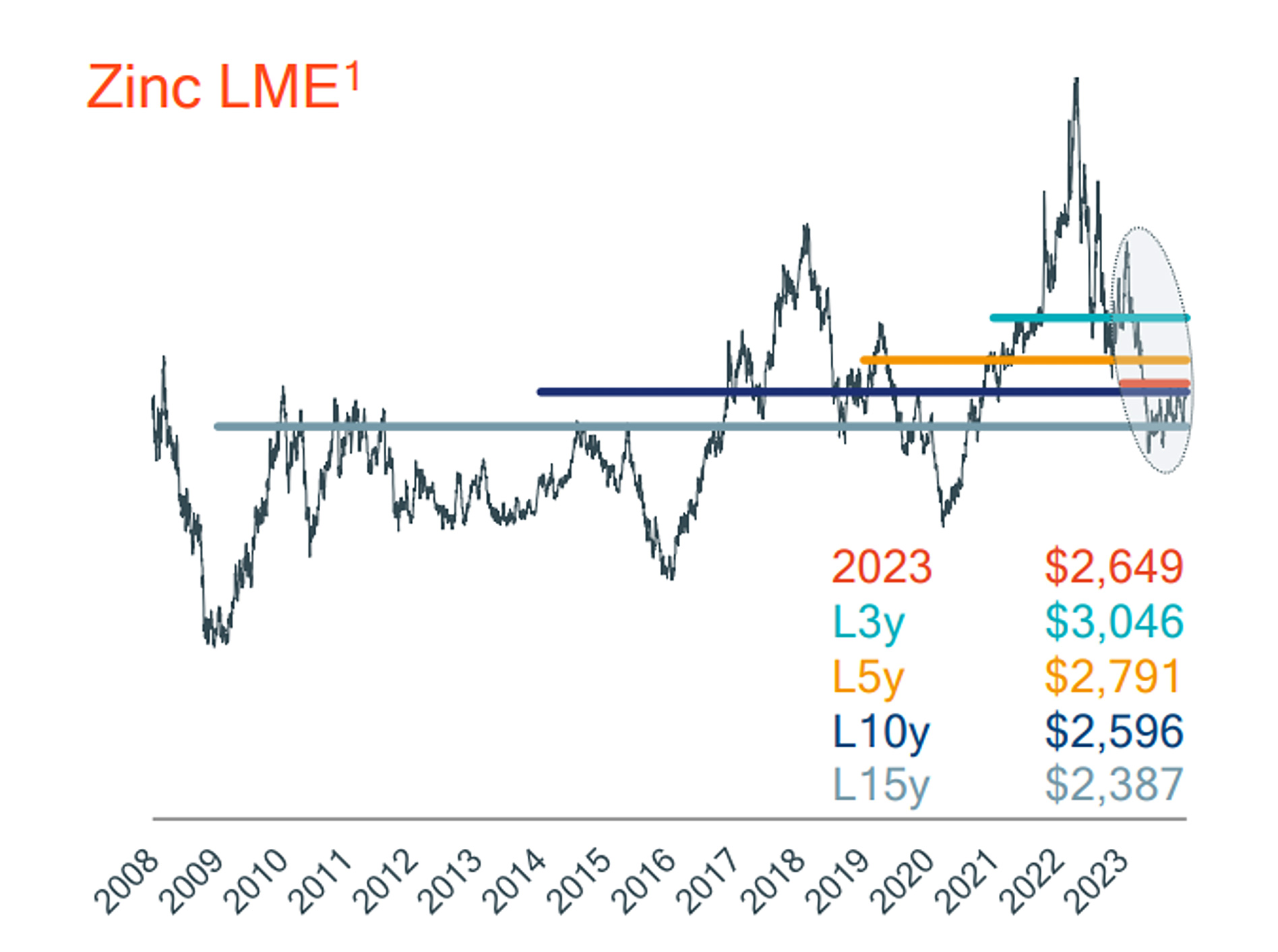

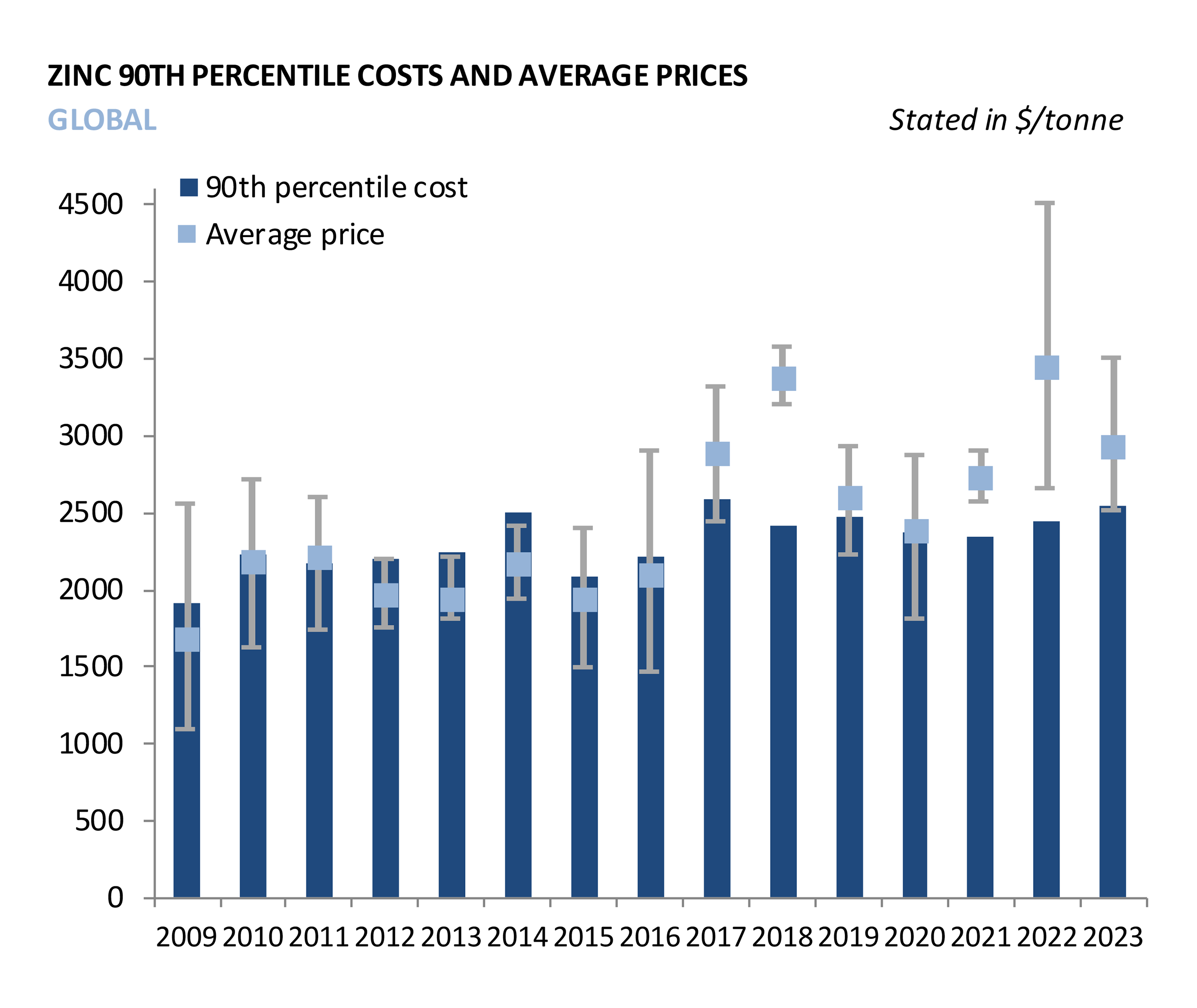

German steel dust recycling company Befesa, which produces zinc as a by-product, had calculated the 5 year and 10 year average prices for zinc. As you can see below, the 5 year average zinc price was just under $2,800/t while the 10 year average was $2,600/t.

The average zinc price is pretty straightforward and easily accessible data. But if you combine the average price with the 90th percentile cost basis of the zinc producers (provided by Trafigura again), there is no margin of safety anymore. According to Trafigura’s cost estimates below, the average production cost per tonne for the 90th percentile of zinc production IS the current price of $2,500/t.

This means that about 10% of the output is being generated at a loss and although we already saw some mine closures in 2023, several more producers are operating at very narrow margins (or at a loss). And this is where it gets interesting. Removing 10% or even just 5% of the supply on a market that is in some sort of an equilibrium could send the zinc price higher.

