Sometimes companies don’t have to do anything fancy to attract attention. Integra Resources (ITR.V) doesn’t need Integra Gold’s fancy Gold Rush Challenge as an element to draw the market’s attention as simply executing on the business plan is sufficient to keep investors interested in the story.

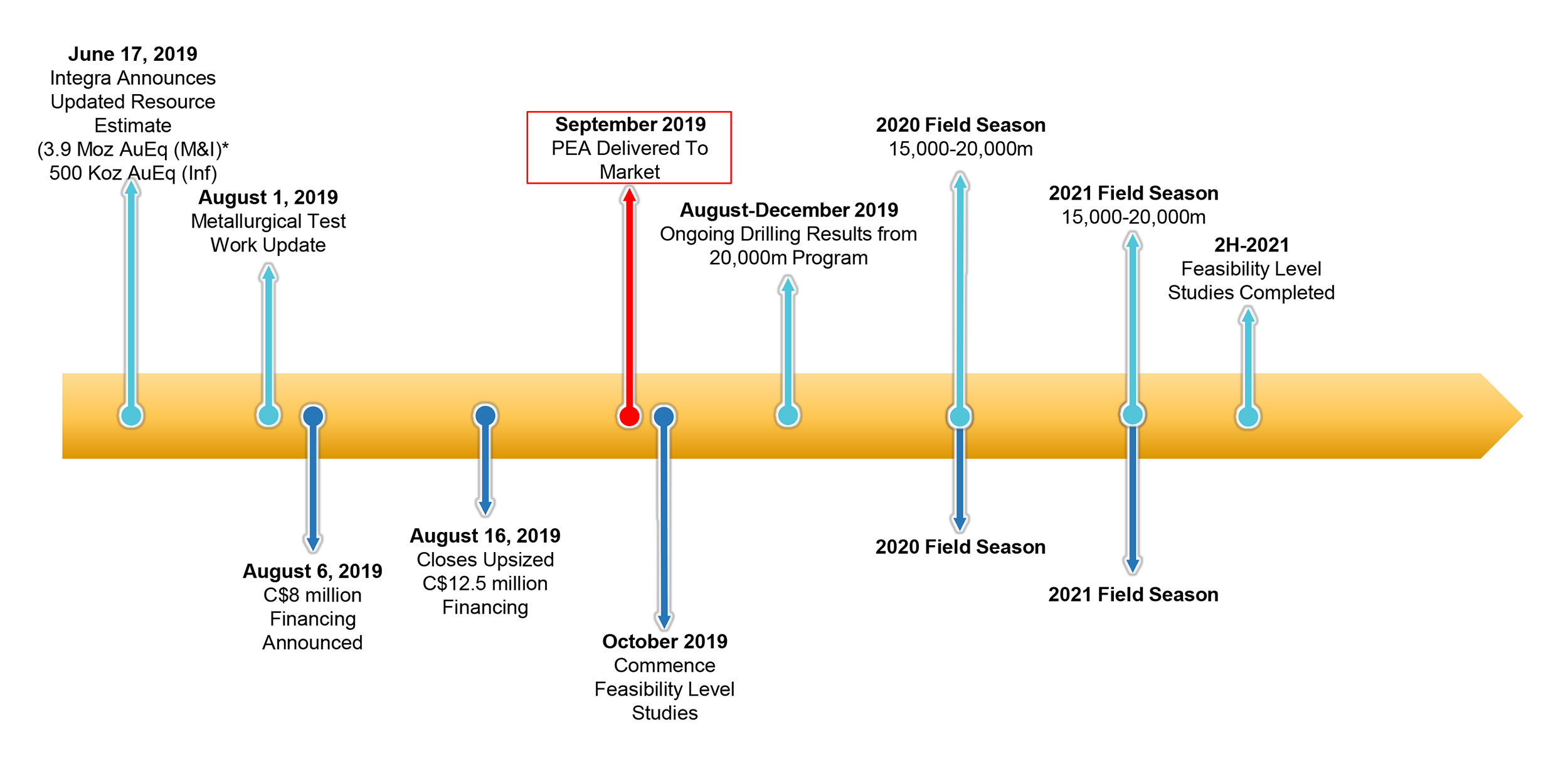

Just over two years after initially acquiring the DeLamar project, Integra has already published two resource estimates and used the most recent resource (with most gold and silver ending up in the measured and indicated resource categories) to complete a Preliminary Economic Assessment which confirmed the excellent economics of the DeLamar project. And this whilst the PEA focused on the heap leach side of the project and barely included any sulphide zones.

