K92 Mining (KNT.V) continues to develop its gold mine in Papua New Guinea at an aggressive pace. The 500 tonnes per day mill is up and running now, and in a recent press release, K92 Mining confirmed it’s now expecting the average grade of its ore to increase compared to the production plans.

K92 Mining (KNT.V) continues to develop its gold mine in Papua New Guinea at an aggressive pace. The 500 tonnes per day mill is up and running now, and in a recent press release, K92 Mining confirmed it’s now expecting the average grade of its ore to increase compared to the production plans.

The first two stopes are now expected to contain a total of 2,390 ounces of gold (compared to 1,550 ounces), at an average grade of 9.21 g/t gold (versus a previous estimate of 5.82 g/t). That’s a very positive achievement, as these two stopes are located on the southern part of the currently known resource estimate, and lower grades were expected due to the limited amount of drilling on those zones.

Let’s refresh your memory on the background of the Kainantu mine

Two years ago, Barrick Gold (ABX, ABX.TO) faced a cash crunch and started to unload smaller non-core assets to get rid of them on the balance sheet. Unfortunately (for Barrick, but fortunately for K92 Mining), a lot of good projects were sold at rock-bottom prices, and K92 Mining was able to acquire the past-producing Kainantu mine for $2M in cash, and up to $60M in milestone payments.

The asset was taken public through a Reverse Take Over (‘RTO’) of Otterburn Resources, and K92 has been listed since the end of May. Originally raising cash at C$0.35, its share price immediately increased to in excess of C$2 before losing some ground again and ending up in the lower C$1-rarnge. Unfortunately, the recent contraction in the gold price has caused more people to go back to the sidelines, and K92’s share price has now fallen to less than a dollar per share, which drastically improves the risk/reward ratio.

At the end of September, the mill at the Kainantu mine has processed the first batch of underground ore, and concentrate is being produced as we speak. We haven’t seen a production update recently, but we expect an imminent update on the first concentrate shipment and anticipated gold production before the end of this year. The ramp-up to the nameplate capacity of the mill is ongoing, and CEO Ian Stalker confirms the company is now aiming to reach the targeted design production rate in the next quarter. This will be a huge step forward and a major milestone, as we think that a continuous quarterly production update might help the market to truly understand the value of being a producing gold miner.

An updated technical report contained a simplified mine plan and cash flow model for Irumafimpa, and AMDAD expects the mine to generate a total net cash flow of $153M, for a NPV8% of $110M. Another, simplified mine plan, calls for a total production of 133,000 ounces of gold, and has a DCF8% valuation of $49M.