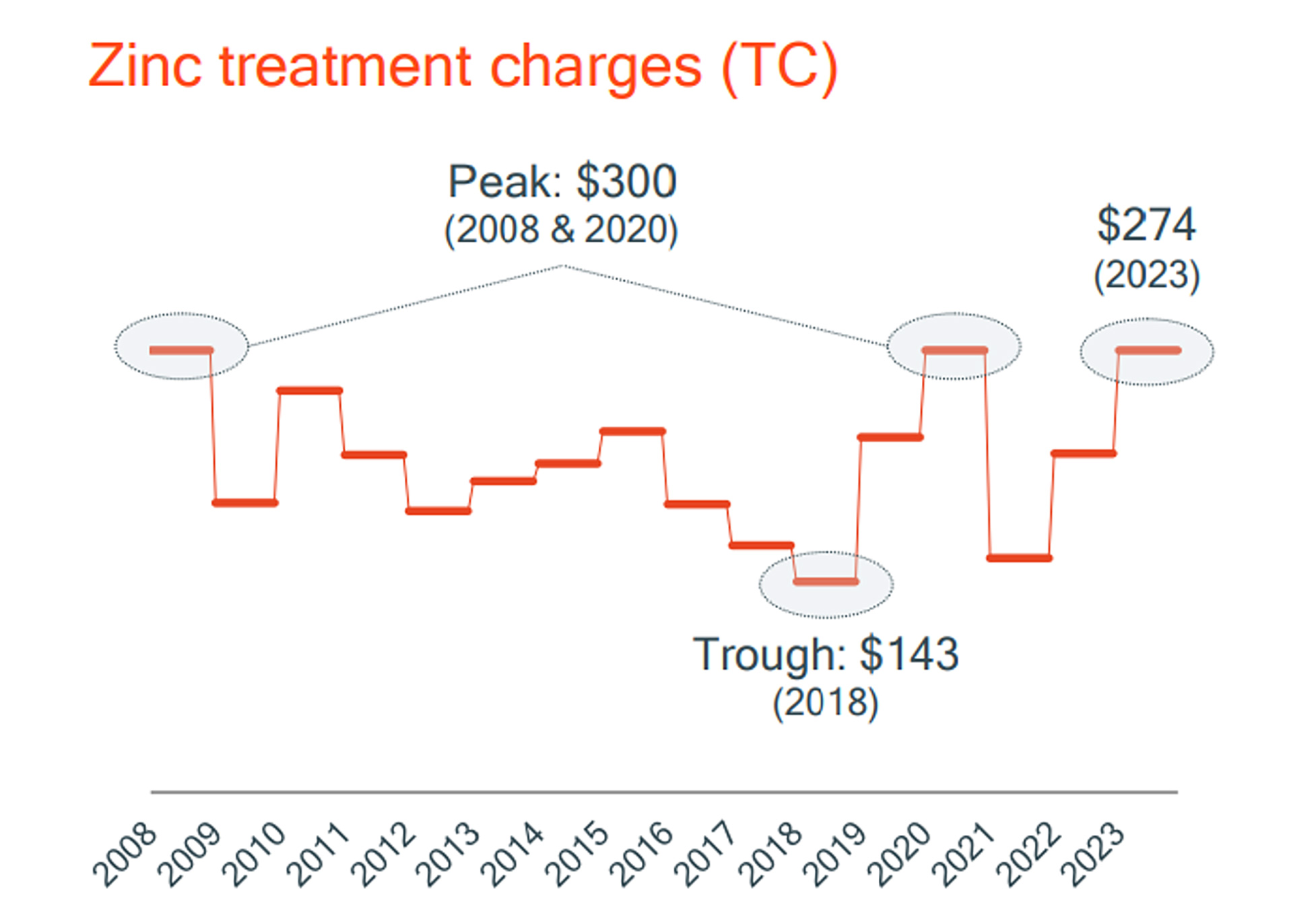

A final piece of ‘evidence’ why the zinc price may have reached its bottom is the anticipated TC/RC charges. The image below is provided by Befesa again, and it shows how the treatment charges and refining charges by the smelters have evolved in the past decade.