A look at the PEA numbers

As expected, the PEA was predominantly focusing on bringing as much of the heap leachable tonnage into the PEA as this would allow Integra to keep the initial capex low which would in turn:

- Increase the Internal Rate of Return

- Reduce the payback period and

- Boost the life-of-mine cash flows

As a direct consequence, the low capex and high internal rate of return also means Integra could be in a position to develop the project themselves.

And it looks like Integra succeeded as the initial results indicate a total of 1.03 million ounces and 16.6 million ounces of silver will be recovered from processing almost 94 million tonnes in a combined heap leach and milling scenario. The summarized results speak for themselves:

The main takeaway is the after-tax NPV5% of C$472M (C$5.14/share) at $1350 gold and $16.90 silver which increases to C$623M (C$6.79/share) at $1500 gold. Keep in mind the NPV/share is based on the current share count of 91.8M shares and the share count will obviously increase should Integra decide to put the project into production themselves. But even if you’d use a share count of 190M shares (the additional 95M shares would allow Integra to raise roughly C$115M at the current share price), it’s clear the value per share is higher than the current C$1.25-1.30. The conclusion is quite simple: it’s a good and robust PEA, and the value is mainly generated through the low-cost heap leach phase which will auto-fund the construction of the mill in the second year of the operations.

Also, keep in mind the economics were based on a base case scenario of $1350 gold and $16.90 silver and the current prices for both precious metals are quite a bit higher with gold hanging in there around $1500/oz and silver hovering around $18/oz. The sensitivity analysis of the calculations also provides interesting additional information.

At $1500 gold, the after-tax NPV5% increases by $106M to US$464M which is approximately C$600M at the current exchange rate. The after-tax payback period would decrease to just below 2 years while the Internal Rate of Return would be boosted to 54%.

But even if you’d look at the other end of the spectrum the DeLamar economics continue to impress. At $1200 gold the project remains viable with an after-tax NPV5% of around C$330M and an IRR of 32%, and the relative resilience to lower gold prices will make this project very appealing to pretty much any mid-tier and senior producer who’s looking to add commercially viable ounces in a Tier-1 jurisdiction.

We identified several areas that could boost the economics

Basically it’s a numbers game and although no two projects are 100% equal, we do have the impression Integra’s consultants have been quite conservative with their cost projections. One easily identifiable example would, for instance, be the processing cost per tonne of rock in the heap leach scenario.

The mining cost

It looks like the technical report used a mining cost of $2.20/t and a processing cost of $3-3.35/t for the heap leach operation. A mining cost of $2.20 is relatively conservative for a mining scenario with a daily tonnage of 54-55,000 tonnes (consisting of 27,000 tonnes per day of rock that will be processed and a similar amount of waste material) as the economies of scale could play a very important role here and it could perhaps be possible to reduce the mining cost to around $2/t. Considering the combined strip ratio will be around 1 (sub-divided in 0.65 for DeLamar and around 1.20 for the Florida Mountain pit) and almost 10 million tonnes of rock will have to be moved on an annual basis the $2.20/t used in the technical report are relatively low.

The processing cost

Secondly, we were a bit surprised to see the processing cost of $3.35/t in the resource calculation and the use of $3.35/t at DeLamar and $3/t at Florida Mountain. Again, we realize no two projects are the same but when you see how both Fiore Gold (F.V) and SSR Mining (SSRM, SSRM.TO) use a processing cost of around $1.25/t for their own heap leach operations in Nevada, we do have the impression the processing cost per tonne appears to be very conservative as well. And while the DeLamar project may not be able to benefit from Nevada-specific elements, it shouldn’t be too tough to reduce those processing costs. We’re not saying $1.25/t will be feasible but $2-2.50 should be the target.

