It hasn’t been easy for exploration stage companies lately as the financing window opens and closes erratically. Fremont Gold (FRE.V) took advantage of an open window in January when it announced a C$1.02M financing, which was quickly upsized to almost C$1.5M thanks to a high investor demand.

This puts enough cash in Fremont’s treasury to start drilling the Griffon gold project in June. Further, by adding the former exploration manager of Alta Gold (the past operator of the Griffon gold mine) as a technical advisor, the upcoming exploration program may see an efficiency boost.

A quick recap on the Griffon Gold project

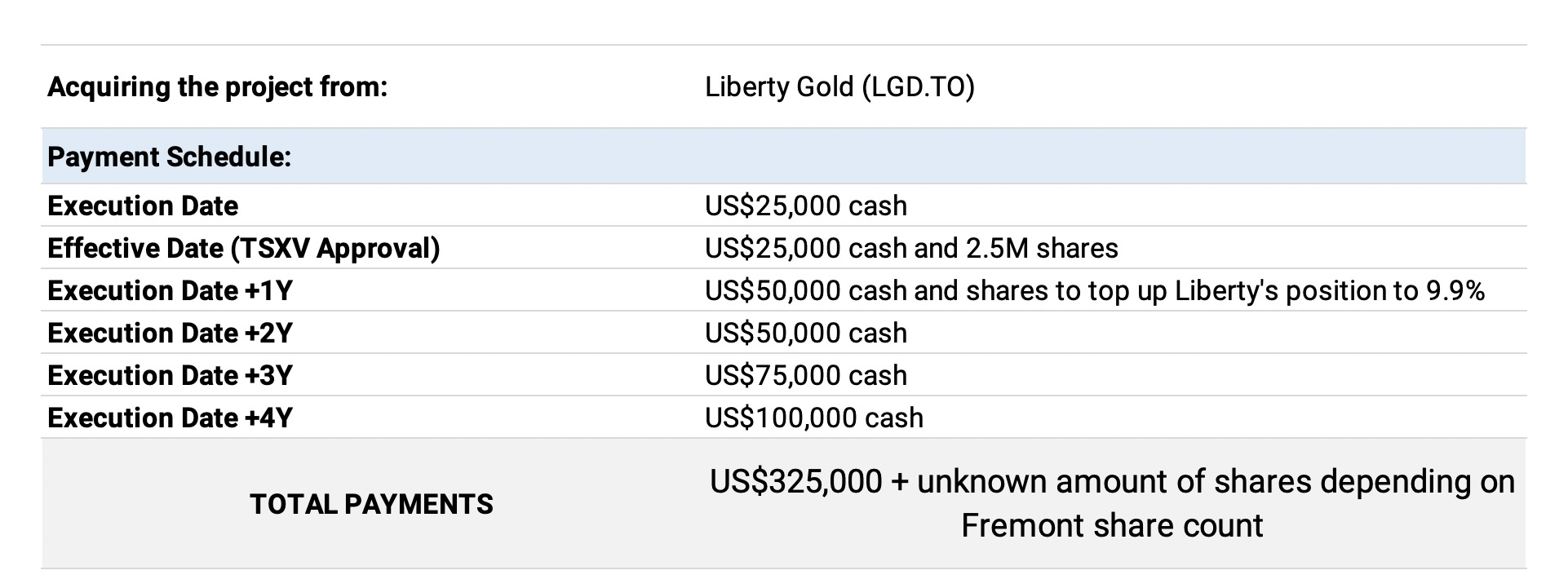

Griffon is a past-producing gold project located at the southern end of the Cortez Trend, less than 75 kilometres southwest of Ely, Nevada. Fremont entered into an agreement with Liberty Gold (LGD.TO), which is focused on the Black Pine exploration project in Idaho, in December to acquire a 100% interest in Griffon. Fremont immediately jumped at the chance to acquire the past-producing Griffon, an oxide heap-leach operation. The earn-in schedule for Fremont is very reasonable with minimal cash payments as Liberty Gold was happy to take Fremont’s stock in lieu of cash payments.

