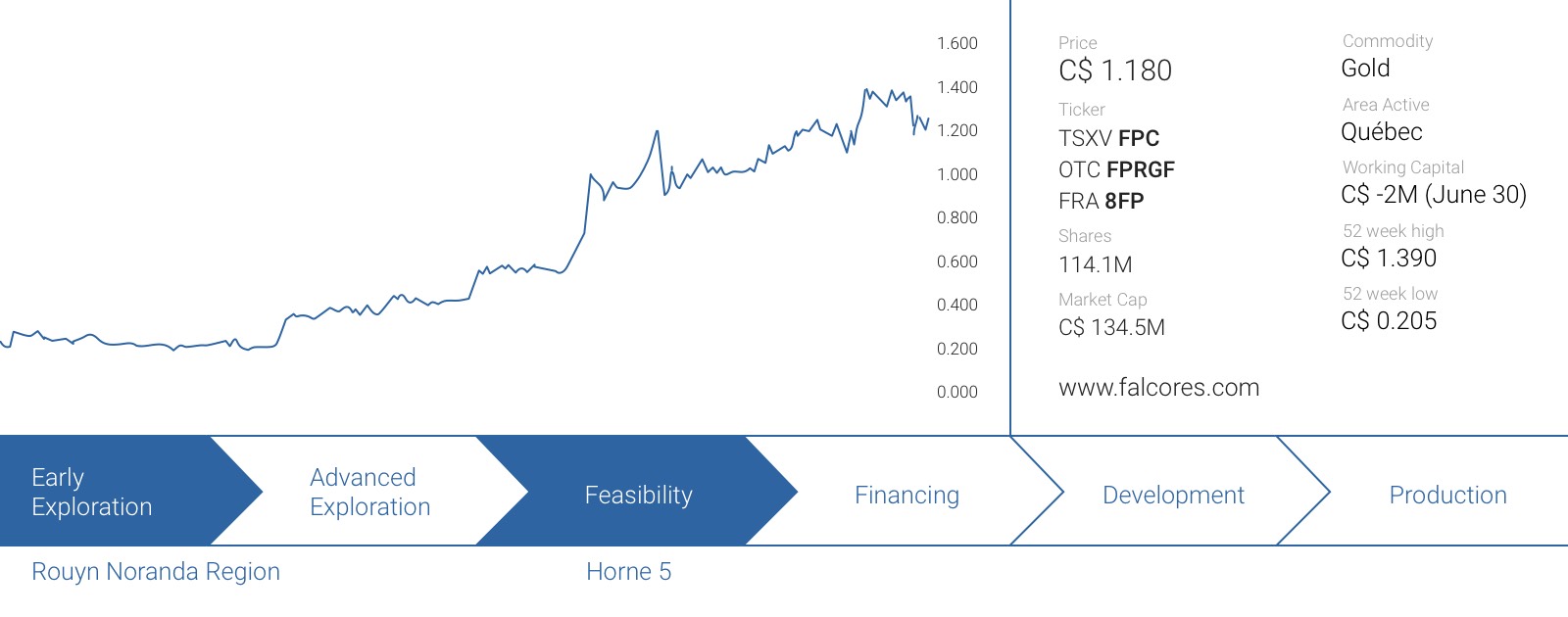

It has already been a great year for Falco Resources (FPC.V) so far as the company’s share price has tripled since we published our first report. Meanwhile, Falco has continued to work on the Horne 5 Deposit, released a positive Preliminary Economic Assessment (which we already discussed in a previous report), and recently retained full ownership of the Horne 5 project whilst drilling 10,000 meters on the Horne 5 Western Expansion which could increase the value of the project.

We told you not to bet against this team!

The market wasn’t stupid and has been expecting a relatively high capex, and these expectations were confirmed in the PEA as the company’s consultants estimated the initial capex at C$905M (including contingency). The required initial investment was a bit higher than expected though as Falco’s base case scenario used a higher average daily throughput to unlock additional economies of scale.

It’s normal for the market to be wary of high-capex projects, but we already said on Day 1 Falco Resources isn’t like any other company. Whereas most smaller companies would indeed face severe dilution, Falco Resources enjoys the benefits of having excellent ties with Osisko Gold Royalties (OR.TO), and we told you it wouldn’t be the smartest idea to bet against this management team being backed by some serious players on the Québec playing field.

