Talk is cheap and very few mining CEOs that talk the talk, can walk the walk. As we have been able to observe CEO Charles Funk in the past half decade, we can now clearly state we have rarely seen a CEO that sticks to his game plan (and executes accordingly) as he did. Under Funk’s impulse, Heliostar Metals (HSTR.V) grew out from an exploration and pre-development stage company with assets in Mexico and Alaska just three years ago, to a company that will generate about $100M in pre-tax mine site cash flow this year (assuming a gold price of $4500/oz). This will not only cover the anticipated expenses and investments this year, but will likely add to the net cash position of approximately US$41M (C$55M) as of the end of last year.

The recently announced acquisition of the Utah-based Goldstrike project will further boost the total resource base which already contained 6.3 million ounces of gold in the measured and indicated resources (inclusive of almost 2 million ounces in the calculated reserves) to 7.25 million ounces while the consolidated inferred resources will increase to 1.4 million ounces of gold. It’s almost unimaginable this company is now sitting on almost 10 million ounces of gold across the measured, indicated and inferred resource categories.

But even more importantly than sitting on a pile of gold in the ground (which doesn’t mean much if you can’t get it out), the recent acquisition efforts in the past few years were focusing on sequencing the projects. And that’s also how the purchase of the Goldstrike project should be seen, as Heliostar is assembling a portfolio of projects it can self-fund in various stages on the development curve whereby the cash flows from producing assets will be helpful to regularly bring a new asset online. Or at least, that’s the plan.

The acquisition of Goldstrike

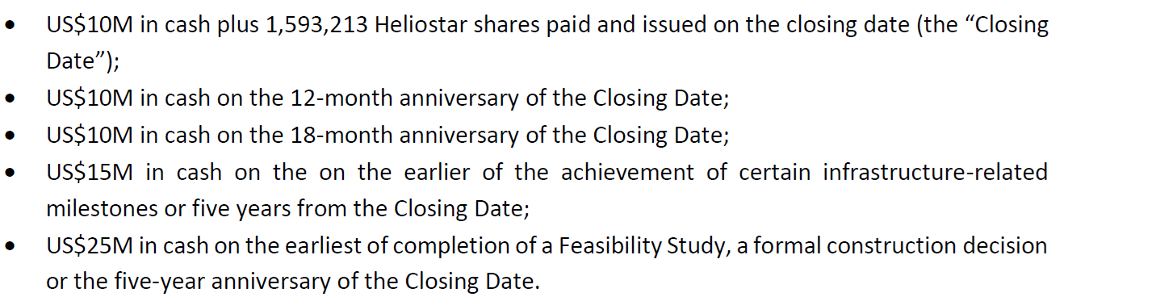

At the end of March, Heliostar announced it entered into an agreement with Liberty Gold Corp. (LGD.TO) to acquire the Goldstrike gold project in Utah from the latter. The total purchase cost will be US$72.5M with $70M in staged cash payments over the next five years, and 1.6 million common shares of Heliostar (as well as an initial $10M of the $70M in cash payments) due on the closing date.

The Goldstrike project consists of almost 5,200 hectares located in Washington County, Utah. The central block of the project consists of patented claims which are surrounded by a contiguous block of unpatented claims and land leased from the Utha School and Institutional Trust Lands Administration.

The Goldstrike project is a past producing asset that was in production as recent as the nineties. 30 years ago, ore from eleven different open pits was processed, resulting in a total production of just over 200,000 ounces of gold and a similar amount of silver. Goldstrike has been pretty dormant since and has been on the backburner at Liberty Gold (despite completing in excess of 200,000 meters of drilling) as the company’s main focus lies with the Black Pine feasibility-stage gold project in Idaho.

As part of its due diligence process, Heliostar had access to all historical data, and this allowed the company to immediately publish an updated resource calculation for Goldstrike. As indicated below, the project hosts 1.07 million ounces of gold across all categories, with in excess of 90% of the ounces hosted in the indicated resource category. The average grade of that indicated resource is 0.46 g/t gold.