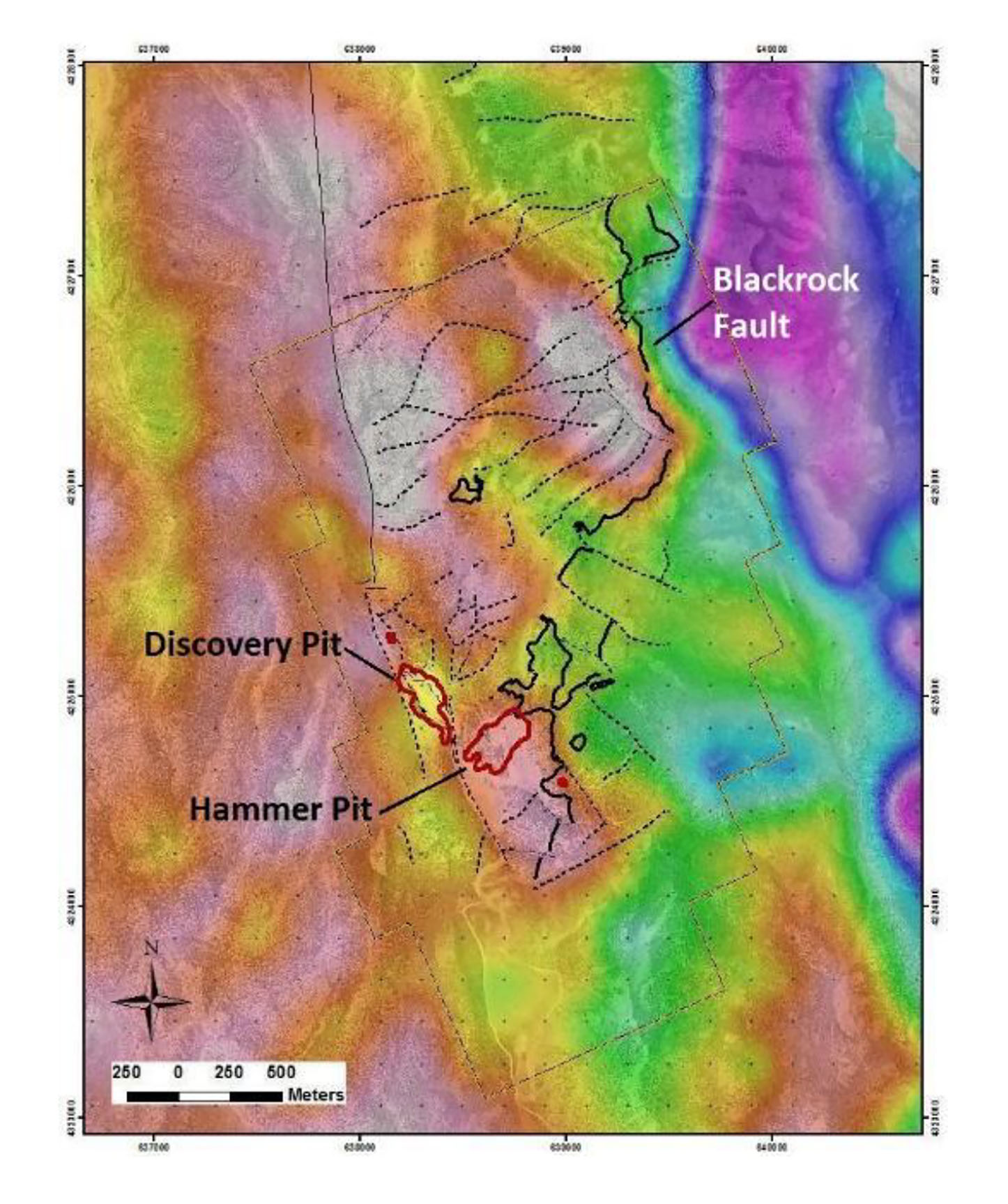

Mineralization at Griffon is Carlin-type and is comparable to the mineralization found at several deposits at the Kinross Bald Mountain Mine complex, approximately 70 km to the north. After the initial discovery was made in 1988, previous operators drilled over 200 holes (outlining two deposits) and quickly brought the project into production in 1997. And although past operators had success with their exploration programs, drilling was principally focused on delineating the two deposits that were subsequently mined.