And indeed, Osisko GR stepped up the plate and when Falco’s treasury was running on fumes, both companies reached an agreement whereby Osisko Gold Royalties provided Falco with a C$10M loan, which will be used to continue to work on the Horne 5 project.

This loan will mature in 18 months and will bear an interest rate of 7% which will be compounded on a quarterly basis, and the interest expenses will only be payable on the maturity date of the loan (November 30, 2017). Of course, Osisko couldn’t care less about making a million in interest payments on the loan, and the real reason why it entered in this loan agreement with Falco Resources was to initiate preliminary discussions about a potential gold/silver royalty/stream with the company.

We have very little doubt the companies will come to an agreement (after all, they share the same office floor), so it will be very interesting to see how a potential deal will be structured, and if a win-win situation could be created. In fact, according to our own interpretation of the loan agreement, Falco seems to be in the best position here because whether or not an agreement could be reached, Falco doesn’t have to repay the loan.

Should a deal be reached, the C$10M (+ applicable interest payments) will be deducted from the negotiated upfront payment associated with a streaming deal or a royalty sale. But even if no deal has been reached by November 30 next year, Falco doesn’t have to repay the C$10M, as the total amount will be converted into a 1% NSR, indicating Osisko Gold Royalties seems to be happy to value the total cash flows expected at Horne 5 at C$1B.

Falco Resources has now secured 100% ownership of the asset

Falco now also owns 100% of Horne 5 after Glencore (GLEN.L) elected not to exercise its back-in right, which means Glencore is falling back to ‘just’ a 2% NSR on all the metals produced at Horne 5.

That’s not really surprising considering Glencore has been slowly falling back to its core business, processing and trading metals, and retaining its ROFR (Right Of First Refusal) to either process the Horne 5 ore, or to purchase the concentrate.