Perhaps important to keep in the back of your mind as additional color: the resource calculation was based on a gold price of $2000/oz.

Heliostar Metals also highlighted the Antimony Ridge prospect, that’s part of the Goldstrike project. That ridge is an area with historical antimony production (historical records indicate small-scale production, recovering about 10 tonnes of antimony ore), but recent rock sampling programs have confirmed the presence of widespread antimony mineralization. Over a total strike length of 450 meters, samples have returned antimony, with grades of up to 5-5.7% with some gold values.

It goes without saying Heliostar plans to continue the prospecting activities at the antimony ridge to continue to improve its understanding of what drives the mineralization and how extensive the antimony zone is. Heliostar also mentioned it is considering using special purpose vehicles to separate the gold and critical minerals streams (read: the antimony project could be spun off or JV’ed independent of the Goldstrike gold project).

The operational and financial performance

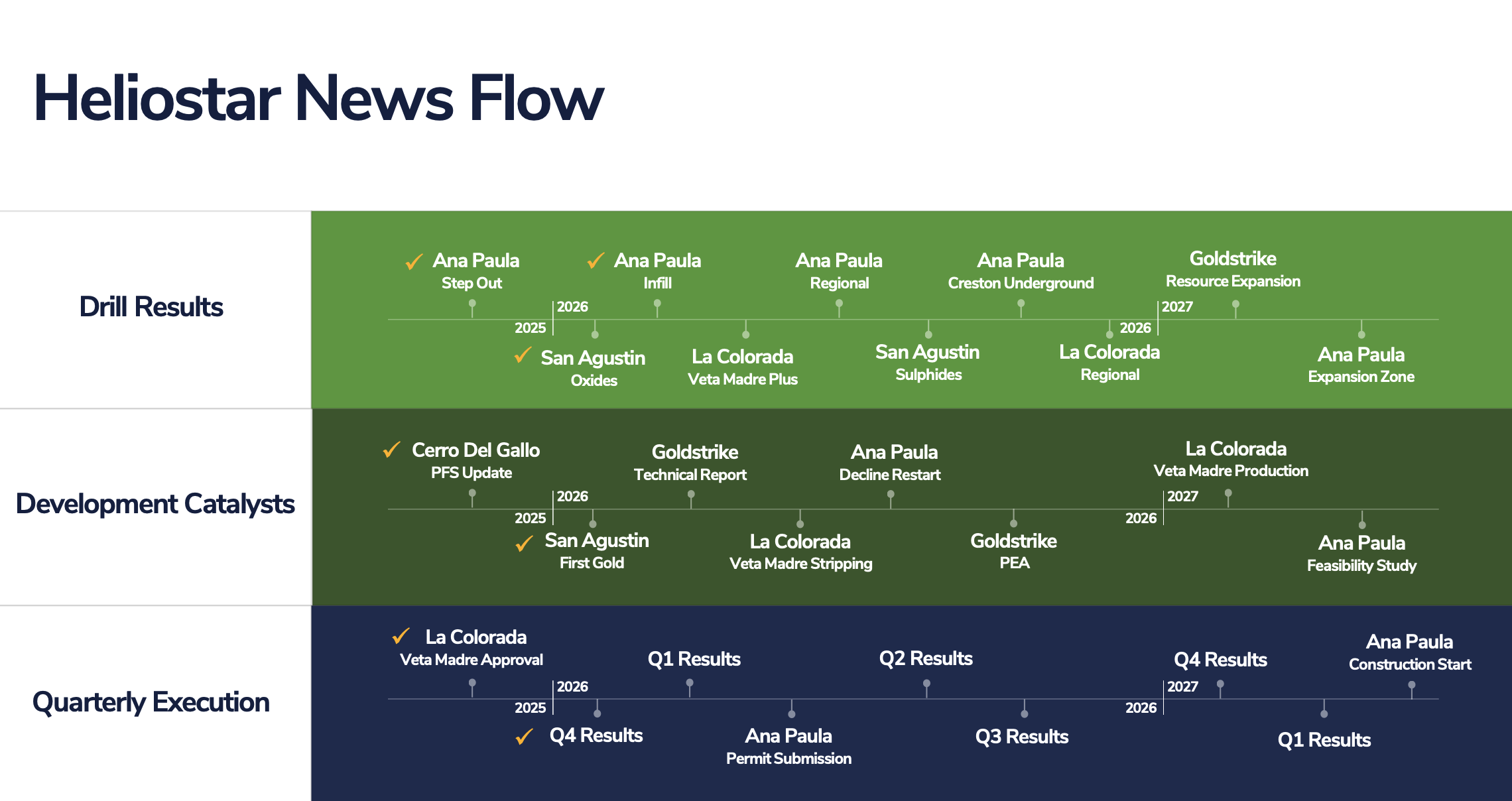

Heliostar ended 2025 on a strong note. In the final quarter of last year, the company produced just over 8,000 ounces of gold and just under 8,450 ounces of gold-equivalent. The all-in sustaining cost per gold-equivalent ounce was pretty high at $2658/oz but this was of course entirely related to the start-up of the San Agustin mine. So while it optically looks like a weaker quarter, Heliostar is firm in its commitment to reduce the consolidated AISC back to $2025-2125 per ounce this year.

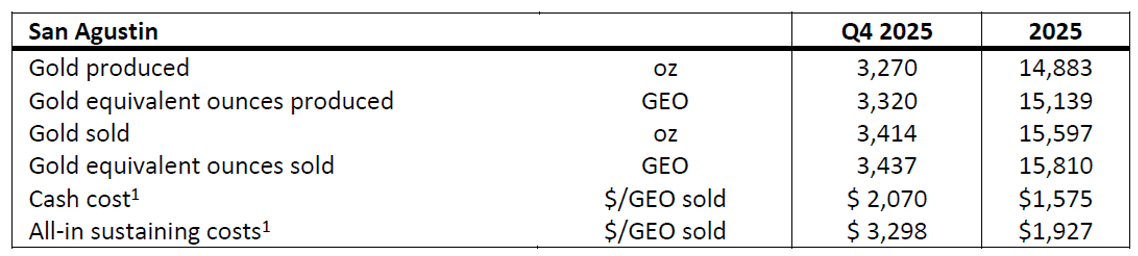

As you can see below, the San Agustin mine produced just under 3,300 ounces of gold in the final quarter of the year, and the AISC pretty much doubled from the past few quarters to almost $3,300/oz.