And if the mining costs could be cut by $0.10 to $2.10/t and the processing cost drops to $2.50/t (so we’re not exaggerating in our assumptions), the total operating cost per tonne of rock would drop by $0.85/t. This sounds absolutely meaningless but as the average processing cost per tonne of rock is estimated at $7.82/t, the total production cost could be cut by in excess of 10%.

Of course this is just a theoretical improvement for now, and it will be up to Integra to try to reduce these operating expenses.

The sulphide resources

Additionally, it looks like the mill to process the sulphide resources is just in the PEA on a pro-forma basis. The contribution of processing the sulphides is just around 1/10th of the total NPV and seems to serve as a primary stepping stone. The capacity of the plant in the Preliminary Economic Assessment is just 2,000 tonnes per day and only 4.3 million tonnes of rock will be processed in the mill.

We expect Integra to spend more time on the sulphide zones to bring more of the material into the mine plan which will very likely require Integra to re-think the size of the mill and expanding it from 2,000 tonnes per day to perhaps 10-15,000 tonnes per day should help the company to unlock the eyed economies of scale. Of course, everything will depend on a subsequent trade-off study; are the expected additional cash flows high enough to justify the construction of a larger (read: more expensive) mill? And the more ounces captured in sulphide mineralization (at an acceptable grade), the more likely it is for Integra to increase the mill capacity and adding more years to the mine life.