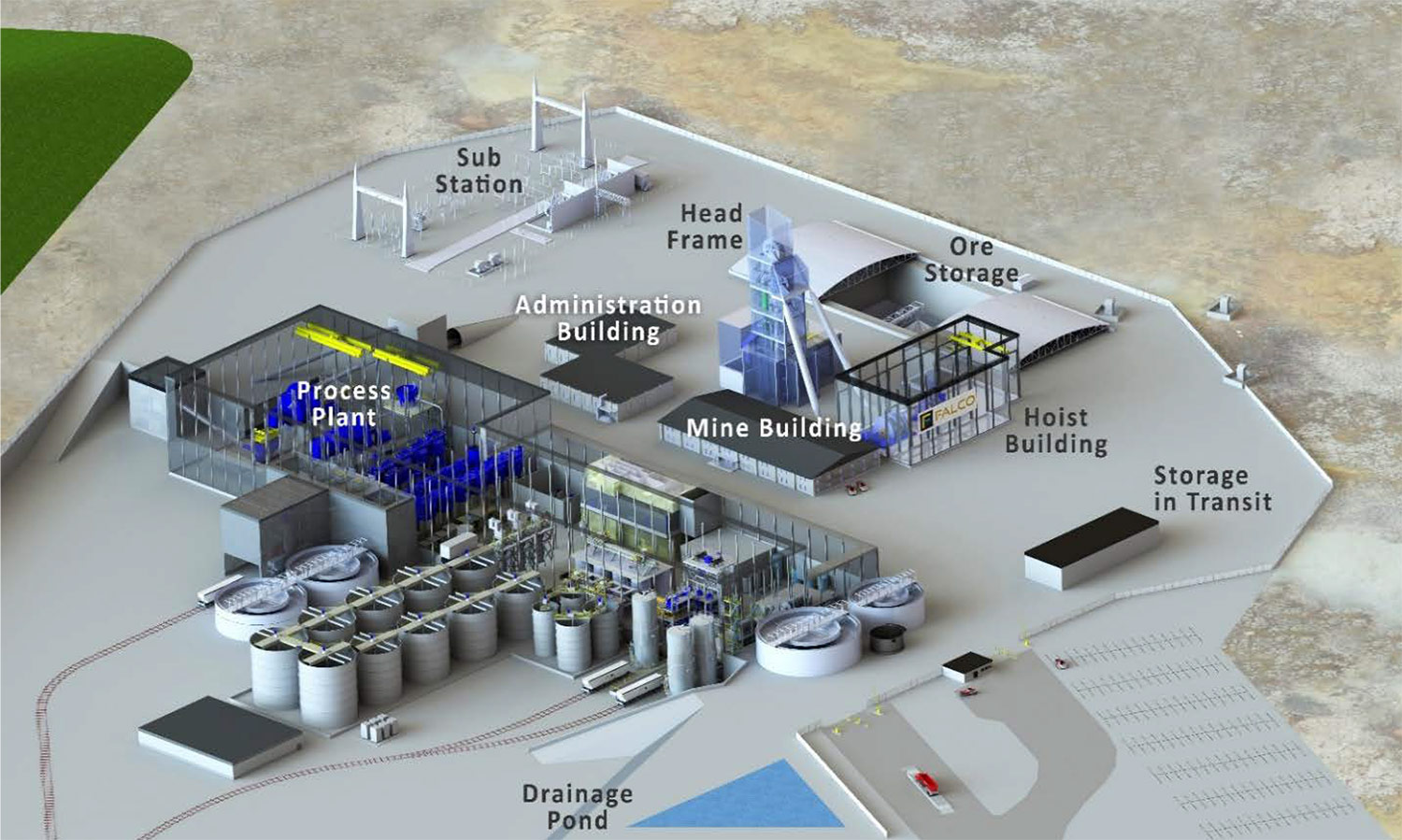

It would actually be very interesting to see a toll processing proposal by Glencore. Yes, the operating expenses would increase (Falco budgeted a processing cost of C$20.63/t), but should Falco be able to use existing Glencore facilities (on the condition Glencore can guarantee a sufficient capacity allocation), it could reduce the initial capex by several C$352M (which is the expected cost associated with the construction of a stand-alone Horne 5 process plant). But of course, as long as no such scenario has been put on the table, we will consider the current development plan to be the ‘base case’ scenario.

The exploration program yields the expected results – and confirms the Western Extension potential