This does not worry us: mining operations in San Agustin were restarted in Q4 2025 (leading to higher operating expenses), but it takes some time for the additional gold production (and thus revenue) to pop up in the stats as recovering ounces from a leach pad doesn’t happen overnight. As 2026 progresses and more gold from the freshly mined areas is being recovered, the San Agustin AISC should trend down as back in the fourth quarter, the company incurred the additional operating expenses but did not record any incremental gold production yet.

Heliostar remains firmly committed to its 2026 guidance as the company expects to produce 50,000-55,000 ounces of gold and a handful ounces of silver at a cash cost of $1850-1950/oz and an all-in sustaining cost of $2025-2125/oz. This takes a silver price of $47.5 per ounce into account. Applying a silver price of $70/oz would reduce the AISC for the gold on a by-product basis by approximately $130/oz. In this case, the full-year AISC would come in below $2000/oz.

And with the gold price still trading firmly above $4000/oz, Heliostar should be able to lock in pre-tax mine operating cash flows of around US$100M. Not only will this help to fund the non-sustaining capex items on both La Colorada (Heliostar plans to ramp up the pre-stripping activities at Veta Madre to access higher grade rock with an average grade of just over 0.7 g/t gold in 2027) and San Agustin, it will also fully cover all anticipated investments at the Guerrero-based Ana Paula gold project.

Revisiting Ana Paula’s PEA in the current gold price environment

As you may remember, Heliostar Mining reported the results of an updated PEA on Ana Paula in December of last year.