The exploration upside

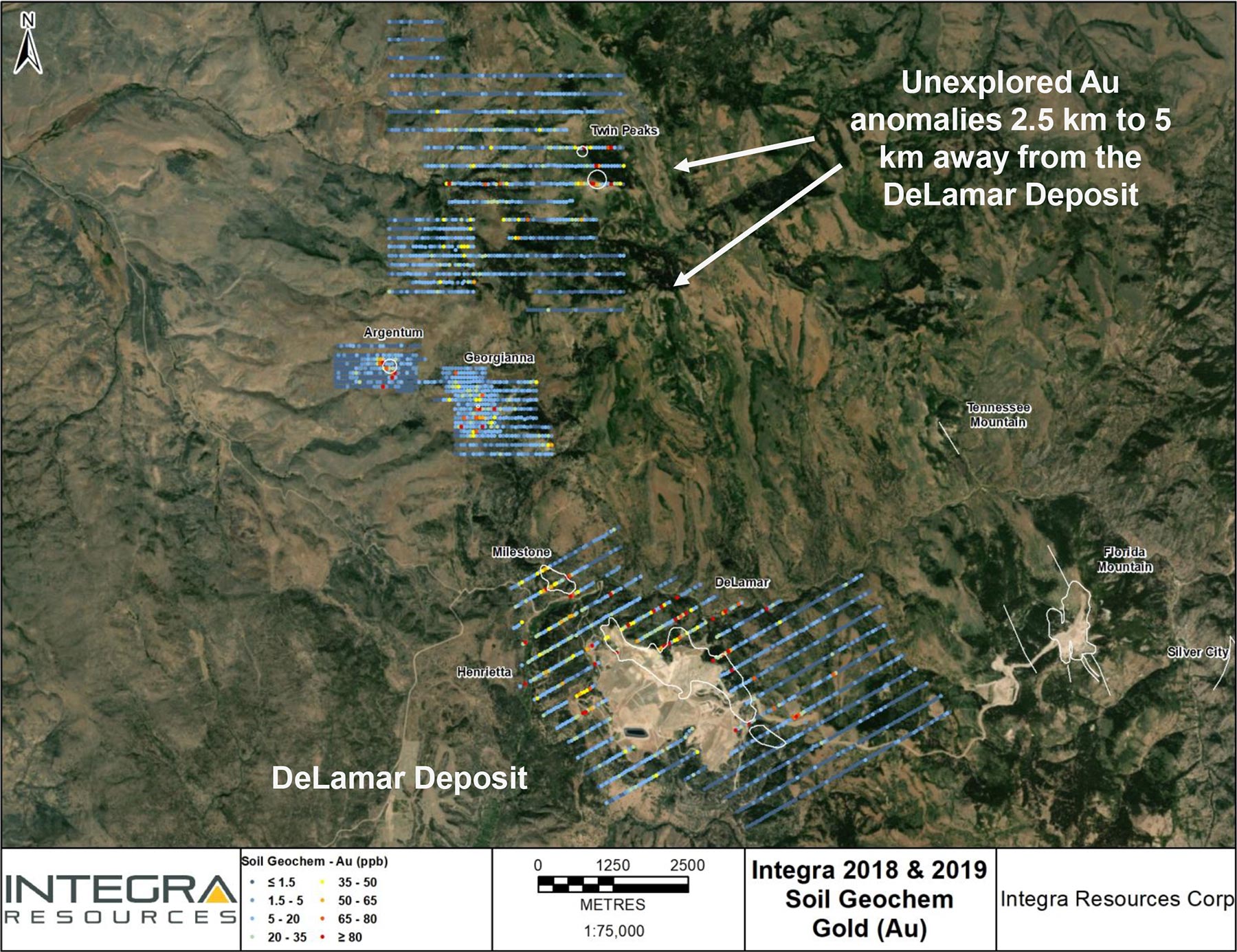

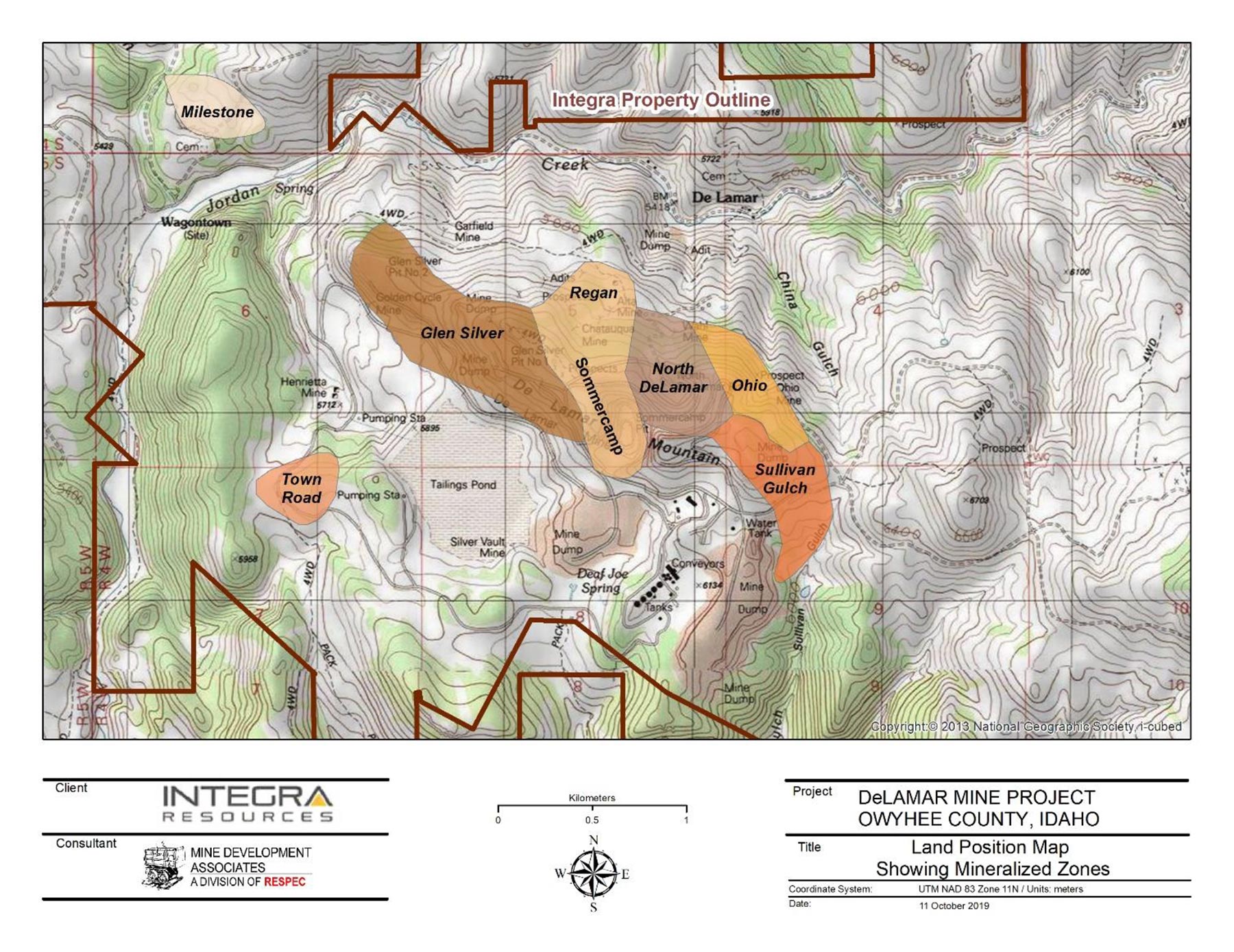

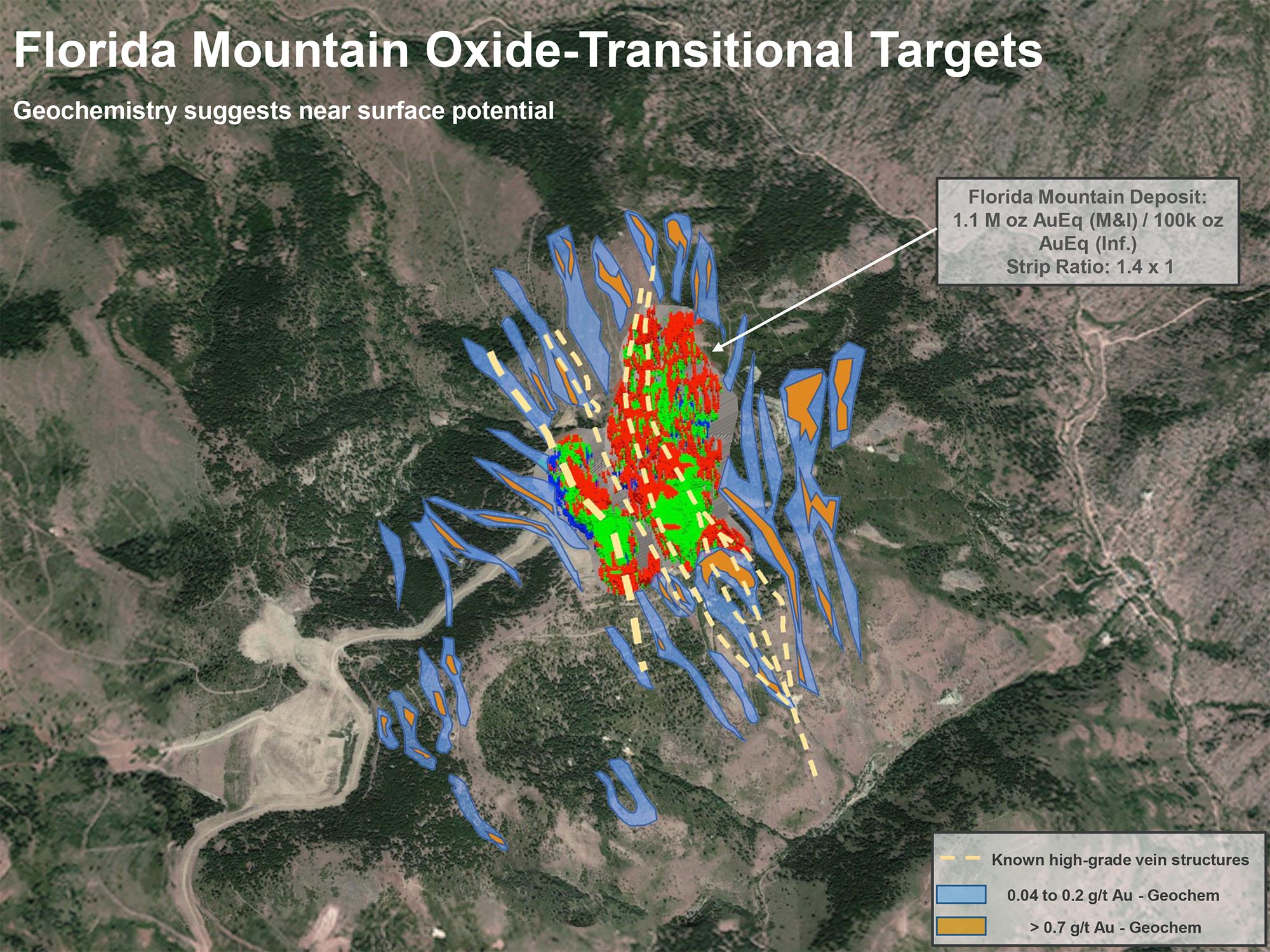

And finally, continuing to explore the DeLamar and Florida Mountain deposits as well as the other targets in the neighborhood could also help to add more value. Previous drill campaigns have already identified a few higher-grade vein zones. The company will probably follow up on these veins in one of the upcoming drill campaigns. We are particularly interested in seeing some more work around the Trade Dollar/Black Jack vein which has historical workings from the 19th century extending up to 600 meters further away from the current resource envelope while virtually no drilling has taken place to test for additional extensions (either lateral or at depth). Additionally, the Milestone zone (to the northwest of Glen Silver) has never been drill-tested for higher grade mineralization at depth.

And of course let’s not forget less than half of the currently know resource is included in the mine plan. The more ounces that will end up in the DeLamar mine plan, the better the economics will be as the initial capex is a sunk cost anyway.

What’s the plan from here on?

