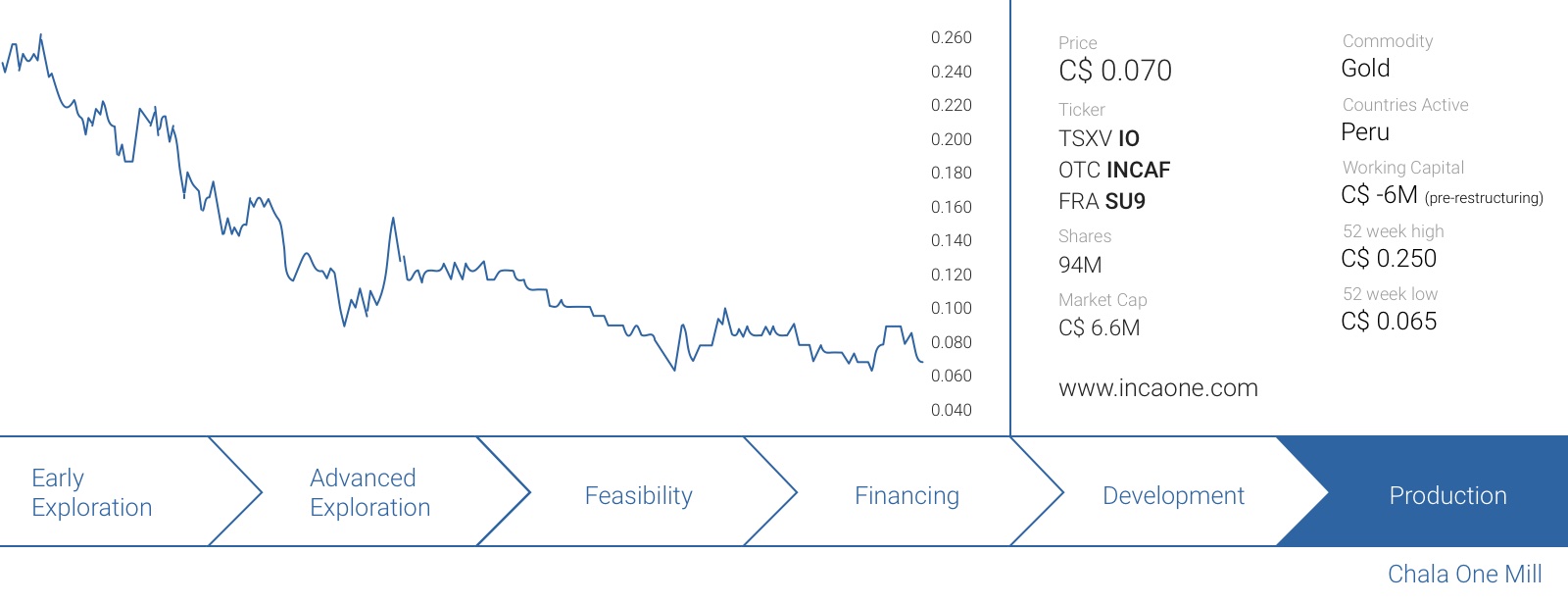

Inca One Gold (IO.V), our favorite toll milling idea in Peru, recently had to reduce its throughput at the Chala One processing plant once again, as the lack of funds prevented the company from buying more ore. However, the company is currently in the process of restructuring its balance sheet and the new cash inflow should allow the company to get back to 100 tonnes per day (on a sustaining basis) in no time!

Inca One Gold (IO.V), our favorite toll milling idea in Peru, recently had to reduce its throughput at the Chala One processing plant once again, as the lack of funds prevented the company from buying more ore. However, the company is currently in the process of restructuring its balance sheet and the new cash inflow should allow the company to get back to 100 tonnes per day (on a sustaining basis) in no time!

The terms of the agreement

Inca One’s balance sheet had quite a bit of debt on it, and the company has now entered into an agreement with its lenders to restructure US$10M of debt in three different phases. 30% of the debt will be cancelled and re-issued at the same terms of the new 2 year bond (see later), whilst another 20% will be converted to a contingent debt security payable when Inca One meets certain and pre-defined performance metrics.

Half of the debt will be converted into common stock at a fixed price of C$0.11 (which will result in an additional 59 million shares being created) and this is very likely the most important part of the restructuring. US$5M of debt will be removed from the balance sheet and converted into stock at a substantial PREMIUM to the market price, rather than a discount. Not only will this result in a healthier debt/equity ratio on the balance sheet, it will also reduce the interest expenses by in excess of half a million Canadian Dollar per year.

