As the political tensions and regulatory framework in Tier-3 mining countries is deteriorating, more companies are looking towards safe regions to develop assets. Idaho has recently been in the spotlights as well-respected companies like Integra Resources (ITR.V, ITRG) and Liberty Gold (LGD.TO) are working on their DeLamar and Black Pine assets, but as those companies already reached market capitalizations exceeding C$200M and C$400M respectively, it could make sense to have a look at assets that are a bit lower on the food chain.

Freeman Gold (FMAN.C) is an exploration-stage company with the Lemhi gold project in Idaho as its flagship asset. Lemhi has a historical resource exceeding a million ounces of gold (predominantly hosted in oxidized material) and as the company has just closed a C$10.35M raise, Freeman Gold is now off to the races.

The flagship property

Freeman Gold’s exploration efforts will be focusing on the Lemhi gold project in Lemhi county, Idaho. The project is located about 40 kilometers north of Salmon and the 1,270 hectare project (1,019 hectares of unpatented claims and 249 hectares of surface rights) is situated on the Cordilleran fold and thrust belt.

The first gold discovery on the property occurred about 100 years ago in the late 1800s but it was only about 30 years ago the property was effectively subject to more up-to-date exploration techniques. Exploration happened on an on and off basis and only in 2011 there was a more dedicated exploration approach when Northern vertex Capital and Idaho State Gold completed thousands of meters of drilling when both companies partnered up in the Lemhi Gold Trust joint venture.