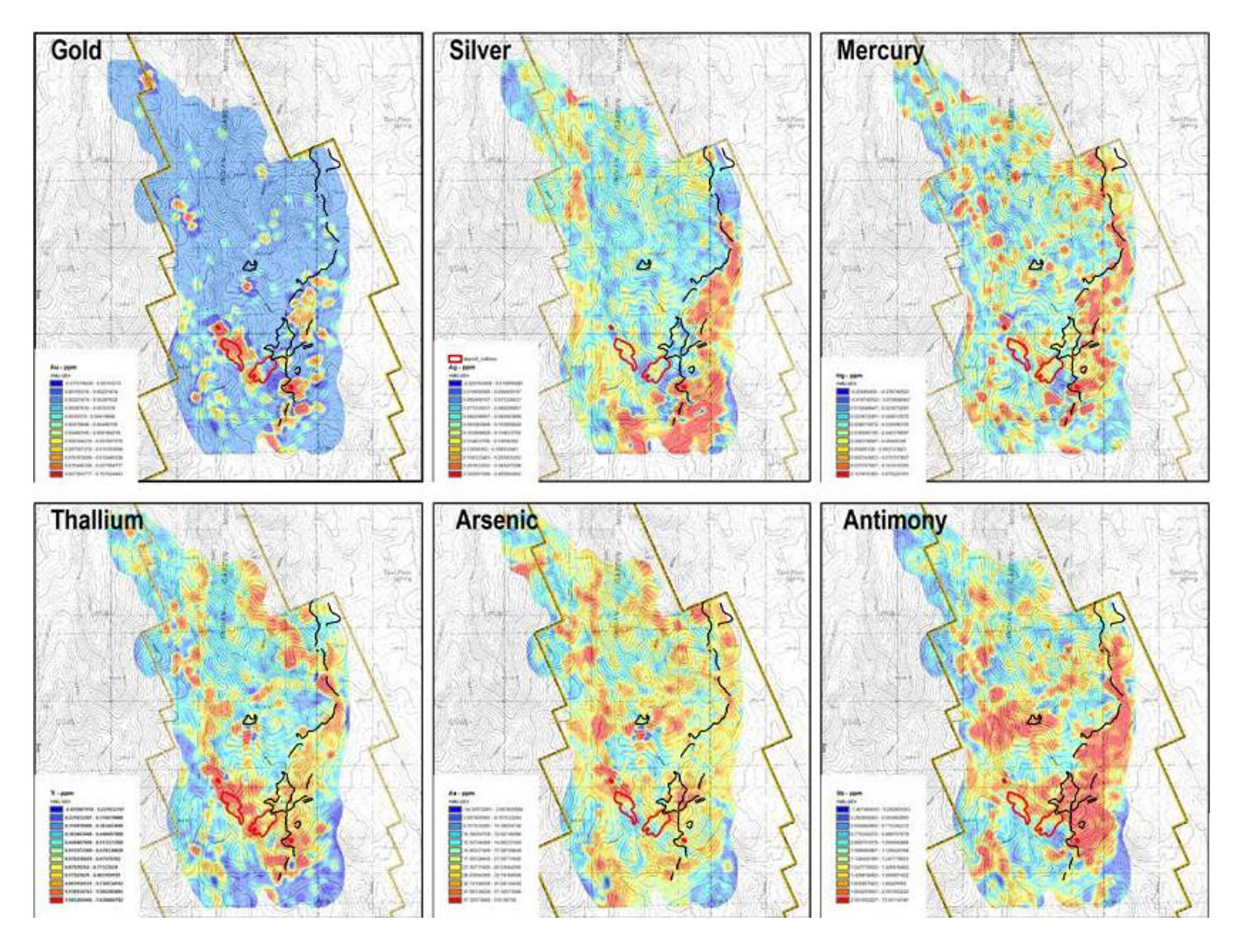

When you couple limited property-wide exploration with a mine life truncated by a collapse in the price of gold in 1999, you have to wonder what exploration potential remains at Griffon. The exploration work completed by Liberty Gold hints at that potential.