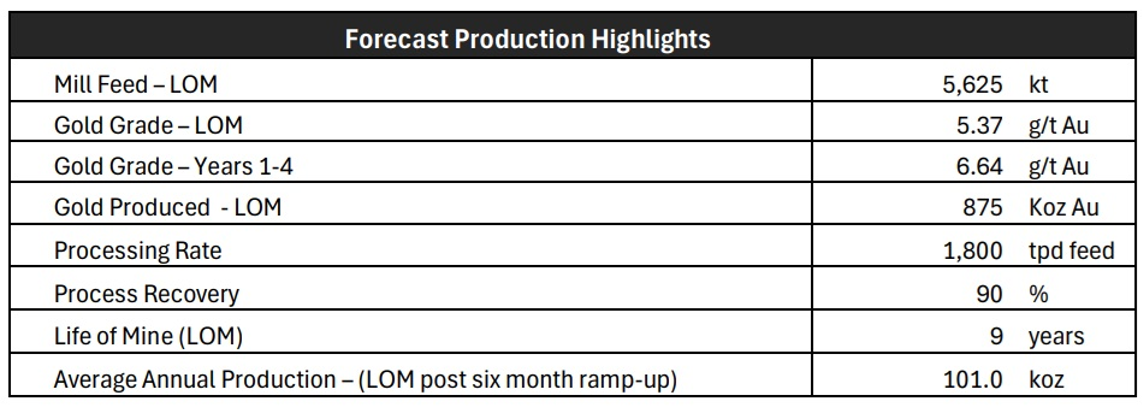

The initial capex for a 1,800 tpd operation is estimated at US$300M and given the nice grade and robust production profile of just over 100,000 ounces of gold per year, the anticipated AISC per produced and payable ounce is approximately $1011/oz. This means that at the current gold price, the net margin (on a pre-tax basis, of course) at Ana Paula would exceed $3000/oz. Years 2-4 of the mine life will be important for the mine as the average production rate in those three years will exceed 130,000 ounces per year thanks to an above-average grade of just under 7 g/t gold.

