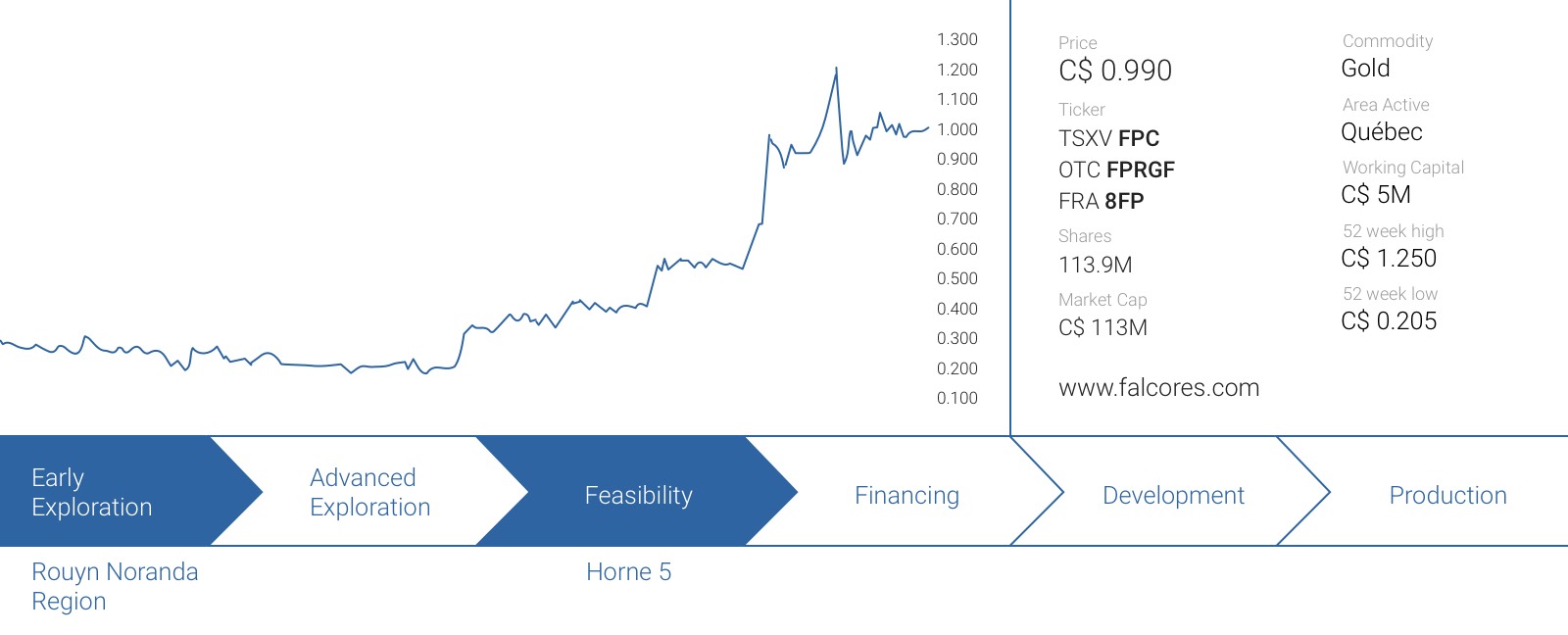

Preliminary Economic Assessments exist in all shapes and forms and definitely haven’t been created equal. When we first talked to the Falco Resources (FPC.V) management team, it became quite obvious the new management team (ex-Osisko people) wanted to advance this project as fast as possible, but they also wanted to make sure the market wasn’t disappointed with the PEA. An updated resource estimate in January revealed a bump in the total resources to 6.6M gold-equivalent ounces, and we were already looking forward to see the economics of the Horne 5 project.

In this report, we are having a closer look at the full technical report filed by Falco Resources.

