We have been following Lupaka Gold (LPK.V) for several years now as the company has two very nice horses in its stable; Invicta (the near-term production asset) and Crucero (the 2Moz+ exploration asset) in Peru. As you can (and should) expect from a small mining and exploration company, Lupaka is now prioritizing the Invicta mine towards production which would cover Lupaka’s overhead expenses and maybe add some cash to the till for exploration activities.

We met with local representatives of Lupaka Gold at our most recent trip to Peru and gained a lot of additional useful insight.

View PDF

The first batch of metallurgical test results were good, very good

A very important part of the pre-production process is obviously to determine what the mine will (and could) produce. Lupaka Gold has completed a metallurgical test program at a toll mill where it processed 342 tonnes of ore to determine what types of concentrate it would be able to produce.

The results were actually really good (and better than what we expected to see in a first test run), as the copper concentrate had an average grade of 28.8% copper, 10.9% zinc-lead, almost 3 ounces of gold as well as in excess of 30 ounces of silver per tonne of copper concentrate. That’s already pretty good for a first pass, but Lupaka was also able to optimize the flowsheet a little bit, and processed a 110 tonne lot using this improved flow sheet, and the results were pretty spectacular.

The average grade of the copper concentrate is better than what we were hoping for

The copper concentrate grade increased to in excess of 30%, whilst the average grade of the gold and silver of the copper concentrate also increased to respectively 108.4 g/t and 1109 g/t. Meanwhile, Lupaka was also able to produce a lead-concentrate (containing 31.5% lead, 2 oz/t gold and in excess of 40 ounces of silver per tonne) as well as a zinc concentrate (at an average grade of 47.7% zinc, 13 ounces of silver per tonne and almost 1 ounce of gold per tonne of concentrate). And that’s actually pretty good and the average grade of the copper concentrate is better than what we were hoping for before the test runs especially considering the average recovery rates were also pretty good (with for instance in excess of 95% of the copper being recovered).

[table caption=”342 tonne average over six days” colalign=”left|right|right|right|right|right|right|right”]

Concentrate Stream;Tonnes Con Prod;Au g/t;Ag g/t;Cu %;Pb %;Zn %; Fe %

Copper (Cu);16.1;88.0;1,032.1;28.8;6.4;4.5;25.5

Lead (Pb);8.4; 88.2;1,339.3;13.1;25.7;8.5;16.9

Zinc (Zn);3.9;49.6;692.2;8.1;2.7;37.1;11.8

[/table]

[table caption=”110 tonne attempt at optimization” colalign=”left|right|right|right|right|right|right|right”]

Concentrate Stream;Tonnes Con Prod;Au g/t;Ag g/t;Cu %;Pb %;Zn %; Fe %

Copper (Cu);5.24;108.4;1,109.4;30.1;5.8;2.6;26.6

Lead (Pb);2.46;61.5;1,294.2;10.5;31.5;7.2;15.1

Zinc (Zn);1.21;30.2;393.9;5.1;1.6;47.7;8.0

[/table]

A second metallurgical test run will focus on producing just one concentrate

The results of the first metallurgical test work were good, but Lupaka has decided to send a second batch of ore to another toll mill near Nazca, where it will work with the toll mill owner (who could also be a buyer of the concentrate) to produce one single concentrate.

That could be seen as a negative, as the average grade of the copper in that concentrate could drop to less than 25%, but this could actually turn out to be a positive catalyst.

Why?

Lupaka already knows it’s able to produce a high-grade copper concentrate, but the new metallurgical test program has commenced on request of a potential offtaker who’d be interested in buying a lower-grade copper concentrate to blend it with its own higher-grade concentrate. Additionally, the Invicta concentrate has a very low arsenic content whilst a lot of other copper concentrates in Peru have much higher values of arsenic which makes it subject to pricing penalties from copper smelters.

This could be a good thing for Lupaka Gold as it would ensure it has a buyer for its concentrate and it would avoid the penalties on for instance the lead concentrate that would be produced in the other scenario.

Of course, nothing has been decided yet, but we are looking forward to get an update on the new metallurgical test program because this request by a yet unnamed potential offtake partner could be the missing piece of the puzzle for Lupaka Gold.