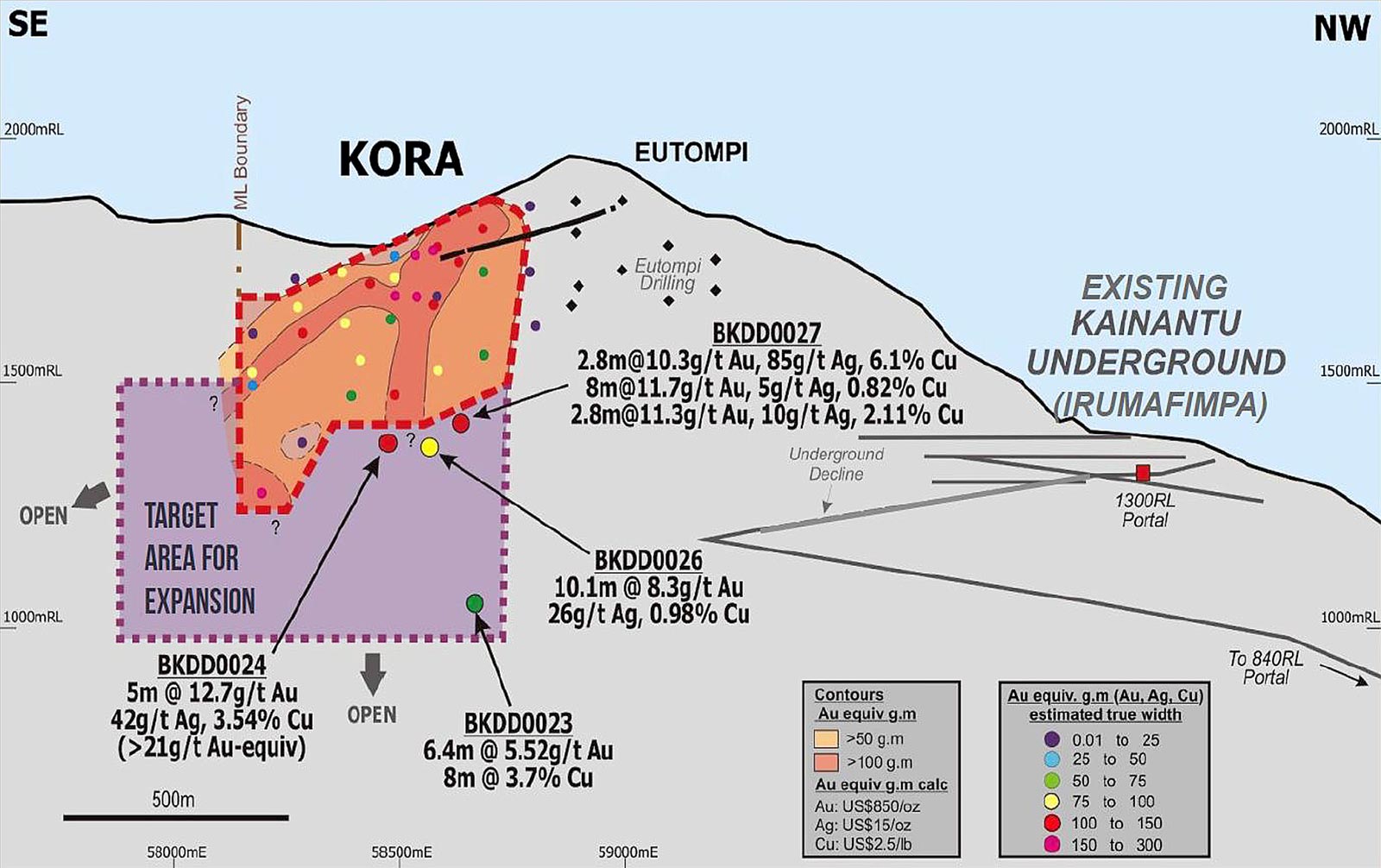

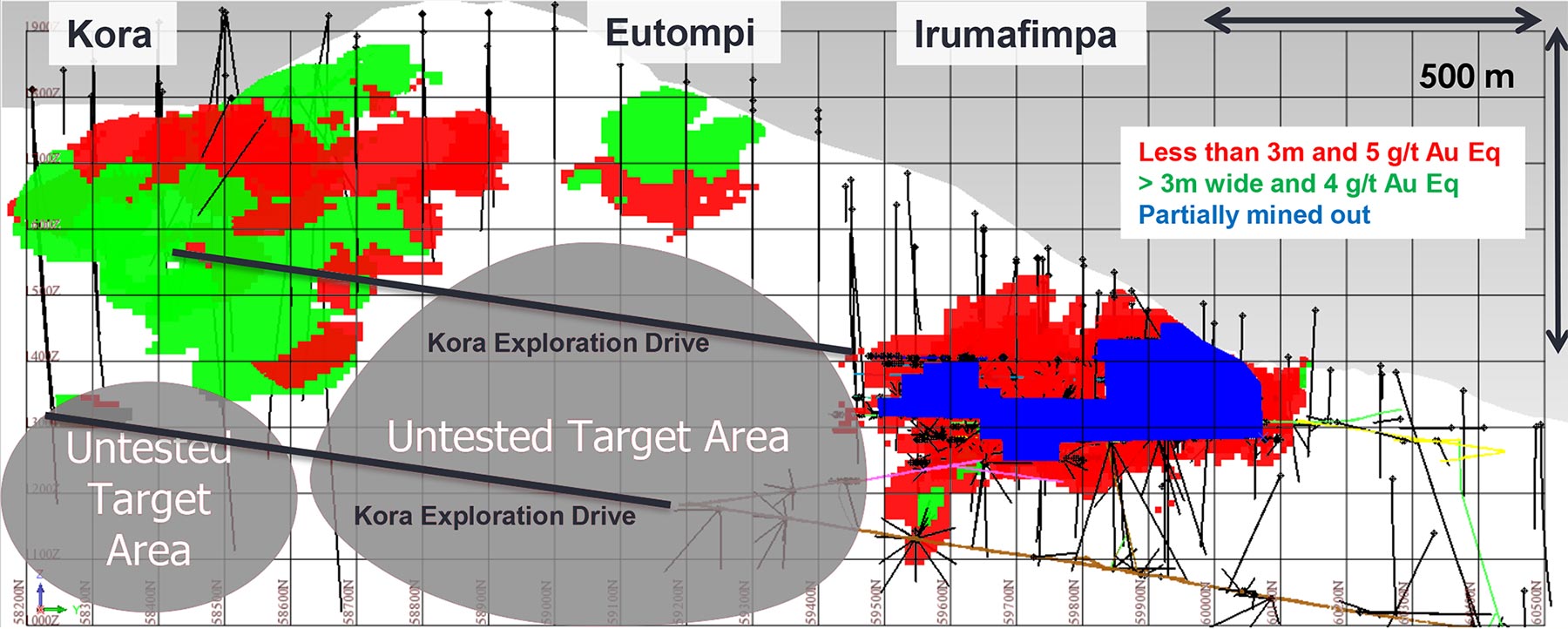

But let’s face it, Irumafimpa – the zone K92 is currently mining – is just a ‘warm-up exercise’. The real money will be made at the larger Kora zone, which is located on the other side of the hill.

The Kora PEA

As Irumafimpa will have a mine life of just a few years (although this could be extended to 7-9 years), K92 Mining has been taking care of the planned second stage of the project. The company is planning to push an underground development work towards Kora from the existing underground infrastructure at Irumafimpa.

As there was a historical resource estimate on the Kora zone, K92 has immediately moved onto determining the viability of Kora by commissioning and publishing a Preliminary Economic Assessment.

In this PEA, K92 Mining used a total mine life of 9 years, wherein a total of 3.2 million tonnes would be processed (at an average grade of 7.1 g/t gold, 25 g/t silver and 1.7% copper). K92 Mining made the right decision to commission a scoping study to determine the impact of a throughput increase of the processing plant by Mincore, as it allowed the company to give the other independent consultant, AMSAD, which was completing the PEA on the Kora deposit. K92’s input was particularly helpful on the G&A expenses and processing cost per tonne, which reduced the total operating cost per tonne by in excess of 10%, to $125/t.