High TC charges put the profitability of a mine under pressure and are an indication there is an ‘abundance’ of zinc concentrate available for processing. In 2023, the TC charges were close to its highest level in 15 years which slowly suffocates mining operations. The TC charges are usually set by the largest players in the industry and are published in April. Generally speaking, the lower the tighter the markets are, the lower the TC/RC charges are. Back in 2023, smelters were able to hike their treatment charges as the mine supply rebounded pretty sharply after the COVID years, but with the numerous mine closures and lack of new supplies, the tables have turned.

Although we still have to wait for the official announcement of the 2024 TC charges, Nexa Resources, a Peru-based zinc miner and smelter, is using a TC charge of $174/t in its 2024 guidance. That’s a 37% decrease compared to 2023 and a clear indication the zinc market is getting tighter. And the $174/t isn’t just an anecdotal element; large zinc producer MMG mentioned that in Q3 and Q4 of 2023, the last minute spot TC charges dropped to respectively $110-140/t and $70-80/t in those two quarters as smelters scramble to get their hands on enough feed to keep their smelters running. That makes Nexa’s guidance for $174/t in TC charges very reasonable.

Of course, none of this really matters to Canterra Minerals as Canterra is still in the exploration phase and is not directly impacted by changing zinc prices or the intricacies on the zinc market. But there could be indirect benefits.

First of all, as the mine supply is stabilizing (or even decreasing if more mines are shut down and the new large Russian mine doesn’t perform as expected) smelters will continuously be looking for additional smelter feed to keep their smelters up and running. As Boliden had to shut down a zinc mine, it will require spot purchases of zinc concentrate to replace the smelter feed that was initially provided by the Tara mine and security of supply will play a key role as those smelters generally prefer a multi-decade mine life. Added bonus: Boliden was the partner of privately held Buchans Minerals in 2021 and 2022 before it passed as Buchans and Boliden couldn’t agree on the terms of a joint venture agreement after the Swedes completed their initial commitments. The initial agreement called for Boliden to spend C$18.6M on exploration to earn a 75% stake in the project. About C$1.1M was effectively spent before Boliden walked. Another interesting feature is that Rodney Allen was recently appointed to Canterra’s technical advisory committee. You may be familiar with Mr. Allen as he also is a technical advisor to District Metals (DMX.V) in Sweden, but as he also was Boliden’s Chief Scientist for over a decade and that very same Boliden recently announced a joint venture agreement with District Metals to explore for base metals in Sweden.

Secondly, when the copper TC charges dropped earlier this year, the copper price moved up as the market participants understood the significance of the TC decrease. Hopefully we will see a similar outcome in the zinc space. If the Treatment Charges indeed fall by 30-40% this year, the zinc market could likely attract more/new eyes.

So, while Canterra would not directly benefit from a tighter zinc concentrate market, it should hopefully draw more attention to the (zinc) sector as a whole.

Management team

Chris Pennimpede – CEO & Director

- 14 years of exploration experience

- VP Corporate Development at Contact Gold

- Operations Manager CSA Global

- Smash Minerals/Prosperity Goldfields/Northern Empire

Paul Moore – VP Exploration

- More than 30 years of exploration experience focused in Eastern Canada

- Former Senior Geologist at Teck Corporation and Anglo American

David Butler – Exploration Manager

- More than 30 years of exploration experience, primarily in Newfoundland-based VMS assets

- Board Member, Professional Engineers and Geoscientists of Newfoundland and Labrador

Investment thesis

Although Canterra Minerals still owns the Wilding Gold project (and it also still owns the Ring of Fire claims as well as 50% of the Buffalo Hills diamond project in Alberta), it is clear the focus is now on the base metals properties as the company seeks to capitalize on the addition of zinc to the list of critical minerals in Canada. While zinc definitely isn’t an exciting or exotic commodity, the fundamentals appear to be improving as the low zinc prices have caused mines to shut down while the decreasing treatment charges for zinc concentrate indicate a certain tightness in the market, and hopefully, this will make zinc somewhat attractive again.

The assay results from the Lemarchant drill program should be released soon. Once those are out, we’ll sit down with CEO Chris Pennimpede to discuss the results and the potential follow-up plan.

Disclosure: Canterra Minerals is not a sponsor of the website but may become a sponsor in the near future. The author has a long position in Canterra Minerals. Please read our disclaimer.