Until Liberty Gold acquired Griffon in 2012, no meaningful exploration work had been completed there since the late 90s. The exploration conducted by Liberty Gold was comprehensive and identified numerous untested drill targets (some of them are quite obvious, while others may need to be further developed). While Liberty Gold permitted and bonded Griffon, they never did get around to drilling it, likely because their focus shifted to Kinsley Mountain, then Goldstrike, and now Black Pine. Now Fremont has the golden opportunity to drill Griffon.

For further background to this transaction, we would recommend you to re-read our Q&A session with CEO Blaine Monaghan, conducted in January. You can re-read that interview here.

Fremont just raised almost C$1.5M, keeping the treasury healthy

As mentioned in the introduction, Fremont closed a C$1.48M placement in February after having upsized the placement by almost 50% due to strong investor interest. Fremont issued 24.7M units at C$0.06 with each unit consisting of one common share and a full warrant which will allow the warrant holder to acquire an additional share of Fremont by February 14th 2021 at 10 cents per share. Should these warrants expire in the money (assuming this year’s drill campaign at Griffon will be successful and the market will actually care about drill results), an additional C$2.47M will be added to Fremont’s cash position.

The 24.7M new shares that have been issued increase the share count to approximately 81.5M, while the fully diluted share count has increased to just over 121M shares, which consists of 4.3M options (which are all out of the money) and 35.6M warrants (which are also out of the money).

Additionally, the fully diluted share count will decrease fast. 5.12M warrants at C$0.25 are expiring at the end of June and unless Fremont’s share price quadruples by then (hardly something we would complain about) I dont expect them to be exercised.

It’s also worth emphasizing that the insiders of Fremont are putting their money where their mouths are. Chairman Alan Carter invested an additional C$10,000 (the original filing of C$100,000 appears to be incorrect) while President Dennis Moore and CEO Blaine Monaghan each invested an additional C$25,000 in Fremont Gold, putting their money where their mouths are. These three insiders alone now own combined in excess of 9M shares, which represents in excess of 11% of the current share count.

The capital raise was also necessary as Fremont ended 2019 with a working capital of close to zero. The C$1.4M added to the treasury (net of finders fees and raise-related expenses) boosted Fremont’s working capital position to approximately C$1.2M (our estimate) at the end of its financial year (March 2020) and is sufficient to complete the maiden drill program at Griffon.

Considering that the burn rate (excluding exploration expenses) is just C$200,000 per quarter (as per the most recent financial results, calculated as operating expenses minus non-cash expenses like depreciation and stock-based compensation), raising C$1.4M is a big deal for Fremont as the cash might get them to the end of 2020.

A new technical advisor

As Fremont is fully focused on Griffon, it has assembled a dream team for the next phase of its exploration strategy. Andy Wallace joined the advisory board last year and Clay Newton still is Fremont’s VP Exploration. However, Fremont just added Jamie Robinson as a technical advisor.