The background of Horne 5

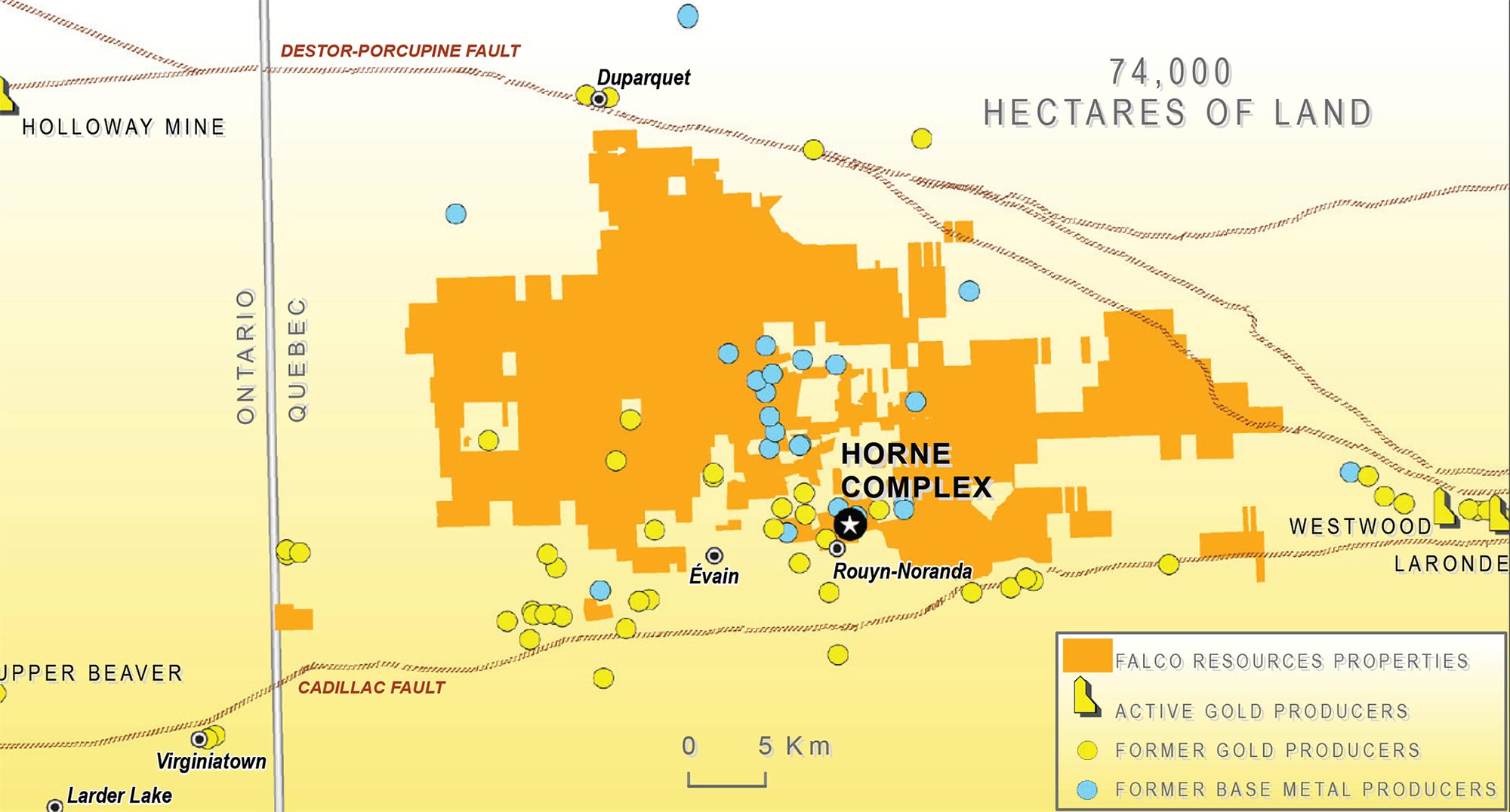

Falco’s flagship asset is the Rouyn Noranda project which is located right outside the city limits of Rouyn-Noranda in Québec, Canada. The property covers an area of almost 2,000 square kilometers, and the epicenter of project is the past-producing Horne 5 mine.