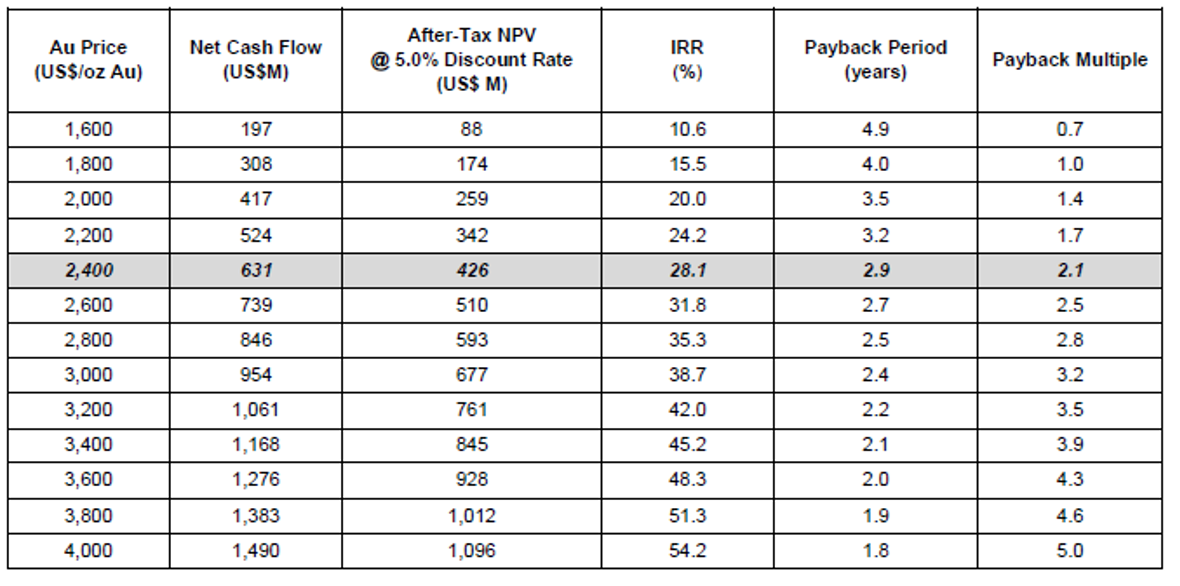

Using a base case gold price of $2400/oz, this results in an after-tax NPV5% f US$426M while at a gold price of $3800/z, the NPV jumps to just over US$1B while the IRR increases from 28.1% to 51.3% (still on an after-tax basis). At $3200 gold we are talking about a US$761M after-tax NPV5%, which represents almost C$1.1B at today’s exchange rate.

The metallurgical flow sheet indicates the importance of the BIOX plant, as that will boost the recovery rate to around 90%. That’s an improvement compared to the conventional flotation and CIL processing which would have resulted in a much lower recovery rate. This means the $46M in additional capex to build the BIOX plant likely has a payback period of less than a year given the substantial increase in gold recovery versus the higher upfront capex.