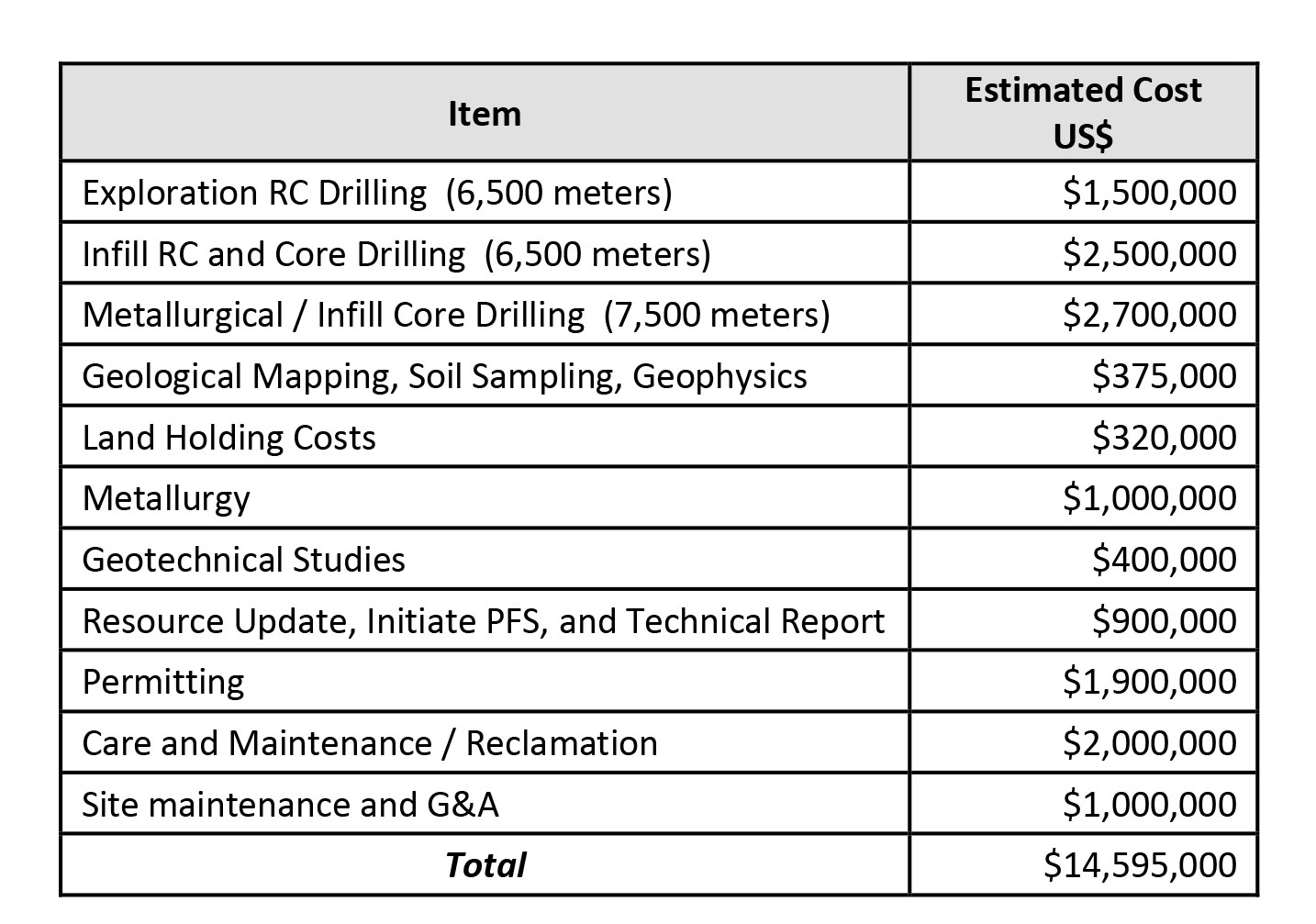

The PEA contained a summary of the recommended plans for Integra to move ahead with the project in order to bring everything up to (pre-)feasibility level. The total budget for these activities was estimated at US$14.6M (almost C$20M) and based on conversations with a company representative Integra seems to think this is a fair estimate and is budgeting a similar C$20M to complete the next study.

As you can see in the previous table, approximately US$5.2M has been earmarked for infill drilling (both RC and core drilling) and to perform additional metallurgical test work on fresh core samples.

We also notice there’s a US$1.5M allocation for exploration drilling but we expect Integra to remove this part from the PFS/FS budget and allocate the corresponding C$2M exploration expenditures as part of the planned C$20M exploration program over a two year period.

That C$20M program will be split up in roughly three sessions of 20,000 meters of drilling and as the first phase has already commenced in August we expect to see the initial drill results within the next few weeks.