Horne 5 was a producing mine between 1926 and 1976, wherein it produced almost 12 million ounces of gold and 2.5 billion pounds of copper (as Noranda, the previous operator, was more interested in copper rather than in gold back then). As the mining operations were suspended approximately 40 years ago, it’s not difficult to imagine the mining methods that are currently available could allow a new owner to re-think a mine plan and go after the lower-grade and gold-rich ore (again, Noranda was only focusing on copper and chased the mineralized zones with a high average copper grade).

So, how good are the economics?

The mine plan outlined a total mine life of 12 years wherein Horne 5 will produce 3.05 million ounces of gold (of which 2.9 million ounces will be payable), as well as in excess of 800 million pounds of zinc, almost 200 million pounds of copper and close to 25 million ounces of silver. As the total revenue from by-products will be approximately US$1.8B, it’s very obvious Horne 5 should be seen as a poly-metallic mine, and the substantial amount of by-products will have a huge impact on the total operating cost of the gold, so it’s important Falco uses ‘acceptable’ prices for its by-product credits.

This does seem to be the case, as the used prices for the silver, copper and zinc are respectively $17/oz, $2.85/oz and $1/lbs. So, yes, the copper price is currently lower than what has been anticipated in the PEA, but the zinc price is pretty much trading at the used price whilst silver is currently being sold for more than $17/oz.

In the first three (full) years after commercial production has started, Falco will produce 36 million pounds of copper, 236 million pounds of zinc and in excess of 5.5 million ounces of silver. If you would apply the current spot prices to the economic model, the pre-tax cash flow would be less than $20M lower compared to the pricing used in the PEA. As Horne 5 will produce 684,000 ounces in those first three years of the mine life, the total impact of the lower by-product revenue remains limited to just $26 per ounce. That being said, should silver reach $22/oz and copper $2.50/lbs by the time the project goes into production, the actual by-product credits would come in higher than expected in the PEA.

Using the company’s base case assumptions ($1250 gold and an USD/CAD exchange rate of 1.33), the after-tax NPV5% comes in at C$667M, which is approximately US$510M. The initial capital expenditures are estimated to be C$905M (which does include C$60M in contingency) whilst the all-in sustaining cost per produced ounce of gold will be just US$427 which definitely puts the Horne 5 mine in the lowest quartile of gold producers (thanks to the by-product revenue). This means that at the current gold price of in excess of $1300/oz, the operating margin will be almost $900/oz, and that’s very comfortable.

The numbers aren’t the best in the world, but you know they will hold up

Even though Falco is a sponsor of the website, we always stay honest. An after-tax IRR of 16% using $1250 gold isn’t exciting it all, and didn’t meet our threshold of an internal return of 20%. At first, we weren’t too impressed and we flew to Montréal to have a chat with Vincent Metcalfe, Falco’s CFO to get some more background on this PEA.

And we’re glad we had that conversation as we left Québec with a better understanding of the PEA, and more important, the quality standards that were used in this PEA. Officially, the accuracy of the PEA is -20% and +25%, but CEO Luc Lessard thinks the ‘real’ accuracy rate of the PEA is as good as a pre-feasibility or feasibility study at -10% /+10%. Practically all capital costs and operating costs were based on quotes received from contractors and are pretty reliable as Lessard wanted the PEA to be robust.

Yes, the capex of C$905M is quite high, but the financing risk is being mitigated by robust cash flows. At $1250 gold, the NPV5% is C$667 but even at $1100 gold you’d still end up with an after-tax NPV of C$451M, and the IRR would only be slightly reduced, from 16% to 12.8%. The results based on a gold price of $1000/oz haven’t been published, but our back of the envelope calculations indicate the IRR will remain a double digit percentage at that price point.

How could the PEA’s results be improved?

There are a few internal and external factors that will have a positive impact on the economics of the Preliminary Economic Assessment.

First of all, the most important external factor is the gold price. To calculate the after-tax NPV5%, Falco used a gold price of US$1250/oz. Whilst that might have seen quite optimistic a few months ago, gold is now trading at almost $1325/oz, and using $1250/oz as base case isn’t unrealistic at all. Unfortunately, the high operating margin also has a ‘negative’ impact on the NPV, as the NPV doesn’t increase as fast as a project with a smaller operating margin.