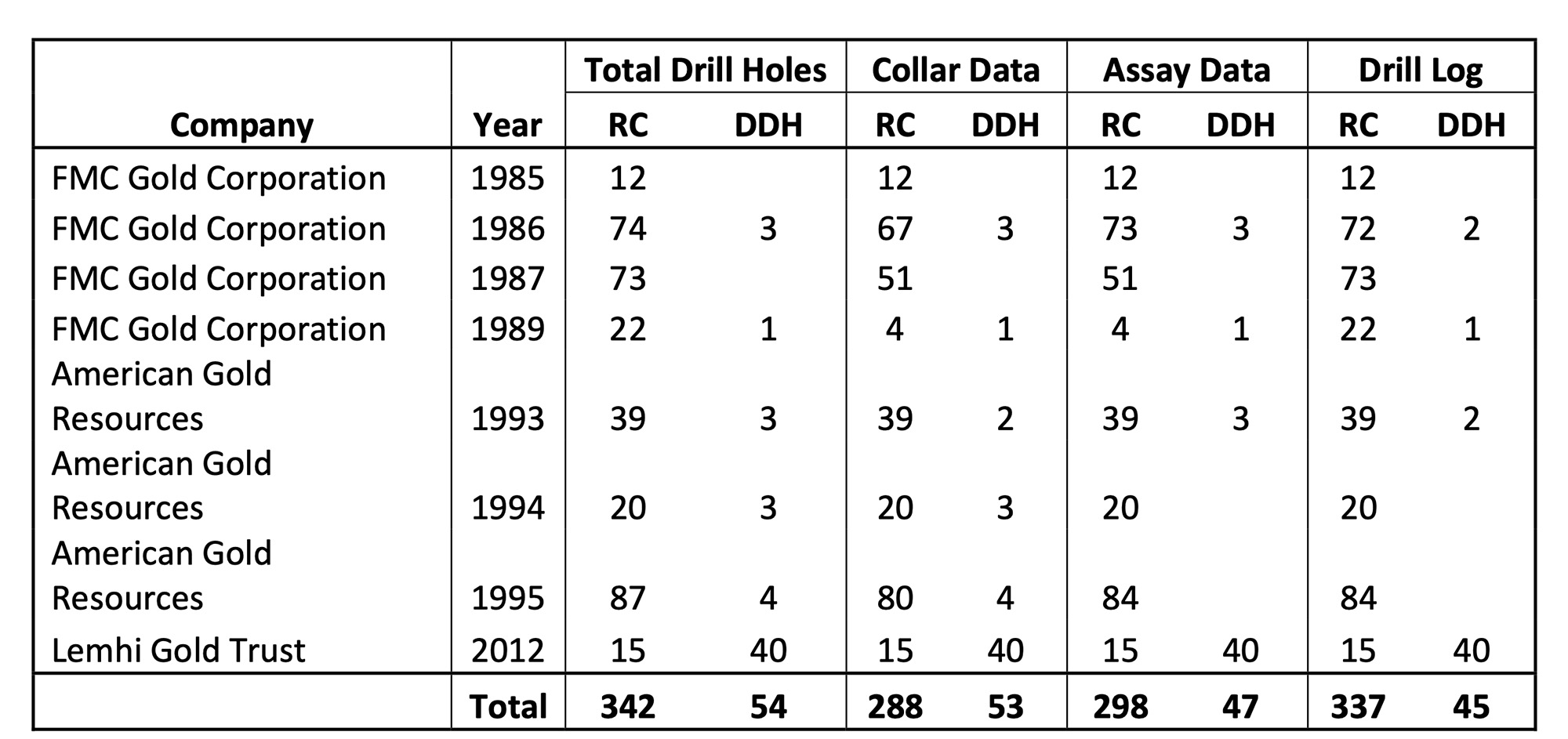

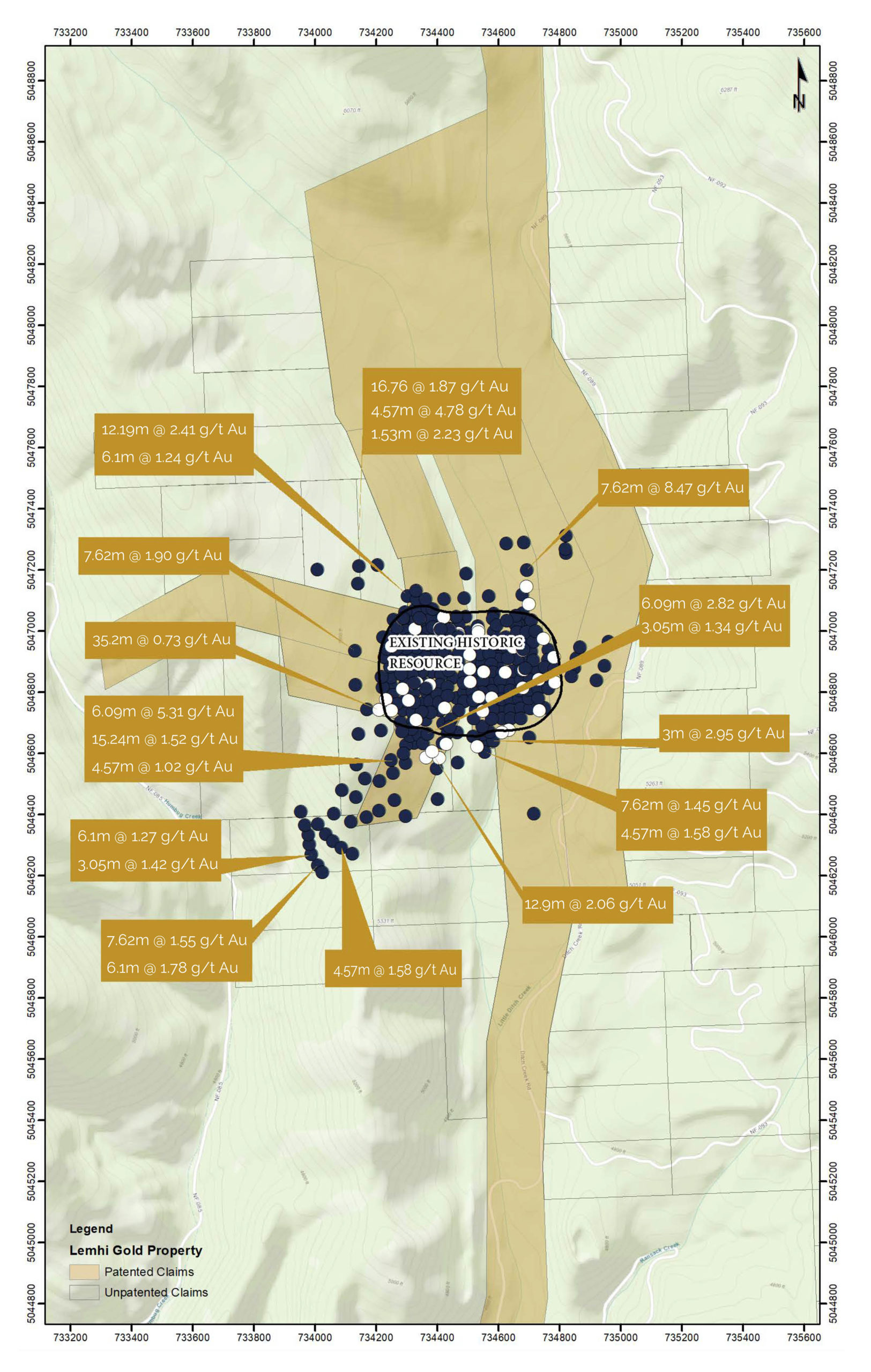

According to the technical report on the project, which has been filed on SEDAR, the historical operators drilled a total of 396 holes of which approximately 85% were RC holes with the remainder diamond drill holes. This culminated in several different resource estimates, as you can see here below.

When you look at the table above, we immediately notice two things. First of all, the operators in 2012 (the Lemhi Gold Trust) already felt confident in putting out a sizeable resource that contained approximately 800,000 ounces of gold. This was later downgraded in 2013 to almost 700,000 ounces of gold.