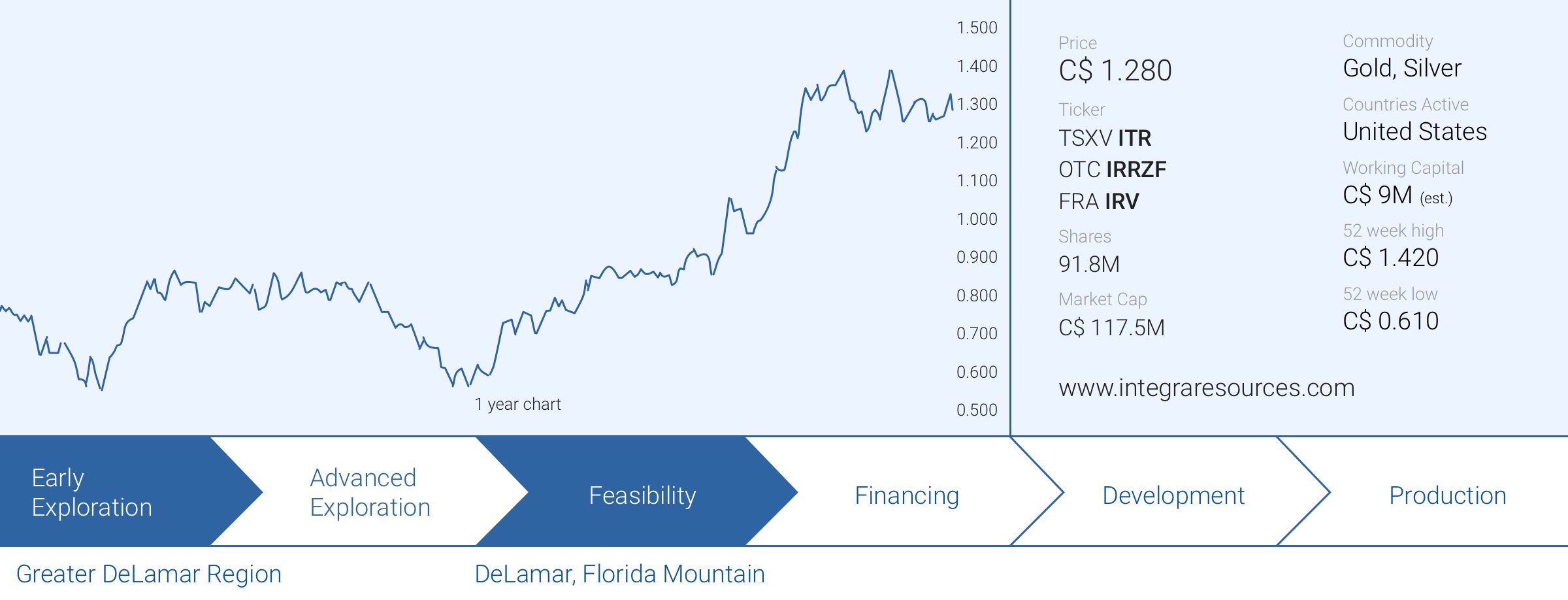

Integra’s financial situation

Back in August, Integra Resources was able to announce and almost immediately close a substantial capital raise as it issues 14.49 million special warrants at C$0.86 per special warrant. Each special warrant was subsequently converted into a common share of Integra after having published a short form prospectus. As this financing was completed without attaching a warrant and by applying only a small discount to the share price right before announcing the cash call, it was a pretty good deal as it allows Integra to have enough cash on hand to immediately work on a 15-20,000 meter drill program while making the final cash payment to Kinross Gold (KGC, K.TO) as part of the DeLamar purchase agreement.

As of the end of June, Integra’s balance sheet showed a negative working capital position of C$300,000 (which already included the promissory note liability – the final Kinross payment) so we expect Integra’s balance sheet at the end of September to show a working capital position of around C$9M considering the company has restarted drilling.

The existing cash position should last until well into next year, but we expect Integra Resources to raise more money in the first semester as it embarks on its plans to get to a pre-feasibility or a feasibility study as fast as possible.

The company signaled in Brussels it’s still undecided on whether it will complete a pre-feasibility study on the DeLamar project or if it’ll skip that step by moving straight ahead to a full feasibility study. Integra has already started feasibility-level studies but the final decision will depend on the engineering work that needs to be conducted as part of the FS. We expect Integra to make a decision in the next few months.

Integra did mention it expects to need approximately C$40-50M to complete the feasibility study, which includes roughly C$20M of additional drilling on the DeLamar and Florida Mountain deposits to further increase the total resource base and to once again increase the confidence in the resource by converting a large part of the measured and indicated resource into a reserve category. The C$40M guesstimate appears to include a certain margin of safety but nonetheless, we would be very impressed if Integra Resources could move from project acquisition to a feasibility study in 4.5 years while keeping the share count limited to 125 million shares (currently: 91.8M shares outstanding).

And considering the massive amount of drilling that will occur between now and the completion of the feasibility study, as well as the potential cost-saving items we discussed, we would be very surprised if the definitive feasibility study would indicate weaker economics than the PEA. And that’s something that would almost be unheard of in this sector.

Conclusion

Integra had no issues this summer to raise C$12.5M in a no-warrant and almost-no-discount financing this summer. The funds that were strategically placed into that financing round must be happy as Integra’s share price is still trading approximately 50% higher. Although the PEA is a very important milestone for the company, one should not underestimate how important having access to capital is these days for PEA-stage companies. There are plenty of other companies in Integra’s peer group that may have an interesting project as well but are simply unable to raise the cash needed to further develop the asset.

The PEA confirms the expectations DeLamar could be a high-margin asset but keep in mind this first study very likely is just the first stepping stone. Over half of the resource isn’t even included yet while the regional exploration programme should also add more ounces to the overall mine plan in the next few updates.

The PEA is an excellent start, but there still is so much more to come.

Disclosure: The author holds a long position in Integra Resources. Integra Resources is a sponsor of the website.