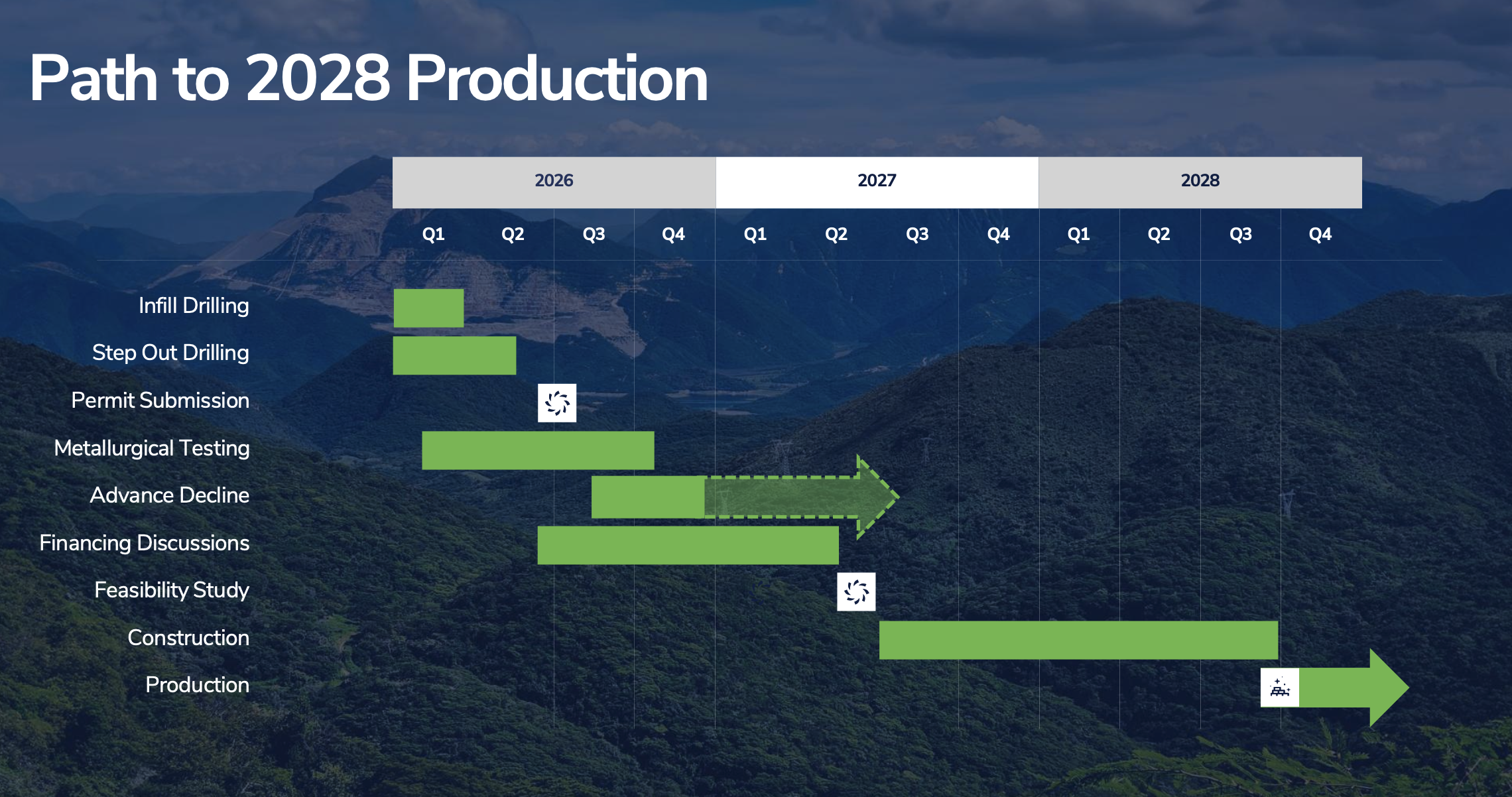

Activities at Ana Paula this year will focus on completing the underground decline, which will be advanced again in the second half of this year. Heliostar is budgeting US$15M for this pre-development expenditure which will allow the company to have immediate and direct access to the high-grade underground mineralization if and when a construction decision will be made. Additionally, completing the decline (which is already 412 meters long) will provide Heliostar with an excellent possibility to establish an underground drilling platform to continue to explore the mineralized structures of Ana Paula down-dip. Drilling from an underground platform will be more efficient (and thus cheaper) compared to a surface drill program, especially when deeper zones are to be drill-tested.

And while the decline will be further advanced towards the high-grade underground zone, Heliostar will continue to work on the feasibility study at Ana Paula. After seeing the positive results of the PEA, Heliostar is skipping the pre-feasibility study (most of the engineering work was already on a PFS-level and the sole reason the recent technical report was a PEA was caused by the all-inferred resource estimate) and is moving straight towards feasibility. That makes sense, as the company has to make hay while the sun shines. And the incoming cash flow from San Agustin and Cerro Colorado will allow Heliostar to start putting down deposits on long-lead items for Ana Paula.

The results of the Cerro de Gallo pre-feasibility study

The fourth quarter of 2025 was busy for Heliostar as the company also published the results of the pre-feasibility study on its Cerro del Gallo project in Mexico.

With an initial capex of just US$195M, Heliostar expects to produce just over 1.3 million ounces gold-equivalent over a 15 year mine life for an average output of just under 86,000 gold-equivalent ounces per year. In the first five years of the mine life, the production will be higher at approximately 94,000 ounces. Interestingly, the all-in sustaining cost is expected to be just under $1400/oz on a co-product basis, so at the current gold price of around $4500/oz, the net pre-tax margin on Cerro del Gallo mineralization would exceed $3000/oz.