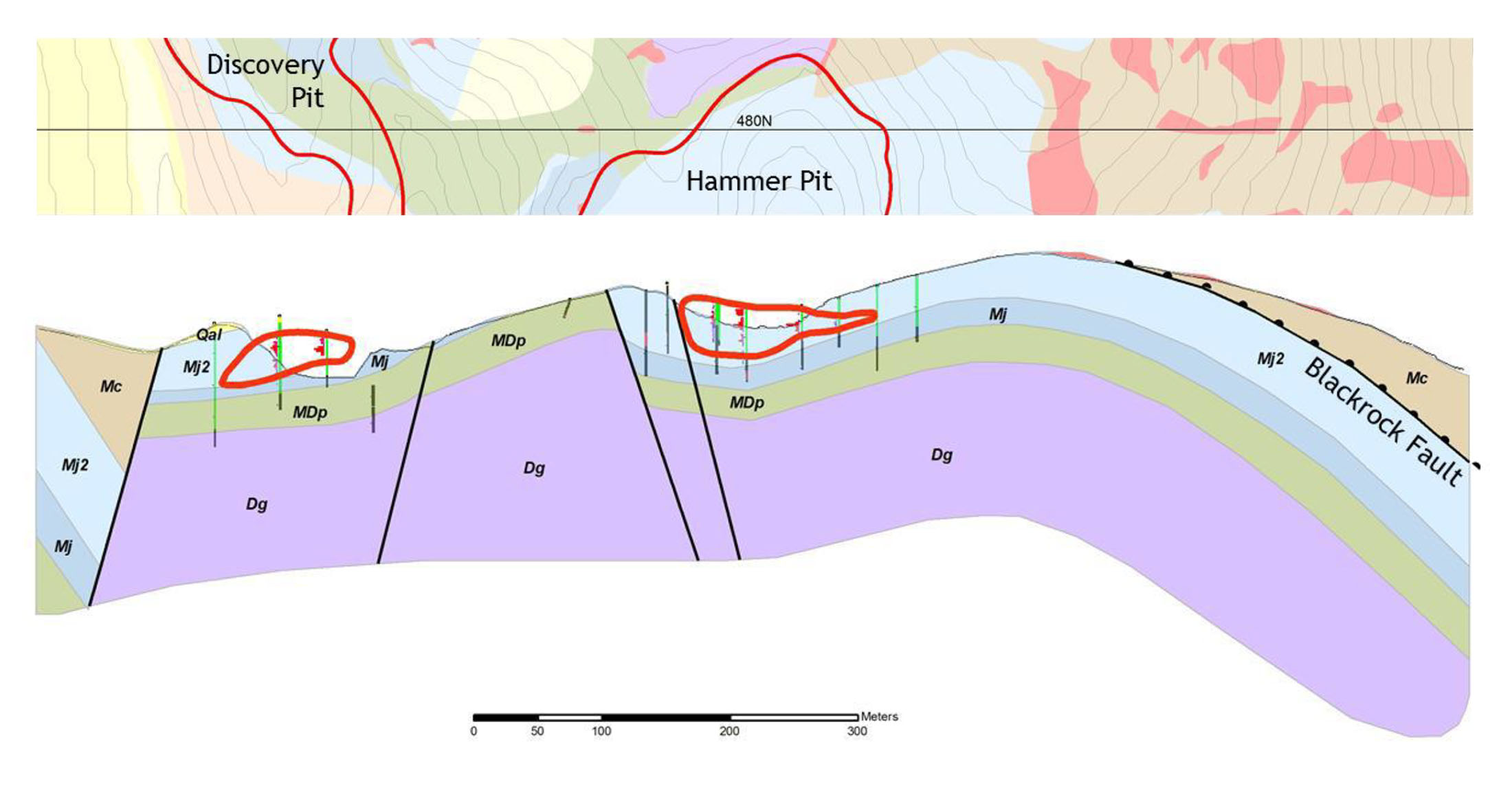

The name may not ring a bell but he may very well be the best man for the job as he has plenty of experience with Griffon. From 1992 to1997, he was the exploration manager of Alta Gold, the previous owner of Griffon, and during his stint with Alta Gold, Robinson discovered the Hammer Ridge deposit at Griffon.

Drilling at the Hammer zone in 1997 intersected thick economic-grade material. A few highlighted intervals include almost 26 meters of 1.1 g/t gold, 47 meters of 0.89 g/t gold and 58 meters of 0.86 g/t gold. It’s important to note that these intervals were not mined, meaning that there is still plenty of gold mineralization in and around the Hammer Ridge deposit. And given the historical recovery rates at Griffon, (almost 88% for crushed material and about 65% for run-of-mine material), you’re doing something very wrong if you can’t make these grades work in Nevada!

Given his direct experience with the project, we expect that Jamie Robinson will help to increase the efficiency of the upcoming exploration program.

Conclusion

It’s no wonder that Fremont jumped at the chance to acquire Griffon. How often does a small exploration company get the opportunity to acquire a past-producing gold mine, with ready-made, untested drill targets, in one of the world’s best gold trends? With a healthy treasury and a first-class exploration team, we expect Fremont Gold to hit the ground running when the drills start turning in June.

Disclosure: The author holds a long position in Fremont Gold Ltd. Fremont Gold Ltd. is a sponsor of the website.