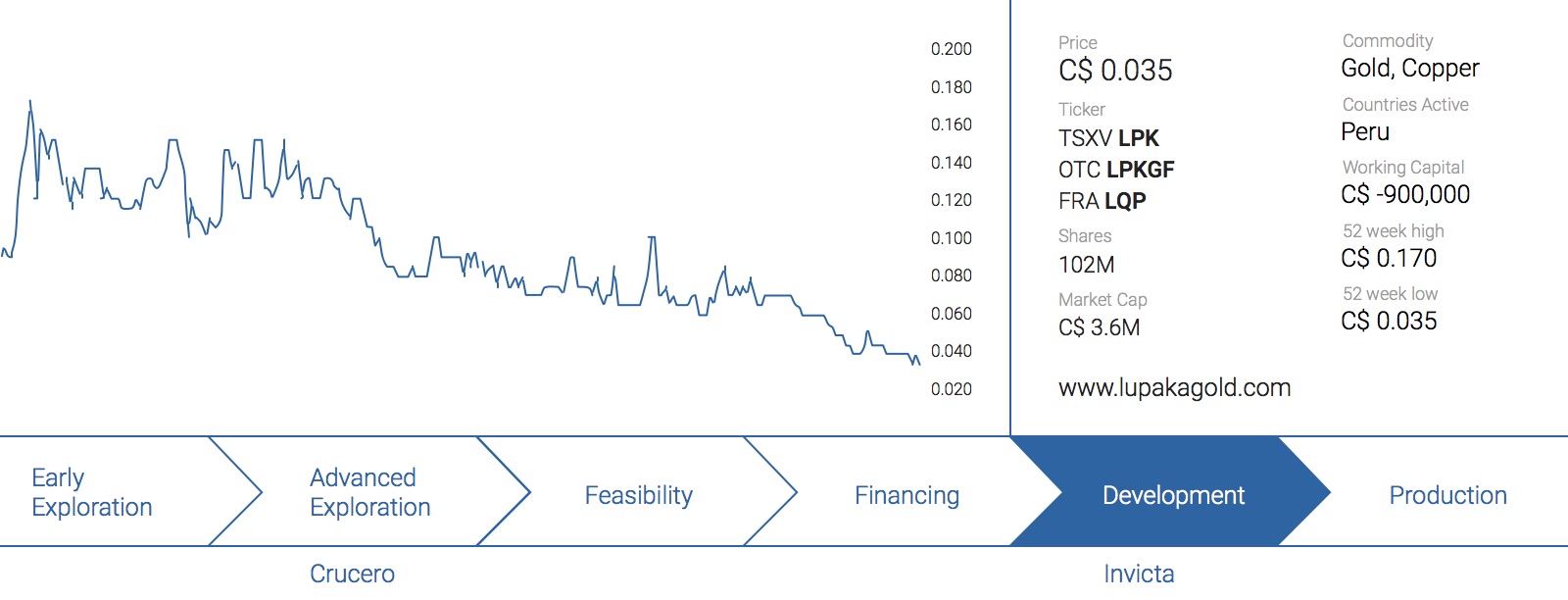

Lupaka’s financial situation

Lupaka had a negative working capital position of C$1.1M as of at the end of June, and as the cash position fell to just C$43,000 so something had to be done and the company raised C$602,000 in a private placement by issuing 8.6 million units consisting of one share and a full warrant expiring three years after closing the placement. Each unit was priced at C$0.07 (55% higher than the current share price).

This solved the immediate cash problem, but the working capital deficit remains and Lupaka will have to try to fill the gap in the next few months, one way or another. That’s probably what’s holding the market back as well and we would expect the share price to recover immediately should Lupaka be able to announce a non-dilutive financing (for instance a pre-paid copper concentrate offtake agreement) or a ‘creative’ financing like a streaming deal. Unrelated to Lupaka, we have heard there are some players in the market looking to purchase base metal streams, and we hope this could be a viable solution for Lupaka Gold.

The working capital deficit remains and Lupaka will have to try to fill the gap in the next few months

Conclusion

Lupaka’s metallurgical test results were excellent and it’s encouraging to hear the company has some irons in the fire to further customize the characteristics of its concentrates to please the potential customers.

The company is making excellent progress at Invicta but definitely hasn’t escaped from the general ‘malaise’ hitting the commodity markets, and we hope Lupaka is able to continue its development activities at Invicta in 2016.

Disclosure: The author holds a long position in Lupaka Gold. Lupaka is a sponsor of the website. Please see our disclaimer.

Good day Caesars Report,

Thank you for the write-up on Lupaka. I am just conducting some D.D.

When do you expect an update from Lupaka on the new metallurgical test program?

Thank you in advance for your respon

Hi Andrew,

We are expecting to see something in the next few days/weeks!