One of the requirements of this recapitalization and restructuring plan is Inca One Gold will have to raise US$3M in a new convertible bond offering (and the company has already received a commitment for 1/3rd of the total amount). This new bond will have a 24 month term and a 10% coupon. The interest will be payed quarterly but the first interest payment has been deferred to 9 months after the issue date. That’s an excellent clause as this allows Inca One to ramp the production back up to 100 tonnes per day and use the operating cash flow to pay the interest on the new debt.

The new debt can be converted into common shares at C$0.10, C$0.15, C$0.20 and C$0.25 per share in 4 different tranches per six months. So after six months, the debtholders can convert 25% of the debt into common stock at C$0.10, after 12 months an additional 25% can be converted into common stock at C$0.15, and so on. Should all debt be converted into common stock, an additional 45 million shares will be created, resulting in a fully diluted share count of almost 186 million shares.

What will Inca One be able to do with the additional US$3M cash injection?

The short answer is: ‘basically everything it wants to’.We were in Vancouver in April and had a chat with management who think they will only need $1.5M to be able to ramp the plant back up to the nameplate capacity of approximately 100 tonnes per day. The 1.5 million should be sufficient to purchase a certain amount of ore which would cover the working capital needs of the plant.

Obviously there is always a time gap between the moment Inca One purchases- the ore it wants to process, and the moment it gets paid for the gold (and silver) that has been recovered from that ore. This was the company’s Achilles heel in the past. Inca One seemed to have underestimated the working capital needs as the repayment of the IGV (Value Added Tax) bills took longer than expected. It’s too bad Inca One had to learn this the hard way but as the company is now receiving IGV repayments on a regular basis, this issue has now been dealt with.

One of the questions we received quite often was whether or not Inca One was able to purchase a sufficient amount of ore from the small-scale miners.

Whenever Inca One was able to get some money in the till, the company was immediately able to increase its ore purchases. Back in March last year the company purchased 1269 tonnes of ore and was able to immediately increase the amount of ore it could get its hands on by exactly 100% to 2537 tonnes just two periods later! Within weeks after receiving a cash injection, Inca One increased its ore purchasing rate by almost 40%. So, yes, we are confident Inca One will continue to be able to buy the amount of ore it needs to keep the plant up and running at 100 tonnes per day, there’s no shortage at all.

The implications of being a ‘large company’ according to the SUNAT rules

Inca One has now also been promoted to the ‘large tax group’ status at SUNAT (the Peruvian tax authority), and this has one very important implication. Because of its status, Inca One is now allowed to claim tax repayments on a monthly basis. This will have a huge impact on the company’s operations as this reduces the turnaround time between having to pay IGV for the ore it purchases and the repayment from the government. And as you can imagine, a shorter turnaround time also reduces the working capital need to bridge the gap in-between paying the IGV and receiving a cheque from SUNAT.

Since January, Inca One has already received repayments totalling US$755,000. Not only is this cash infusion very welcome, it also shows the SUNAT is perfectly comfortable with Inca One’s operating style and no issues have been raised.

That being said, two large IGV claims are still being audited by SUNAT, and we expect this audit process to be concluded in the very near future (before the summer). Should SUNAT indeed complete the audit of the two claims and send Inca One the cheque, the company can add an additional US$1.58M to its treasury, and then we’re really off to the races.

Conclusion

From a technical point of view, there was and still isn’t anything wrong with Inca One Gold. The company was able to secure ore and had no problems at all to recover the gold and silver from the ore, so the Chala One facility is operating as planned. The only issue Inca One had to deal with was a cash crunch as the turnaround time between paying the IGV and getting a cheque back from the government was hurting the company’s working capital position.

This resulted in some sort of negative financing spiral as Inca obviously still had to pay its employees and service its debt. The current recapitalization plan solves these issues and the total debt will decrease from US$10M to US$6M, even though the cash position will increase by US$3M. Yes, the total share count will increase and if the remainder of the convertible debt would be converted into common stock, Inca One will have in excess of 185 million shares outstanding.

But even then it would remain an interesting opportunity. Even with the expanded share count, the company would command a valuation of approximately C$0.27 based on a production scenario of 100 tonnes per day, processing ore at an average grade of 0.7 ounces of gold per tonne of rock and an EBITDA multiple of 9.

Inca One Gold is a sponsor of the website, we hold a long position. Please read the disclaimer