The initial capex of the development of the Kora deposit is estimated at just $14M, which once again emphasizes the importance of having all infrastructure-related assets already in place. The mill could be expanded for just a few million dollar, and the ‘real’ development cost of Kora Underground is just over 10 million dollar. This does exclude the exploration inclines and additional core drilling, and the additional sustaining capex which is budgeted at $64M. This additional $64M is actually very reasonable as this is just $100 per produced ounce of gold and that’s not too high for an underground mine which will need continuous underground development.

As you can imagine, this low initial capex results in superior economics of this underground mine, which has an average gold-equivalent grade of just below 10 g/t. This results in an annual production rate of 82,500 ounces of gold, 290,000 ounces of silver and 13.4 million pounds of copper, and K92 Mining thinks it will be able to start to put the Kora mine into production in 2018.

According to AMSAD’s calculations, the total revenue of the production plans at Kora will be almost $340/t, which provides a really healthy margin based on an expected production cost of just $125/t. The Discounted Cash Flow calculation (using a discount rate of 8%) comes in at $341M, using a gold price of $1300/oz and a copper price of $4,800/t. We’ll ignore the silver price for now, as the total expected silver revenue represents less than 4% of the total revenue per tonne. So, for now, we’ll consider the silver revenue to be the proverbial ‘cherry on the cake’.