But what really matters for the Lemhi gold project is the average grade. Considering the material is oxidized and should be amenable to a heap leaching process just like Integra Resources’ DeLamar gold project in Idaho where a Preliminary Economic assessment confirmed the viability of heap leaching rock with an average grade of just 0.39 g/t gold. You notice how the average grade in the 2012 and 2013 resource estimates exceeded the 0.65 g/t so this bodes well for Lemhi.

But if you carefully review the evolution of those historical resource estimates, you’ll notice something strange. Both resource estimates in 1996 estimated the average grade at around 1.3 g/t gold but in the subsequent resource in 2012, the grade dropped by almost 50% to just around 0.65-0.7 g/t. This could indicate the historical operators in the eighties and nineties were dead-wrong, but the opposite is true. In an initial drill program aimed to twin the historical holes from the 80s and 90s, the Lemhi Gold Trust encountered significantly different grades compared to the old assay results. There is no good explanation for the substantial discrepancies encountered in the first twin program, but the technical report refers on page 29 to ‘the uncertainty of the locations of the historical holes, combined with the lack of downhole surveys, [and this] could easily be problematic along with other more concerning issues such as nugget effect and/or smearing of gold during drilling due to poor drilling practices […] in the 1980s and 1990s’. However, the initial interpretation in 2011 contained this very important passage (page 32 of the technical report). While commenting on the grade variation, the geologist who analyzed the 2011 drill program mentions that ‘although the variation in grade on detailed scale is significant, overall mineralization holds together and the effect on tons and grade should be minimal’ which minimizes the importance a nugget effect could have played.

Long story short: the truth is very likely somewhere in the middle and there’s only one way to find out what the effective grade of the gold-bearing zones at Lemhi is: a rigorous drill program executed while obeying the modern exploration standards. A drill program Freeman Gold will undoubtedly immediately start with.

The two main boxes to tick

Figuring out the grade of the Lemhi oxide zones will be Freeman Gold’s main task. Although an average grade of 0.65 g/t would definitely viable at the current gold price, any bump in the average gold grade would further boost the viability of the project and further improve the economics.

Secondly, Freeman Gold will have to spend some time on confirming the recovery rates (and thus the economic viability) of a heap leach scenario. A historical metallurgical test program confirmed an average recovery of 80% of the gold using a crush size of 80 mesh (roughly 0.1 inches) with a cyanide consumption of approximately 1 pound per tonne of rock. This is a good first start, but the metallurgical aspect of a mining project has become more important in the past few decades and it would be useless to use a 1996 study to determine the viability of the project. Thanks to a continuous evolution of metallurgical test work in the past 2.5 decades since the previous study was completed it will be possible to finetune the cyanide consumption, crush size and anticipated leach time.

Looking at the PEA prepared for Integra Resources, the heap leach phase uses a mining cost of US$2/t and a processing cost of $2.8/t. Even if we would add 50% to these cost inputs (which is beyond being conservative) and use a 3:1 strip ratio, the operating cost for the heap leach phase would be just below US$15/t. Even if no higher grade will be found and no progress is being made on increasing the recovery rates, recovering 80% of the gold in 0.65 g/t rock would result in a recoverable rock value of US$29/t at $1750 gold.

So while the project would work if Freeman Gold confirms a NI43-101 compliant resource of 1 million ounces at an average grade of 0.65 g/t with a recovery rate of 80%, improvements in both the grade and/or the recovery rate have the potential to rapidly increase the value of the Lemhi gold project.

Freeman is now fully cashed up after completing a C$10.35M raise

On July 28th, Freeman Gold confirmed it had closed the previously announced bought deal financing, raising C$10.35M by issuing 20.69 million shares at C$0.50. Considering this was a warrant-free bought deal financing, there will be no warrant clipping and the stock is immediately tradeable.

Freeman Gold now has approximately 76.3M shares outstanding and the only warrants that remain outstanding are almost 130,000 warrants with an exercise price of C$0.10 and the 4.27M warrants that were issued in May as part of the C$0.35 financing. These 4.27M warrants have an exercise price of C$0.50 and are currently in the money. Considering the C$0.50 warrants only expire in May 2021 and them barely being in the money at this point, we don’t expect a near-term warrant overhang. We think it would be in Freeman’s best interest if these warrants would be exercised as that would result in an additional C$2M in cash proceeds and this, combined with the net proceeds of the recent bought deal, should go a long way towards reaching some milestones on the Lemhi gold project. Additionally, Freeman issued 1.42M broker warrants in July 2020 valid for 2 years in connection with the underwritten capital raise which could result in an additional cash inflow of C$710,000.