Using a gold price of US$1350/oz, the after-tax NPV5% does increase to C$804M whilst the IRR increases to 18% (which is already closer to our target of 20% on an after-tax basis).

On top of that, a higher price level for the base metals will also have an impact. $3 copper will increase the LOM pre-tax cash flows by $30M, whilst $25 silver will have a positive impact to the tune of almost $200M and $1.10 zinc will also contribute an additional $80M in cash flow. There still are a lot of moving parts here, and a lot can happen to these base metal prices in the next 4-5 years.

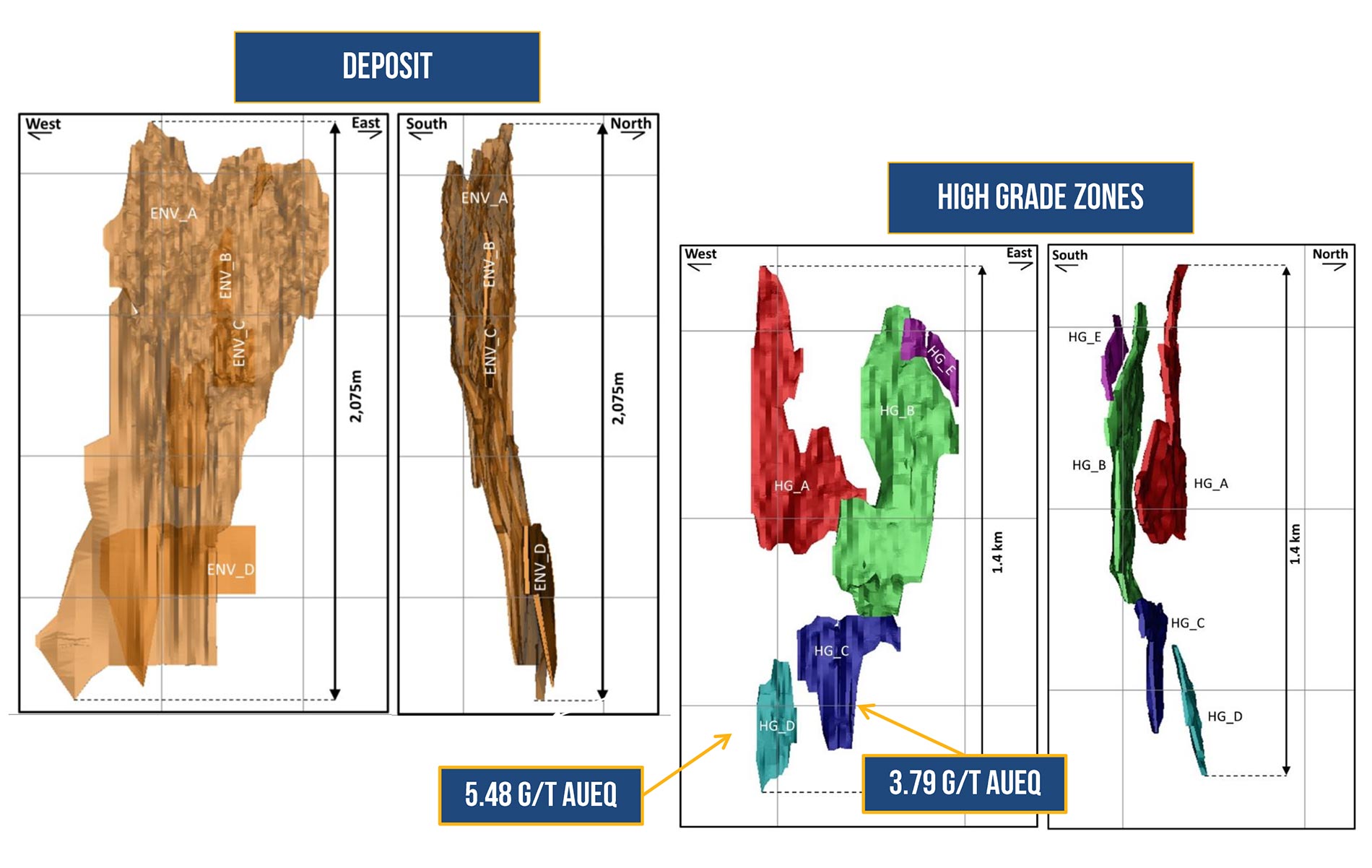

There are also is one important internal factor that could potentially boost the NPV (and IRR) of the project. As you might remember from one of the shorter articles on our website, Falco has started a 10,000 meter drill program to drill-test the Western Extension of the Horne 5 mine. This drill program is designed to follow up on precious intercepts of 45 meters at 3.4 g/t AuEq and 44 meters at 2.6 g/t AuEq.

The drill rig will test the mineralization in between the levels 17 and 33 of the Horne 5 mine, and if the Western Extension contains a sufficient amount of ore to be economic, it’s very likely any resource at the Western Extension will be included in the final mine plan. For every additional 6 million tonnes of ore, Horne 5’s mine life could be extended by an additional year, so if Falco would be able to outline a 10 million tonne resource at WE, it would produce an additional half million gold-equivalent ounces, further boosting the NPV.

Additionally, a higher-grade resource could potentially boost the cash flows in years 4,5 and 7 when the mine plan is taking some lower cash flows into consideration.

What are the next steps from here on?

The market seemed to have been betting against Falco Resources right before and right after the PEA was released. The company was indeed running low on cash (with C$1.1M in cash and a working capital deficit of C$0.4M as of at the end of the first quarter), but it’s usually not the best idea to bet against a company operated by ex-Osisko Mining employees and backed by Osisko Gold Royalties (OR.TO, OR) which has access to C$700M+ in liquidity.

As Falco is working out of the same offices as Osisko Gold Royalties, it should have been pretty clear Osisko had a pretty good idea of what was going on at Falco, and as OR is predominantly Québec-focused, it’s not too much out of line to expect Osisko helping Falco out.