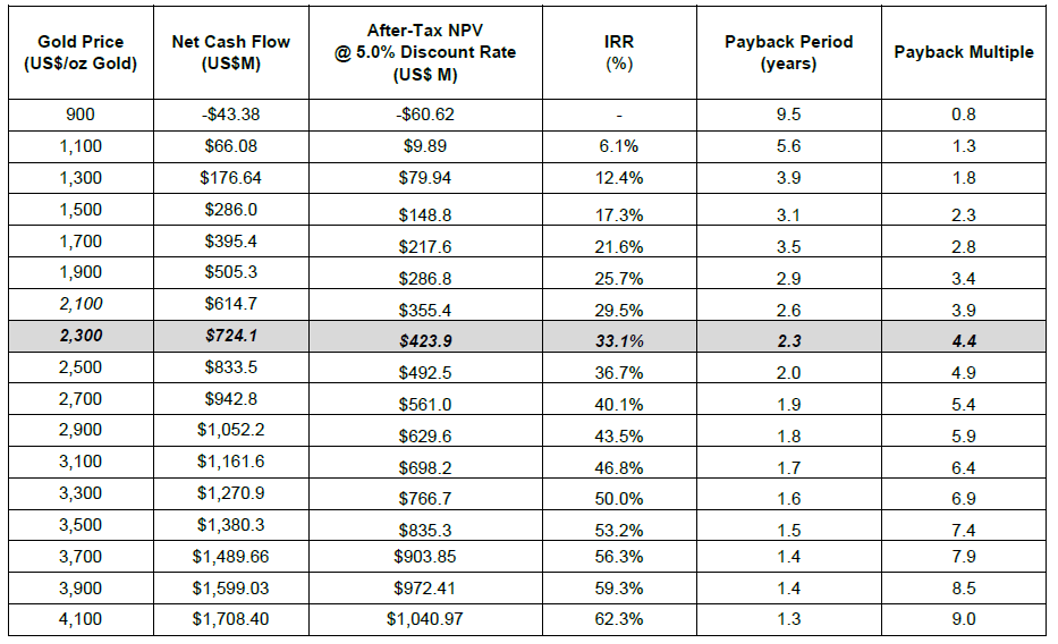

Although most developers and producers are using a gold price in the high-$2000 or low-$3000 range for their studies, Heliostar used a base case gold price of $2300/oz (show-offs!) resulting in an after-tax IRR of 33.1% and an NPV5% of US$424M (approximately C$575M using the current exchange rate). As always, Heliostar published an extensive sensitivity table for Cerro del Gallo as well, so an investor can just pick their preferred long-term gold price (up to a maximum of $4100/oz) and immediately see the NPV and IRR.

The economics of Cerro del Gallo in Heliostar’s mining scenario and economic scenario are strong. The after-tax stays above 20% even at $1700 gold and at that gold price the project will generate almost $400M in cash flow and offers an after-tax NPV5% of $218M. This is one of the rare projects that would still work at $2000 gold (and slightly below $2000 gold).

On the other hand, the upside potential is clearly shown in the table as well. At $3500 gold, the NPV jumps to $835M with an after-tax IRR of 53%. And although not shown in the sensitivity analysis, at $4500 gold, the Cerro del Gallo project likely sports an after-tax NPV5% of around US$1.2B (or in excess of C$1.6B at the current exchange rate).

There’s also upside at Cerro del Gallo as there are opportunities to further improve the economics. Some of the oxide-hosted ounces were excluded from the mine plan due to the lack of metallurgical data. Completing an additional round of met work could bring these ounces into the mine plan. A second important element would be to sign additional land access agreements as this would result in greater flexibility (moving the leach pad and waste dump further away from the pit could allow for a larger pit and adding a few hundred thousand ounces of gold to the mine plan).

So while the pre-feasibility study at Cerro del Gallo provides a very useful look under the hood, there appears to be more value that could be unlocked in the near future.

Conclusion

There has rarely been a company that was able to capitalize on aligning stars as well as Heliostar Metals. While CEO Charles Funk will be the first to admit that the booming gold price provides a very strong tailwind to support the operational assets while making the lives of the technical teams on the development projects easier, seeing how Heliostar was built out to the company it is right now can not solely be attributed to ‘luck’.

The methodological approach and the somewhat surgical precision to secure assets and sequence them into a company-wide growth plan requires skills. The Goldstrike project wasn’t just purchased on a wimp. It’s the type of asset Heliostar excels at in bringing (back) into production: low capex ounces to get production going, and using the cash flow to accelerate the production across the portfolio.

