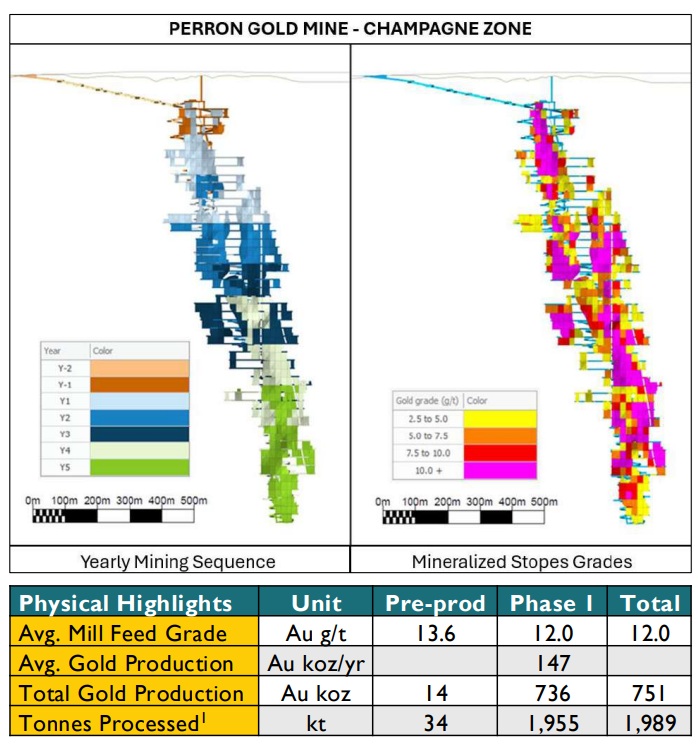

Amex Exploration (AMX.TO) has released the results of an initial feasibility study using just a portion of the potential mine life as outlined in the PEA which was published in the third quarter of last year. The feasibility takes just 2 million tonnes into account but considering the average grade exceeds 12 g/t gold and considering the feasibility study is using a toll milling scenario in its base case, the economics of this study are phenomenal.

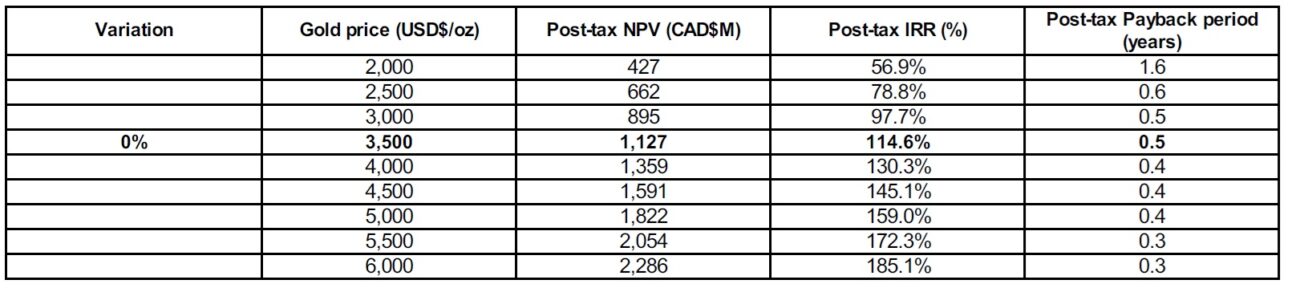

The initial capex is estimated at just under C$200M, resulting in a payback period of just six months using a gold price of US$3500/oz. This scenario consists of two years of pre-production followed by five years of commercial mining and toll milling. The mine is then expected to produce an average of 147,000 ounces of gold at an all-in sustaining cost of US$910/oz during those five years (including C$238M of sustaining capital expenditures). This results in an after-tax NPV5% of C$1.13B at $3500 gold, increasing to C$1.36% and an IRR of 130% at $4000 gold.

Although Amex has not yet entered into a definitive agreement with a mill operator, it has included a pro forma transportation cost of C$50/t in its opex calculations, which is the equivalent of a 160 kilometer trucking distance.

Disclosure: The author has no position in Amex Exploration. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read the disclaimer.