The shares issued to purchase the property should be in strong hands – but stink bids could make sense

Now the capital raise has been completed, Freeman Gold has approximately 76.3M shares outstanding, of which roughly 33.7 million shares were issued to acquire Lower 48 Resources from a numbered parent company. The shareholders of that company haven’t been disclosed, but it looks like 1132144 BC was also involved with earlier transactions in the mining space. A google search shows the company dealt with Voltaic Minerals/Alpha Lithium in the past before selling the Lemhi gold project to Freeman Gold, but there’s no additional information available on the shareholders of the Numbered Company.

As Freeman paid for the acquisition using its own shares it can focus on spending its precious cash on the upcoming exploration plans to prove up the value of the gold project. That’s positive, but that also means we need to keep an eye on when those 33.74M shares are coming out of escrow as it’s normal for the shareholders of a private company to take money off the table given the single-digit cost base of their paper. The table here below shows the escrow schedule and the release date of the shares.

Upon conversations with the company’s management, it’s our understanding a part of the shares that were originally supposed to be released from Escrow in April were voluntarily escrowed for an additional three months.

As this is a capitalist world, we can reasonably expect some of these shares to be sold upon being released from escrow as the weighted average cost base of the shares is C$0.0395 (20.7 million shares were issued at C$0.05, 2.54M shares were issued at C$0.10 while the initial 10.5M shares that were already outstanding in 2018 – way before the numbered company acquired Lemhi – had a cost base of approximately C$0.0057 according to the recently refiled Material Change Report) is substantially lower than Freeman’s current share price. That being said, it’s encouraging to see a portion of the first tranche that was supposed to be released from escrow in April was subsequently escrowed again for several months, and this could indicate the sellers aren’t in a rush to sell the stock.

Selling shares is fine and inevitable anyway. It will be up to Freeman Gold to hit the ground running at Lemhi to convert the theory into reality by proving up a 1Moz+ high-grade oxide resource to remove the incentive to sell and absorb the shares that do hit the market.

There will always be sellers but with a current anticipated enterprise value of around C$41M (C$51M market cap and an estimated C$10M in net cash) there appears to be plenty of upside left and it could make sense -depending on the progress made by Freeman Gold- to put in stink bids around the dates the shares come out of escrow in case there is some blind selling.

The Team

Will Randall – President, CEO & Director

- Mr. Randall is a professional geologist with over 20 years of experience in the mining and mineral exploration industry.

- One of the early movers in the lithium brine industry, where he acquired, discovered and developed the Sal de los Angeles lithium brine project in Argentina.

- During his time running Sal de los Angeles, approximately $70M was raised for the development of the project which he led through resource development, feasibility, mine permitting and initial construction before being sold in an all-cash deal for $265M.

- He has been involved in raising over $200M and the successful development of several mining projects, including joint ventures with majors and national governments.

- Mr. Randall was raised in Argentina, before moving to Canada where he completed a BSc (Geology) and MSc. (Economic Geology) at the University of Toronto.

Dean Besserer – VP Exploration

- Mr. Besserer has more than 2 decades of exploration experience working in over 50 countries, including much of North America, often leading projects with annual exploration budgets exceeding $20 million U.S.

- Previously the Vice President and partner at APEX Geoscience Ltd., a consulting firm with offices in Canada, South America and Australia, where clients included BHP Billiton, Debeers, North Country Gold, Kaminak Gold etc.

- Mr. Besserer was a director of Brilliant Mining, Niblack Resources, Graphite One and the Vice President of Exploration for various Junior Mining Companies.

- Mr. Besserer is a Qualified Person with respect to National Instrument 43-101, and will fulfill this role for Freeman Gold.

Conclusion

Freeman Gold appears to be in an excellent position to pick the low-hanging fruit on the Lemhi gold project in Idaho as it should be easy and not too expensive to convert the historical resource estimate into a NI43-101 compliant resource estimate containing about 1 million ounces. Given the historical grade on the property (exceeding 1 g/t gold), a 1M+ ounce oxide gold deposit with recovery rates exceeding 80% should be viable at $1200 gold and extremely profitable at $1800 gold.

Freeman Gold has secured the asset, has raised the cash to fund the next few exploration stages, and hopefully the company is now off to the races in proving up a high-grade oxide gold resource in a Tier-1 mining jurisdiction. The size is decent, the anticipated recovery rates are good and the average gold grade is excellent for an oxide deposit. Now it’s up to the Freeman technical team to connect the dots and move the project forward.

Yes, there are shares that will very likely be offered up for sale once they come out of escrow but it looks like the Lemhi project is strong enough to ‘carry the company’ and although short-term pain on those release dates seems likely given the low-cost base of those shares, the Lemhi project looks very promising at the current gold price.

Disclosure: The author has a long position in Freeman Gold. Freeman Gold is a sponsor of the website.