And that effectively happened, as Osisko provided C$10M in cash structured as a loan for with a maturity date in 18 months and a 7% interest rate. During the term of this loan, Falco and Osisko will negotiate in good faith about a potential gold and/or silver stream. Should both companies reach an agreement, we think one of the biggest issues will have been dealt with, as it won’t be easy for a small company like Falco to fund its equity share of the capex requirement, and we think the silver production at Horne 5 might prove to be very important to fund the project.

Should both parties be unable to reach an agreement on a streaming deal, the C$10M won’t have to be repaid, but will be converted into a 1% NSR.

Conclusion

Falco’s PEA might not be the shiniest or most appealing PEA, but it’s a robust PEA that will hold up, even at a gold price of $1000/oz. And keep in mind the after-tax NPV increases to C$800M when using the current gold price.

Additionally, the Horne 5 mine will be a low-cost asset with a relatively long mine life (which could still be expanded with additional resources from for instance the Western Extension and the results from the regional exploration program), and as it’s located in a safe region, it might be an asset that could appeal to almost any mid-tier to senior mining company looking for new. The mining sector still is in a full ‘flight to safety’ mode, and the senior producers are trying to find large assets in First Tier mining jurisdictions such as Canada. The amount of projects that could produce in excess of 200,000 ounces of gold per year can be counted on one hand, so Falco Resources is very likely already popping up on several radar screens.

We told you before CEO Luc Lessard is determined to build the Horne 5 mine, and we have very little doubt he will be able to do so. The permitting process should be pretty straightforward (Falco thinks it will need 18 months to permit the Horne 5 mine, but we’d like to point out the similar permitting process for Canadian Malartic took just 14 months), and with Osisko Gold Royalties as its main financial backer, we’re also quite confident there will be an acceptable solution on the table to fund the C$905M initial capex. With gold trading at $1325/oz, the fun times have barely started.

Disclosure: Falco Resources is a sponsoring company, we have a long position.