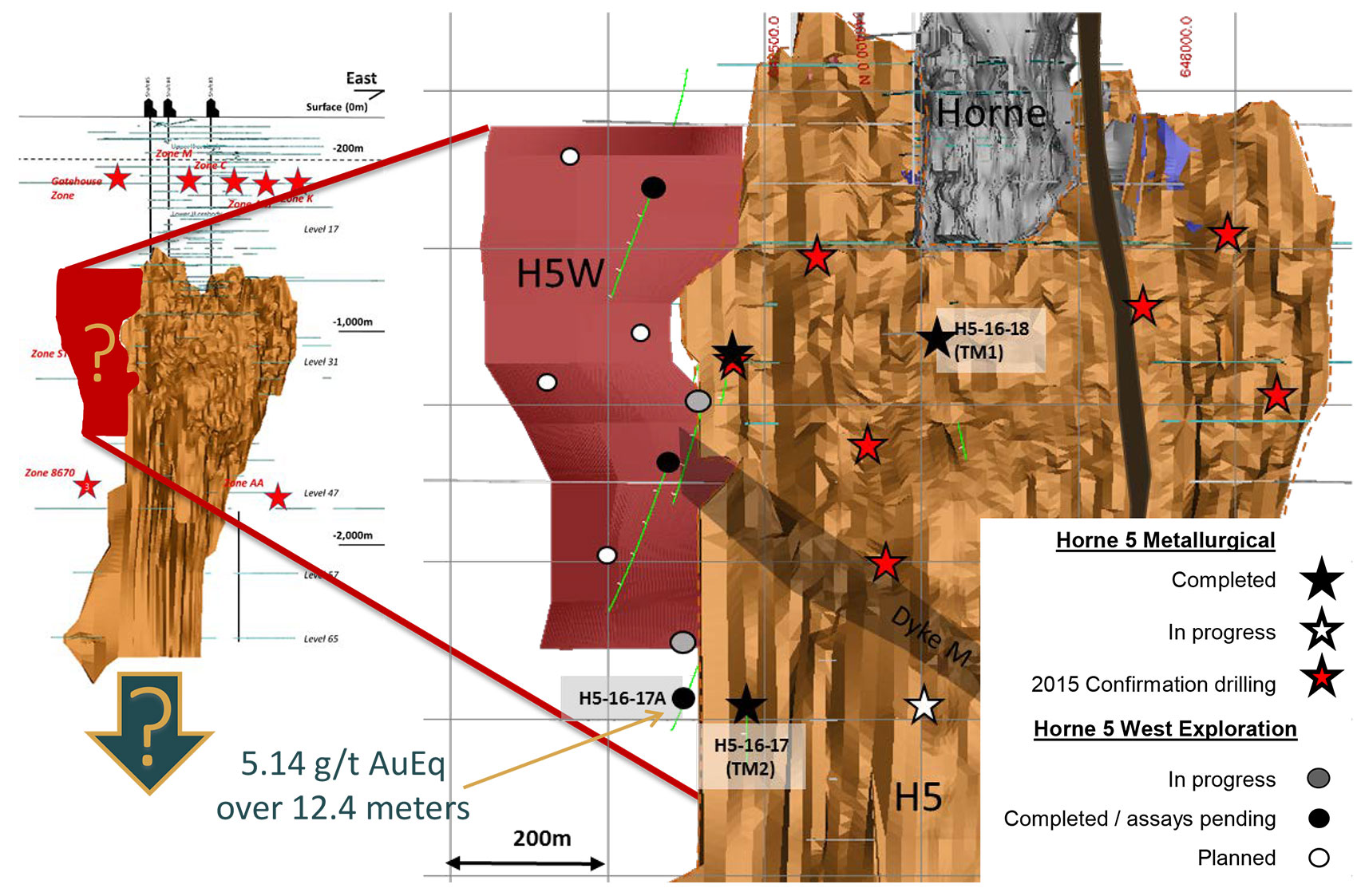

Back in April, the company directed two drill rigs to the Horne 5 deposit to complete an additional 20,000 meters of drilling with a special focus on the Quemont extension and Western Extension. We were very interested to see assay results from the Western Extension as this program was specifically designed to follow up on previous drill results of 44 meters containing 2.6 g/t AuEq and 45 meters at 3.4 g/t AuEq.

Falco’s plan was to drill two wedges from an existing (deep) pilot hole to drill an additional 3 pilot holes and 4 wedges. As the drill bit was supposed to go deep (Falco wanted to drill test the rocks between the levels 17 and 33), we weren’t too surprised we had to wait until September to see the first assay result from the Western Extension zone.

And we weren’t disappointed with the first hole, as the drill bit encountered 12.4 meters containing 3.01 g/t gold, in excess of 1.5 ounces of silver per tonne of rock as well as 0.29% copper and 1.77% Zinc, resulting in a gold-equivalent grade of 5.14 g/t. This interval does confirm the existence of mineralized zones with a similar grade (or even a higher grade) and thickness in the Western Extension zone, and as you can see on the next image, this mineralization was intercepted outside of the current resource outline of the Horne 5 deposit.

This does validate our thesis the Western Extension could be very valuable for Falco Resources as it could allow the company to A) extend the mine life (and increase the NPV of the project) and B) blend ore from the Western Extension with the ore from the ‘main’ deposit to create a consistent mill feed to maximize the performance of the processing plant.

A new resource update

We were expecting Falco Resources to update its resource estimate to take a different cutoff grade into consideration, but we were positively surprised the company was already able to release the update on the very first trading day of the fourth quarter.

As expected, there’s a substantial increase in the total amount of gold-equivalent ounces in the resource, as the total measured and indicated resources now contain almost 7.1 million gold-equivalent ounces (of which almost 4.6 million ounces pure gold) at an average grade of 2.41 g/t AuEq, whilst an additional 1.7 million gold-equivalent ounces are part of an inferred resource estimate, using a cutoff grade based on a C$55/t rock value.

This resource estimate is based on almost 6,000 (!) diamond drill holes, for a total of almost half a million meters (which is roughly the distance from Toronto to Montréal as the crow flies), so Falco Resources now has a pretty good understanding of the mineralization which will allow the company to complete a feasibility study in the first half of 2017 (which would put it on track to have a FS before negotiating a streaming/royalty deal with Osisko Gold Royalties).

Conclusion

Falco’s efforts to increase the value of Horne 5 and to improve the economics of the mine plan are paying off. The market wasn’t convinced about Falco Resources’ capability to continue to work on the property, but the C$10M loan arrangement with Osisko Gold Royalties seems to be a good deal for Falco, as the C$10M won’t have to be repaid in cash but will be deducted from the upfront streaming payment, or converted into a 1% NSR (valuing the sum of the cash flows at C$1B) should no agreement be reached.

Meanwhile, the Western Extension could easily add half a million gold-equivalent ounces to the mine plan and it’s really great to see the first hole has confirmed our expectations. Of course, one swallow doesn’t make a summer, but we’re already looking forward to see more assay results which could perhaps already lead to an (inferred) resource estimate and allow us to calculate a more ‘tangible’ added value to the entire Horne 5 project.

Disclosure: Falco Resources is a sponsoring company, we have a long position.