According to the mine plan, based on the aforementioned commodity prices, the mine will generate a positive cash flow of $35M in year 2 (which is actually the very first year the plant will be running at in excess of 90% of its designed capacity), and a total DCF 8% of $341M. It’s not always right to take these results at face value, but if we would use an USD/CAD exchange rate of 1.33, the DCF8% expressed in Canadian Dollar is approximately C$453M, or C$2.85 per fully diluted share. That’s impressive, and it will be really interesting to see of K92 Mining will be able to live up to these expectations.

Why the current lower gold price shouldn’t worry you too much

Granted, the Kora PEA was based on a gold price of $1300/oz, and as the current gold price is just $1180/oz, you could be worried the economics of the Kora deposit will crumble.

Well, there’s no real reason to be scared, as the lower gold price is being compensated by the (much) higher copper price. Whilst the gold price is currently approximately 10% lower than the price used in the base case scenario of the PEA, the copper price is currently $5,850 per tonne, compared to the $4,800/t used in the PEA;

The metallurgical test work on the Kora deposit in 2009 confirmed a recovery rate of in excess of 90% for both the copper and the gold (which is really great!), but as we like to be a bit more conservative, we will use an 85% recovery rate for both metals. This leads to the next net amount of produced ounces of gold and pounds of copper. We are also using the base case scenario of $1300 gold and $2.18 copper for our base case revenue calculation.

[table caption=”” colalign=”center|right|right|right”]

YEAR;Gold production (koz) at 85% recovery;Copper production (Mlbs) at 85% recovery;Revenue (1300 gold, 2.18 copper) (rounded!)

1;9,500;2.2;17

2;57,000;14;104

3;65,000;15.8;118

4;75,000;15.8;140

5;82,000;15.8;134

6;77,000;14;136

7;82,000;13;133

8;92,000;13;150

9;69,000;12.8;118

;;;1050

;;;

[/table]

The total revenue based on these parameters (excluding the silver) is $1.05B. But what would happen if we would use a gold price of $1175/oz, and a copper price of $2.65/lbs?

[table caption=”” colalign=”center|right|right|right”]

YEAR;Gold production (koz) at 85% recovery;Copper production (Mlbs) at 85% recovery;Revenue (1175 gold, 2.65 copper) (rounded!)

1;9,500;2.2;17

2;57,000;14;104

3;65,000;15.8;118

4;75,000;15.8;130

5;82,000;15.8;138

6;77,000;14;128

7;82,000;13;130

8;92,000;13;143

9;69,000;12.8;126

;;;1034

;;;

[/table]

As you can clearly notice, the higher copper price is compensating for the lower gold price. Using the current gold and copper price, the total (undiscounted) revenue is just 1.5% lower compared to the base case scenario using 1300 gold and 2.18 copper.

This is a huge thing. Even though the gold price has moved down, the higher copper price is reducing the impact of this lower gold price and the total revenue will be relatively flat.

Conclusion

You shouldn’t expect the Irumafimpa deposit to throw off a substantial amount of free cash flow right away, as the mine plan estimates the mine will only start to produce in excess of 1,000 ounces of gold per month from month 5 on, but the total production rate will increase rapidly, and due to the expected higher grade and production rate in months 8-11, a large part of the gold production will be recovered in the first half of next year, which should be really good (the total gold production between months 8 and 15 is expected to be 37,400 ounces of gold).

But the real money-maker will be the Kora-deposit. Based on a relatively conservative mine life, the total revenue will be in excess of $1B, whilst the DCF8% comes in at in excess of $300M (which is in excess of C$400M). And even if we would apply the current commodity prices, the higher copper price is actually mitigating the impact from the lower copper price, which confirms the resilient economics of the Kora deposit.

At less than a dollar per share, the risk/reward ratio of K92 Mining has improved. Obviously, we are still very keen to see the company’s production results as well as the operating cost results (either per tonne or per produced ounce of gold), but the Kora PEA indicates the lower gold price shouldn’t really be a reason to be concerned, as the copper price is compensating the lower revenues from the gold sales.

Disclosure: K92 Mining is a sponsoring company, we hold a long position. Please read the disclaimer