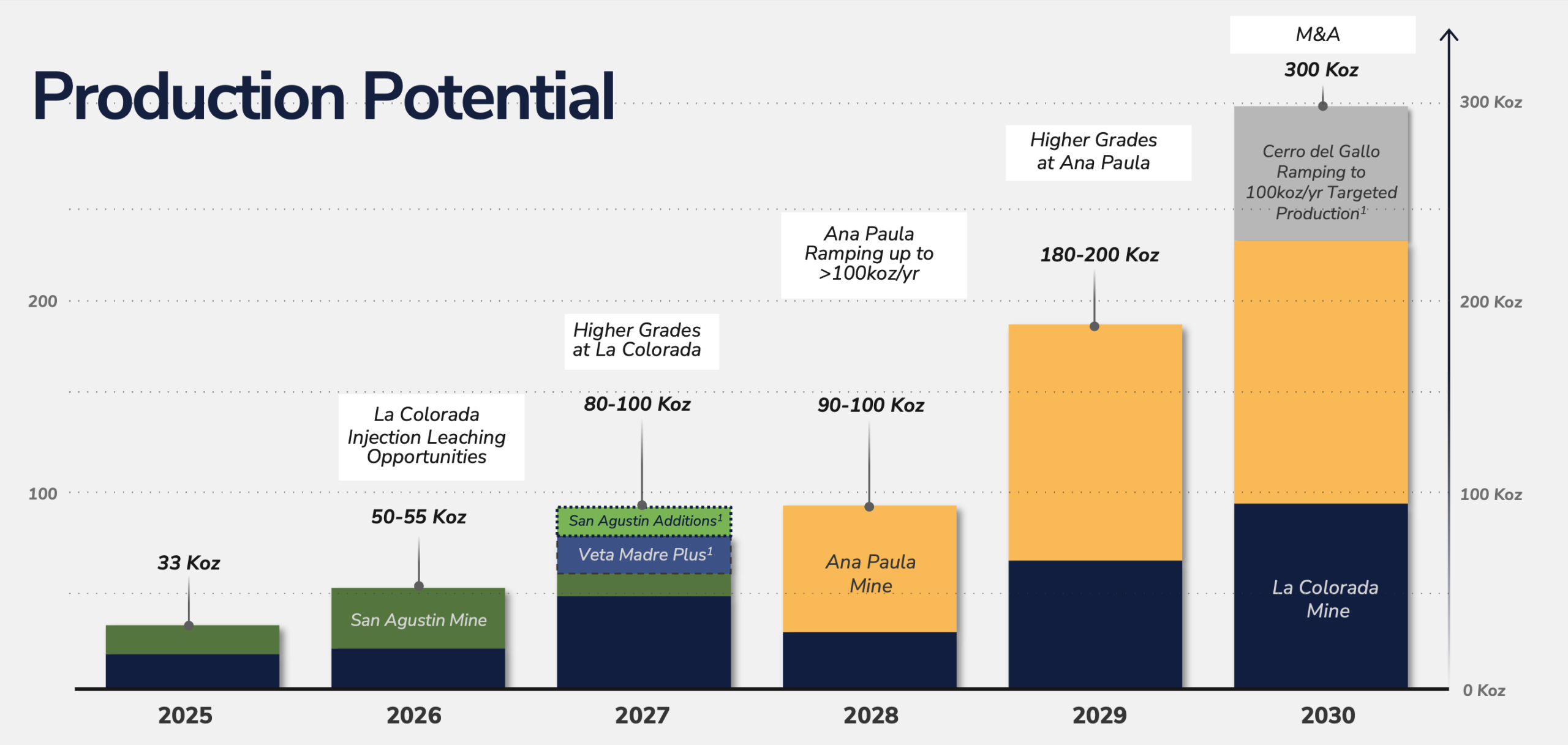

Starting out with La Colorada and now adding San Agustin to the mix, Heliostar will generate about US$100M this year in pre-tax mine site net cash flow and this will take care of all the plans and budgets across all the projects this year.

And that’s how you build a mid-tier gold producer. Heliostar hopes to get closer to 100,000 ounces per year from next year on (on the back of higher grades at La Colorada) which could hopefully build a new floor as Ana Paula could come online in 2028. If successful, this could set the scene to effectively reach the eyed 300,000 ounces per year production rate by 2030.

Disclosure: The author has a small long position in Heliostar Metals. Heliostar Metals is a sponsor of the website. This post is for educational purposes only; be mindful investing in junior mining stocks is risky and you may lose your entire investment if things go wrong. Please read our full disclosure.